Quick Answer

Pick a plan that matches your headcount, admin tolerance, and savings target. Solo 401(k) fits owner-only setups seeking higher combined contributions. A SEP IRA offers simple, employer-only funding you can establish by your tax return due date using IRS Form 5305-SEP. SIMPLE IRAs enable employee participation with light administration. Align contributions to cleared invoices to protect cash flow.

How to choose a self-employed retirement plan without breaking cash flow#

Start with the plan you can actually fund without squeezing the business. Most bad retirement decisions by a self-employed owner do not start with the wrong tax idea. They start with a plan that looks good on paper, then collides with payroll, uneven collections, or a hiring change six months later.

A practical first pass uses three filters: who is on payroll now and who is likely to be there in the next 12 months, how much administration you are willing to handle all year, and what savings rate is realistic from net earnings. That usually narrows the field fast. If you are owner-only, a Solo 401(k) is often a strong fit. If income lands unevenly and you want to decide later with cleaner numbers, SEP IRA is often easier. If staff participation is a real goal, SIMPLE IRA should be part of the decision before payroll is already running, not after.

Treat headcount as a forward-looking filter, not a snapshot. Owners often choose based on current payroll and ignore likely hiring or classification changes over the next year. That is how avoidable rework starts. If you already expect staffing changes, build that into the first decision so you do not spend months funding a plan you may need to revisit.

The order matters: structure first, elections second, funding cadence third. Cash pressure usually shows up when owners reverse that sequence. Pick an ambitious savings target first, and weak months start dictating the rest. Choose the structure so the rules are clear, make the elections so contribution types are clear, and only then schedule funding against money that has actually cleared. That keeps retirement saving aligned with the way your business gets paid.

Here is the first-pass screen:

- Solo 401(k): combines employee deferrals and employer contributions from self-employed earnings. For 2024, deferrals can be up to $23,000, plus a $7,500 catch-up at age 50 or older, with total annual contributions up to $69,000 excluding catch-up. If the plan includes a designated Roth account, deferrals are after-tax and qualified distributions are generally tax-free. This is often a strong fit when you expect to remain owner-only and can keep records tight.

- SEP IRA: built for simplicity and late-year flexibility. Contributions follow the IRS special self-employed calculation. Employer contributions may be up to 25 percent of net earnings under applicable rules, and you can establish the plan by your income tax return due date, including extensions. This is often the practical answer when revenue is uneven and you want to make the funding call after the books are final.

- SIMPLE IRA: gives small teams a payroll-deferral path with required employer contributions. It works when employee participation matters and you can budget the employer obligation every year.

- Traditional or Roth IRA: individual accounts that can sit alongside a business plan as a second savings path after the employer-plan choice is made.

Two mechanics deserve attention early because they affect nearly every plan decision. First, plan compensation for a self-employed owner is not the same thing as net profit. You generally reduce net earnings by deductible self-employment tax and by your own contribution before computing the employer amount. Second, if you are age 50 or older, record catch-up elections early so deposits and year-end reconciliation stay clean.

The operating standard is simple: every contribution decision should be reproducible. If someone asks why a number was chosen, you should be able to pull up settled cash, the worksheet, and the election record in a few minutes. That discipline protects cash flow now and cuts down correction work later.

Use these checkpoints before and during funding:

- Run the IRS self-employed contribution worksheet before sending large deposits, then save it with plan records.

- Tie planned transfers to cash that has settled, not invoices that are still open.

- For SEP IRA, calendar setup and funding deadlines by your return due date, including extensions, then make the final funding call after books close.

- For Solo 401(k), complete deferral elections early, stage deposits after major invoices clear, and track catch-up separately from base deferrals.

- Reconcile every transfer to ledger entries and provider statements so corrections stay small.

- Recheck plan fit after any hiring or classification change, because eligibility and cost can shift quickly.

- Keep a short quarter-end note showing planned versus funded amounts and why any adjustments were made.

Once you do that first pass, the rest of the decision gets easier. You are really comparing contribution timing, employee impact, and the amount of year-round recordkeeping you are prepared to maintain. If you want a tighter owner-only comparison, see SEP IRA vs. Solo 401(k): Which is Better for You?. If you want a quick way to tighten billing before setting contribution cadence, try the free invoice generator.

