Quick Answer

The best international money transfer service is the one that reliably fits your corridor, payout method, urgency, and record-keeping needs. Instead of picking a universal winner, use a repeatable framework: lock one apples-to-apples scenario, compare total cost (fees plus FX outcome), verify delivery certainty, and keep a tested fallback route. For many operators, Wise is a useful baseline, but final choice should be scenario-specific.

You don't need "the best app" - you need a repeatable "get paid" route per client, corridor, and urgency#

Build one primary route and one fallback route per client and currency pair, and you'll usually do better than any "best international money transfer" list when cash flow certainty matters. If you run a business-of-one, you are the CEO. Your job is to build a reliable "get paid" system, not chase whatever app is trending this week.

For the rest of this guide, the operating standard is simple: fewer delays, fewer fees, and fewer surprises because you follow the same decision path every time.

Who this is for (and not for)#

If you invoice internationally as a freelancer, creator, or small team, you care about certainty. The payment arrives, the fees make sense, and you can reconcile it without living in screenshots.

This is not aimed at personal remittances where you optimize for cash pickup in a single corridor and stop there. You can still use the framework, but your "best" often means "most convenient pickup experience," which leads to a different decision tree.

The operator-grade promise (beyond Wise)#

Most "Wise alternatives" content fails in one of two ways. It compares headline fees without checking the exchange rate, or it pushes you toward provider marketing pages instead of a repeatable test. We'll do neither.

Here's the standard we'll use, and you can re-run it anytime:

- One test scenario you can rerun: same sender country, same recipient country (your corridor), same currency pair, same funding method, same payout method, same timestamp window.

- A risk-first workflow: you choose based on failure modes (holds, returns, unclear status), not just "cheap" or "fast."

- A defensible baseline: Wise explicitly says it uses the mid-market rate (the one you can check on Google) and that you "Always know what you're paying upfront." Wise also lists sending fees from 0.48% on its Canada pricing page (and other regions show different "from" rates, so you must verify where you operate).

Use that baseline to compare providers on the things you'll actually deal with: delivery certainty, payout fit, and clean records.

| Decision variable | Safe default | Fallback trigger |

|---|---|---|

| You invoice in USD/EUR and need audit-friendly records | Bank transfer route with clear records you can reconcile | Recipient cannot receive, transfer returns, or status stays unclear |

| Corridor changes (example: India (INR) or Mexico) | Re-run the same test scenario before the next invoice | Availability, payout methods, or effective rate shifts at send time |

Hypothetical: a client pays a USD invoice on Friday and your contractor needs funds in INR. You run your saved test, pick your primary route, then keep a second route ready if the first one slows down or fails.

By the end, you should have (1) a shortlist by use case, (2) a comparison table you can scan, and (3) a "get paid" checklist that stays reconciliation-friendly.

The 10-minute selection framework (risk-first, not hype-first)#

Choose your route by locking down corridor, payout method, control priority, failure tolerance, and proof trail, in that order. This is a 10-minute decision path you can rerun per client and per corridor without getting pulled into hype or "Wise alternatives" rabbit holes.

