Quick Answer

The best personal finance books for freelancers are the ones that match your current payment bottleneck and lead to one immediate operational change. Use titles like The Psychology of Money, I Will Teach You to Be Rich, Get a Financial Life, and Die with Zero as inputs, then convert each into a concrete control: clearer terms, tighter invoicing cadence, stronger follow-up, or a written runway rule.

Stop "reading about money" and build a Freelancer Money Playbook (so you get paid on time)#

If you run a business-of-one, you're not here for vibes; you're here for a repeatable system you can run.

Build a simple money playbook that turns financial education into actions you can run the same way every time. You do not need more opinions. You need defaults, checklists, and "when X happens, do Y" rules.

Most roundups of the "best personal finance books" stop at what to think. You need what to do: a system you can execute under pressure, when the numbers are messy and the choices are framed to steer you.

One Harvard Journal of Law & Technology article argues that perceptions of pricing can get disconnected from reality, in part when people ignore behavioral economics and "dark patterns" that contribute to "consumer misperception." Translation: do not outsource your decisions to vibes, rankings, or snippets. Build your own controls.

What this list actually solves (and what it avoids)#

Money stress is often about timing and friction: bills hit before you feel "ready," fees creep in, subscriptions pile up, and pricing is presented in ways that can blur the true cost. This list treats money like operations, not entertainment.

You will not get stock tips here. You will get a way to turn personal finance reading into routines that keep your decisions consistent.

This list is for readers who:

- manage recurring bills and irregular expenses and want safer defaults

- deal with fees, subscriptions, and "small leaks" they keep meaning to fix

- prefer checklists over "motivation"

This list is not for people chasing a "one weird trick" or readers who only want investment-picking content.

Selection criteria: every book must map to an operational artifact#

A Medium writer claims, "I read 47 money books in 2 years." You do not need that. You need a smaller set where each title produces at least one concrete upgrade you can implement quickly.

| Operational need | What you create after reading | Safe default output |

|---|---|---|

| Spending decisions | A pre-purchase checklist | "Wait and re-check total cost" rule |

| Fee control | A fee review habit | Monthly "fees and subscriptions" sweep |

| Price and choice framing | A decision guardrail | "Compare like-for-like and avoid default add-ons" rule |

| Long-term planning | A transfer-and-review cadence | Automatic transfers + scheduled reviews |

Hypothetical scenario: you are about to click "buy," and the checkout flow nudges you toward an add-on, a subscription, or a "limited-time" upgrade. You do not debate. You open your playbook, run your checklist, and decide fast whether it is worth it.

Which book should you read first if getting paid is the bottleneck?#

There is not one universally "right" first book here. Start with the resource that matches why payments keep breaking, then install one simple control that makes getting paid repeatable.

Choose by bottleneck (not by popularity)#

- Inconsistent client payments (late payers, vague terms, awkward follow-ups) Pick something practical on payment terms, receivables, and collections. Operator move: set one default you do not renegotiate on every project (for example: clear payment terms, an upfront deposit policy, and a consistent follow-up process).

| Bottleneck | Start with | Immediate control |

|---|---|---|

| Inconsistent client payments (late payers, vague terms, awkward follow-ups) | Something practical on payment terms, receivables, and collections | Set clear payment terms, an upfront deposit policy, and a consistent follow-up process |

| Self-sabotage in high months (behavior beats math) | Something on money psychology and decision-making under uncertainty | Create a pay-yourself rule and separate business cash, taxes, and spending |

| Cash flow is fine, but profit feels random | A guided, implementation-style resource such as The Profit Answer Man podcast | Schedule a recurring money review and make one small, repeatable change each cycle |

| You make money, but you do not build wealth | Low-cost, diversified index fund basics associated with Jack Bogle/Vanguard | Keep the plan simple and consistent, and automate investing only once cash flow is stable enough |

| Stable, but you want better tradeoffs | Something that forces explicit prioritization and tradeoffs | Write a runway policy and a spending rule you can defend when the month gets emotional |

-

Self-sabotage in high months (behavior beats math) Pick something on money psychology and decision-making under uncertainty. Operator move: create a simple "pay yourself" rule and separate your money so it is harder to blur business cash, taxes, and spending.

