Quick Answer

The best way to teach kids about money is to run a simple weekly system they can repeat, not a one-time lecture. Use a short family check-in, clear spend/save/give categories, written rules for allowance and approvals, and a lightweight ledger. Start with basics, then add friction concepts like fees and delays so kids learn how real money decisions work in everyday life.

You don't need "money talks" - you need a 20-minute weekly system your kids can run#

You don't need a grand "money talk." You need a short, repeatable system your kids can help run, especially if your household cashflow comes from client work.

Run a simple 20-minute weekly workflow to see what money came in, what money went out, and what friction showed up along the way. Stripe describes its standard pricing as pay-as-you-go, with no setup fees, monthly fees, or hidden fees, but every transaction still incurs a cost, and those costs can affect profitability.

If you freelance, create, or invoice clients, it's easy to treat processing costs as background noise until they quietly eat into net revenue. A lightweight weekly review keeps you in control, and it gives you a concrete way to show kids that timing, fees, and tradeoffs matter.

The 20-minute weekly workflow (pull → spot add-ons → summarize → decide)#

Treat this like a weekly close, not something you mean to get to later. Keep one shared note and one simple spreadsheet tab (date, amount, payment type, fees, notes).

| Segment | Minutes | What you do | Output you log |

|---|---|---|---|

| Pull | 5 | Pull a list of successful transactions for the week | Transaction count + total volume |

| Spot add-ons | 5 | Flag transactions that trigger extra fees (when applicable) | "Add-on" notes per transaction |

| Summarize | 5 | Write a plain-English summary of what drove fees this week | Top drivers + questions |

| Decide | 5 | Pick one change to test next week (if any) | One action + owner |

Fees as friction (with a real-world anchor)#

Stripe lists 2.9% + 30¢ per successful transaction for domestic cards, and it also lists additional card-payment fees of 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. The takeaway is simple: systems charge for convenience, and certain transaction types can add incremental costs.

| Payment item | Listed pricing |

|---|---|

| Domestic cards | 2.9% + 30¢ per successful transaction |

| Manually entered cards | Additional 0.5% |

| International cards | Additional 1.5% |

| If currency conversion is required | Additional 1% |

| Instant Bank Payments | 2.6% + 30¢ per successful transaction |

| Klarna | 5.99% + 30¢ per successful transaction |

If you are evaluating payment methods beyond cards, Stripe's pricing page also shows examples like 2.6% + 30¢ per successful transaction for Instant Bank Payments and 5.99% + 30¢ per successful transaction for Klarna. The point isn't to declare one option "best." Pricing varies by method, so review what you actually used and what it cost.

Platform note (if you use Stripe Connect)#

If you are a platform using Stripe Connect, verify who actually pays which fees. Stripe describes a model where Stripe bills connected accounts for payment fees directly, and the platform does not incur additional account or per-payout fees in that model.

Selection criteria (and who this list is for - and not for)#

Use this list if you want money skills to come from ongoing, practical conversations, not a one-time lecture. The goal is a simple rhythm you can repeat in real life, especially in the moments where money decisions actually happen.

This list is for families who prefer clear routines over big speeches. If you like keeping a notes doc that captures what you decided and why, you'll feel at home here. The through-line is simple: talk, decide, repeat.

Who this is for (and why it works)#

- You want everyday money conversations, not a one-time "money talk." The secret isn't a textbook or a formal lecture. You normalize money management through small, repeatable moments.

- You want hands-on decision-making with guardrails. Kids get real chances to make choices, and you set the boundaries that keep those choices safe and age-appropriate. Autonomy builds through consistency.

- You live with variable timing and want to teach tradeoffs without drama. Narration is a practical teaching tool: talking through your own financial decisions out loud gives you a natural way to explain why you're choosing one option over another, without turning it into a stressful event.

If you delay a nonessential purchase because an invoice has not cleared yet, narrate the decision: the timing, the tradeoff, then the plan. Your kid learns planning without panic.