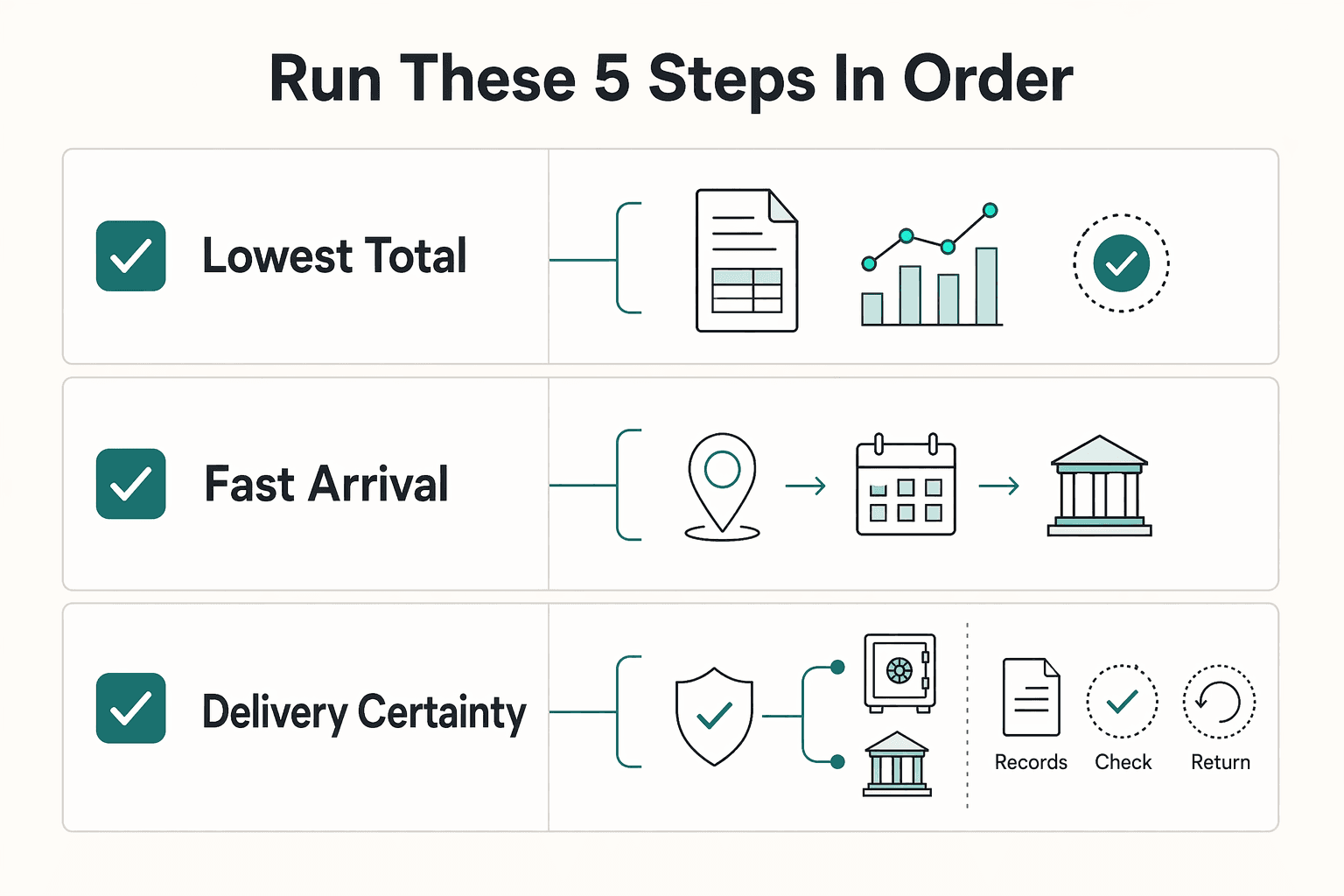

Run these 5 steps (in order)#

| Step | Decision | Key detail |

|---|---|---|

| 1 | Corridor + currency pair | Write sender country → recipient country, then currency pair; treat edge cases as "verify before you promise" |

| 2 | Recipient payout reality | Pick bank deposit vs card vs cash pickup vs mobile wallet before you compare apps |

| 3 | Control priority | Choose lowest total cost, fast arrival, or high certainty + fallback routes |

| 4 | Failure tolerance | Decide what you do if the transfer gets delayed, returned, or held |

| 5 | Proof trail | Require downloadable receipts, reference IDs, and consistent transaction details for reconciliation |

- Step 1: Define the corridor + currency pair. Write it as sender country → recipient country, then currency pair (example: United States → Philippines, USD → EUR, USD → INR). Assume availability, pricing, and friction can vary by corridor. Treat edge cases (example: Iraq) as "verify before you promise," not "assume it works."

- Step 2: Decide the recipient's payout reality. Don't debate apps before you pick the landing method: bank deposit vs card vs cash pickup vs mobile wallet. If you choose a bank-optimized flow when your recipient cannot receive a bank transfer, you built failure in on day one.

- Step 3: Pick your control priority. This is where the comparison starts to matter:

- Lowest total cost (fee + FX markup): compare quotes at the same timestamp. * Fast arrival: compare delivery estimates across the funding and payout options you actually have available. * High certainty + fallback routes: keep an alternate route ready even if you prefer your primary method.

- Step 4: Define failure tolerance. Decide what you do if the transfer gets delayed, returned, or held, especially when rent and payroll still run in USD. If a one-day delay breaks operations, you need a documented fallback, not optimism.

