Quick Answer

Prioritize payment controls before discretionary growth spend. The article recommends locking terms before work starts, standardizing invoice and payment link handoffs, and screening client risk so delays, holds, and chargeback exposure are harder to trigger. It also flags a hard stop on any request to send your own money first to unlock future payouts, echoing the FTC task-scam warning. Once those controls are stable, then add optional tools and training.

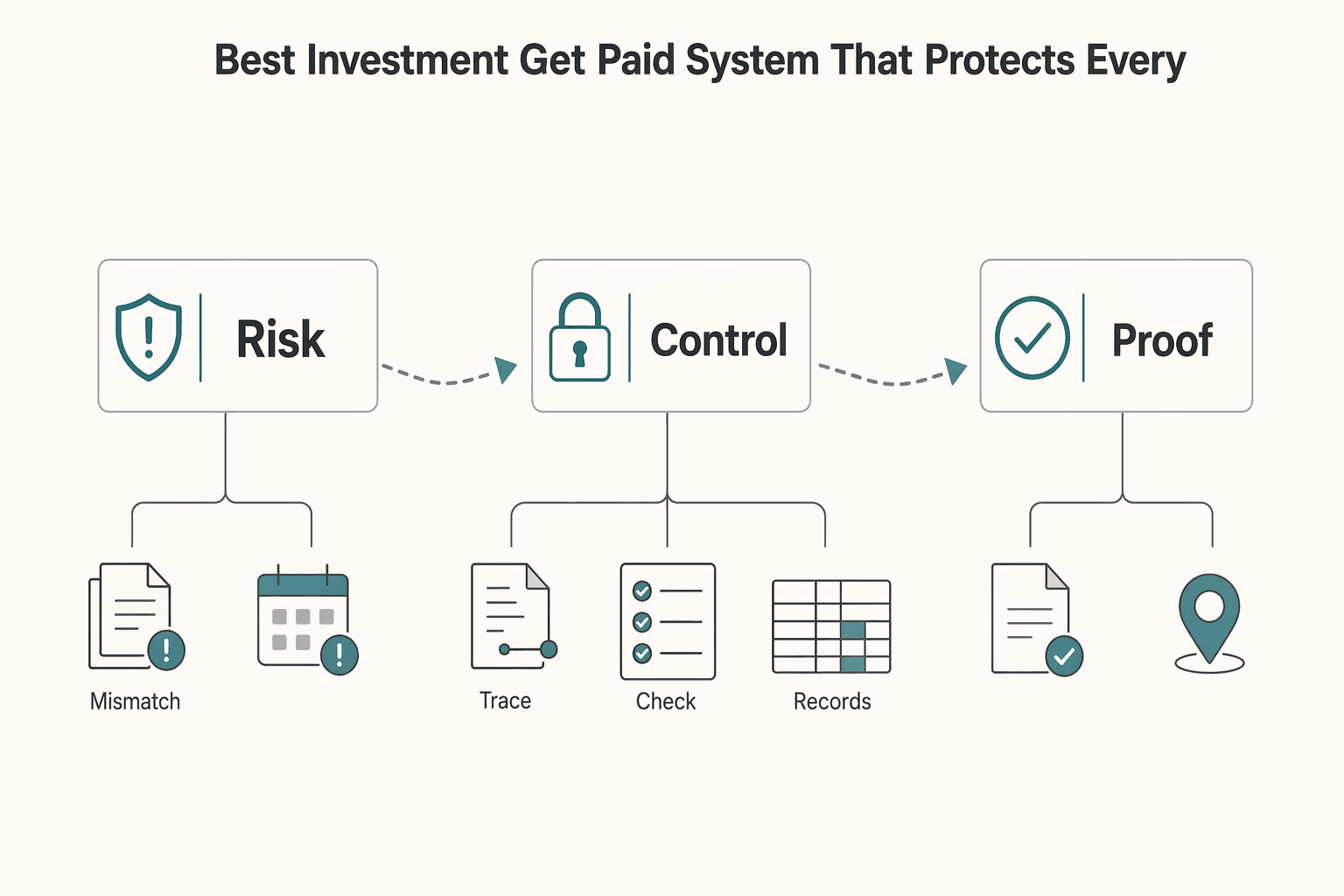

The best investment is a get paid system that protects every client engagement#

Start with payment reliability before you buy another growth tool. Courses, coaching, and software can help delivery, but they do not protect cashflow when payment is delayed, disputed, or never sent. A practical move is to make each engagement payable, traceable, and harder to derail from kickoff to settlement.

