Quick Answer

Use a three-part workflow: clear compliance first, submit an AP-ready invoice second, and choose the rail by net outcome third. To invoice canadian client from us llc, verify GST/HST position, place-of-supply facts, service location, and the exact form request before billing. Then set currency and fee responsibility in the agreement, compare bank wire, PayPal, and multi-currency options with one net-received calculation, and keep forms, invoice files, and remittance evidence in one record trail.

Landing a high-value Canadian client is a good problem to have. It can surface cross-border issues fast: unfamiliar tax rules, inconsistent payment instructions, and fees that quietly cut into what you earned.

This is not a field-by-field invoicing checklist. It is a practical way to manage cross-border billing through three connected pillars: Compliance, Operations, and Finance. Get those three right, and invoicing gets less stressful, more predictable, and easier to defend if questions come up later.

Pillar 1: The Compliance Foundation - Mitigating Catastrophic Risk#

Start with compliance, not invoice formatting. If you skip that step, you can end up with the wrong GST/HST treatment, miss a registration trigger, or delay payment while the client waits for the right tax documents. Use these as working terms, not abstract definitions:

- Small supplier status (GST/HST): CRA status used in registration analysis. CRA materials tie this to a benchmark often shown as $30,000, but you should confirm the exact regime and applicability to your facts before relying on it.

- Place of supply: Rules that determine where a taxable supply is made, which drives GST/HST treatment decisions.

- Permanent establishment: Treaty concept for a fixed place of business in Canada through which business is carried on, wholly or partly.

- Beneficial owner (W-8 context): The person or entity required to include the payment in gross income under U.S. tax principles.

Use a trigger table before every invoice#

A simple trigger table helps you catch avoidable mistakes before they turn into invoice problems. It works best when you confirm two facts first: where the services were performed and which tax form the client is actually requesting.

| Trigger condition | Required action | What to include on invoice | What to document for records |

|---|---|---|---|

| You appear to remain within small supplier treatment (after verification) | Keep monitoring revenue and confirm whether you are making taxable supplies in Canada | Document service details clearly; confirm GST/HST treatment only after registration and place-of-supply checks | Threshold tracker, client location, short memo with threshold status after verification |

| You are not a small supplier and you make taxable supplies in Canada | Determine whether GST/HST registration is required before billing | Apply GST/HST treatment only after confirming registration status | Registration evidence, threshold calculation, place-of-supply notes, client location or province evidence |

| Services were provided in Canada | Review Regulation 105 exposure before payment; CRA guidance puts withholding responsibility on the payer, and cited CRA material references a 15% withholding rate for certain independent services in Canada | Clear service dates and service location where relevant | Travel and work-location records, SOW, timesheets, related client correspondence |

| Facts suggest a fixed business footprint in Canada | Pause routine invoicing and escalate to cross-border tax counsel | Avoid assumption-based tax language | Contracts, workspace or office facts, authority or delegation facts, delivery model details |

| Client requests foreign-status or treaty forms | Confirm which regime the client is administering, then send the correct form set | Add only needed vendor or reference details | Signed forms, delivery confirmation, validity tracking, request context |

Handle W-8BEN-E as a workflow, not a catch-all form#

Use W-8BEN-E when a payer or withholding agent asks for foreign-entity status documentation in a U.S. withholding or reporting context. Send it to the payer or withholding agent, not the IRS.

| Situation | Form or action | Timing or note |

|---|---|---|

| Payer or withholding agent asks for foreign-entity status documentation in a U.S. withholding or reporting context | Use W-8BEN-E | Send it to the payer or withholding agent, not to the IRS |

| Canadian treaty-benefit and beneficial-owner documentation | Use NR301, NR302, or NR303 | Do not use W-8BEN-E as a stand-in |

| Ordinary W-8BEN-E validity period | W-8BEN-E is generally valid | Through the end of the third succeeding calendar year |

| Change in circumstances affects form accuracy | Provide a new W-8BEN-E | Within 30 days |

Do not use W-8BEN-E as a stand-in for Canadian treaty-benefit documentation. CRA treaty-benefit and beneficial-owner documentation points to NR301, NR302, or NR303.

Refresh cadence:

- W-8BEN-E is generally valid through the end of the third succeeding calendar year.

- If a change in circumstances affects form accuracy, provide a new form within 30 days.

Pre-invoice checklist for a US LLC#

Before you bill, make sure these points are covered and documented:

- Verify small-supplier treatment status and whether you are making taxable supplies in Canada.