Quick comparison at a glance#

Use this table to screen options, not to make the final call. Headcount and your tolerance for administration should do most of the work up front. After that, confirm the details with your provider and current IRS guidance before you set elections or communicate limits.

| Plan | Best for | Employee participation | Setup timing | Plan features | Admin burden |

|---|---|---|---|---|---|

| Solo 401(k) | Owner-focused when eligible | Check plan eligibility; varies | Varies by provider | Features vary by plan and provider | Varies |

| SEP IRA | Simplicity and late-year funding | Employer contributes for eligible employees | Establish by adopting IRS Form 5305-SEP or a prototype document | Employer contribution only; employees do not defer | Low; no employer filing requirement |

| SIMPLE IRA | Small teams that want participation | Employees may contribute; employer rules apply | Varies by provider | Participation and employer requirements set by rules | Low to moderate |

| Traditional IRA | Individual side savings | Individual account | Varies by provider | Tax treatment depends on current rules | Low |

| Roth IRA | Individual, eligibility-based saving | Individual account | Varies by provider | Tax rules depend on current eligibility | Low |

| Defined benefit plan | Specialized predictable benefits | Possible for owner and employees | Varies and more complex | Provider-structured benefits | High |

| HSA (complement) | Long-term medical savings where eligible | Individual account | Varies by provider | Can complement retirement goals | Low |

If two choices look similar on paper, break the tie with a cash test. Which option lets you fund from settled receipts, and which pushes commitments before revenue is stable? That question resolves more real decisions than another round of feature comparison.

Keep complements separate from the core plan. Defined benefit plans and HSAs can matter in the right setup, but they should not distract you from choosing the primary structure you can actually maintain. Make the core choice first, then decide whether any complement belongs on top of it.

The easiest way to use the table is a two-pass method. Pass one eliminates plans that do not match your headcount reality. Pass two ranks what is left by administration load and funding flexibility. That keeps the decision practical and reduces the temptation to over-index on features you may never use.

Before the plan-by-plan sections, start with the option most often treated as "simple enough to handle later." That is usually SEP.

SEP guardrails that matter#

SEP is simple, but it is not casual. The paperwork load is lighter than with some other options, yet the controls still matter: eligibility, compensation data, contribution math, and a plan file you can reproduce later. A common failure mode is treating low admin burden as if it means low discipline. In practice, that is how cleanup work starts.

Keep these guardrails in view:

- SEP can be used by businesses of different sizes, including self-employed owners.

- You can establish it by adopting IRS Form 5305-SEP or a provider prototype agreement.

- Only the employer contributes to SEP-IRAs. Employees do not make salary deferrals into SEP.

- SEP-IRA balances are fully vested for employees.

- Employers generally do not have an annual filing requirement for the SEP itself.

- Contribution room is compensation-based and can be up to 25 percent under applicable IRS rules.

- If you use Form 5305-SEP, you cannot maintain another retirement plan other than another SEP.

The practical mistake to avoid is scattering SEP records across inboxes, payroll folders, and provider portals. Keep plan adoption, eligibility support, calculations, and proof of funding in one place. When the record trail is centralized, year-end verification is faster and small errors are easier to catch before they turn into bigger ones.

Before you fund anything, confirm provider deadlines and your calculations against IRS Publication 560, then store the signed plan document, your contribution worksheet, and provider confirmation together. It is a small habit, but it prevents a lot of last-minute repair work.

Once you see why SEP still needs structure, it is easier to evaluate the owner-only alternative on its real merits rather than on marketing language alone.

Solo 401(k) when no employees and higher limits matter#

Choose Solo 401(k) when you are owner-only and you want both contribution lanes. That is the real edge here: employee deferrals plus employer contributions from self-employed earnings. For 2024, deferrals can be up to $23,000, with a $7,500 catch-up at age 50 or older, and total annual contributions are capped at $69,000 excluding catch-up.