This is a risk-control decision, not just an invoice-speed decision. In a December 12, 2024 consumer alert, the FTC described a big increase in reports of gamified job scams known as task scams. The pattern is consistent: fake earnings are shown, then people are told to deposit their own money, often in crypto, to keep earning. The commissions are fake, and scammers get paid.

Use this ranked list to reduce delays, avoidable fees, and payment failures in client work. Treat it as a sequence, not a menu. Pick one control, implement it completely, track what changed, and only then move to the next layer. That keeps execution clean and makes it easier to see which action produced the result.

- Delay control

Shorten the path from signed scope to settled funds. Lock terms and approval paths before kickoff so timing is not renegotiated mid-project.

- Fee control

Cut preventable transfer and handling costs. Keep one invoicing path and payment-method set, with fewer one-off exceptions.

- Failure control

Reduce nonpayment, holds, and scam exposure. Verify payer identity, billing ownership, and the first payment route before delivery.

Use one pre-start checkpoint before kickoff. Confirm that the legal entity name matches the contract, the billing owner is confirmed, the due date and currency are written, and the first payment route is accepted in writing. If any item is unclear, pause the start date. A hard red flag is any client asking you to send money first to unlock future payouts or commissions, which matches the task-scam pattern the FTC flagged.

Here is a simple way to use this article: define your current failure mode, define the evidence you will use to confirm improvement, then run the process for one full billing cycle. If your issue is delayed approvals, your evidence is not a feeling. It is signed milestones, on-time invoice issuance, and fewer stalled releases. If your issue is payment confusion, your evidence is complete invoice records and fewer status disputes.

The rest of this guide stays deliberately narrow: operational controls first, with personal allocation topics handled separately.

How this list picks winners and who should use it#

Use this list if your main goal is payment reliability. Every recommendation is chosen because you can implement it quickly and verify it in your own records.

| Criterion | Higher rank when |

|---|---|

| Cashflow timing | It shortens the path from signed scope to confirmed payment |

| Chargeback and hold risk | It adds practical pre-work and pre-release checks meant to reduce avoidable failures |

| Implementation effort | A freelancer or small team can apply it quickly |

| Audit-ready records | It leaves clear documentation for reconciliation and tax prep |

That filter is intentional. The article prioritizes moves you can execute fully and keep running without tool sprawl. Treat these inputs as practical guidance, not hard evidence of payment-outcome improvements.

The four criteria work together. Fast timing with weak records can create cleanup pain later. Strong records with slow collection timing can still leave you cash constrained. Lower-risk checks that are too complex to maintain can fail in practice. The winner is the option that is fast enough to ship, clear enough to verify, and stable enough to repeat without constant exceptions.

Use this scoring lens before you commit: what breaks today, what can you fix in one cycle, and what evidence confirms the fix worked? If you cannot answer all three, simplify the plan until you can. Overly ambitious rollouts usually fail because they spread attention across too many partial changes.

This list is for freelancers, creators, and small teams that want a simpler, more disciplined operating approach to getting paid. It is not for readers focused only on personal allocation products without a business payment-risk goal. If you want a quick next step, try the free invoice generator.

Best investment one lock payment terms before kickoff#

Lock payment terms before kickoff so you are not renegotiating basic expectations once work starts. It is a strong first control because it reduces ambiguity during delivery.

Advance payment structure is deal-specific. Decide whether you will use a flat retainer or a percentage of project value, then confirm the terms in writing before work starts.

Use this minimum set before kickoff, and confirm each item in writing.

- Whether payment is required up front before starting the work

- Whether that upfront amount is a flat retainer

- Or a percentage of the project value

When you request advance payment, presentation matters too. One freelancer anecdote makes a useful point: you need to come across as trustworthy when asking a client to put money up front.

A common failure mode is verbal alignment followed by vague written terms. Close that gap with a brief written recap and explicit confirmation before work starts.

Present terms in plain language when requesting advance payment. If a client resists basic clarity on payment structure, pause kickoff until the terms are explicit.

