Quick Answer

Start with a blocker count, then pick the city. For a best digital nomad cities eastern europe shortlist, verify your legal path on official europa.eu-linked pages, save dated screenshots, and keep one evidence folder before paying any deposit. Use OSS/IOSS/CBR only as planning context, and treat local stay rules, appointment timing, and housing proof as the real go/no-go items. If two cities tie, keep a fallback active until critical checks are closed.

How to Choose the Right Eastern Europe Base#

If you are choosing among the best digital nomad cities eastern europe can offer, make the call in this order: legal path first, city second, spending last. That sequence helps you avoid the most expensive relocation mistake: paying deposits based on assumptions you have not verified.

Use a simple split from the start:

- Known now: OSS, including its non-Union, Union, and import schemes, and VAT Cross-border Rulings, or CBR, are real EU-level mechanisms and belong on your verification list.

- Still needs checking: your stay rights, permit timing, lease rules, appointment availability, and any city-specific registration step.

- Decision gate: if a claim affects money or timing, do not act on it until you have the current official page and the date you checked it.

Keep that rule strict. The EU's own guidance is simple: official European Union websites use the europa.eu domain. Before any housing deposit, flight booking, or prepaid coworking plan, require two things: an official source and a dated record in your files. If a rule came from a forum post, WhatsApp group, or a creator without a live official reference, treat it as a lead, not proof.

The goal is not to turn you into a tax specialist. It is to separate stable EU-level structures from city-level variables that can still derail a move. For example, EU VAT rules for cross-border B2C e-commerce changed on 1 July 2021. Official pages also reference a EUR 10 000 threshold in one VAT context, while the cross-border SME scheme has its own Union cap of EUR 100 000.

Those numbers matter only if they fit your taxpayer status and transaction type, so add any threshold to your notes only after you confirm it applies to you. A useful checkpoint is to watch for the exact trigger that makes a rule usable. Under the cross-border SME scheme, exemption starts only after the EX number is granted and confirmed by the Member State of establishment. The stated registration target is 35 working days, but the process can take longer if anti-evasion or avoidance checks are needed. That kind of timing risk can turn a cheap city plan into an expensive scramble.

Build one working evidence folder before you spend anything meaningful:

- Identity and income: passport copy, proof of remote income, and client or employer documents

- Coverage and housing: insurance proof, draft accommodation terms, cancellation rules, and deposit conditions

- Dated rule snapshots: screenshots or PDFs of official pages, plus any threshold or timeline you rely on once it has been verified

You do not need every answer on day one. You do need a shortlist built around unresolved dependencies, with one fallback city still active until the critical checks are closed.

How this list works and who it is for#

Use this framework if you want a workable shortlist built around timing, documents, and downside control. If you prefer a lifestyle-first pick, that can still work, but you are accepting a higher risk of committing to a city before the move is operationally clear.

Apply the same criteria to every city: legal stay path, paperwork load, cost pressure, internet reliability, coworking and cafe depth, safety, and community fit. Tag each item as known now or verify before commit:

known now: stable context you can anchor to official sourcesverify before commit: anything that could change your timeline, cash exposure, or ability to settle

Keep this boundary clear: EU-level frameworks like OSS, IOSS, and CBR are context for planning, not city rankings. OSS is optional, but if you use it, you must declare all supplies that fall under that OSS scheme through the OSS return. Your Member State of identification choice can also lock in for the current calendar year plus the next two. In the cross-border SME route, you first file prior notification in your Member State of establishment, and VAT exemption starts only after EX-number confirmation. The stated 35 working days timeline is a target and can take longer in specific cases.

For each city, complete this quick worksheet:

- Blocker: what stops your move today if it stays unconfirmed

- Uncertainty: what still needs an official page, dated screenshot, or landlord document

- Fallback: which next city you can switch to without rebuilding your housing, paperwork, and timeline

Once each city has blocker, uncertainty, and fallback labels, move to the comparison table and rank by unresolved dependencies first, lifestyle second. This pairs well with The Best Digital Nomad Cities for Creatives and Artists.

