Quick Answer

Yes, travel insurance electronics coverage can help, but protection is often limited by caps, exclusions, and filing rules. One example in the article is the WorldTrips Atlas Travel add-on via bolt, which is damage-focused and uses a 30-day claim window. Other routes may apply baggage-style reimbursement or actual cash value, which can leave gaps for high-value work gear. For remote professionals, the best choice is the option with clear limits and claim steps in writing.

Why Electronics Coverage Fails Remote Workers When They Need It Most#

Electronics coverage problems often start before the trip, not only after damage happens. Many trace back to purchase-stage choices: broad labels read as guarantees, eligibility details entered too quickly, or exclusions ignored until a claim is active. If a denied claim would interrupt your income, choose clarity over price from day one.

Use this section in a simple way. Treat every policy page as a draft summary until the certificate confirms the same terms. If the certificate language is harder to understand than the marketing page, slow down and resolve the gap before you pay.

- Benefit labels can look broader than they are: A baggage and personal effects benefit may help with lost, stolen, or damaged gear, including laptops and cameras, but it is not blanket protection in every incident. Marketing language can make two plans look similar even when exclusions and caps differ in ways that matter to remote work. Key differentiator: treat broad labels as a prompt to check exclusions before purchase.

- Residency inputs change quote context: Some insurers use country of residence to show plan details during quoting. A small entry mistake can send you toward wording that does not match your real eligibility path. Key differentiator: enter accurate residence details and keep the quote version you reviewed.

- Late purchase limits options: One travel-insurance source notes that most insurers do not allow purchase after departure, while a smaller group does. Waiting can narrow choices and push you toward plans that are available, not plans that fit. Key differentiator: buy before departure when possible, and verify eligibility first if you are late.

- Theft risk is practical: Tech-safety guidance from a travel insurer frames phone theft as a real risk and gives a

$500resale incentive example. That matters because theft-focused risk can require explicit wording and clear claim requirements, not assumptions based on general trip protection language. Key differentiator: if theft is your top concern, prioritize explicit theft terms and claim requirements over marketing copy. - Exclusions and appeals decide outcomes: SafetyWing policy materials explicitly address exclusions and denied-claim appeals. Ratings such as

4.3/5from5,892reviews can reflect sentiment, but they do not prove payout in your case. Key differentiator: favor clear exclusions and a defined appeal path, then consider preparing ownership proof before departure.

Decision rule for the rest of this article: if one denial would affect your income, prioritize eligibility certainty, written exclusions, and a clear appeals path. Do that before chasing the lowest monthly premium.

If you want a deeper dive, read The Crypto Cautionary Tale: Why Freelancers Should Be Wary of Crypto Payments.

How This List Was Chosen and Who It Fits#

This list ranks options by coverage clarity and eligibility first, then uses price as a secondary check. The goal is protection you can actually use when a device incident disrupts work.

The scoring lens is practical. We assumed you care less about headline pricing and more about what happens after an incident, when time pressure is high and device access is urgent. That pushes wording quality, limits visibility, and document clarity to the top of the ranking.

- Coverage language and exclusions visibility: Plans ranked higher when coverage terms were clear and exclusions were easy to find before purchase. Vague wording or buried exclusions lowered rank quickly.

- Limits and add-on clarity: We prioritized options that clearly explain coverage limits and optional add-ons. A lower premium did not score well if likely reimbursement stayed unclear.

- Eligibility and residence fit (including U.S. constraints where relevant): Eligibility came before pricing because unusable coverage has no claim value. Residence rules and policy-type constraints were treated as major factors, including that some medical-only policies may require primary U.S. health insurance.

- Purchase timing and policy-document clarity: Plans scored better when timing-sensitive benefits and policy terms were easy to understand in plain language. If requirements were unclear, the plan was treated as higher risk even when benefits looked attractive.

How to use this list: shortlist quickly, then run a slower verification pass on the final choices. The shortlist keeps you from reading every policy in the market, but it does not replace policy-level checks.

This list fits remote workers whose income depends on reliable gear outcomes during a move or long stay. It is not built for short leisure trips with low downtime impact, or for readers who only want theft-prevention tips.