Best investment two standardize invoicing and payment link operations#

After terms are locked, standardize how you issue invoices and handle payment links. The goal is one clear path from invoice issuance to payment confirmation.

| Step | Action | Key detail |

|---|---|---|

| 1 | Issue the invoice first | Send it as soon as a milestone is accepted, with owner, due date, currency, and line items |

| 2 | Attach the payment link in the same handoff | Keep payment action and invoice together |

| 3 | Confirm payment state before release | Make delivery decisions from status records, not memory |

| 4 | Log the provider reference | Keep invoice and payment events linked |

| 5 | Trigger delivery and payout steps last | Release files, access, or outbound payouts only after payment confirmation |

Late payments and slow collections are common in freelance work, and the time loss is real. Hours disappear into spreadsheets, email threads, and manual checks when each client gets a different process. Even small variations can cause confusion, like sending an invoice in one channel and payment instructions in another.

In practice, sequence matters: issue the invoice first, attach the payment link in the same handoff, confirm payment state before release, log the provider reference, and trigger delivery or payout steps last.

The upside is a cleaner handoff and fewer avoidable delays. The tradeoff is setup and enforcement, especially when clients request one-off handling. Costs can start small, but they are still real. One invoicing plan example is around $19 per month, which is a budgeting reference rather than a standard.

Use one weekly or monthly verification checkpoint: every invoice should show owner, due date, currency, status trail, and provider reference. If key fields are missing, fix the record before moving the next delivery forward.

You can make this easier by defining one internal handoff script. Keep it short and consistent: invoice sent, payment action attached, status reviewed, reference logged, release approved. That script gives you a shared language with assistants, contractors, or future hires and reduces decision drift when workload is high.

The common failure mode is exception creep. A few off-process requests can lead to missed invoices, status disputes, and cashflow uncertainty. When a client needs a different path, document the exception and require confirmed payment state before continuing. If exceptions become frequent, revise the base process and communicate the update to all active clients at once.

Best investment three screen clients for payment risk before work starts#

Screen clients for payment risk before kickoff, especially with new clients or unclear billing ownership. Confirm who pays, how approval works, and what happens if terms change before any delivery starts.

Use a pre-client checklist and save each answer in the deal file before you approve kickoff.

- Legal entity confirmation: Match contract counterparty, invoice recipient, and expected payer name. If names do not align, pause and request written clarification.

- Billing contact validation: Collect one primary billing contact plus one backup, then confirm both can receive invoices and reminders.

- Approval path: Identify who approves milestones, who releases payment, and the expected approval window.

- Expected payer country: Record where funds will originate so currency and timing expectations are clear.

- Dispute and acceptance process: Ask what proof is needed for milestone acceptance and disputes, then include that evidence list in scope and handoff notes.

The checklist is most useful when you treat it as a go or no-go gate, not a formality. Missing answers can be warning signals, not just paperwork gaps. If a client cannot identify the payer, approval owner, or acceptance standard before kickoff, you may end up carrying that uncertainty during delivery.

One risk pattern to treat cautiously is a client-requested insurance deposit where you are told to pay first and get refunded later. A public freelancer Q&A example describes this exact request, and one answer was direct: do not pay. It is user-generated content, not policy guidance, but it is still a warning signal to pause and renegotiate.

When signals are mixed, use this routing rule before signing:

| Risk signal before signing | Structure before kickoff |

|---|---|

| Unclear budget, conditional payment language, missing finance owner | Smaller milestones, upfront deposit from the client, strict acceptance criteria per milestone |

| Clear budget, named finance contact, documented approval path | Larger milestone windows with written acceptance criteria and release conditions |

Final checkpoint: do not start work until all five checklist fields are complete and saved with signed scope. If risk stays high after screening, pair this step with A Guide to Transaction Monitoring for High-Risk Payments. Keep the same checklist in your renewal process too, because payment conditions can change after the first engagement.

Best investment four set cross border currency rules before you scale#

Set cross-border currency rules before volume grows. You get better payout predictability when FX decisions are planned in advance, not made under deadline pressure.

If you are paid in U.S. dollars and spend in another currency, this step can reduce conversion surprises. Cross-border payments can add friction beyond exchange rates, including data privacy requirements, tax differences, language barriers, and timing delays.

- Fee ownership rule: Decide before kickoff who pays transfer fees, where fees are deducted, and whether invoice totals are gross or net.

- Currency separation rule: Keep incoming U.S. dollars separate from local-currency spending until a defined conversion trigger is met.