-

Cash flow is fine, but profit feels random (you need a system) If you want a guided, implementation-style resource, The Profit Answer Man podcast is described as a weekly show hosted by Rocky Lalvani, a business coach and Certified Profit First Professional, focused on scaling profit and cash flow for 7-8 figure businesses. Operator move: schedule a recurring money review and make one small, repeatable change each cycle (categories, timing, and rules you can actually keep).

-

You make money, but you do not build wealth (long-term investing clarity) When you are ready for investing education, learn the basics of low-cost, diversified index fund investing associated with Vanguard founder Jack Bogle. The excerpt notes Bogle launched his first groundbreaking retail index fund in 1976, and that Vanguard's index funds have "always had a low threshold for entry" (no dollar amount is specified). Operator move: keep the plan simple and consistent, and only automate investing once cash flow is stable enough to support it.

-

Stable, but you want better tradeoffs (time vs money) Pick something that forces explicit prioritization and tradeoffs. Operator move: write a runway policy (what "safe" looks like for you) and a spending rule you can defend when the month gets emotional.

Fast decision rule (use this today)#

| If your reality is... | Read first | Install this control immediately |

|---|---|---|

| Late payers drive stress | A practical guide on payment terms and collections | Clear terms + a consistent follow-up process |

| You overspend in good months | Money psychology / behavior | Pay-yourself rule + separated buckets/accounts |

| Profit feels random | A system-focused profit/cash-flow resource (or Profit Answer Man) | Recurring money review + one repeatable rule |

| You want to build wealth long-term | Index-fund basics (Jack Bogle/Vanguard context) | Simple, consistent plan once cash flow is stable |

| You want intentional spending | Tradeoff-focused personal finance | Runway policy + explicit priority rules |

Quick comparison table: book → core lesson → freelancer application → first action#

Pick one investing or personal finance book from a credible "core collection," extract one core lesson, and install one small control today. The goal is not "finish the book." The goal is "install the control."

A practical place to choose from is the UF Business Library's investing page, which describes itself as a core collection of books on all aspects of investing and also includes an Investment Books: A-Z section.

How to use this (so you actually get momentum)#

Popularity signals tell you what is popular, not what works for your workflow. Choose one title, do the first action immediately, and save it as a reusable template.

Timebox the task to a short sprint. If you finish early, stop. If you run long, capture the next step in one sentence and schedule it. James M. Barrie's line, "Life is a long lesson in humility," fits here. Your money system gets better through small iterations, not heroic overhauls.

Table (drop into your notes; treat it like a mini system)#

| Book (pick one from a core collection or A-Z list) | Core lesson (your extraction) | Freelancer translation (your context) | First action (timebox a short sprint) |

|---|---|---|---|

| [Title you chose] | What's the 1 repeatable idea? | Where does this show up in my cashflow/admin/pricing? | One tiny control I can install today |

| [Title you chose] | What behavior/system is it pushing? | What part of my workflow needs that most right now? | Draft the checklist / rule / template |

| [Title you chose] | What would "good enough" look like? | What would make next month less fragile? | Set it up once, save it, reuse it |

| [Title you chose] | What's the simplest version? | What can I standardize across clients/projects? | Write the default line / default term |

| [Title you chose] | What would I stop doing? | What's creating avoidable whiplash? | Remove one step / cancel one unused thing |

Best personal finance books for freelancer cashflow, budgeting, and "don't-go-broke" systems#

Pick one book (or book list) you will actually finish, then pair it with one control you can run this week. Treat reading as financial education you operationalize, not inspiration you consume.