Quick Comparison Table for Remote Professionals#

Use this as a shortlist, not a final decision. Comparison roundups can narrow choices quickly, but certificate wording should be verified before you buy.

| Option | Best for | Coverage shape | Main risk to verify |

|---|---|---|---|

| Roundup-style digital nomad travel insurance lists | Building an initial shortlist | Multiple options summarized in one place | Treating roundup language as policy wording |

| Dedicated digital nomad travel insurance comparison sections | Narrowing to a few finalists | Direct side-by-side framing | Missing terms that only appear in the certificate |

| Budget digital nomad insurance comparisons | Price-sensitive travelers | Cheap and flexible plan positioning | Choosing on price before confirming policy terms |

| Head-to-head comparisons (for example, SafetyWing vs Genki framing) | Deciding between two close options | Simple "which is better" decision format | Assuming the comparison answer applies to your exact plan version |

Read the table in this order: fit first, risk second, coverage shape third. Most bad decisions happen when buyers start with headline positioning and skip certificate verification.

- Use the table for a first-pass filter, then validate policy wording line by line in the certificate.

- Do not treat marketing summaries as contract terms.

- Final checkpoint: if one denied claim would disrupt income, prioritize wording clarity over the lowest monthly price.

Best for Travelers Already Buying Atlas Travel#

If you are already purchasing Atlas Travel, this is a straightforward way to add device protection alongside that plan. Treat it as damage-focused protection, not complete coverage for every electronics risk.

WorldTrips describes this as an optional travel medical insurance add-on tied to Atlas Travel for trips starting or ending in the U.S. The published scope here is damage coverage for smartphones, tablets, and laptops while traveling abroad, plus access to bolt's global repair network and 24/7 online claims process.

The key tradeoff is term visibility. This description does not show per-item or per-claim limits, and it does not explicitly state theft terms. It also says claims must be submitted through bolt within 30 days.

For readers who value speed at purchase, this can be a practical starting point. If you carry high-value gear or have strict downtime limits, treat this as one part of your protection, not the full answer. Use it that way until you confirm cap and exclusion details in issued documents.

- Best-fit profile: You are already buying Atlas Travel and want damage coverage for phones, tablets, or laptops while traveling abroad.

- Operational upside: An add-on tied to Atlas Travel plus a

24/7online claims process. - Main risk to verify: Limits, exclusions, and claim requirements in the issued certificate.

- Failure mode to avoid: Missing the

30-dayclaim-submission window.

Before checkout, compare your own device list against what is clearly stated in your policy documents. If trip eligibility (starting or ending in the U.S.) and the filing window are clear and acceptable, this path can remove friction at purchase time. If any one of those points stays unclear, keep it on the shortlist but continue comparing standalone and hybrid options. You might also find this useful: The Best Email Encryption Tools for Freelancers.

Best for Dedicated Device Risk During Long Stays#

For long stays with business-critical gear, do not assume one basic plan will cover everything. Use travel insurance for health and trip disruption, then decide whether you need additional device-focused coverage for hardware risk.

Treat dedicated-device policies as options to evaluate, not full trip protection. That keeps your device decision separate from broader travel benefits and makes cap comparisons easier.

Start with the math. One digital-nomad guide cites a $3,000 personal-electronics example cap on a travel plan. If your laptop-plus-camera setup is above that level, compare additional device coverage alongside travel coverage.

That comparison should focus on where your real exposure sits, not on where plan summaries sound reassuring. If one device represents most of your working capacity, a narrow cap can create a large gap even when a claim is accepted.

Make the final call from the policy packet, not the summary page. Review policy exclusions, check language around professional gear, and confirm claim handling before departure. If replacement cost is your priority, require clear written valuation terms.

A practical way to decide is to run two quick scenarios against each option: a partial-loss event and a full device replacement event. You are not predicting the future; you are testing whether the policy language stays clear when the cost impact changes.

Best for Frequent Business Travel Context#

A single plan network can be convenient for frequent trips, but it only works if electronics terms are explicit in writing before purchase. Some comparison frameworks explicitly include frequent business travelers as a best-fit profile, but profile labels are not proof of fit.

This option appeals to repeat travelers because it can simplify administration across trips. The risk is assuming broad baggage wording protects expensive equipment the way you need it to.

Use hard screening questions before you buy. One 2025 equipment-coverage explainer describes a plan example with a $2,000 baggage loss benefit. In the same example, per-item reimbursement often sat in the $250 to $500 range, and delay benefits often started after 12-24 hours. The same explainer notes reimbursement may use actual cash value, which can track depreciation rather than full replacement expectations.