- Timing and quote rule: Match conversion timing to cash needs. For near-term obligations, use shorter windows. For later obligations, stage conversions and recheck quote validity.

| Obligation timing | Conversion approach | Required checkpoint |

|---|---|---|

| Due soon | Convert in short windows after funds settle | Save quote timestamp, applied rate, and expected payout date |

| Due later | Stage conversions in planned tranches | Recheck quote validity before each tranche |

The tradeoff is execution discipline. Set quote timing and fee ownership before funds arrive. Use one release checkpoint before each outbound payment: invoice settled, payer country recorded, transfer rail logged, conversion trigger documented, and payout reference captured. If any field is missing, hold release and complete the record first.

A simple conversion log can reduce confusion. Keep one line per conversion event with source currency, target currency, quote timestamp, applied rate, fee treatment, and payout reference. This can make month-end reconciliation easier and help explain variance when actual settled amounts differ from your initial estimate.

Concrete use case: a client pays in U.S. dollars by invoice, funds land in a receiving account, conversion happens only when a documented trigger is met, then payout is sent with traceable records. The value is not just fewer surprises. It is faster decisions because everyone can see what rule was applied and why.

Best investment five make payout reliability and status visibility non negotiable#

Make payout reliability and status visibility non-negotiable before payout volume grows, especially if you pay contractors or vendors on repeat cycles.

Treat payout operations as a defined process with clear ownership. In a 2026 Ask a Manager freelance thread with 153 comments, readers described freelance admin work as self-directed, including invoicing, and one commenter suggested retaining an accountant with relevant client experience. The useful takeaway here is simpler: assign owners early and document payout decisions so follow-through does not depend on memory.

- Duplicate-safe payout handling: Keep one internal record per payout request and avoid accidental resubmission while an attempt is unresolved.

- Clear status language: Define a small, shared set of payout states so updates and handoffs stay unambiguous.

- Single exception queue: Route failed or blocked payouts into one queue with a named owner, next action, and timestamp, plus a clear retry or escalation path.

The upside is fewer manual investigations and clearer updates, while the tradeoff is setup effort across integration, ownership, and policy. Use this checkpoint before each payout batch:

- Each payout record includes payee, amount, method, current status, and latest update time.

- Each blocked item has a named owner and next action.

- Each retry has a documented reason.

To keep status visible, use one shared view for payout state and one owner for exception triage. Splitting status across separate spreadsheets, inboxes, or chat threads can create blind spots. A blocked payout may then sit unresolved because each person assumes someone else is handling it.

Concrete use case: a team combines direct client collections with scheduled payout batches across multiple payout paths. Shared status rules and one exception queue can keep one failed transfer from stalling the full batch. When a failure repeats, escalate from retry to root-cause review so the same error is less likely to repeat next cycle.

Best investment six build a monthly tax and reconciliation evidence pack#

Build one monthly evidence pack that links invoices, payments, fees, and ledger entries before month close. This can reduce tax-season guesswork and make reconciliation easier to review later.

This step is especially useful when income arrives through multiple channels in the same month, for example platform payouts, direct invoices, and transfers. The tradeoff is monthly discipline.

Evidence pack checklist#

| Evidence item | What to include |

|---|---|

| Invoice list | One register with invoice ID, client, issue date, due date, currency, and gross amount |

| Payment confirmations | Receipts or transfer confirmations mapped to invoice IDs |

| Payout reports | Monthly statements from each payment channel |

| Fee breakdowns | Fees recorded separately from net payouts |

| Ledger-aligned export | Bookkeeping export for the same month, matched line by line to source records |

At minimum, include the five items above.

If a record does not map cleanly across these files, fix it before closing the month. A practical routine is to build the evidence pack as transactions happen, then run one month-close review pass. Waiting until quarter close can make mapping gaps harder to unwind. Keeping records current can also help if a client disputes timing, amount, or fee handling after delivery.

Tax context fields that prevent rework#

- Income type field: A simple internal category so similar income is grouped consistently.

- Preparation notes field: Plain-language notes for filing prep.

- Jurisdiction field: Country tag per line so country-specific treatment stays separate.

For UK freelancers, keep Self Assessment context explicit and separate from other jurisdictions. HM Revenue & Customs uses Self Assessment to collect Income Tax from individuals whose income is not taxed at source, and UK guidance emphasizes who needs to file, allowable expenses, and accurate income tracking. Use that as UK-specific context, not a universal rule.