Not for (so you don't waste time)#

| If you want... | This list will feel like... | Better approach |

|---|---|---|

| A single inspirational principle | Work you have to repeat | Pick one family value and keep it verbal |

| A one-time "money talk" | Too operational | Do a one-off conversation, then stop |

| Zero tracking or rules | Annoying accountability | Keep money private and unstructured |

How we picked these methods: every tactic has to support simple, everyday conversations, not formal lectures, and it should help you talk through real choices as they come up. It also needs to be practical enough to use in normal life, not just in "teaching mode."

If you like the "risk signals" mindset from payments ops, you might also enjoy A Guide to Stripe Radar for Fraud Protection.

What should kids learn first: spending, saving, giving - or investing?#

Start with everyday money basics, then teach fees and friction early. Save higher-variance money moves for later. The goal is an order of operations that keeps things understandable and reduces surprises.

"Buckets before bets" is a useful mental model. Build repeatable habits before you add concepts where outcomes swing more.

A simple "buckets before bets" sequence (optional)#

If it helps, run a simple weekly routine with a few categories (for example: Spend / Save / Give), using jars, envelopes, or a notes doc plus a simple ledger line.

Then add a "friction" step before purchases and payouts: a quick check for what it will actually cost and how long it will take.

Here's a progression you can actually run. It stays simple and gives you a clear "policy gate" for moving forward.

| Stage | What you teach first | "Policy gate" to advance |

|---|---|---|

| Buckets | Basic categories (e.g., spend, save, give) | Allocates weekly without reminders |

| Friction | Fees, delays, approvals | Predicts total cost before buying |

| Next (optional) | More complex, higher-variance decisions | Asks questions before acting |

Teach fees and friction early (because every transaction costs something)#

Teach fees as friction that shrinks your options. Stripe notes that every transaction incurs a cost, and payment gateway fees can affect how much a business pays to accept payments. For example, Stripe lists 2.9% + 30¢ per successful transaction for domestic cards. It also lists add-ons like 1.5% for international cards, 1% if currency conversion is required, and 0.5% for manually entered cards. Those line items land with kids when you translate them into one rule: moving money is not free, so you plan before you click.

If you run side hustles or pay allowances digitally, point out payout friction too. Stripe Connect lists 0.25% + 25¢ per payout sent, plus $2 per monthly active account in certain setups. (Stripe defines an account as active in any month payouts are sent to its bank account or debit card.) That gives you a concrete way to show why "getting paid" and "getting your money out" can both involve costs.

Hypothetical scenario: your kid wants to buy something in-app. Instead of debating the item, ask them to estimate the all-in cost first, including any fees that might apply. You model controls, not fear.

Should kids get an allowance - and what policy actually works?#

There is no one "right" allowance policy for every family. If you do run an allowance, it usually goes more smoothly when you treat it like a repeatable routine with clear expectations and a simple record you can check.

If you want fewer renegotiations, jot your "house rules" down somewhere shared (notes app, printed page, fridge). It does not need to be formal. You're just creating shared expectations and a place to track exceptions.

You might note:

- Cadence: when money shows up (weekly, biweekly, monthly).

- What it covers vs. doesn't: snacks, toys, apps, gifts, outings.

- What happens when it's gone: wait, earn, or reallocate.

- How you log it: a simple line-item record (date, amount, note).

Pick an allowance model that matches your reality#

If you are choosing a structure, here are a few patterns people use. None is automatically "best," but each teaches something different.

| Model | How it feels to a kid | Good fit if you want | Built-in lesson |

|---|---|---|---|

| Salary | Predictable payday | Predictability | Planning |

| Commission | Money follows completed work | A tighter link between work and pay | Prioritization |

| Hybrid | Base plus bonuses | Stability plus incentives | Tradeoffs |

If you pay digitally, it is also worth remembering that "friction" can be real. For example, Stripe lists 2.9% + 30¢ per successful transaction for domestic cards, with additional fees of 0.5% for manually entered cards, 1.5% for international cards, and 1% if currency conversion is required. And for payouts in Stripe Connect (when you handle pricing for your users), Stripe lists 0.25% + 25¢ per payout sent and $2 per monthly active account.