Decision rule (so you choose fast)#

Use this filter. It keeps you out of "reading about money" mode.

| If your issue is... | Install this control in your ops |

|---|---|

| Decision fatigue, inconsistent savings, spending swings | A simple "payday" rule: when money lands, move a pre-decided share to savings before you spend |

| Your bank balance feels fine until bills hit | Separate "buckets" (separate accounts or a simple tracking setup) so money has a job before it disappears |

| You need baseline money hygiene and admin habits | One folder + one tracker: keep invoices/receipts together and track what's been paid vs. what's still owed |

| Consumer debt eats your runway and raises your stress floor | Cut fixed costs first, then tighten payment expectations so you are not financing other people's timelines |

| You underprice your time and overbuy tools | Price with your real time cost in mind, and bill in milestones to reduce payment-delay risk |

Where to find book lists and formats (without overthinking it)#

| Source | What it shows | Grounded detail |

|---|---|---|

| Lemon8 | "Books That Help You Get Rich" topic feed | Shows "Last updated: 2026/03/02" and "liked by 75.9K people" |

| Everand | Content categories | Lists Audiobooks, Ebooks (selected), Podcasts, and an "Unlimited" offering |

| Scribd | "Book On Making Money, The - Steve Oliverez" listing | Displays "4K views," "177 pages," and "Download free for 30 days" |

One control to install now: "save your raise"#

A commonly shared tactic online is to "save your raise," meaning you pre-commit to saving a large fraction of any future pay increase. In one Quora answer, the example given is "say 50%." Treat that as one person's advice, not a universal rule, and scale it to your own cashflow reality.

Best personal finance books for mindset, investing, and the long game (without breaking your month-to-month cashflow)#

Personal finance books are a good start. Use these picks to set behavioral rules and investing triggers that fire only after you fund Tax and Runway. Get your "don't-go-broke" controls working first (buckets, invoicing cadence, basic budgeting). Then build the long game without sabotaging cashflow.

| Book | Use when | Operator install |

|---|---|---|

| The Psychology of Money | You want a mindset reset before you add more strategy | Write a minimum runway policy and a good-month allocation rule; track transfers in a simple dashboard |

| The Simple Path to Wealth | You want to keep investing simple once cashflow runs stable | Automate a monthly investing transfer only after Tax + Runway fund; keep 1099 documentation ready |

| Die with Zero | You are already stable and want sharper decisions about spending intentionally | Raise lifestyle spend only when pipeline looks healthy, invoices sit current, and compliance friction is cleared |

| The Millionaire Next Door | You want guardrails against lifestyle creep after you finally "make it" | Define a raise cap policy and route the rest to Runway, Tax, and investing |

| The Richest Man in Babylon | You want timeless rules you can execute, not tactics you have to maintain | Set an owner draw date after invoices clear and keep a receipt trail |

Safety gate (so "investing energy" does not sabotage cashflow)#

| Gate | What "yes" means | What you do if "no" |

|---|---|---|

| Tax is funded | Your tax set-aside sits ready (treat it like a bill on 1099 income) | Pause investing transfers. Fix allocations first. |

| Runway meets your minimum | You hit your written minimum runway policy | Route extra cash to Runway until you hit the floor. |

| Payouts clear reliably | No active KYC friction or payout holds | Delay lifestyle upgrades and investing increases until cash clears. |

- The Psychology of Money (Morgan Housel)

Read it when: you want a mindset reset before you add more "strategy." Operator install (2 rules, written): (1) your minimum runway policy, (2) your good-month allocation rule. Track transfers in a simple dashboard (for example, Monarch) so behavior shows up as data, not vibes.

- The Simple Path to Wealth (JL Collins)

Read it when: you want to keep investing simple once your cashflow runs stable. A grounded snapshot: Collins frames it plainly: "This book grew out of a series of letters to my daughter... mostly about money and investing." A credit union ranking lists strong reader ratings (Amazon rating 4.7, Goodreads 4.46) and includes the reminder that "Complex investments exist only to profit those who create and sell them." Operator install (1 trigger): automate a monthly investing transfer only after Tax + Runway fund. Keep your 1099 documentation ready so "investing" never steals from obligations.

- Die with Zero (Bill Perkins)

Read it when: you're already stable and want sharper decisions about spending intentionally (time, money, experiences). Operator install (3 gates): raise lifestyle spend only when (1) pipeline looks healthy, (2) invoices sit current, (3) you cleared compliance friction (including KYC reviews that can sometimes slow withdrawals). Hypothetical: you land a dream client, then a platform flags your payout. Your Spend Plan blocks the celebration purchase until funds clear.