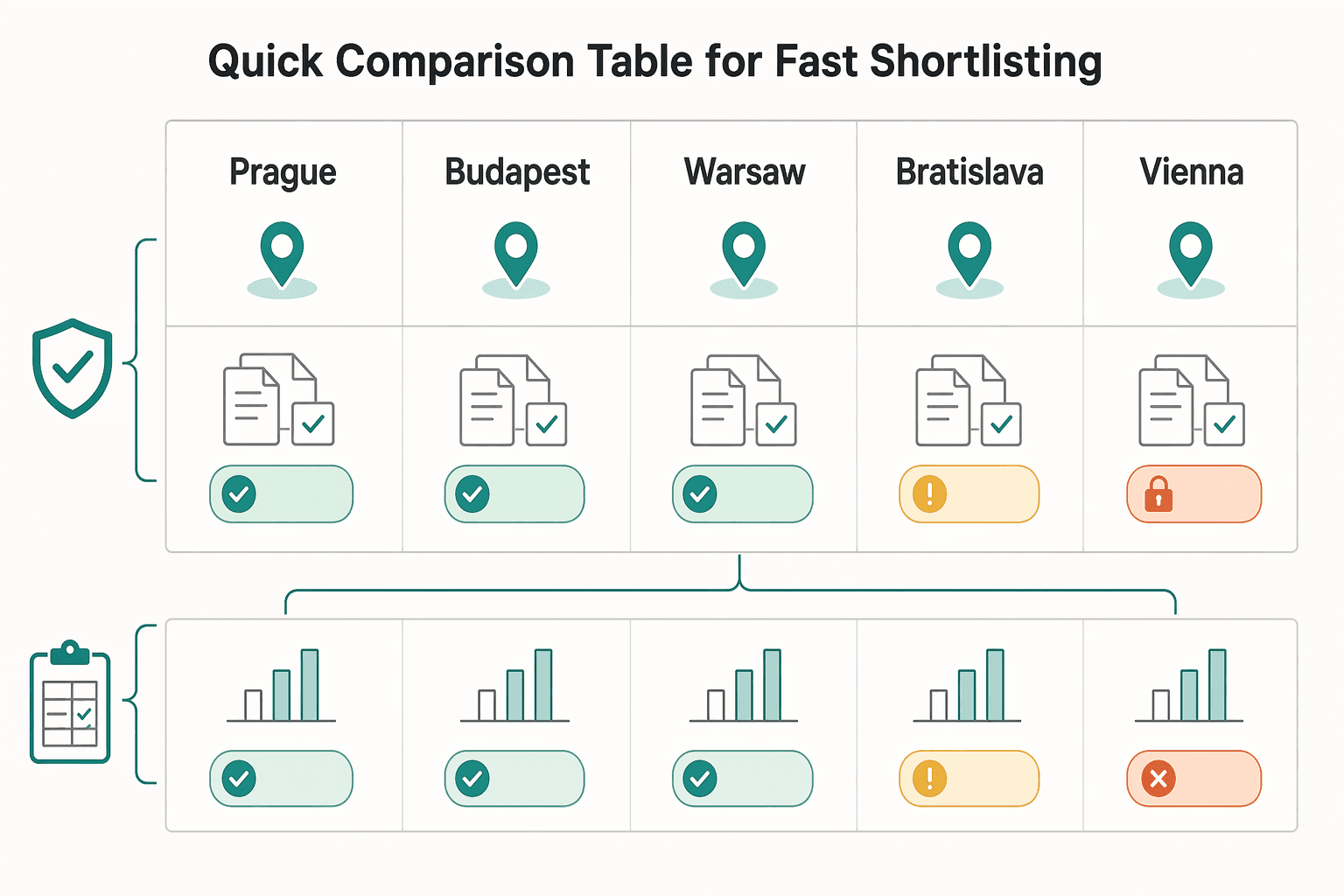

Quick comparison table for fast shortlisting#

Use this table to shortlist by execution risk first, then lifestyle fit. A city can look great and still be a hold if key legal-path items are unresolved.