- Step 5: Require a proof trail (and know when it becomes compliance). Demand downloadable receipts, reference IDs, and consistent transaction details for reconciliation. If your audit trail currently lives in screenshots, fix that (pair this with Separating Business and Personal Finances: An Important Step for LLCs).

If you are a U.S. person, keep an eye on whether your activity creates an FBAR obligation. FinCEN Report 114 (FBAR) is used to report a financial interest in, or signature authority over, a foreign financial account, and filing is required when the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year. The FBAR must be filed electronically using the BSA E-Filing System. The filing deadline is generally April 15, and FinCEN provides an automatic extension to October 15 each year for filers who miss the April deadline.

| If you optimize for | Your safe default decision | Your operator-grade fallback |

|---|---|---|

| Lowest total cost | Bank-funded quote comparison | Re-quote at send time, switch provider if total cost jumps |

| Fast arrival | Choose the fastest route you can verify end-to-end | Send partial now, remainder via cheaper route |

| Delivery certainty | Primary route with clear tracking + support path | Alternate route or payout method you can execute quickly |

Hypothetical: your client pays late, your contractor in the Philippines needs funds today, and your primary route shows an uncertain delivery estimate. You run Steps 1 to 3, choose a speed-first route for the urgent portion, then apply Step 5 so your books still reconcile cleanly.

Want a quick next step? Try the free invoice generator.

How do you compare international transfer services correctly (without getting fooled by "zero fees")?#

Compare services by locking one scenario, then measuring both the money outcome (effective FX vs mid-market) and the operational outcome (proof, tracking, and timing). The goal is a comparison method you can rerun monthly without getting distracted by headline claims.

Run an apples-to-apples test (one scenario, same timestamp)#

Pick one standardized scenario and stick to it. You want pricing differences, not scenario noise.

- Amount (example): $2,000 USD

- Destination (example): Mexico

- Payout type: bank deposit

- Funding method: bank transfer (not card)

- Timestamp: capture quotes within the same few minutes

- Second pass: repeat the same test for USD → EUR if you invoice EU clients

If you use Wise as a baseline, anchor on what it explicitly says about its pricing and rate. Wise says: "We only use the mid-market rate, the one you can check on Google." It also says: "You only pay for what you use, no subscriptions or plans."

Wise also states its send-money fee "varies by currency" and starts "From 0.48%." That's a concrete example of what a quote can look like when the fee is clearly shown.

| What you record | Why it matters | What "good" looks like |

|---|---|---|

| Total you pay (including fees) | Prevents "zero fee" games | One clear debit amount |

| Recipient amount (in destination currency) | Tells you the real outcome | One clear delivered amount |

| Mid-market rate at quote time | Lets you sanity-check FX | You can independently verify it |

| Implied rate from the quote | Reveals FX markup | Close to mid-market, with any gap clearly explainable |

Log operational facts (this saves you later)#

Your books do not reconcile on vibes. For international payments, log these every time, especially when you test Wise alternatives like Revolut, WorldRemit, or Remitly:

| Operational fact | What to record | Key detail |

|---|---|---|

| Confirmation time | When the provider confirms the transfer | Not when you click "send" |

| Delivery estimate | What the provider shows at send time | Log the estimate shown at send time |

| Tracking availability | Status page, transfer history, downloadable receipt | Track what proof is available |

| Reference format | A clean provider reference ID | One you can paste into your accounting system |

At minimum, log confirmation time, the delivery estimate shown at send time, what tracking or downloadable proof is available, and the reference ID format you can carry into your accounting system.

Then validate "speed" by rerunning the same scenario with a different funding method (bank transfer vs debit or credit card). A provider can look fast in one method and merely normal in another. Test the method you will actually use.

Hypothetical: you pay a contractor abroad and cannot tolerate a missing receipt. You choose the option that gives you a downloadable confirmation and a stable reference ID, even if another option advertises "zero fees." That is operator math.

Are transfer fees or exchange rates more important? (The math that protects your margin)#

Exchange rate quality and fees both matter, but you should optimize for the lowest total cost (fee plus FX rate impact) while protecting your ability to prove what happened later. Once you can compare providers apples-to-apples, you can stop arguing about "fees" in isolation.

The operator math (fee + effective rate)#

Treat every quote like two line items, even when the app only shows one:

- Fee line item: the explicit service charge (often shown clearly).