Set spend permissions and recurring-charge controls (simple, not dramatic)#

Some families use simple "permissions" to reduce surprises, especially with digital purchases. Recurring charges, in particular, are easy to miss compared with a one-time buy.

Example scenario: a kid wants an app add-on that also offers a subscription. You pause to confirm whether it repeats, then decide together how, or whether, subscriptions are allowed in your house.

How do you run a 20-minute weekly family money meeting that actually sticks?#

Keep it consistent: pick one day each week, set a timer for 15-20 minutes, and run the same simple check-in every time. Consistency beats complexity: a weekly 15-20 minute money meeting works.

Use a simple repeatable agenda (and end with what happens next)#

Set a timer for 15-20 minutes and keep the flow tight. You do not need anything fancy, just the same few beats each week:

| Agenda item | What to review |

|---|---|

| What came in | Allowance, gifts, odd jobs |

| What went out | The spending since last time |

| What the plan is now | Decide how you want to split money across your priorities (for example, spending vs saving vs giving) |

| What you are doing next | Any decisions to make and anything to follow up on before the next meeting |

Run it in that order each week, then write down what happens next before you stop.

Operator rule: no lecturing during close. Log, decide, move on. If you keep decisions traceable, nobody has to argue from memory. That is the audit-trail mindset you want in any money workflow.

Build a "family ledger lite" (keep it minimal, but written down)#

Teach that budgeting is money planning, and that a budget is simply a plan to track income and expenses (money coming in and money going out).

To make it real, keep one shared place where you write down the basics each week, like:

- what happened (a short note)

- whether it was money in or money out

- a simple category you all recognize

The point is not perfect bookkeeping. It's building the habit of tracking what came in, what went out, and what that means for the next week.

If you want a quick next step, you can also try the free invoice generator.

The best ways to teach your kids about money (risk-first, age-banded, and built for variable income)#

Pick 3 to 5 modules you can run weekly, then rotate 1 "new skill" monthly so the system grows without chaos. At this point, you already have the cadence and the log. The next step is to stop improvising and start training repeatable money habits: rules first, edge cases later.

How to run this like an operator (not a motivational poster)#

Use one competence test (age-agnostic): your kid can (1) explain the rule, (2) follow it for 4 weeks, (3) reconcile what happened in the ledger.

| Module | Best for | Do this week | Control |

|---|---|---|---|

| 3-bucket jars (Spend/Save/Give) | First-time structure | Label 3 containers and log every inflow allocation in family ledger lite | Physical limits plus a required log entry |

| Payday workflow (earn → allocate → approve → review) | Variable income family finance | Run the 4-step flow only when client payments land | Batch payout days so spending never front-runs income |

| Allowance policy one-pager | Negotiation fatigue | Write 1 page: 'we pay for' vs 'you pay for' by category | Every exception gets logged and reviewed weekly |

| Spend-approval thresholds ladder | Impulse buys | Set 3 tiers (small = decide, medium = ask, large = 24-hour wait) | Approvals queue |

| Weekly money jobs list | Kids who learn by doing | Assign 3 roles (receipt catcher, subscription checker, charity chooser) | Named owner signs off in the ledger |

| Subscription creep drill | Teens | Monthly audit, and require 2 approvals for any new recurring charge | Recurring spend lock plus a log |

| Irregular income simulator (Green/Yellow months) | Freelancer households | Define 2 modes and the exact pause list for Yellow | Pre-written contingency policy |

| Teen first invoice project | Teen earners | Create 1 invoice, track paid/unpaid status, and explain any required paperwork to get paid (as applicable) | Records folder plus a payment status log (Payouts mindset) |

| Values budget | Purpose beyond kids savings | Pick 1 quarterly giving goal and log contributions | Earmarks plus a review checkpoint |

Also, do not debate at the register or app store. Decide once, document it, and review it monthly like policy.

-

3-bucket jars (Spend/Save/Give). Good first-time structure. This week, label 3 containers and log every inflow allocation in family ledger lite. Keep the control simple: physical limits plus a required log entry.