- Confirm place-of-supply facts and whether they change GST/HST treatment.

- Confirm service location; if work was performed in Canada, assess Regulation 105 before billing.

- Confirm whether the client needs W-8BEN-E, NR301/NR302/NR303, or no form.

- Ensure records are complete: contract, location evidence, threshold tracking, registration or form history.

- Pause and escalate to cross-border tax counsel for unclear or mixed facts, a possible Canadian business footprint, or uncertain tax-form requests.

If you are also tightening your accounting setup, see Separating Business and Personal Finances: An Important Step for LLCs.

Pillar 2: The Operational Blueprint - Guaranteeing Flawless Execution#

Once compliance is settled, payment speed often comes down to execution. Your job is to send a conforming invoice through the right AP channel, with terms that match how the client actually pays.

1. Build a conforming invoice#

A useful invoice is built for AP processing, not for looks. Missing required references or payment details can push an otherwise valid invoice back for correction. Use this as your baseline, then match each field to the client's AP spec:

| Field | Why AP may need it | Common processing issue | How you should format it |

|---|---|---|---|

| Your legal entity name and address (if requested) | Matches supplier onboarding and contract records | Entity details do not match onboarding records | Use your LLC legal name and registered address as onboarded |

| Client legal entity name and billing address (if specified) | Routes invoice to the correct payer record | Wrong billing entity | Copy legal billing details from the contract, PO, or vendor profile |

| Invoice date and unique invoice number | Commonly required for tracking and payment workflow | Missing date or duplicate invoice number | Use one clear invoice date and a unique sequential invoice number |

| Contract or PO reference (when required) | Connects invoice to approved spend | Missing or incorrect contract or PO number | Label and place the required reference exactly as AP requests |

| Service period and line description | Supports service review or acceptance where applicable | Vague descriptions with no period or deliverable detail | List billing period, deliverable, rate, and quantity in plain language |

| Amount due and currency | Confirms payable amount in the required currency | Currency omitted or totals inconsistent with line items | Declare currency clearly and keep all lines consistent |

| Tax details (if applicable) | Supports buyer documentation for GST/HST recovery where relevant | Incorrect GST/HST registration details | Show tax as a separate line when applicable and include current registration details once verified |

| Supplier or procurement identifier requested by AP | Matches invoice to vendor records and required documentation | Wrong identifier type or unverified format | Include only the requested ID, in the format AP requires |

| Remittance details for the approved payment rail | Supports release of funds to the approved destination | Beneficiary or bank mismatch with onboarding | Match remittance details to the approved rail and vendor setup |

For larger invoices, expect tighter documentation checks. Canadian GST/HST documentation tiers differ for totals under $100, $100 to under $500, and $500 or more. That makes tax-line accuracy and registration details more important as invoice value rises.

2. Run the same pre-invoice sequence every billing cycle#

Consistency matters more than speed here. Use the same pre-invoice sequence every cycle so "sent" also means "received and processable."

- Verify billing entity and required supplier identifiers. Match the invoice addressee to the contract, PO, or vendor profile, and confirm any buyer-required onboarding identifiers.

- Confirm AP contact and acceptance path. Validate the payable inbox or portal contact and who confirms service acceptance, because payment timing may depend on both invoice receipt and acceptance.

- Confirm submission channel and file rules. Check the required channel and format before sending.

- Save proof of submission and acceptance. Keep the final invoice file, portal or email confirmations, and acceptance messages in one record trail; usually, GST/HST-related records are kept for 6 years from the end of the year they relate to.

If you skip this sequence, the payment clock may not start when you think it did. In some contract frameworks, non-conforming invoices can be flagged within 15 days, and timing restarts after a corrected invoice is received.

3. Set payment terms around the client's actual AP setup#

Do not default to whatever terms sit in your template. Set terms around the client's real payable process. Procurement-heavy clients often need tighter references, controlled intake channels, and formal acceptance steps. Leaner teams may approve more directly, but they still need clear payment rails and clear responsibility for fees.

Use these decision checks before invoicing:

- Determine the client setup first: procurement-heavy AP flow or lean direct-approval flow.

- Confirm which payment rail is operationally approved.

- State who covers transfer and intermediary fees in writing before billing.

- Confirm whether payment timing runs from invoice issue date, or from receipt of an acceptable invoice plus acceptance.

- Escalate to a contract addendum before invoicing if currency, rail, fee allocation, PO requirement, or approved remittance destination is still unclear.