- FX impact: the gap between the provider's effective rate and a mid-market reference (often where cost hides).

Use this safe rule of thumb: once a transfer amount feels material for your business, a small rate difference can matter as much as, or more than, a visible fee. Do not assume. Measure.

Here's the simplest sanity table to keep you honest:

| What you check | How to compute it | Why it protects margin |

|---|---|---|

| Provider effective rate | (amount received) / (amount sent minus fees) | Reveals the real currency exchange outcome |

| Mid-market reference | Look it up right before confirming | Gives you a neutral baseline |

| Rate gap | mid-market minus effective rate | Flags hidden spread when fees look "low" |

Rate sanity check (build into your invoicing routine):

- Open a public mid-market reference in a separate tab.

- Capture the provider quote and record the timestamp.

- Save a screenshot or PDF of the confirmation that shows fee, delivered amount, and currency pair (USD/EUR, USD/INR, etc.).

Watch "zero fee" structures across app-first providers. Plans, tiers, and corridors can change what you pay. Treat every quote as new information, not a promise.

Margin-protection defaults + audit trail#

Pick a default based on the payment shape, not vibes about the app.

- Retainers: prioritize predictability and repeatability. Choose one primary route and rerun the same test monthly.

- One-off high-ticket: prioritize lowest total cost plus a clean receipt trail. This is where bank-to-bank proof and support can matter.

If you are a U.S. taxpayer and you hold specified foreign financial assets, FATCA can require reporting those assets on Form 8938 when their total value exceeds the appropriate reporting threshold, and Form 8938 is attached to your annual tax return. If you do not have to file an income tax return for the year, you generally do not have to file Form 8938, regardless of value. Failure to report can trigger penalties (including $10,000, and up to $50,000 for continued failure after IRS notification). The IRS also notes you may also have to file FinCEN Form 114 (FBAR), which is separate.

Hypothetical: you invoice a US client, then pay a contractor abroad. Pick the route that gives you a stable reference ID and downloadable receipt, even if another app looks simpler in the moment. Your future self will thank you.

How fast is "fast," really? (Speed vs funding method vs payout method)#

"Fast" is situational and often comes with tradeoffs, especially cost. Treat "speed" like a three-part pipeline (funding, conversion, payout), because many "instant" claims describe one leg, not end-to-end delivery.

Speed is three clocks, not one#

Think in systems. You do not buy "fast." You assemble it.

| Speed leg | What it means operationally | Where "fast" marketing usually points | What you should capture for your records |

|---|---|---|---|

| 1) Funding time | How quickly your money becomes usable by the provider (your chosen funding method) | Funding confirmation | Funding method, timestamp, and any hold notice |

| 2) FX/conversion time | When the provider actually converts currencies (USD/EUR, etc.) | Rate lock screens | Quote timestamp, effective rate, fee line item |

| 3) Payout time | When funds become accessible to the recipient (your chosen payout method) | "Delivery estimate" | Payout method, reference ID, recipient confirmation |

A credible default: speed usually competes with cost. Faster options can come with higher fees and/or less favorable exchange rates, so treat "fast" promises as a reason to re-check the all-in quote (fee plus rate), not as a reason to stop checking.

Funding method tradeoff (operator framing):

- Planned payments: optimize for total cost and clean reconciliation.

- Time-sensitive payments (emergencies, urgent bills, travel, business, education): prioritize getting funds there quickly, then verify what that speed costs you in fees and rate.

Operator playbook: payout method, buffers, and backups#

Cash pickup can beat bank deposit on "recipient actually gets funds today" in some corridors. You may pay for that convenience with messier documentation. Bank deposit often gives you cleaner statements and references for bookkeeping.

Build timeline buffers into your contract. If you promise a pay-by date, send earlier unless you have already proven the route and method you are using for that corridor.

Reliability changes by country and network. Providers can restrict routes (Wise notes, "Not all apps support every country or currency for transfers."). Keep a backup with a different payout path so one outage does not stop payroll.

Hypothetical: a contractor needs funds before a trip. You run your primary bank-deposit route first. If tracking stalls, you switch to a cash-pickup backup and document the pickup receipt the same day.

Best international money transfer services (beyond Wise): operator picks by use case#

Pick the provider that matches your corridor, payout reality, and urgency, then standardize it into a repeatable route. This is a use-case menu, not a popularity contest.