-

Payday workflow (earn → allocate → approve → review). This works well in a variable-income family because it mirrors real cashflow timing. Run the 4-step flow only when client payments land, and batch payout days so spending never front-runs income.

-

Allowance policy one-pager. If the same negotiation keeps coming back, write 1 page: "we pay for" vs "you pay for" by category. The control is simple too: every exception gets logged and reviewed weekly.

-

Spend-approval thresholds ladder. Set 3 tiers (small = decide, medium = ask, large = 24-hour wait). The tradeoff is obvious: kids get autonomy, but you need to respond fast enough for the system to work. If you like risk-signal thinking, borrow the mindset from A Guide to Stripe Radar.

-

Weekly money jobs list. Assign 3 roles (receipt catcher, subscription checker, charity chooser). Keep it from getting fuzzy by making sure the named owner signs off in the ledger.

-

Subscription creep drill. For teens, do a monthly audit and require 2 approvals for any new recurring charge. Keep a recurring spend lock plus a log so the rule is visible.

-

Irregular income simulator (Green/Yellow months). Define 2 modes and the exact pause list for Yellow. The goal is clarity without oversharing, backed by a pre-written contingency policy.

-

Teen first invoice project. Create 1 invoice, track paid/unpaid status, and explain any required paperwork to get paid (as applicable). Keep a records folder plus a payment status log.

-

Values budget. Pick 1 quarterly giving goal and log contributions. If a must-have shows up mid-week, route it to the next meeting and decide against the documented goal, not emotion.

Quick comparison: which method fits your kid's age and your cashflow?#

Pick methods your kid can repeat and explain, then align them to your cashflow so the habit survives real life. You now have a menu. The next job is a selection rule that keeps random tips from cluttering the weekly close.

Choose a small core set you run consistently. Then rotate in one extra skill when the core runs smoothly.

How to choose your set (safe defaults)#

Use two filters, in this order:

- Readiness (not vibes): Can your kid follow a rule, use the right words, and review what happened after? Treat cash flow language as a long-runway skill you introduce early, then deepen over time.

- Cashflow shape: If you invoice clients or ride uneven income, you may want to teach timing before you teach "growth." Hands-on learning early can be as simple as counting loose change into a jar. That same hands-on pattern can work later too: money comes in, you label it, you decide what happens next.

Hypothetical: a client pays late, your kid wants to buy something now, and you feel pressure to smooth it over. Instead, route it through your chosen method - payday-based allocation, approvals, or a written policy - and review it at the next close. You teach family finance without panic, and you protect trust.