What makes this plan attractive in practice is control. You can set a deferral approach, pace employer funding around collections, and, if the written plan offers it, use designated Roth deferrals for after-tax contributions with qualified tax-free distributions later. That flexibility is useful only if records are clean. Late elections or loose calculations turn a strength into correction work.

Before you open the account, read the written plan document rather than relying on provider marketing pages. Some plans allow pre-tax deferrals, designated Roth deferrals, loans, or hardship distributions. Others do not. If a feature is unlikely to matter to you, skipping it can reduce complexity and make ongoing administration easier. The best plan is not the one with the longest feature list. It is the one you can run accurately quarter after quarter.

The math is where most overfunding mistakes begin. Employer nonelective contributions are generally up to 25 percent of compensation as defined by the plan, but self-employed owners have to use the IRS special method in Publication 560. The calculation is circular because compensation is net earnings reduced by deductible self-employment tax and reduced again by the contribution itself. This is where owners often treat net profit as plan compensation and overshoot. Run the worksheet every time and keep it with the funding record.

Election timing deserves the same rigor as contribution math. Deferral intent that is not documented in time does not become valid just because you meant to do it. Put election dates on your planning calendar, save confirmations when they happen, and keep one reference sheet showing which contribution type each transfer belongs to. That one-page view clears up a surprising amount of confusion during quarter close and tax preparation.

A funding sequence that holds up in real businesses usually looks like this:

- Complete deferral elections early in the year or before the funding period.

- Stage larger transfers after major client payments settle when receivables are volatile.

- Calculate employer amounts from the Publication 560 self-employed worksheet and save the output.

- Track catch-up deferrals separately from base deferrals if you are age 50 or older.

- Reconcile each transfer to invoice receipts, bank entries, and provider statements.

- At quarter end, compare year-to-date contributions to your target and adjust while gaps are still small.

The red flags are predictable, which is good news because predictable problems are easier to prevent:

- Flat 25 percent applied to net profit: rerun the self-employed worksheet and coordinate corrections with the provider.

- Hiring changes ignored: if you add a W-2 employee, reassess plan eligibility and design before additional deposits.

- Feature assumptions: do not assume loans or hardship options exist in every plan. Confirm them in the signed document.

- Mismatched records: if ledger totals and provider statements drift, pause new transfers until the tie-out is clean.

If a problem does show up, fix the sequence first. Confirm elections, rerun the calculations, then reconcile the deposits. Owners who jump straight to amended transfers without checking the underlying election trail often end up doing the work twice.

Solo 401(k) usually wins when owner-only contribution room is the priority and you are prepared to keep disciplined records. If staffing may change soon or you want the easiest late-year funding call, compare it again with SEP IRA and SIMPLE IRA before you lock in your pace for the year.