- The Millionaire Next Door (Thomas J. Stanley, William D. Danko)

Read it when: you want guardrails against lifestyle creep after you finally "make it." Operator install (1 cap): define a raise cap policy. When a big client lands, only a fixed percentage becomes lifestyle. Route the rest to Runway, Tax, and investing. Export clean reports from QuickBooks so you can prove income for lender or lease applications without a scramble.

- The Richest Man in Babylon (George S. Clason)

Read it when: you want timeless rules you can execute, not tactics you have to maintain. Operator install (1 recurring event): set an owner draw date after invoices clear. If platforms pay you, document each transfer and keep a receipt trail like lightweight ledger journals so your money story stays auditable.

How do I turn these books into a freelancer "get paid" operating system?#

Convert what you read into more predictable money by turning "good advice" into written defaults for terms, invoicing, collections, and documentation. Books become policies, templates, and routines you can run on tired days.

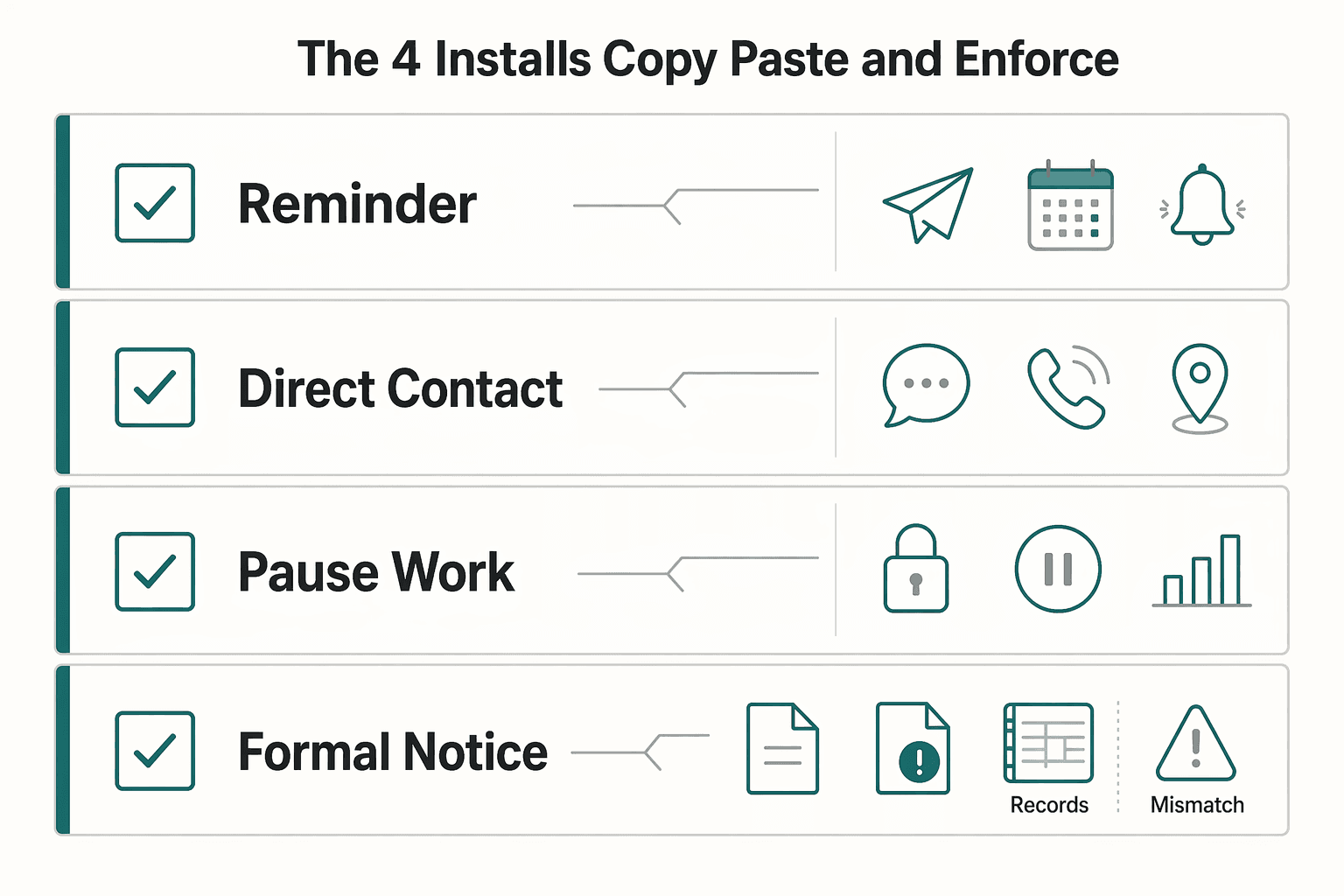

The 4 installs (copy, paste, and enforce)#

- Write your default payment terms as a reusable clause (one paragraph, always the same). Treat this like a durable tool, not a custom draft every time. Nick Usborne (a freelance copywriter) says, "For the past 30 years, I've been a freelance copywriter," and longevity comes from repeatable terms you can apply client after client.

Your clause should cover the practical essentials of how you get paid and how payment-related friction gets handled, in plain language you can actually enforce.

- Install an invoice workflow with a follow-up cadence (and make it non-negotiable). The AWAI headline contrasting $80,000 vs $350,000 (marketing numbers, not "typical") still points at a real lever. Operators get paid more cleanly because they run tighter workflows.

Send invoices as soon as your contract says you earned them. Track invoice status in your billing/accounting system, and store your "proof of yes" (email approval, PO, or deliverable sign-off) so you can handle disputes with evidence, not opinions.

- Use more structured collection paths when risk is higher (decide before you start). A single purchase like a $42.45 hardcover (or a $37.50 used copy) feels easy because the process is straightforward. Your client payments should feel just as straightforward.