Operator picks (use-case menu, not favorites)#

Use this as your alternatives menu. Match the row to your main constraint first, then run your apples-to-apples quote check at send time (fee, exchange rate, payout method).

| Provider type | Choose it when... | Operator differentiator to verify before you send |

|---|---|---|

| Transparent baseline option | You need a defensible baseline quote for a bank-deposit transfer | Can you see the fee line item and effective rate clearly, with a clean receipt trail? |

| Bank-to-bank specialist | You run bank-to-bank payouts where support matters when something breaks | What proof do you get if a bank returns the transfer, and how do you re-send cleanly? |

| Multi-currency account/app | You operate in multiple currencies (hold one, bill in another) | What plan limits apply to your conversions and transfers for this currency pair? |

| Recipient-choice remittance provider | The recipient needs specific delivery options, depending on the corridor | Which payout methods exist for this corridor today, and what does tracking look like? |

| Backup payout network | You want payout flexibility as a backup when bank rails fail | What receipt artifacts do you get for reconciliation if the recipient uses a non-bank payout? |

| Cash pickup option | Delivery certainty matters more than perfect pricing | Can your recipient actually pick up, and can you document pickup without chasing screenshots? |

| Card-funded option | You accept higher total cost for speed and convenience | What is the all-in cost at confirmation (fee + rate), and what delivery estimate shows for this corridor? |

Concrete use-case pattern (hypothetical): you invoice a US client in USD, pay a contractor in EUR, and the contractor travels tomorrow. Your default route stays bank deposit for clean books. If tracking stalls, you switch to a backup with pickup or alternate rails, then file both receipts with the same invoice ID.

Record-keeping safe defaults (especially if you're a U.S. person)#

Treat receipts and reference IDs like part of the payment, not a nice-to-have.

If you qualify as a United States person, and you have a financial interest in or signature authority over foreign financial accounts, FinCEN says you must file an FBAR (FinCEN Report 114) if the aggregate value of your foreign financial accounts exceeds $10,000 at any time during the calendar year. FinCEN also notes you file it electronically using the BSA E-Filing System, with a deadline that generally tracks April 15 and an automatic extension to October 15.

If you want this to stay clean all year, separate business and personal flows: Separating Business and Personal Finances: An Important Step for LLCs.

Quick comparison table (scan this first, then choose)#

Use one standardized send scenario to compare providers, then pick the tool that matches your corridor and payout reality, not the loudest claim. This table is a fast filter. Your real decision still comes from a consistent test scenario.

Standard test scenario (publish this and stick to it)#

Pick one repeatable scenario and re-run it whenever you evaluate Wise alternatives like Revolut, Remitly, WorldRemit, Western Union, OFX, or Xoom.

Example scenario: $2,000 USD from United States to Mexico, bank deposit, bank-funded, checked in the same timestamp window. "Best" only means "best under this scenario," so you can compare total cost and operational certainty apples-to-apples.

| Provider | Best for | Payout methods (typical) | Speed profile (depends on funding) | Cost transparency | Reliability / change risk |

|---|---|---|---|---|---|

| Wise | Baseline benchmark for fee + FX math | Varies by corridor and setup (verify at checkout) | Varies (verify at checkout) | Wise says it shows pricing upfront | Varies by corridor |

| OFX | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

| Revolut | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

| Remitly | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

| WorldRemit | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

| Western Union | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

| Xoom | Compare under the same scenario | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) | Not covered here (verify) |

How to read the table (decision rule)#

Treat these as starting hypotheses, then verify at send time.

For Wise, you can anchor your math because Wise says, "We only use the mid-market rate (the one you can check on Google)," and it positions pricing as "Always know what you're paying upfront." On Wise's Canada pricing page, Wise also states send fees start from 0.48% (fees vary by currency). If you send large amounts, Wise says volume discounts can apply once you send over 35,000 CAD (or equivalent) in a month (and it resets on the first of the month).

Then run this operator script:

- If the recipient needs bank deposit and clean reconciliation: start with a bank-deposit scenario, price it with Wise first, then run the exact same scenario across your other shortlisted providers.

- If time beats cost: test faster funding/payout options where available, but confirm the all-in cost at confirmation.

- If payout rails break: keep a fallback provider you can switch to under the same scenario, and verify availability before you promise delivery.