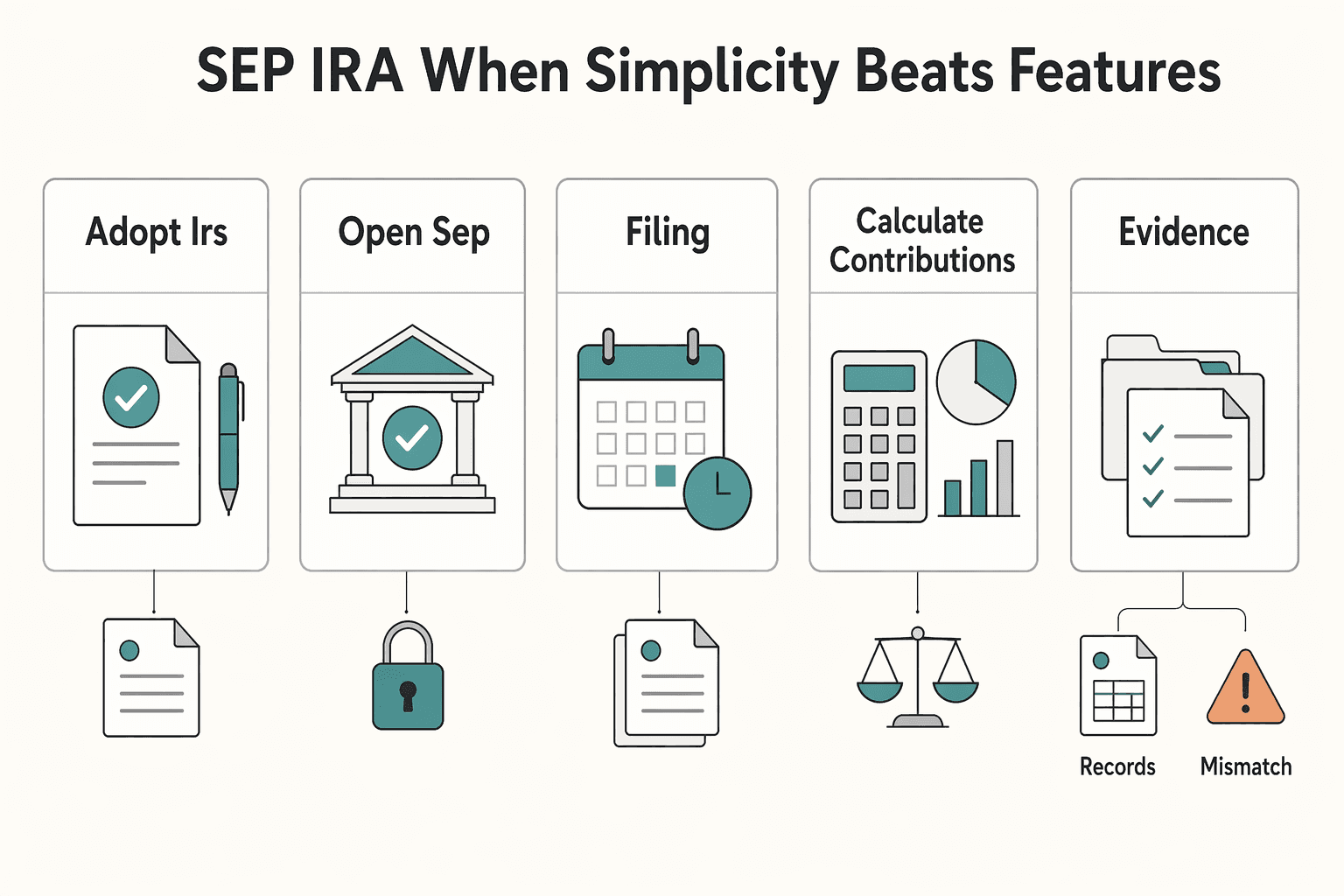

SEP IRA when simplicity beats features#

Choose SEP IRA when simple setup and late-year funding flexibility matter more than extra features. Its biggest advantage is timing. You can establish the plan by your tax return due date, including extensions, and fund with finalized numbers instead of estimates. Adoption is typically done through IRS Form 5305-SEP, which you keep in your records, or through a provider prototype agreement.

That simplicity comes with a tradeoff: contribution uniformity. If you contribute for yourself, you generally contribute the same percentage of compensation for each eligible employee. That rule is easy to miss when hiring happens late in the year or worker status changes midyear. Before you set a contribution percentage, verify eligibility and compensation inputs. Miss one eligible participant and a straightforward plan turns into a cleanup project.

The easiest way to reduce that risk is a short eligibility review right before funding. Confirm who qualifies, confirm the compensation data, and confirm that your intended percentage is applied consistently across eligible participants. It does not take long, and it is far easier than repairing a missed allocation after deposits are already in motion.

SEP still offers meaningful contribution capacity. Employer contributions are based on net earnings from self-employment and may be up to 25 percent under applicable rules, with a 2024 cap of $69,000. The real control point, though, is documentation. Keep the adoption paperwork, participant account details, calculation worksheet, and deposit confirmations tied back to your ledger. A contribution number is only useful if you can trace it later without rebuilding the story from memory.

The key decision checkpoint is when your numbers become reliable. If your books usually finalize late and receipts are uneven, SEP often fits better because the funding decision can wait until the picture is stable. If you need in-year deferrals or broader plan features, Solo 401(k) may still be stronger even with more administration.