Keep known and verify before commit separate:

Known: only stable framework context, such as the 1 July 2021 B2C VAT change, the EU-wide EUR 10,000 threshold, OSS being optional, possible Member State of identification binding (calendar year of choice + 2 following years), and OSS filing cadence (quarterly for non-Union/Union, monthly for import).Verify before commit: only blockers that can delay or stop execution, including legal stay path, appointment availability, accommodation documents, and national VAT-ruling conditions where relevant. If the cross-border SME route matters, exemption starts only after the EX number is granted, and the standard 35 working days can run longer in anti-evasion cases.

| City | Stable framework context | Verify before commit | Process clarity | Cost certainty | Fallback readiness | Book now or hold |

|---|---|---|---|---|---|---|

| Prague | Use EU-level context only. Verify Prague-specific CBR participation directly. | Legal stay route, appointment access, accommodation proof rules, and whether a VAT route is relevant to your case. | Low until you have dated official pages and reusable landlord documents. | Low until deposit, notice, and registration terms are in writing. | Keep one alternate city active with the same evidence pack. | Hold unless legal path and housing proof are both confirmed. |

| Budapest | Hungary appears in listed CBR participants. Any CBR request still follows Hungarian national VAT-ruling conditions. | Stay route, document sequence, appointment timing, and the current national threshold to confirm with the national tax authority if the SME route matters. | Medium only after national conditions are checked against your case. | Low until rent and deposit terms are documented. | Strong if Debrecen stays active as fallback. | Conditional book only after stay path is confirmed or tax routing is irrelevant. |

| Warsaw | Poland appears in listed CBR participants. National ruling conditions still control CBR usability. | Stay route, queue timing, accommodation proof, and the current national threshold to confirm with the national tax authority if the SME route matters. | Medium once document order is locked. | Low until total housing commitment is written. | Better if one non-Poland fallback stays active. | Conditional book only after document sequence is closed. |

| Bratislava | Use EU-level context only. Verify Bratislava-specific CBR participation directly. | Legal path, housing proof, and whether any advance-ruling route is needed. | Low until official pages are saved with dates. | Low until landlord terms are fixed. | Useful only if your main evidence pack transfers cleanly. | Hold until blockers are cleared. |

| Vienna | Use EU-level context only. Verify Vienna-specific CBR participation directly. | Legal path, accommodation documentation, and verified full monthly burn. | Low until legal route is documented. | Low until total spend is modeled from real offers. | Good backup only if budget is already stress-tested. | Hold unless legal path and budget are both closed. |

| Debrecen | Hungary appears in listed CBR participants, so the same national VAT-ruling conditions may matter if relevant. | Stay route, local document sequence, housing proof, and the current national threshold to confirm with the national tax authority if the SME route matters. | Medium only after Hungarian checks are complete. | Low until written housing terms are in hand. | Strong if it can reuse the same Hungary-level documents as Budapest. | Conditional fallback book after Hungary checks are closed. |

| Tie-break rule | If two cities look equal, choose the one with fewer open verify before commit items. | If still tied, choose the one whose fallback can reuse the same identity, income, insurance, and accommodation evidence pack. | Clearer beats cheaper at this stage. | Certainty beats optimism. | Reusable documents beat starting over. | Book only when blocker items are closed. |

Practical check: save the date on every official page behind legal or tax assumptions. If CBR is relevant, keep the 19 April 2024 public info notice in your evidence folder as the current reference point before you verify national conditions.

Then remove any city with unresolved legal-path blockers and rank the rest by dependency count before rent, neighborhood, or social scene. Need the full breakdown? Read The Best Digital Nomad Cities for Entrepreneurs and Startups.

Prague is best for professionals who want structure over spontaneity#

Choose Prague if you can run your move as a process, not a gamble: legal path first, appointment path second, document order third, money last. If that chain is not clear on paper, keep Prague as a candidate, not a commitment.

What structure means in practice#

For you, "structure" means an admin-first sequence with dated proof at each step. Confirm the legal stay route on current official pages, map which document unlocks each next step, then test or document the appointment route before you commit housing funds.

Keep the VAT context short and operational. Use stable EU anchors as filters: the 1 July 2021 rule changes, the EU-wide EUR 10 000 threshold, and OSS as an optional scheme. If OSS applies, map the filing cadence before you commit: quarterly for non-Union and Union, monthly for import. If your case depends on a Member State of identification, account for possible lock-in for the current year plus two following calendar years.