The practical implication is straightforward. Broad trip language may still leave you undercovered for the specific devices that carry your client work. Convenience is useful, but only after the key electronics terms are clear.

Use this checkpoint before you buy:

- Confirm explicit

theft coveragewording for electronics and any conditions. - Confirm valuation basis in writing:

actual cash valueordepreciationversusreplacement cost. - Confirm how claims are handled when another policy is active.

If these answers are clear and workable for your gear profile, this route can still be efficient for frequent travel. If any answer stays ambiguous, treat this as trip protection and pair it with dedicated device coverage.

Best Overall for High-Dependency Remote Work#

If one week without your main laptop would disrupt income, continuity prep matters as much as the policy itself. For insurance structure, the available evidence here supports careful planning but does not prove one setup is universally best.

For this use case, prepare in three lanes:

- Build a continuity plan for laptop and phone downtime that protects client delivery.

- Use official policy documents and certificates when confirming what is covered.

- Decide your incident-response path in advance, including backup work options and replacement steps.

Use full policy documents and certificates, not summary pages. Verifying details in official documents can reduce last-minute surprises.

Because the evidence here is limited on insurer-specific mechanics, treat policy design choices as case-by-case and confirm terms before relying on them.

Pre-departure checkpoint:

- Confirm your immediate response path for a device incident (workaround, rental, or replacement).

- Keep proof in one place, including purchase records, device details, and condition photos.

- Write a

24-hourreplacement plan for your laptop and phone.

This approach takes more setup, but it can reduce disruption risk when your work depends on fast recovery.

A useful way to keep this manageable is to keep your checklist focused on actions you can take quickly during an incident. Clarity under pressure matters more than a long document you will not use.

Decision Rules for Add-On Versus Standalone Coverage#

Use an add-on only when policy wording clearly fits your device profile. If key terms remain unclear, standalone coverage is usually the safer choice.

| Test | What to confirm | What to keep |

|---|---|---|

| Label test | Exact coverage wording and matching exclusions in the same document set | Coverage wording and exclusions |

| Price test | Your gear list against written item and payout-limit terms, including whether limits increase with an added premium | Written item and payout-limit terms |

| Theft test | Explicit theft coverage wording and claim denial conditions, including unattended-property and hand-luggage requirements | Clarification in writing with your policy copy |

| Jurisdiction and movement test | Eligibility geography before purchase | Description of coverage, full exclusions, limit details, and written clarifications |

Apply the rules below in order. When one test fails, move to the next option instead of trying to interpret unclear language in your favor.

- Label test

If a plan is framed as a travel insurance add-on, treat electronics protection as uncertain until your own documents confirm otherwise. One provider may state coverage for stolen, lost, and damaged gadgets, but that is provider-specific, not a market standard. The practical check is simple: find the exact coverage wording and the matching exclusions in the same document set.

- Price test

Low monthly cost is not enough. Match your gear list against written item and payout-limit terms. If limits can increase only with an added premium, treat low base pricing as a prompt to stress-test the plan. Cheap premiums are helpful only when payout mechanics still fit your real exposure.

- Theft test

If theft is your top risk, require explicit theft coverage wording before purchase. Review claim denial conditions, including unattended-property and hand-luggage requirements. If required evidence is vague, ask for clarification in writing and keep it with your policy copy.

- Jurisdiction and movement test

If you may change countries mid-policy, confirm eligibility geography before purchase and keep written clarification with your policy documents. Keep one folder with the description of coverage, full exclusions, limit details, and written clarifications for edge cases.

The point of these rules is speed and consistency. You should be able to apply them to each shortlisted plan and reach a clear yes or no decision without guessing.

Pre-Departure Evidence Pack That Prevents Claim Friction#

Prepare records before departure, not after an incident. Good documentation does not guarantee approval, but stronger records can help claims get reviewed faster when disputes arise. Treat your evidence pack as a practical readiness step tied directly to filing clarity.

- Build an evidence-linked device inventory

Create one row per device with model and serial details. Attach ownership and purchase proof to the same row, and link each item to a verified photo or video record so it is easy to trace.