A simple setup and funding sequence helps keep year-end clean:

- Adopt IRS Form 5305-SEP or a provider prototype and store the signed copy in your plan file.

- Open SEP-IRA accounts for yourself and each eligible employee before funding.

- Put setup and funding deadlines on your tax calendar and recheck them as filing approaches.

- Calculate contributions from finalized net earnings after books close.

- Document the uniform contribution percentage and keep support for eligibility determinations.

- Match each deposit date and amount to provider statements and internal ledger entries.

- Prepare a short year-end summary that ties total SEP deposits to final compensation data.

After deposits post, do one final tie-out before you close the year: contributions sent, contributions received, and contributions recorded in the books. That final pass often catches small posting mistakes while the records are still fresh.

Two operating guardrails matter most for cash flow. First, do not lock in aggressive deposits before revenue settles. Second, review hiring and classification changes early, because even one additional eligible employee raises total outlay at the same percentage. Choose SEP when late-year flexibility and employer-only funding are the priority. If owner-only contribution headroom is the main goal, compare it again with Solo 401(k). For a direct owner-only breakdown, see SEP IRA vs. Solo 401(k): Which is Better for You?.

When employees need a payroll-deferral path rather than employer-only funding, that is usually when SIMPLE IRA moves to the front of the discussion.

SIMPLE IRA for small teams that want participation#

Choose SIMPLE IRA when employee participation matters and you need a plan you can run without a heavy annual filing burden. It gives employees a payroll-deferral path and requires an employer contribution. It is commonly adopted with IRS Form 5304-SIMPLE or 5305-SIMPLE, and while it is active you generally cannot sponsor another retirement plan. Be explicit about that before setup because it affects what you can do later.

This option works best when you treat the employer contribution as a recurring payroll cost, not as an aspirational target. Each year, you choose one formula: match up to 3 percent of compensation or make a 2 percent nonelective contribution for each eligible employee. Once you choose, budget it as a standing cost. If cash is consistently too tight to cover that amount, the problem is not communication. The problem is that the plan may not fit the business.

Execution depends heavily on clarity. If employees do not know how to change deferrals, or payroll does not have a clean path for handling errors, corrections pile up at year-end. A short written summary usually prevents most of that. Keep it practical: the employer formula, the deferral-change process, the deadlines, and one internal contact for issues. You do not need a long handbook. You need one version of the truth.

In day-to-day use, SIMPLE IRA runs more smoothly when payroll, accounting, and provider records are reconciled on a fixed rhythm. Build that rhythm early. For most small teams, a monthly check is enough: compare payroll deductions to provider receipts, resolve small mismatches right away, and save the tie-out note. Small monthly fixes are easier than one large year-end cleanup.

Cash flow is often easier to manage here than with owner-only lump-sum funding because employee deferrals move with payroll and employer amounts can be scheduled alongside them. That makes the cost visible throughout the year instead of concentrating it in one late decision. If a weak quarter hits, cut optional spending first and protect required contributions.

A clean launch sequence keeps the plan from becoming an administrative distraction:

- Adopt the plan using IRS Form 5304-SIMPLE or 5305-SIMPLE and keep the signed documents together.

- Collect employee deferral elections before the first active payroll period.

- Configure payroll codes before live runs and verify account mapping to SIMPLE IRA destinations.

- Run a test payroll to confirm percentages and contribution types before first real deposits.

- Publish the internal summary with the employer formula, election process, and correction contact.

- Save annual notices, signed forms, payroll reports, and provider confirmations in one file.

- Reconcile payroll registers to provider statements at year-end with spot checks back to signed elections.

Keep the communication cadence simple too. Reconfirm deferral-change instructions and correction contacts at least once before year-end so employees and payroll are not guessing during close. That small reminder lowers noise and improves deposit accuracy.

Exact annual dollar limits and provider cutoff dates for SIMPLE IRA change periodically. Confirm those with your provider and current IRS guidance before you communicate caps to employees.

Use SIMPLE IRA when you want participation for a small team and can fund the employer commitment consistently. If the business shifts back toward owner-only operations or you decide employer-only flexibility matters more than participation, reassess SEP IRA and Solo 401(k) rather than carrying the wrong plan by inertia.