When a project, client, or geography increases uncertainty, choose a collection method you can reconcile, document, and explain, and make it part of your default process (options and availability vary by provider and market).

- Create a "payment risk escalation path" before you need it (and document every touch). Use a simple ladder and keep timestamps. Example (hypothetical): a client "forgets" to pay, then claims they never approved the final deliverable. Your paper trail ends the argument.

| Step | Your action | Evidence you save |

|---|---|---|

| Reminder | Polite written nudge | Sent email + invoice link |

| Direct contact | Call or direct message | Call note (date/time) |

| Pause work | Stop new deliverables | Screenshot of pause notice |

| Formal notice | Written demand per contract | Final notice + attachments |

If scope conflict drives nonpayment risk, tighten your boundary language and align IP terms too: How to Protect Your Intellectual Property as a Strategic Consultant. If you want a quick next step, try the free invoice generator.

The risk-first client screen checklist (so you avoid holds, chargebacks, and bad terms)#

Screen for payment risk before you accept scope, because fixing "bad client math" costs more than declining the work. If your money playbook is your engine, this screen is your intake gate.

The 5-step screen (copy into your intake form)#

- Confirm identity and authority (legitimacy + payability). Ask for the legal entity name, the billing contact, and the signer's name and title. Then cross-check the basics you can see: website, address, and whether the signer matches the company. Tiny naming details matter in real life.

A public comment dated February 25, 2026 highlights a draft provision described as prohibiting use of the name "TEAM-WV" without written consent, which shows how seriously organizations treat names and permissions.

- Lock your "paper trail" up front, not during a dispute. Decide what you will save every time: signed agreement, written approvals, invoice copy, and proof of delivery. If the client asks for tax documentation or other internal paperwork, surface that request early in onboarding so it never becomes a last-minute reason Finance "can't release payment yet."

You do not need to litigate rules here. You need to remove surprise requests.

-

Assume reviews and internal gates create timing friction. Some platforms and payers run identity or compliance-style reviews that slow payouts. Treat that as a calendar risk. Build your schedule so a review never forces you to beg, discount, or accept worse terms just to keep cash moving.