4. Use a clean handoff checklist#

Before you send, confirm these four points so the invoice arrives complete and processable:

- Invoice fields match legal entities, references, service period, and agreed currency.

- Submission channel and format match AP requirements.

- Terms reflect the actual payment rail, including fee allocation.

- You saved the submission evidence pack: invoice, confirmation, and acceptance record.

That clean handoff can improve approval speed, cut avoidable disputes, and make cash flow timing easier to predict.

Pillar 3: The Financial Strategy - Maximizing Profit and Minimizing Fees#

Once the invoice is processable, the real question is simple: what actually hits your account? Choose currency and payment rail invoice by invoice, based on who carries FX risk, how much AP friction the client has, and how stable you need your margin to be.

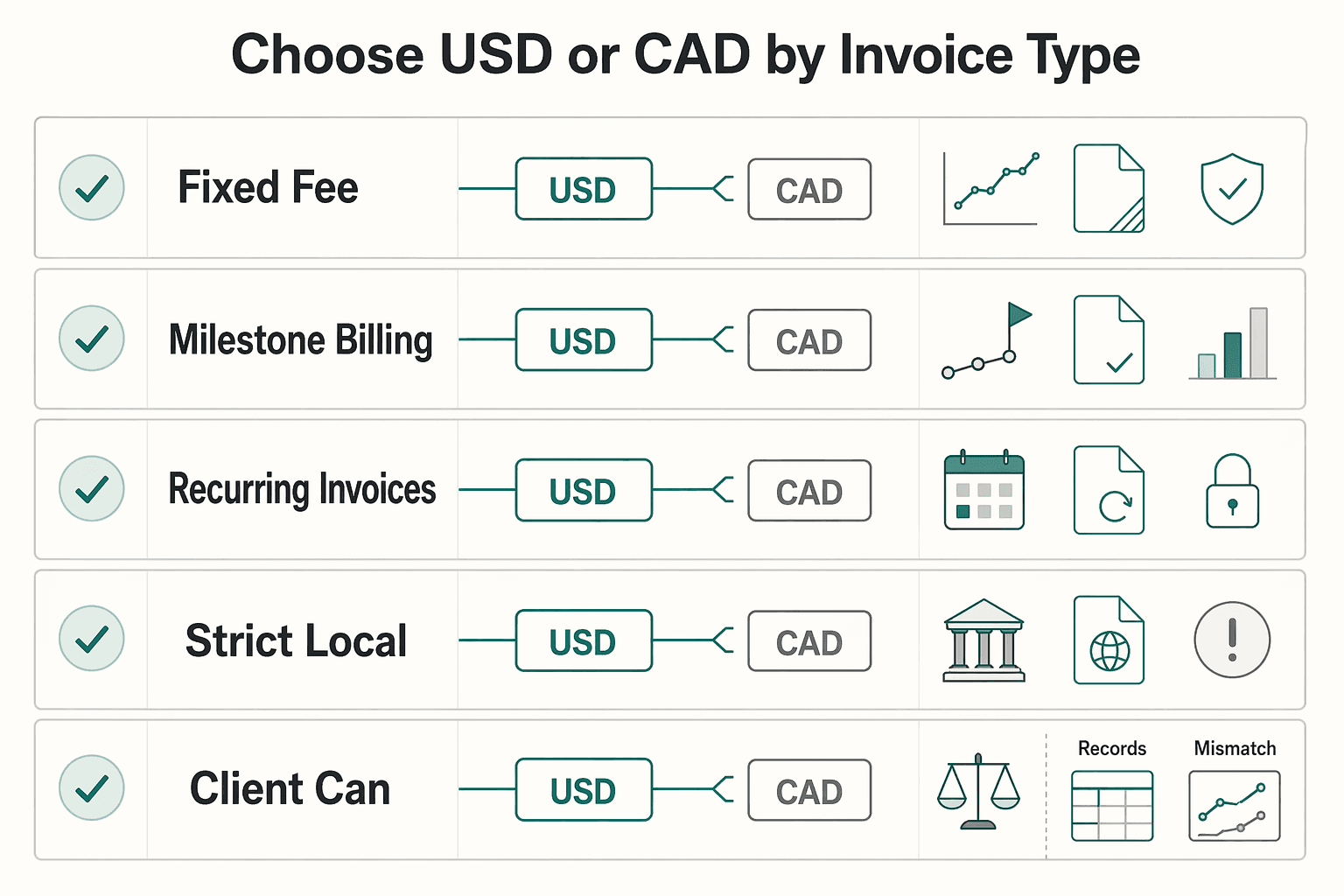

1. Choose USD or CAD by invoice type, not habit#

If margin stability matters most, invoice in USD. That shifts conversion risk to the client and keeps your booked amount more predictable, especially for fixed-fee work and milestone billing.