Corridor reality matters. Payout options and speed behave differently by corridor and method, so validate availability before you promise delivery.

Hypothetical: your contractor in Mexico cannot receive bank wires this week. You switch from bank deposit to a pickup-capable backup, save both receipts, and keep the invoice reference consistent so your books still reconcile cleanly.

The "Get Paid Safely" workflow (delays, holds, exceptions - handled like a system)#

Run every international payment through a written-terms, two-rail, proof-first workflow so delays and holds become routine exceptions, not cashflow emergencies. This turns "which provider should I use?" into a system you can reuse across clients, corridors, and payout realities.

1) Put invoice terms in writing (you control the ambiguity)#

Write the terms that stop "surprise spread" fights later:

| Term | What to state | Key detail |

|---|---|---|

| Invoice currency | State USD or EUR explicitly | If you accept currency exchange, specify who chooses the provider and when you lock the rate |

| Funding method expectation | "Client pays via bank transfer" (or card) | Funding method can change fees and speed |

| Fee responsibility | "Payer covers transfer fees" (or "fees deducted from settlement") | Without this, you often eat the difference |

If you want a safe default clause: "Client pays invoice in USD via bank transfer. Client covers all transfer and intermediary fees. Payment counts as received when funds clear in our account."

2) Build an exception playbook with two rails (primary + fallback)#

You do not need 10 apps. You need two different rails:

- Primary (bank-first, clean reconciliation): a bank-transfer-first provider that gives strong references/receipts and predictable tracking.

- Fallback (different last-mile reality): a provider with alternative delivery options (for example, cash pickup or other recipient-first methods, where available).

Use this operator table to choose quickly under stress:

| Situation | Primary move | Fallback trigger |

|---|---|---|

| Bank deposit works, you need clean books | Use your bank-transfer-first rail | Recipient cannot receive a bank payout this week |

| Delivery certainty beats price | Use your bank-transfer-first rail | Switch to the alternative-delivery rail |

| Client insists on card-funded speed | Confirm total cost at checkout | If fees spike, offer bank-funded option and a new ETA |

Hypothetical: a client pays on the last day and your contractor says their bank rejects incoming transfers right now. You switch to the fallback rail, keep the same invoice reference, and ship the receipt to close the loop.

3) Create a proof trail + "quote → confirm → reconcile" loop#

Every transfer should leave a paper trail you can defend:

- Save invoice + transfer receipt + provider reference ID in one folder (client, invoice number, currency pair like USD/EUR).

- Run quote → confirm → reconcile:

- Quote: record timestamp and shown rate. * Confirm: capture final receipt and reference ID. * Reconcile: match receipt to invoice, mark paid, and note any fees.

This is not busywork. The IRS states Form 8938 reports "specified foreign financial assets" when total value exceeds the appropriate reporting threshold, and the form must attach to your annual return. The IRS also notes penalties can apply for failure to report (including $10,000, and up to $50,000 for continued failure after notice). The IRS also notes you may have to file FinCEN Form 114 (FBAR).

If app juggling is starting to break down, move to a platform approach that centralizes collection, currency exchange, and payout records. In Gruv, that can look like Virtual Accounts for receiving (where enabled), FX quotes/conversions with audit trails, and Payouts with status tracking (where enabled). For the accounting foundation that makes this easier, read: Separating Business and Personal Finances: An Important Step for LLCs.

If you want a deeper dive, read How to Set Up a US LLC from the UK.

Build your default route, then add one fallback (that's the whole game)#

Build one "default route" you run every time, then keep one "fallback rail" you can switch to quickly when delivery breaks. The goal is predictable payments, clean receipts, and no scrambling when a corridor or payout method changes.

1) Your default route (optimize for repeatability, not vibes)#

Pick a primary provider or rail that fits your most common invoice pattern (example: USD → EUR, bank deposit, consistent downloadable receipts). Then run the same comparison scenario monthly (same corridor, same funding method, same payout type) so you catch pricing drift and policy changes early.

Operator checklist for your default route:

- Payout fit: bank deposit first if you want clean reconciliation.

- Proof trail: require a downloadable receipt and a reference ID you can match to an invoice.

- Total cost math: log fee plus effective currency exchange rate (use a mid-market reference as your sanity check).