- Create one claim-ready folder and make it accessible

Store essential records and claim documents together. Keep access on more than one device, with a backup copy if your primary device fails. If your folder is easy to open when stressed, you are more likely to submit complete information on the first pass.

- Set a replacement continuity plan before departure

Decide how you will keep critical work moving if a primary device is unavailable, including temporary access paths for essential accounts and tools. This step is about continuity while claims are in progress, not waiting for reimbursement before acting.

- Run a final documentation checkpoint

Before your flight, confirm each device entry has clear ownership and purchase evidence, and that file names are consistent so documents are quick to retrieve during filing.

Keep essential records safe, complete, and reachable when you are under time pressure. As a final pass, review the folder from the perspective of incident day. If you cannot find a needed document quickly, reorganize now while stakes are low.

Incident-Day Claim Sequence That Keeps You Operational#

On incident day, order matters. Document first, notify quickly, and confirm how the benefit applies before paying out of pocket.

This sequence is meant to keep your first notice consistent and tied to the terms the cited benefit explicitly states.

- Log the timeline first

Record what happened, where it happened, and when each action was taken so your initial report and follow-ups stay consistent.

- Document the incident details before making payment decisions

Capture clear details about the theft or collision event and keep them organized for claim review.

- Notify the provider with a complete first notice

Report early, and include core details up front. If your policy names a Benefit Administrator, use that contact when scope or process is unclear.

- Confirm coverage position and limits before paying out of pocket

The cited Auto Rental Collision Damage Waiver is described as primary coverage for covered theft or collision damage, with reimbursement up to Actual Cash Value for most rented cars and rental periods up to 31 consecutive days. The cited guide language is in effect as of 11/17/19.

If you need to move fast, keep the sequence simple: document, notify, and verify terms first.

The practical outcome you want is not just a submitted claim. You want a clean claim record and a clearer path while the claim is being processed.

Red Flags That Predict Denied or Underpaid Claims#

Denied or underpaid outcomes can involve unclear status, unclear terms, or weak documentation. Use these checks before relying on any policy.

These examples are useful for triage, but they come from a federal rule-publication excerpt and a medical-billing report, not every policy category.

- Policy text treated as official when it is only informational

If a source says it is not the official legal edition, do not treat it as binding policy text. FederalRegister.gov's displayed prototype states it remains unofficial until ACFR grants official status.

- Rule references without confirming the exact rule and date

Verify the specific rule text and publication details (for example, the DOT "Refunds and Other Consumer Protections" rule dated 04/26/2024), not just a summary line.

- Signs of

downcodingin reimbursement decisions

A reported red flag is claims being downgraded to a lower reimbursement tier automatically.

- Underpayment gaps dismissed because each one looks small

In the reported example, a visit billed at about $170 was paid at about $125 when treated at a lower level, a roughly $45 difference. Small gaps can compound.

- Appeal requirements that depend on strong documentation

When an underpaid claim must be appealed with supporting documentation, weak records increase the risk of unresolved underpayment.

If one denied or underpaid claim would materially hurt you, use a hard filter: avoid options where official status, reimbursement method, and appeal requirements are not explicit in writing.