Treat CBR and the cross-border SME scheme as verification tasks, not reasons to rush Prague. CBR is for advance VAT treatment on complex cross-border transactions and follows national ruling conditions where you are VAT-registered. If the SME route matters, use EUR 100 000 as the EU filter, then keep the current Czech threshold pending until it is verified on an official page. Exemption starts only after MSEST confirms the EX number, and the 35 working day timeline can extend when anti-evasion checks are required.

Use one evidence pack and one hard gate#

Build one evidence pack before you pay anything: identity, income proof, insurance, draft accommodation terms, and any VAT workflow documents in one dated folder. Save official snapshots from europa.eu and any national pages you rely on. If CBR might matter, keep the 19 April 2024 public info notice in your folder as a reference point, then re-check current national conditions.

Use one rule: if any blocker is open, deposits wait.

When Prague moves up and when it stays on hold#

- Move Prague up when your legal path is confirmed on dated official pages, your appointment route is documented enough for your timeline, your accommodation proof format is checked, and your fallback city can reuse the same evidence pack.

- Keep Prague on hold when the legal path is still unclear, the booking sequence is not locked, or VAT dependencies still have unresolved national conditions, including CBR usability or a threshold you still need to verify.

Related: The Best Cities for a Workation in Europe.

Budapest is best for balancing livability and flexibility#

Budapest is a strong choice when you want flexibility without loosening compliance. Commit in this order: confirm your legal route, map your tax posture, then keep housing, deposit timing, and arrival window flexible.

This is controlled optionality, not informal planning. You can leave practical variables open, but only after the non-negotiables are documented.

What you should lock before you call it flexible#

Start by confirming your legal stay basis on current official pages and saving dated copies of what you rely on. Then check whether your activity creates VAT touchpoints now. If you have cross-border B2C services or goods, use the 1 July 2021 changes and the EUR 10 000 threshold as your first filter.

| Framework | How to treat it | Key condition |

|---|---|---|

| OSS | Confirm whether registering through one Member State of identification fits your setup | Optional; if you use it, you must report all supplies covered by that scheme through the OSS return. Union/non-Union is quarterly; import is monthly. |

| CBR | Use this when you need an advance ruling on a complex cross-border VAT transaction | Hungary is in the participating set. Requests are filed in the participating country where you are VAT-registered, under that country's ruling conditions. |

| Cross-border SME scheme | Treat this as eligibility work, not an assumption | Union turnover cap is EUR 100 000. Prior notification is filed in your Member State of establishment, and exemption starts only when EX-number use is confirmed. |

Use each EU framework as a decision gate:

- OSS: Confirm whether registering through one Member State of identification fits your setup, then map the filing cadence before you commit. OSS is optional, but if you use it, you must report all supplies covered by that scheme through the OSS return. Union/non-Union is quarterly; import is monthly.

- CBR: If you need an advance ruling on a complex cross-border VAT transaction, Hungary is in the participating set, but the filing rules still come from Hungarian national conditions. Keep the 19 April 2024 public info notice in your evidence folder as a checkpoint, then re-verify current conditions.

- Cross-border SME scheme: Treat this as eligibility work, not an assumption. The Union turnover cap is EUR 100 000, prior notification is filed in your Member State of establishment, and exemption starts only when EX-number use is confirmed. Keep the current Hungarian national threshold pending until it is verified on an official page.

How to plan a real trial period#

A Budapest trial period works only if you keep the right things flexible. Keep your neighborhood, first lease format, and arrival window adjustable. Do not keep documentation completeness or official verification adjustable.

Delay long commitments until your evidence pack is complete: identity, income proof, insurance, draft accommodation terms, and any VAT-related records that affect your setup. If SME timing matters, plan around the stated 35 working day target, with buffer for cases that take longer.

Quick risk check#

Move Budapest from primary choice to backup if any of these are still open:

- Your legal route still depends on forums or old checklists.

- Your VAT posture depends on OSS, CBR, or SME treatment you have not confirmed on official pages.

- You are about to pay a deposit before your documents are complete.

- Your plan assumes a threshold or exemption you have not verified for the current country.