Traditional vs Roth IRA that stack with business plans#

Treat IRAs as the second layer, not the starting point. Decide the business plan first, then use a Traditional IRA or Roth IRA to add flexibility and keep savings moving in weaker months. That order lets the higher-capacity employer plan do the heavy lifting while preserving a personal savings path you can keep funding consistently.

Keep one distinction clear because it causes frequent confusion: a Roth IRA is an individual account, while a designated Roth account in a 401(k) is a plan feature. In a 401(k), designated Roth contributions are taxable when made and qualified distributions are generally tax-free. If your Solo 401(k) includes designated Roth deferrals, document that election in the plan file before you add IRA deposits. Clear separation up front avoids tax and recordkeeping confusion later.

A practical funding order usually works best:

- Set business-plan elections and targets first.

- Fund required or priority employer-plan amounts based on current cash and finalized calculations.

- Use remaining capacity for Traditional IRA or Roth IRA contributions based on eligibility and tax planning.

- Keep a minimum IRA contribution level that survives weaker months, then add top-ups in stronger months.

For Solo 401(k), the same 2024 anchors apply: a $23,000 employee deferral, a $7,500 catch-up at age 50 or older, employer contributions based on self-employed earnings, and a combined cap of $69,000 in 2024 excluding catch-up. Use those numbers as planning anchors only if they are the same numbers you are documenting in your operating file for the same year.

This layering works because it separates must-do items from adjustable ones. Employer-plan commitments and eligibility-driven choices stay at the center. IRA deposits become the flexible piece that can expand in strong months and contract in weak ones without breaking the overall saving plan.

It also helps you avoid all-or-nothing behavior. If business-plan funding has to pause briefly because of cash timing, a smaller IRA deposit can still preserve momentum without forcing overcommitment. With uneven income, consistency usually matters more than intensity.

Verification should stay simple. Reconcile IRA deposits quarterly to provider records, keep confirmations with year-end statements, and store owner-contribution calculations for Solo 401(k) or SEP decisions in the same file. Keep Publication 560 references with your contribution log so you can support the math later without recreating the analysis from scratch.

IRAs do not replace the business-plan decision. They make the overall approach more resilient by adding a second savings path and, where appropriate, tax diversification. If you want a practical budgeting companion, see Financial Management for Freelancers: Budgeting, Saving for Taxes, and Retirement.

Funding with uneven invoices#

Fund retirement contributions from cleared cash, not forecasted revenue. That one rule does more to protect operations than most optimization ideas. When receivables slow down, protect required obligations and operating liquidity first, then restart optional saving when cash normalizes.

| Plan | Funding timing | Cash-flow note |

|---|---|---|

| SEP IRA | Funding decision can wait until books close; the plan can be established by the tax return due date, including extensions | Often fits better when books finalize late and receipts are uneven |

| Solo 401(k) | Deferral elections need to be in place and deposits can be staged after major invoices settle | Can still work well with uneven collections if election steps are not late |

| SIMPLE IRA | Employee deferrals move with payroll and employer amounts can be scheduled alongside them | Makes the cost visible throughout the year instead of one late decision |

Plan choice matters most when invoices are irregular. SEP IRA often feels easier because employer contributions can be set after books close. Solo 401(k) can still work well with uneven collections, but only if deferral elections are already in place and deposits are staged after major invoices settle. If the election steps are late, you lose part of the control that makes the plan useful.

A common mistake is treating retirement saving like a fixed monthly bill when collections are variable. It can look disciplined on paper and still create pressure in real life. A better pattern ties deposits to settlement events. Save when cash is real, not when an invoice is still optimistic.

Use a cadence you can repeat each quarter:

- Record income when funds clear, not when invoices are issued.

- Move money in a consistent order: required obligations, operating buffer, then retirement contributions.

- Maintain a multi-month operating reserve before optional top-ups.

- Pause optional transfers during thin periods and protect required plan commitments.

- Increase deposits in stronger periods and update annual targets based on actual pace.

- At quarter end, compare funded amounts with plan targets and adjust next-quarter pacing.