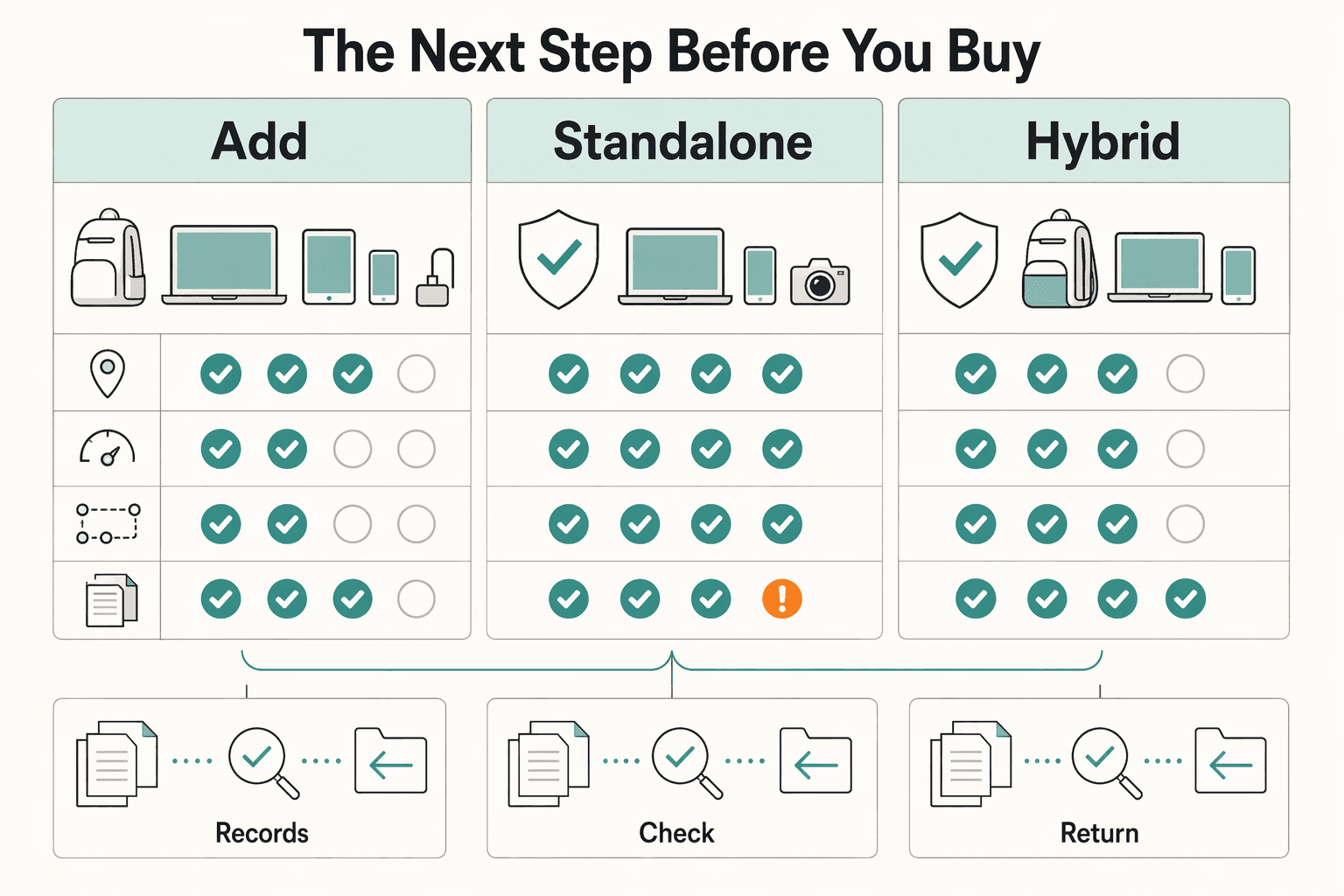

The Next Step Before You Buy#

Shortlist one add-on path, one standalone path, and one hybrid path. Then choose the option with the clearest eligibility, claim mechanics, and payout logic for your route and device inventory.

| Path | Fit | Key details |

|---|---|---|

| Add-on | Already buying Atlas Travel and your route starts or ends in the U.S. | WorldTrips Atlas Travel plan plus bolt device protection; damage to smartphones, tablets, and laptops, including accidental damage; claims through bolt with 24/7 online access; submission required within 30 days; up to $2,000 per plan and up to $1,000 per claim, plus a deductible and a repair or replacement service fee |

| Standalone | Device value is high relative to common travel-policy item limits | Separate gadget policy with overseas cover; can be purchased as a standalone policy rather than as a travel-policy add-on; standard travel insurance can apply single-item limits, typically around £250 |

| Hybrid | One policy cap could leave you short on replacement funds | One travel-plan option plus one standalone device policy; keeps trip-level protection while adding device-focused coverage for primary work hardware; tradeoff: more admin and two policy wordings to manage |

Use the same decision filter for all three: route fit, cap fit, claim-step clarity, and documentation readiness. The option that reads best on a summary page is not always the option that performs best during a claim.

- Add-on path: WorldTrips Atlas Travel plan plus bolt device protection.

- Tied to buying an Atlas Travel plan and currently described for trips starting or ending in the U.S. - WorldTrips says coverage includes damage to smartphones, tablets, and laptops, including accidental damage. - Claims go through bolt with

24/7online access, and submission is required within30 days. - Cap mechanics are up to$2,000per plan and up to$1,000per claim, plus a deductible and a repair or replacement service fee.