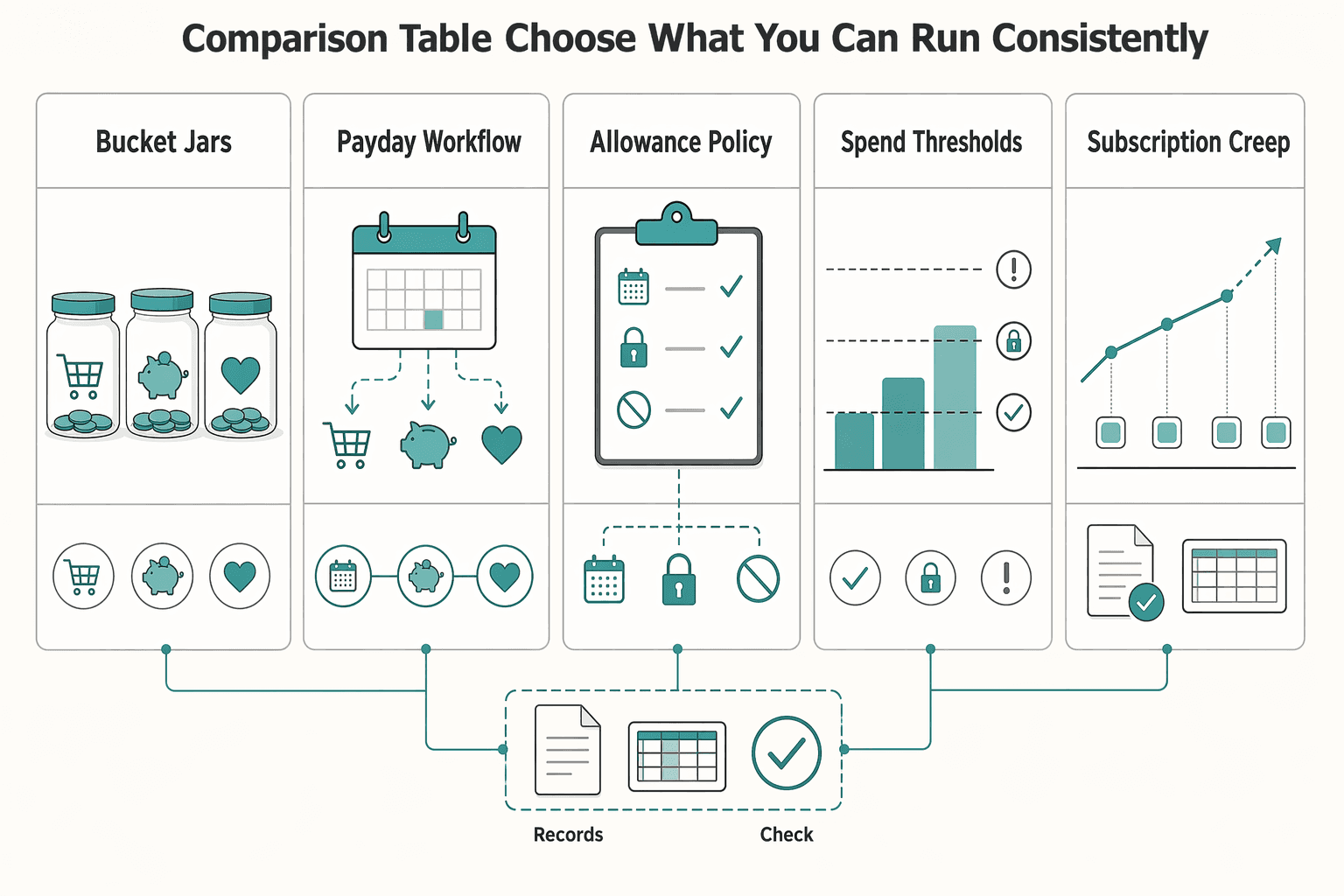

Comparison table (choose what you can run consistently)#

| Method | Best starting cue (readiness) | Best for (money management outcome) | Simple rule to add (make it predictable) | Lightweight record to keep | Tight-month friendly? |

|---|---|---|---|---|---|

| 3-bucket jars (Spend/Save/Give) | Counts cash and likes visual categories (jar counting helps early) | First structure for savings and tradeoffs | Allocate the same way every time money arrives | One line per inflow: date, amount, split | Often |

| Payday workflow (earn → allocate → approve → review) | Understands "not paid yet" vs "paid" | Cash flow timing and planning | Only allocate after income hits (no forecasting promises) | "Received" log plus allocation note | Often |

| Allowance policy one-pager | Repeats the same arguments weekly | Fewer fights, clearer boundaries | "If it's not on the page, it waits for review" | The policy note plus an exceptions list | Often |

| Spend thresholds ladder | Impulse buys create friction | Decision-making with guardrails | Define what requires a check-in vs solo decision | Approval notes (what, why, outcome) | Often |

| Subscription creep drill | Uses apps, forgets recurring costs | Modern spending awareness | New recurring costs require a deliberate review | Recurring list (name, price, keep/cancel) | Often |

| Irregular income simulator (good month/tight month rules) | Can discuss cash flow plainly | Resilience when income swings | Define what changes in a tight month | Two-mode note (rules for each) | Often |

| Teen first invoice project | Earns from gigs | "Get paid" literacy and admin competence | Every job gets a simple record until paid | Invoice list with paid/unpaid status | Sometimes |

The safe default: run the system, not the debate (and scale it as your kids grow)#

Run a tiny, repeatable money system your kids can execute, because consistency beats winning a weekly argument about allowance or spending. The goal is to make money management feel like a normal household workflow, not a high-stakes conversation.