- Reconciliation habit: store receipts alongside invoices (client, invoice number, currency pair). If you haven't separated business and personal flows yet, fix that first: Separating Business and Personal Finances: An Important Step for LLCs.

Reality check: in some countries, the "default route" isn't cards or wires anymore. Spreedly describes Pix (Brazil) as an instant payments rail that became the default starting point for payments in Brazil.

2) Your fallback rail (optimize for certainty under constraints)#

Add a backup rail you can use when the recipient can't accept your default payout method (or when a bank-transfer path fails). Your fallback should be something you've already tested for: corridor availability, recipient requirements, and what proof you can download.

A concrete example of the kind of rail you might plan around: Nuvei describes Interac Payments as direct account-to-account transfers through Canadian financial institutions' interbank network, a fast and secure way to transfer money between private and business accounts, and says Interac solutions are universally accepted at over half a million locations. Nuvei also describes Instant Bank Transfer (IBT) as secure payment verification in Canada, intended to simplify deposit and withdrawal processes and support identity verification.

Use this table as your decision rule:

| Route | Primary goal | Choose it when | What you must log every time |

|---|---|---|---|

| Default | Lowest friction + audit-ready records | Same corridor, bank deposit works, you want repeatable receipts | Fee, effective FX rate, reference ID, delivery estimate |

| Fallback | Delivery certainty | Bank rejects, alternative rail required, corridor rules change | Recipient requirements, payout method, proof format, status updates |

Treat your international transfer setup like a system, not a winner badge. Providers and rails shift over time. Your system wins when your default handles the normal case, and your fallback closes the loop when reality changes.

Frequently Asked Questions

What is the best international money transfer for freelancers?

The best international money transfer for freelancers is the one you can run the same way every month for the same corridor, with clean proof when something breaks. Use Wise as the baseline when you want transparent pricing (it says, “Always know what you're paying upfront”) and a clear reference rate (it says it uses the mid-market rate). Then keep one fallback rail (another provider or method) for the moment a recipient cannot take a bank deposit.

Is Wise always the cheapest option?

No. Wise positions itself as transparency-first (it says, “Always know what you're paying upfront” and “We only use the mid-market rate”), but that does not guarantee the lowest total cost in every corridor and funding method. Treat Wise as your comparison anchor, then run the same test scenario against other transfer services.

What is better than Wise for fast transfers?

If you need “fast,” choose based on funding method and payout type, not brand. Card-funded options can reduce wait time in some cases, but they can also increase total cost through fees and currency exchange terms. The operator move: test “bank-funded vs card-funded” in the exact corridor you use, captured in the same timestamp window.

What is better than Wise when my recipient needs cash pickup?

When your recipient needs cash pickup, shortlist providers that support cash pickup in that corridor because bank-first tools may not fit the last mile. Confirm (1) pickup availability in that corridor, (2) what proof of payment you can download, and (3) the recipient name requirements to avoid failed pickups.

How do I compare international transfer services correctly?

Run one apples-to-apples scenario and capture total cost and operational friction in one place. Wise explicitly frames the rate as the mid-market rate (“the one you can check on Google”), so use that as your reference point, then compute implied spread for each provider. | What to log | Why it matters | Safe default | |---|---|---| | Funding method (bank vs card) | Changes both speed and cost | Compare both once | | Fee + effective FX rate | Prevents “zero fee” traps | Use mid-market as reference | | Receipt + reference ID format | Clean reconciliation | Require downloadable proof |

How can I reduce international payment delays and payment risk?

Remove ambiguity up front, then run a two-rail workflow (primary plus fallback) with a proof trail. In practice: specify invoice currency (USD/EUR), who covers transfer fees, and when payment counts as received (when funds clear). Hypothetical: if a contractor’s bank rejects incoming transfers, you switch to the fallback rail the same day and send the receipt to close the loop.

Are transfer fees or exchange rates more important?

On meaningful invoices, exchange rate (spread) can dominate, even when the visible fee looks small. That is why “transparent pricing” claims matter less than your math: compare the provider’s effective rate to the mid-market reference, then add the visible fee. Do this consistently and you stop debating opinions and start managing margin.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

How to Set Up a US LLC from the UK

**If this is your first filing, register for Self Assessment before you try to file online.** That order matters. HMRC can penalize late returns, so lock in your UK registration and filing workflow before you start submitting anything else.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.