- Standalone path: Separate gadget policy with overseas cover.

- Can be purchased as a standalone policy rather than as a travel-policy add-on. - Can be a better fit when device value is high relative to common travel-policy item limits. - A published comparison notes that standard travel insurance can apply single-item limits, typically around

£250.

- Hybrid path: One travel-plan option plus one standalone device policy.

- Practical when one policy cap could leave you short on replacement funds. - Keeps trip-level protection while adding device-focused coverage for primary work hardware. - Tradeoff: more admin and two policy wordings to manage.

Before payment, verify filing requirements in writing: policy wording, claim window, per-claim and plan-level caps, and required incident details. For example, WorldTrips and bolt request IMEI, incident date, and incident details. If your route does not meet the U.S. start or end condition, remove the Atlas add-on path. If your primary laptop value is above a cap you can verify in writing, move to standalone or hybrid.

Final action: pick one primary path and one backup path today, then store the matching policy and evidence files in your claim folder before departure. That single step turns this article into a decision you can execute under pressure.

Frequently Asked Questions

Does travel insurance cover laptops and phones for remote work abroad?

Sometimes, but often through baggage loss, damage, and delay benefits rather than broad device protection. Coverage can be limited, and reimbursement may be based on actual cash value for items lost, stolen, or damaged by a common carrier. Do not assume this matches your full device exposure. Check the exact policy wording before you rely on it for work-critical devices.

What is the practical difference between travel insurance electronics coverage and standalone electronic device insurance?

Travel-plan electronics protection is often tied to baggage rules, limits, and exclusions. Standalone device coverage is a fallback when a travel policy says electronics coverage is limited. The practical difference is claim scope and whether limits fit your actual gear. If your key device value is higher than likely per-item reimbursement, separate coverage is usually the safer setup.

What documents should I collect before departure to file an electronics claim quickly?

Start with the full policy wording and exclusions so you can follow the claim requirements the plan actually sets. Keep those details accessible while traveling, not just on one device. Keep any documentation the policy says is required for a claim. The goal is to avoid guesswork when you need to file fast.

How do I estimate the right coverage amount for a long stay with multiple devices?

Estimate your total at-risk gear value, then compare it against both total baggage benefits and per-item caps. A published example shows how a $2,000 total benefit can still be constrained by per-item limits around $250-$500. Also confirm whether payouts use actual cash value, since that can be lower than replacement cost. If the math is tight for your primary devices, compare separate device coverage options.

Are lost wages covered if my laptop breaks while traveling?

Do not assume they are. One travel-electronics source explicitly says lost wages may not be covered. Treat device coverage and income protection as separate planning problems. Build your continuity plan so work can continue while a claim is open.

When should I buy separate device insurance instead of relying on a travel policy add-on?

Buy separate coverage when your travel policy states electronics protection is limited or when likely per-item limits do not fit your main devices. This is especially relevant if one laptop or camera represents most of your work setup. Separate coverage can also help when travel-plan valuation is based on actual cash value and that payout may not match replacement needs. In that case, pair travel coverage with dedicated device protection.

What policy terms should I verify first to avoid claim denial conditions?

Verify coverage scope, exclusions, per-item limits, total limits, and valuation method first. Also check delay-trigger conditions, since some baggage-delay benefits depend on a window such as 12-24 hours. Confirm the claim requirements listed in the policy wording before purchase. If any of those terms are unclear, keep shopping.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- congress.gov/114/plaws/publ94/PLAW-114publ94.htmtrusted

- federalregister.gov/documents/2020/11/12/2020-24591/transparency...trusted

- federalregister.gov/documents/2024/04/26/2024-07177/refunds-and-...trusted

- gao.gov/assets/a266285.htmltrusted

- alibaba.com/product-insights/why-does-my-travel-insuranc...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Crypto Payments That Protect Cashflow and Reduce Disputes

Crypto payments make sense only when they improve how reliably you get paid after you plan conversion, compliance, and recordkeeping up front. They can reduce friction in some international setups where traditional platforms add fees, restrictions, or extra steps. They also move risk onto conversion timing, exchange-fee exposure, and documentation quality, so use a simple acceptance test before you agree:

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

The Best Email Encryption Tools for Freelancers

You can choose an email encryption route, test it in a real exchange, and keep contract and invoice threads moving.