If those dependencies are closed, Budapest remains a strong balance option. For a step-by-step walkthrough, see The Best Digital Nomad Cities in Southeast Asia.

Warsaw is best for operations-first planners#

Pick Warsaw if you want your move run like an execution plan: verify first, then commit.

You are a fit if#

- You prefer to close dependencies in order and keep dated proof of each check.

- You confirm your legal stay route on current official pages before paying deposits or booking flights.

- You keep one evidence folder ready early: identity, income proof, insurance, and draft accommodation terms.

- You want your cross-border VAT workflow mapped upfront, including whether OSS, CBR, or the cross-border SME scheme is actually relevant to your setup.

- You are comfortable with OSS being managed through one Member State of identification, with ongoing filing, payment, record-keeping, and audit duties.

You are not a fit if#

- You want to choose the city first and settle compliance details after arrival.

- Your plan depends on unresolved thresholds or rule-change dates that have not been confirmed on official pages.

- You are not willing to keep a fallback city active while critical checks are still open.

Keep this checklist active#

- Verify your legal path using current official sources only.

- Confirm your document stack is complete, not almost complete.

- Validate tax workflow assumptions, especially OSS, CBR, and cross-border SME applicability.

- Keep a fallback city live until critical checks are closed.

If you use an OSS Member State of identification in eligible Union-scheme scenarios, that choice can bind you for the current year plus two following calendar years. If the SME route applies, VAT exemption starts only after the EX number is granted. The registration process should not take longer than 35 working days, but it can take longer when anti-evasion checks are required.

The tradeoff is simple: Warsaw favors process reliability over spontaneity. If your style is document first, decision second, keep Warsaw high on your shortlist. If your style is arrive first, sort later, move it down. We covered this in detail in The Best Digital Nomad Cities for Affordable Living.

Bratislava, Vienna, and Debrecen are smart alternatives when your first pick fails#

If Prague, Budapest, or Warsaw stalls, pivot without rebuilding your plan. Keep your legal path, tax logic, and document pack stable, and change only what is city-dependent.

Use this pivot rule: keep non-city dependencies fixed unless official guidance requires a change. If OSS is in scope, you still register in one single Member State of identification, and supplies under that scheme are declared through OSS returns. If CBR may be needed, file in the participating EU country where you are VAT-registered, under that country's national conditions. Keep any country-specific filing condition pending until it is verified on an official page.

Bratislava#

Use Bratislava when your priority is continuity.

Keep your identity, income proof, insurance, and work documents as-is, and update only city-dependent items like draft accommodation terms and local appointment assumptions. Before spending, make sure your official screenshots are current, dated, and still match your route.

Vienna#

Use Vienna when predictability matters more than flexibility.

Keep the same verify-first, book-second sequence. If your OSS setup depends on a fixed-establishment choice, that decision can bind you for the calendar year of the decision plus the next two calendar years. Treat the city switch as an execution change, not a reset of tax assumptions. Re-check only jurisdiction-dependent items. Keep any country-specific registration condition pending until it is verified on an official page.

Debrecen#

Use Debrecen when you need more runway to execute with fewer moving parts.

If the cross-border SME scheme is relevant, re-check the gates before moving money: file one prior notification in your Member State of establishment, confirm the EUR 100 000 Union turnover ceiling is still met, and wait for EX-number confirmation before relying on VAT exemption in selected Member State(s). The process should not take longer than 35 working days, but it can run longer when anti-evasion checks are needed.

Before any deposit or flight, run this pre-spend gate:

- Keep one documentation folder and update only city-dependent files.

- Refresh official screenshots for stay, tax, and registration rules so dates are current.

- Confirm where OSS, CBR, or the SME route sits after the pivot.

- Pause payment if any key rule is still pending official verification.

A controlled pivot preserves momentum; a rushed pivot repeats the same failure. Related reading: The Best Digital Nomad Cities for LGBTQ+ Travelers.