Start this week with a minimum viable system (operator-simple)#

Pick a small set of components and keep them boring:

- One short weekly check-in: same day, same agenda, keep it brief.

- A simple allocation: for example, three buckets like Spend, Save, Give (use whatever categories fit your family).

- A clear "pause-and-ask" rule: if it's above your number, it waits for the check-in.

- A simple log: a shared note or spreadsheet line item (date, amount, category, what we learned).

Hypothetical scenario: your kid wants an in-app add-on. Instead of debating in the moment, you say, "Log it as a request. We decide at the check-in." You make the decision process repeatable.

Scale after consistency, not excitement (add one thing at a time)#

Once the baseline feels routine, add one small capability. Do not overhaul the whole system.

A few optional ideas (not requirements): review recurring charges together, give kids lightweight roles (tracking requests, saving receipts), or practice "tight week" choices where you pause non-essentials.

If you want a real-world friction example, talk about fees. A payment gateway processes card transactions, and every transaction incurs a cost, so small fees add up.

| Example payment cost item (from Stripe pricing pages) | What a kid should learn |

|---|---|

| 2.9% + 30¢ per successful domestic card transaction | Small percentages still reduce what you keep. |

| +1.5% for international cards | Cross-border choices change costs. |

| +1% if currency conversion is required | Conversions create friction, so plan for it. |

Keep one meta-rule: fees and terms change, so you double-check before you commit. If you want an operator analogy, think modular rollouts where you add controls when the basics run cleanly.

Frequently Asked Questions

How do I teach kids about money by age?

Start with age-appropriate tools and language, then level up only when your kid can explain the idea back to you. Scotiabank frames “age-appropriate ways” from early basics (like piggy banks) through later concepts (like credit scores), and it explicitly spans ages 3 to 13+. CIRO suggests grade 2 or 3 as a good time to start teaching kids about money, and using real or play money can help them understand saving and spending. Practical rule: pick one repeatable behavior per age band, then keep it hands-on.

Should kids get an allowance, and how should it work?

There is no one-size-fits-all rule. What matters most is that money conversations happen at home and kids can ask questions, with answers kept simple and straightforward.

What should kids learn first: saving, spending, or investing?

Focus on clear categories and tradeoffs, because kids cannot manage what they cannot label. CIRO defines financial literacy as teaching kids about money, saving, and budgeting so they build tools for smart decisions over time. Using play or real money can help them practice choices like spending versus saving, then review what happened. Add complexity only after they can explain the basics in plain language.

How often should families talk about money?

Make money talk a normal topic at home, not a taboo. MapsCU emphasizes that talking about money matters, and it points to studies (via Greenlight) linking parent-kid money discussions at home with positive outcomes in early adulthood (ages 18-25).

Should children know their parents’ income?

There is not a single rule that fits every family. Keep it age-appropriate, keep it simple and straightforward, and be honest when you do not know how to answer a question.

How can I teach money skills without causing anxiety?

Keep it straightforward, and do not pretend you have every answer. MapsCU explicitly notes, “You don’t even need to have all the answers, and it’s okay to admit when you’re stumped.” Use a script you can repeat: “I’m not sure. Let’s look it up together.”

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- futureofchildren.princeton.edu/document/401trusted

- ir.library.illinoisstate.edu/cgi/viewcontent.cgitrusted

- marriott.byu.edu/magazine/feature/money-talks-teaching-kids-f...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- web.lemoyne.edu/courseinformation/mth%20112/rinaman/instman/...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

A Guide to Stripe Radar for Fraud Protection

**Treat Stripe Radar for fraud as a cashflow protection system, not a vanity fraud score.** Stripe Radar gives you real-time screening with AI and no extra development setup, but outcomes still depend on your rules and operations. Your job is simple: decide when to `Block`, `Review`, or `Allow`, then tie those decisions to fulfillment timing and client communication so fraud protection supports more predictable revenue.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.