If a quarter closes below target, avoid catch-up panic. Recalculate based on the remaining year, keep required commitments intact, and spread adjustments across later strong periods. That keeps operations steady and lowers the odds of forcing contributions at the wrong time.

Documentation is the control layer that keeps corrections small. For each transfer, keep the bank record, provider confirmation, contribution type, invoice reference, and date in one log. That makes true-ups faster and exposes errors while they are still easy to fix.

Keep a short exception log for unusual months. Note why a contribution was paused, reduced, or increased and what trigger will restart normal pacing. That gives you a cleaner basis for the next quarter's decision instead of relying on memory.

One more boundary matters here: keep unrelated reporting tasks on their own track. Form 8938 is filed with your income tax return for specified foreign financial assets when thresholds apply. It does not replace FBAR, which is filed separately as FinCEN Form 114. Keep those checklists separate from retirement funding records so reporting work does not get mixed up with contribution control.

Once contributions are tied to real cash, the next job is making sure the paperwork trail is strong enough to support every deposit without reconstructing the year from memory.

Open, document, and maintain a compliant plan file#

Your plan file should be boring. That is a good thing. It should also be complete and easy to review. The goal is simple: every contribution ties back to plan documents, bank movement, provider statements, and your books without guesswork. Build one index page, use consistent naming, and store records so someone else could follow the trail in one pass.

| Plan | Core documents | Key records |

|---|---|---|

| Solo 401(k) | Written plan document; trust or custody details; amendments | Provider confirmations; election records |

| SEP IRA | Signed adoption paperwork; participant account setup records | Contribution calculations; deposit confirmations |

| SIMPLE IRA | Adoption forms; annual notices | Payroll election records; contribution reports; provider correspondence |

Treat the file as an operating tool, not as a year-end archive. Good records reduce stress before filing, make corrections faster when something changes midyear, and keep decision-making grounded because you can see what has already been elected, funded, and reconciled. If another reviewer had to validate your contributions tomorrow, they should be able to move from election to transfer to tie-out without asking where anything lives.

Start with the core documents for the plan you actually use:

- Solo 401(k): written plan document, trust or custody details, amendments, provider confirmations, and election records.

- SEP IRA: signed adoption paperwork, participant account setup records, contribution calculations, and deposit confirmations.

- SIMPLE IRA: adoption forms, annual notices, payroll election records, contribution reports, and provider correspondence.

Across all plans, keep IRS Publication 560 references with the worksheets used for each funding cycle. Add a running contribution log with invoice IDs, dates, contribution type, amount, and destination account. If your business uses internal approvals, store those notes too so election authority and change history are easy to follow.

The exact folder labels matter less than consistency. What matters is that the structure does not change every quarter. Keep separate subfolders for plan documents, elections, funding proof, and reconciliation summaries, or something equally clear. Consistency is what makes quarter-end review fast when time is short.

Election records deserve extra care because undocumented changes create more cleanup than bad arithmetic. If your Solo 401(k) includes designated Roth deferrals, record the election date and confirmation. If the plan allows loans or hardship distributions, confirm that from the written plan and retain related approvals. If catch-up treatment applies, show it separately from base deferrals in your log.

Do the annual review on a calendar, not by memory. Reconcile contributions to provider statements, bank records, and ledger totals. Cross-check self-employed net earnings and Schedule SE outputs against contribution calculations. Confirm required minimum distribution handling where applicable and save the evidence. Most important, keep the exact worksheet used each time so the math can be reproduced later without reconstruction.

A quarterly evidence pack makes this manageable and prevents drift:

- Quarter contribution log with dates, types, and amounts.

- Provider statements showing posted deposits.

- Tie-out summary from contribution totals to ledger balances.

- Any plan amendments active during that quarter.

- Notes on corrections made and proof they were closed.

The same failure points show up repeatedly. Missing confirmations, election updates with no record trail, and late funding changes without updated logs show up again and again. Deal with them immediately. If you adjust SEP funding near filing, add the final provider confirmation and ledger report the same day. If Solo 401(k) feature usage changes, capture the supporting plan terms and approvals with that quarter's file.