-

Screen for chargeback exposure (especially with card-funded payments). A chargeback can come from "merchant error, criminal fraud, or 'friendly' fraud," according to Kount's chargeback guide published June 6th, 2024. You reduce "merchant error" risk by tightening the basics: clear scope, written acceptance, and a clean delivery trail.

Hypothetical: a client praises the work in email, then disputes the charge when their boss asks questions. Your saved approval turns chaos into a routine response.

- Treat payment terms and IP terms as one negotiation. Clients who push vague payment language often also push aggressive rights grabs. Keep the deal coherent: if they want more flexibility, you need more protection. When you work as a strategic consultant, keep payment risk tied to IP risk: How to Protect Your Intellectual Property as a Strategic Consultant.

Quick red-flag table (use in your yes/no decision)#

| Signal you see | What it often predicts | Your safe default action |

|---|---|---|

| Unclear legal entity or signer | Slow approvals, messy enforcement | Ask for legal entity name + signer title before kickoff |

| "We'll sort paperwork later" | Payment holds due to missing docs | Require onboarding docs before scheduling work |

| Confusing acceptance criteria | "Merchant error" style disputes | Define acceptance in writing and save sign-off |

| Vague rights language | Scope creep plus rights grabs | Align payment milestones with IP and scope boundaries |

If you want a simple way to reduce single-client dependency, track client revenue concentration and cash runway in a spreadsheet. Keep it simple, then make decisions consistently.

Cross-border reality check: what changes when your clients, taxes, and payouts span jurisdictions?#

Cross-border work adds timing friction and documentation load, so you need a "tax-ready by default" workflow that survives delays and keeps your records defensible. This is where money becomes execution: forms, logs, and payout confirmations.

The tax/admin tripwires freelancers actually hit (and how to de-risk them)#

If you qualify for the Foreign Earned Income Exclusion (FEIE), treat eligibility like a compliance project, not a vibe. The IRS says, "If you meet certain requirements, you may qualify for the foreign earned income exclusion," and it also calls out a common misconception: you still must file a return reporting the income to claim it ("the exclusion applies only if you... file a tax return reporting the income.").

Build your default around the physical presence test so you can prove it cleanly. The IRS states: "You meet the physical presence test if you are physically present in a foreign country or countries 330 full days during any period of 12 consecutive months," and that this test "is based only on how long you stay," not intent.

Use this table as a quick-reference guardrail. Keep it tied to your workflow, not your memory.

| FEIE detail (IRS) | 2025 | 2026 | What you do operationally |

|---|---|---|---|

| Maximum exclusion (per qualifying person) | $130,000 | $132,900 | Track qualifying days and foreign earned income in the same system you use for invoices. |

| Housing expense limitation (general rule) | 30% of max | 30% of max | Keep housing receipts organized in a dedicated folder tied to the tax year. |

| Housing amount limitation | $39,000 | $39,870 | Do not wait until January to reconcile. Close your "tax folder" monthly. |

Hypothetical: you bounce between countries while serving a US client. Stop guessing and start logging full days abroad, saving invoices, and exporting payout confirmations monthly so you can support your position without a scramble.

Invoicing and auditability when jurisdictions collide#

You will run into extra requirements on invoices in some VAT-style regimes and cross-border procurement setups. Do not improvise. Ask your client's finance contact for the required invoice format before you send the first invoice, then template it.

Operationalize auditability like you would in accounting ledger journals: invoice → written approval → payment confirmation → payout record. Store each artifact together by client and tax year. If you're choosing where to base yourself, treat location as an admin decision too: Japan Digital Nomad Visa guide.

The bottom line: pick one book, install one control, repeat (that's how you de-risk freelancer cashflow)#

Turn financial education into more predictable operations by running a simple loop: choose one book for your current bottleneck, install one control immediately, then repeat next week. That is how you move from ideas to a system you can run.

Run the loop (Pick. Install. Repeat.)#

You do not need a perfect syllabus. You need one installed behavior that reduces timing risk.

- Pick (one title, one problem): Choose based on the failure mode you actually face.