| Situation | Currency | Reason |

|---|---|---|

| Fixed-fee work | USD | Keeps your booked amount more predictable |

| Milestone billing | USD | Keeps your booked amount more predictable |

| Recurring invoices | CAD | May reduce approval friction, but you own the conversion result |

| Strict local-currency procurement workflows | CAD | May reduce approval friction, but you own the conversion result |

| Client can pay your USD details without forced conversion | USD | Keep USD |

| Client process works cleanly only in CAD | CAD | Either price for that risk or shorten the time between receipt and conversion |

If approval friction matters most, CAD may be more practical. For recurring invoices or clients with strict local-currency procurement workflows, CAD can reduce friction, but then you own the conversion result. You still need USD records for U.S. tax reporting, so keep the conversion details you actually used.

A practical rule: if the client can pay your USD details without forced conversion, keep USD. If their process works cleanly only in CAD, either price for that risk or shorten the time between receipt and conversion. If GST/HST applies, show the applicable GST/HST rate on invoices, receipts, or contracts.

2. Compare rails by total net, not headline fee#

The visible fee rarely tells the full story. FX spread and downstream deductions can materially change what you receive, so compare rails using the same factors every time.

| Payment rail | Visible fees | Exchange-rate spread | Intermediary deductions | Settlement timing | Reconciliation effort |

|---|---|---|---|---|---|

| Bank wire | Example provider fee: $25 digital wire or $40 branch wire | Varies by provider; some banks state their rate includes a markup | Possible; recipient may receive less than sent when third parties deduct fees | Commonly used for large-value, time-critical payments; actual arrival varies | Higher; may require SWIFT or BIC and, by country, IBAN |

| PayPal | Domestic receiving example: 3.49% + fixed fee, plus an additional 1.50% for international commercial transactions | Includes a provider conversion spread | Route-dependent; verify what the recipient will actually receive | Varies by route and wallet setup | Can be moderate; simple intake, but conversion settings can complicate audit trails |

| Multi-currency platform such as Wise | Pricing starts from 0.57% by currency and is shown upfront | Provider states it uses mid-market FX | Route-dependent; confirm deduction behavior before accepting | Varies by route and country | Can be lower when fee and FX details are clearly itemized |

3. Use one net-received calculation every time#

Before you accept a client-preferred rail, run the same net-received calculation every time and save the result with the invoice file.

- Start with the invoice total in the invoiced currency.

- Subtract visible sending, receiving, or platform fees.

- If conversion applies, record the quoted FX rate and compare it to the mid-market benchmark at that time.

- Subtract expected intermediary deductions, or hold a reserve if deductions are possible but unclear.

- Record the expected final credit amount in your home-account currency.

This gives you one comparable net-received number across wires, wallets, and platform transfers. Save the provider quote, benchmark rate check, and remittance confirmation together.

4. Put the money terms in writing before the first invoice#

Payment disputes often turn into documentation disputes, so put the money terms in writing before the first invoice goes out.

| Clause | Include |

|---|---|

| Currency clause | State the invoice currency clearly and keep all line items in that currency |

| Fee-allocation clause | Define who pays transfer, receiving, and bank charges |

| FX-conversion responsibility | State who converts, when conversion happens, and when payment is considered complete |

| Dispute handling | Require payment confirmation and credited-amount evidence for any fee or shortfall dispute |

If a client requires a high-cost rail, use a fallback instead of absorbing the loss. That can mean the same currency on a lower-cost platform, a USD receiving option, or pricing that reflects the required method.

If you want a deeper dive, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Before you lock your payment rail, run your USD-vs-CAD scenarios in the payment fee comparison tool. Choose based on net received, not headline fees.

Conclusion: From Anxious Administrator to Confident CEO#

For your next Canadian invoice cycle, use the same three checks every time: verify the entity, verify the documents, and verify what was credited. That routine can cut avoidable delays and surface issues earlier.

- Compliance

Confirm the billing entity details before you send anything. Keep the contract, invoice, and receiving account details aligned, and re-check them if ownership, structure, or the contracting party has changed.