A short year-end close memo is the last control worth keeping. State what was funded, what changed, and where the supporting records live. That is not extra bureaucracy. It is a practical handoff to your future self when the next planning cycle starts.

Pick one and schedule funding against real cash#

Pick the plan you can run consistently in normal months and thin ones. The right choice is not the highest theoretical limit. It is the structure that fits your headcount, your tolerance for administration, and the way cash actually arrives in the business. Once that choice is made, complete elections early and fund against settled receipts.

A simple filter keeps the decision grounded:

- Solo 401(k): owner-only option for businesses with no employees other than a spouse. Before funding, confirm current deferral limits, combined caps, filing requirements, and feature availability with your provider.

- Traditional or Roth IRA: personal accounts with lighter administration. These work well as steady baseline contributions when business cash flow dips.

- SEP IRA or SIMPLE IRA: revisit these when staffing changes, employee participation becomes a priority, or employer-only flexibility matters more than feature depth.

Then turn that choice into a routine. Set contribution elections first so destinations and contribution types are unambiguous. Schedule deposits from real cash movement, not optimistic receivable timing. Reconcile quarterly against provider statements and your books. Maintain one compliance folder with adoption records, election confirmations, funding logs, and account statements. If you use a Solo 401(k), include a year-end check on plan asset value and any required filings.

If your operations span multiple countries or entities, line up reporting and funding records with the same books-close cycle. Use provider exports that support tax-ready statements when available, and archive them with quarter-end files so the year is easy to reconstruct.

Most owners do not need a more elaborate process than one review checkpoint each quarter. Verify plan fit, verify funding pace, and verify documentation quality. That single habit keeps small issues from turning into expensive year-end corrections.

Before the next calendar year begins, write a short decision memo with your chosen plan, target pace, and the triggers that will make you slow, pause, or increase funding in thin months. That memo reduces indecision during busy periods and makes delegation easier if someone else supports the books.

Bottom line: choose the plan you can actually administer, fund it from cleared cash, and reconcile it every quarter so saving stays reliable even when revenue timing is not. Want help mapping this to your setup? Talk to Gruv.

Frequently Asked Questions

What are the main self-employed retirement plans?

The core lineup is SEP IRA and Solo 401(k). A Solo 401(k) is generally for an owner-only business with no employees apart from a spouse.

How much can I contribute as a self-employed person?

For a Solo 401(k), the 2024 employee salary deferral limit is $23,000, with an additional $7,500 catch-up if age 50 or older. You may also contribute up to 25 percent of net earnings from self-employment, for total 401(k) contributions of $69,000 in 2024. For a SEP IRA, employer contributions can be as much as 25 percent of net earnings, up to $69,000 in 2024.

When is the deadline to set up a SEP IRA?

You can establish a SEP as late as the due date of your income tax return for that year, including extensions. Many providers implement this with IRS Form 5305-SEP or comparable adoption documents. Keep the signed agreement and provider confirmations in your plan file.

Who should choose a Solo 401(k) vs a SEP IRA?

Pick a Solo 401(k) for an owner-only business with no employees apart from a spouse and when higher combined contributions matter. Choose a SEP IRA when you want simplicity and the ability to base employer funding on net earnings, with the flexibility to set up by your return due date.

Are IRAs still useful if I’m self-employed?

A SEP IRA is a traditional IRA and follows traditional IRA rules.

Do self-employed retirement accounts require RMDs?

It depends on the account type and current law. Confirm the current requirement for your plan before year-end planning. These answers give working numbers and dates where supported and keep choices practical. Keep your records tidy so limits, deadlines, and elections are easy to verify at year end.

Watch

Best Retirement Plans for the Self-Employed

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Financial Management That Protects Cashflow First

Stabilize cash timing first. Perfect budgeting can wait. When payments arrive unevenly, the immediate win is a repeatable way to see what came in, what needs to be set aside, and what is actually safe to spend this week.

SEP IRA vs Solo 401(k) for Freelancers With Uneven Cash Flow

Pick the plan you can keep funding in weak months, not the one that looks best in a strong quarter. That is the real decision.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.