- Late payers and loose terms: I Will Teach You to Be Rich * Feast and famine spending: The Psychology of Money * Life-stage basics and admin hygiene: Get a Financial Life: Personal Finance in Your Twenties and Thirties * Time versus money tradeoffs (only after stability): Die with Zero

- Install (one control, same day): Treat "first action" as a short work block, not a research project. Ship something you can reuse:

- Terms control: Paste a default payment terms paragraph into your contract template (deposit, invoice schedule, pause-work trigger). * Invoicing control: Create a single invoice template and a recurring reminder task. * Follow-up control: Write a 3-touch email sequence you can send without rethinking tone. * Risk screen control: Add a pre-work checklist (legal entity name, billing contact, required docs).

- Repeat (weekly): Each week, add one new control or tighten one existing control. That is how you build a system instead of a reading list.

If you want curated discovery beyond Amazon Best Sellers-style popularity signals, borrow a librarian mindset. The University of Florida Business Library describes its list as "a core collection of some of the best business and economics books published since 2000." Use lists like that for options, then apply your operator filter: "What control will I install by Friday?"

If you operate globally or scale, validate your money-movement infrastructure#

Cross-border and platform-mediated payouts can add extra steps, reviews, and documentation moments. If that's your reality, evaluate whether you need receiving accounts (often called virtual accounts), payouts tooling, or Merchant of Record (MoR) workflows, and confirm what is actually supported before you build dependencies into your process.

Confirm coverage by market and program before you build dependencies into your workflow, especially if your payouts face compliance gates or country-specific constraints. For location-driven complexity, keep this handy: Japan Digital Nomad Visa: A Guide to the New 2025 Program.

Frequently Asked Questions

What are good personal finance books if I have variable income, not a steady salary?

There is no single “best” pick for everyone, but the right books will give you clear ideas you can actually use. Debt.ca frames personal finance books as books that offer advice across money management, paying off debt, and retirement planning. If your income is uneven, prioritize books that lean on rules, checklists, and simple defaults, not just inspiration.

Which book should I read first if my main issue is inconsistent income?

Start with the book that pushes you toward process, not motivation. If money feels inconsistent, you need a system mindset that makes you write down a workflow, define “done,” and run the same steps every time. Use the first chapter to extract one policy you can apply immediately, then implement it before you keep reading.

What books help with spending behavior vs books that help with earning more consistently?

Spending behavior books change how you act when money shows up, especially during high months. “Earning more consistently” books tend to focus on decisions and habits that support more stable income over time. In practice, you want both: behavior control reduces self-inflicted volatility; a repeatable plan reduces timing surprises.

How do I turn personal finance advice into a practical money system?

Treat reading as input, then convert it into a one-page system. After each chapter, write (1) one rule, (2) one trigger (when you apply it), and (3) one artifact (template, checklist, or tracking field). Hypothetical: you finish a chapter on automation and immediately create a “money movement” checklist you run every time a payment clears.

What should my money checklist include before I make a big financial commitment?

Keep it boring and complete: the total cost, the timing, the payment method, and the record you will keep. Include what you are committing to, when payments happen, and what changes if circumstances shift. Add a paper trail requirement so approvals, invoices/receipts, and confirmations stay together for cleaner bookkeeping later.

How do I plan for payment timing delays and extra verification steps?

Assume extra waiting time and extra questions, then build your cash plan around that reality. Design a buffer so a document request or processing delay does not force a bad decision. Keep documentation organized by year (and by provider, if helpful) so you can respond fast when someone asks for proof of payment or identity.

Are bestseller lists (Amazon Best Sellers, CNBC Select) a reliable way to choose finance books?

Use bestseller lists as discovery tools, not decision tools. They can show what is popular, but they do not automatically tell you whether a book fits your situation or the habits you are trying to build. Also note that Amazon explicitly mentions showing “interest-based ads” (personalized or targeted), which can affect which ads you see while browsing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

How to Protect Your Intellectual Property as a Strategic Consultant

**Build a repeatable IP system that defines ownership scope, sets confidentiality rules, and makes governing law and dispute forum explicit before work starts.** As the CEO of a business-of-one, your IP is not "nice to have." It is core operating value. You are not trying to lawyer up every project. You are setting safe defaults so deals move fast and preventable disputes stay contained.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.