- Operations

Treat invoicing as a document trail, not a single send. Save a draft invoice PDF before final issuance so you can resolve later questions against a clear record. When the draft, final invoice, and remittance evidence are stored together, payment questions are easier to sort out.

- Finance

Track net outcomes, not just sent amounts. Confirm the credited amount on each payment and file that proof with the invoice.

For the next cycle, keep it simple: confirm the billing entity, refresh the invoice template, restate the money terms in writing, and save the draft PDF, final invoice, and payment proof together. Then repeat the same risk-first habit each time. Document decisions, confirm terms, and review assumptions before every invoice.

For a step-by-step walkthrough, see How to Invoice a US Client from Mexico as a Temporary Resident.

Frequently Asked Questions

1. Can you create a permanent establishment in Canada if you work from the U.S.?

Yes. PE risk can still arise if your operating facts connect your business to Canada. Permanent establishment means a treaty tax nexus, usually tied to a fixed place of business in Canada, a person there who habitually concludes contracts for you, or a construction or installation project that meets the applicable treaty duration test. Even without PE, services physically rendered in Canada can still trigger withholding issues, so track travel, project location, and signing authority and get treaty advice before the next invoice if a trigger appears.

2. Should you invoice in USD or CAD?

Consider USD when you want tighter margin control and easier reconciliation. If the client needs CAD, use it only when your contract states who sets the exchange rate, which date applies, and who absorbs conversion spread or bank fees. | Option | Who bears FX risk | Fee transparency | Reconciliation impact | Client friction | |---|---|---|---|---| | Invoice in USD | Client, unless they convert through your provider | Usually clearer if no conversion happens on your side | Usually easiest to match invoice to credited amount | Higher for clients that budget in CAD | | Invoice in CAD through your bank or PayPal | Usually you | Often weaker because PayPal says its rate includes a retained conversion spread over a base rate | Harder because sent and received amounts can drift | Lower for the client | | Invoice in CAD through a multi-currency provider such as Wise | Usually you, unless contract fixes the rate | Wise says pricing is upfront and it does not inflate the mid-market rate | Better if you keep the quote and payout proof | Lower for the client | Before you lock in the method, run one small live-payment test and save the quote, final invoice, and settlement proof together.

3. Does your client decide whether you charge GST/HST?

No. Your client does not decide this for you. GST/HST is Canada’s federal sales tax system, and your registration duty generally depends on whether you are still a small supplier and whether you make taxable supplies in Canada. Review current CRA guidance as you approach the applicable threshold, and if registration is required, confirm the current CRA rule for when your GST/HST account number must appear on business papers.

4. Do you need a Canadian Business Number before sending invoices?

Not automatically. Business Number (BN) means CRA’s 9-digit business identifier used for tax and program accounts. If current CRA rules require you to open a GST/HST or other CRA account, get the BN then. If not, monitor your Canada-related sales monthly and register if CRA thresholds and taxable-supply tests are met.

5. When should you refresh Form W-8BEN-E, and what if you work in Canada?

Provide Form W-8BEN-E before payment whenever a payer or withholding agent requests it. Form W-8BEN-E is an IRS form foreign entities use to document status for U.S. withholding and reporting, so update it if your entity facts change or if IRS rules require a new form. If you perform services physically in Canada, ask about Regulation 105 early because Canadian payers may need to withhold from gross payments, and waiver or reduction requests should normally be filed about 30 days before services begin in Canada or before the first payment is due. When you finalize your process, use the free invoice generator to keep terms and payment instructions consistent across new Canadian clients.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- consumerfinance.gov/ask-cfpb/i-sent-money-to-someone-in-a-foreig...trusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- files.consumerfinance.gov/f/documents/cfpb_adult-fin-ed_remittance-tra...trusted

- irs.gov/instructions/iw8benetrusted

- irs.gov/forms-pubs/about-form-w-8-ben-etrusted

- lni.wa.gov/licensing-permits/_docs/2026-proposed-WAC-am...trusted

- maine.gov/dep/publications/documents/archive/legislati...trusted

- canada.ca/en/revenue-agency/services/tax/businesses/to...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Best Podcast Hosting Platforms for Beginners

**Pick podcast hosting like an operator: optimize for control, continuity, and clean workflows, not whatever looks appealing on a pricing page.** Podcast hosting is infrastructure. What you choose at signup sits upstream of your RSS feed, Apple Podcasts listing, analytics, monetization options, and how painful it is to change systems later.