You can also reduce future confusion by storing one brief note for unusual events, such as corrected invoices, refunded amounts, or payout reversals. That note can save time during filing and review because it explains variance before anyone has to reconstruct the timeline. A monthly cadence keeps uncertainty smaller, so quarterly and annual work is more straightforward.

Best investment seven fund growth tools only after payment risk controls are in place#

Fund growth tools only after payment controls are stable. If you are putting money back into your freelance business and want to avoid adding cash stress, treat courses, coaching, and automation as phase-two spend. Move there only after your payment process is steady.

This tradeoff matters most when freelance income is unpredictable. Late client payments can create immediate pressure, so stabilize payment timing first and protect optional spending for later. That sequencing can reduce cash stress even if it slows short-term experimentation.

Priority ladder before discretionary spend#

- Terms and invoicing first: Set terms before kickoff, invoice on schedule, and review overdue items weekly.

- Payment reliability second: Track whether payments arrive as expected so collected cash is usable when you need it.

- Records third: Keep invoices, payments, fees, and ledger entries aligned each month.

- Growth spend fourth: Add new tools, courses, or coaching only after the first three layers are consistently working.

Use one hard gate before phase-four spending: if late payments still push you toward outside borrowing, pause new growth purchases. Traditional loans can involve long applications, strict credit checks, and higher rates. Personal loans can add fixed repayments that are harder to carry in slower months.

A useful implementation detail is to keep a short backlog of growth ideas while you stabilize payment controls. This prevents impulse purchases during stressful weeks and keeps evaluation objective. When your gate is met, pick one idea from the backlog, define the expected business result, and test it for one cycle before stacking additional spend.

Scenario contrast when cashflow is unstable#

When cashflow is unstable, defer optional long-term allocations until receivables are steadier. This is sequencing, not a judgment on those options. The red flag is committing funds while payment volatility is still high enough to force emergency financing.

A practical use case is reinvesting only after late payments are no longer creating immediate pressure. Put that budget into one targeted growth experiment instead of broad tool sprawl. Then review after one cycle: did demand improve, and did payment timing stay manageable? If yes, add the next growth expense. If not, route funds back to payment controls.

Comparison table for choosing your first investment#

Use this table as a first-pass filter: pick one primary investment and one backup, then execute both fully before adding more.

Freelancers still carry overhead and monthly expenses, so focus matters more than urgency when cash timing gets uneven. You do not need to run every control at once. You need to run the right control consistently enough to produce a clear signal.

How to choose your first move#

- Start with the biggest failure mode: Choose the issue creating the most friction right now.

- Check implementation readiness: Favor the option you can complete end to end this cycle.

- Prioritize near-term cashflow stability: Choose the row most likely to protect incoming or usable cash first.

- Match current client mix: Make sure your first move reflects where most payment volume sits now.

| Investment focus | Best for | Primary upside | Main tradeoff | First success signal |

|---|---|---|---|---|

| Contract payment terms | Frequent late approvals | Clearer approval and milestone expectations | Possible client pushback | Signed milestones are in place before work starts |

| Invoice and payment link standardization | Manual chasing | More consistent invoicing workflow | Setup and enforcement work | Invoices and payment links follow one standard process |

| Pre-client risk screening | New or high-risk clients | Clearer go or no-go decisions before kickoff | Added sales friction | Screening checks are completed before onboarding |

| Cross-border currency rules | Multi-currency cashflow | Clearer rules for conversion timing and ownership | Requires timing discipline | Currency-handling rules are documented and followed |

| Payout reliability controls | Repeated outbound payments | More consistent payout operations | Integration effort | Payout checks are completed before release |

| Monthly evidence pack | Tax and audit stress | More complete records for filing and review | Ongoing admin cadence | Monthly records are compiled on a fixed schedule |

Use a simple if-then rule to set priority. If approval or contract friction is the blocker, start with terms. If collections lag, start with invoicing and payment link standardization. If disputes rise, move screening up first. A practical risk is launching too many controls at once and running none consistently enough to produce a clear signal.

When you choose your primary and backup moves, define completion before you start. Completion means your process is documented, used across active clients, and reviewed against real records. Without a completion definition, teams can confuse activity with progress and keep changing direction before results are visible.

Build one reusable system and apply it to every client#

The table gives you a starting point. Results usually come from applying one repeatable process across every client, not from adding more tools quickly.

- Pick one starting lane and implement it end to end.

Choose the row tied to your biggest pain and finish it before expanding. A practical model groups core tooling into four categories: project management, invoicing and payments, social media scheduling, and AI. Keep your first cycle focused on the category most tied to collections so you can measure a clear before-and-after result.

- Use one client record that connects delivery and payment status.

Keep the same minimum fields for every engagement: scope, invoice state, payer contact, and next action date. Run one daily checkpoint so each active client has a current status and a named next action. One freelancer example suggests that starting early, even at two clients and with a tool around $20 per month, can be easier than cleaning up fragmented records later.

- Scale through efficiency before adding new spend.

Use a step-by-step rollout instead of ad hoc changes. A scaling-focused view published January 9, 2025 highlights the tradeoff: growth often raises expense, while scaling focuses on efficiency. If payment timing is still unstable, hold new growth spending until payment metrics stay steady for a full cycle.

- Treat channel fees as infrastructure only if performance supports them.

Fees are not automatically bad, but they should pass a reliability test. One freelancer reported over $5,000 in Upwork fees last year after four years full time there and viewed that cost as rent. Treat that as a personal example, not a benchmark. Keep channels that improve payment reliability and reduce escalations, and cut channels that only add cost.

To make this section practical, run a 30-day execution sprint. Pick your starting lane, set one weekly review time, and track only the fields that confirm progress. At the end of the sprint, decide with evidence: continue, adjust, or pause. Move to your backup lane only after the first lane is stable.

If you cannot show faster payment speed, clearer status visibility, or fewer escalations after one full billing cycle, pause new tools and fix execution first. When you are ready to expand, review Gruv docs or request access to confirm market and program coverage for collections, FX, and payouts where supported.

Frequently Asked Questions

What does investing in your freelance business actually mean if my main pain is late payment?

If late payment is the main pain, treating payment reliability and budgeting as your first investment can be a practical starting point. Prioritize cashflow basics before adding growth spend. For uneven income, budgeting is core discipline. In practice, that can mean fewer optional purchases while income timing is uneven.

What should I invest in first if I can only fix one thing this month?

Start with the single failure mode that puts cashflow at the most risk, then complete one fix end to end this cycle. A finished control can be more valuable than several partial upgrades. If you are unsure which failure mode is largest, choose the one that most often delays usable cash.

How do I reduce late payments without damaging client relationships?

Set expectations early and keep follow-up predictable; this can keep payment conversations more procedural than personal. Make the business context clear, because price usually dominates when context is missing. Consistent terms and clear status updates can help reduce tension by keeping a shared record.

What is usually the highest-ROI investment for freelancers in unstable cashflow periods?

In unstable periods, cash protection is often the first priority. Revenue pressure can push freelancers into weaker terms, while more runway supports more deliberate decisions. Use budget guardrails: average income over 12 months and reserve about 25-30% for taxes. Keep growth spend secondary until cashflow is steadier.

How should I handle international payments when I earn in U.S. dollar and spend locally?

Use one consistent process instead of ad hoc decisions. Tie conversion and spending decisions to your budget plan, then document each payment and conversion for clear records. There is no one-size-fits-all rule for fees or conversion timing, so confirm your process with your payment provider before funds arrive.

How much should go to growth spend versus payment safety and reserves?

Prioritize safety first, then fund growth from what remains. A practical baseline is a buffer fund covering 3-6 months of living costs plus your tax set-aside. After that, increase growth spend gradually and consider retirement options such as IRAs. If reserves drop or payment delays rise, shift funds back toward payment controls.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- business.louisiana.edu/sites/business/files/Personal%20Financial%20...trusted

- catalog.albertus.edu/certificates/courses/index.phptrusted

- consumer.ftc.gov/consumer-alerts/2024/11/task-scams-create-il...trusted

- sec.gov/Archives/edgar/data/1627475/0001627475200000...trusted

- payoneer.com/resources/business/5-smart-ways-to-fund-a-ne...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

Transaction Monitoring for High-Risk Payments That Protects Cashflow

A freelancer-ready transaction monitoring setup should protect cashflow and support compliance at the same time. The goal is not maximum speed or maximum friction, but risk-based oversight that keeps routine payouts moving and routes unusual activity to review.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.