The first 30 days checklist before you book flights or housing#

Follow this order, not your excitement: legal path, evidence folder, verification checkpoint, delay plan, then money operations. Do not book flights or housing until your core checks are documented, dated, and consistent.

| Step | What to do | Completion signal |

|---|---|---|

| Define your legal path first | Write a one-paragraph summary of where you are based, what you sell, whether OSS is in scope, whether a VAT Cross-border Ruling (CBR) might be relevant, and whether the cross-border SME route applies | Your summary has no guesswork; unresolved filing conditions are clearly marked as pending official verification. |

| Build one evidence folder and keep it narrow | Create one dated folder with six parts only: identity, income, insurance, accommodation terms, official screenshots, and unresolved items | Someone else can open the folder and understand in two minutes what is confirmed, what is pending, and what still needs an official check. |

| Run a verification checkpoint before any payment | Before spending, re-check your screenshots against current official pages. For OSS, verify registration, declaration/payment, record-keeping/audits, and leaving the scheme | Every action item is either backed by a current screenshot or marked unresolved. |

| Write your delay plan before delay happens | Set your fallback order now: housing length first, arrival date second, city third | You have a written fallback note that states exactly what gets postponed and what does not. |

| Set money operations last, not first | After steps 1-4 are documented, set your invoicing, payout routing, and record routine | Your notes, screenshots, and folder all point to the same conclusion. |

- Define your legal path first

Write a one-paragraph summary of where you are based, what you sell, whether OSS is in scope, whether a VAT Cross-border Ruling (CBR) might be relevant, and whether the cross-border SME route applies. If OSS is in scope, name your single Member State of identification. If the SME route might apply, note the EUR 100,000 Union turnover cap across the 27 Member States and that exemption starts only after EX-number confirmation. Completion signal: your summary has no guesswork; unresolved filing conditions are clearly marked as pending official verification.

- Build one evidence folder and keep it narrow

Create one dated folder with six parts only: identity, income, insurance, accommodation terms, official screenshots, and unresolved items. Use sortable filenames like 2026-03-21_passport.pdf and 2026-03-21_oss_registration_page.png. Completion signal: someone else can open the folder and understand in two minutes what is confirmed, what is pending, and what still needs an official check.

- Run a verification checkpoint before any payment

Before spending, re-check your screenshots against current official pages. For OSS, verify registration, declaration/payment, record-keeping/audits, and leaving the scheme. Keep notes simple, and mark unresolved legal items plainly as pending official verification, such as filing conditions or timing checkpoints. Remember the operational impact: Union/non-Union OSS returns are quarterly, import OSS returns are monthly, and OSS returns do not replace domestic VAT returns. If CBR is relevant, treat it as a path for complex cross-border transactions involving two or more participating EU countries under national ruling conditions. Completion signal: every action item is either backed by a current screenshot or marked unresolved.

- Write your delay plan before delay happens

Set your fallback order now: housing length first, arrival date second, city third. This keeps you from rewriting everything under pressure. If you have multiple fixed establishments and choose a Union-scheme Member State of identification, that choice can bind you for the current calendar year plus the next two calendar years in covered cases. For the SME route, treat 35 working days as a target, not a guarantee, because extra anti-evasion checks can extend timing. Completion signal: you have a written fallback note that states exactly what gets postponed and what does not.

- Set money operations last, not first

After steps 1-4 are documented, set your invoicing, payout routing, and record routine: one invoice naming rule, one payout archive, one monthly review note, and one VAT-record location. Make sure your money trail matches your chosen path: OSS records must support the relevant quarterly or monthly cycle; potential CBR paths need traceable transaction descriptions and counterparties. Completion signal: your notes, screenshots, and folder all point to the same conclusion. If they do not, wait to book.

Optional next steps: Can Digital Nomads Claim the Home Office Deduction? and Indonesia's B211A Visa: The De Facto Nomad Visa for Bali.

Conclusion#

The move usually succeeds because of execution order, not because you guessed the perfect city. Your last step is simple: shortlist, verify, document, then spend.

-

Pick a primary city and one fallback. Choose the option with fewer unresolved assumptions, not the one with the louder online reputation. The real advantage is continuity: if your first choice slips on timing, paperwork, or proof, your fallback should let you keep the same basic plan with the fewest re-checks.

-

Verify only against official pages before you book. Use the

europa.eudomain as your source checkpoint, then save screenshots and the date you checked them. If OSS is relevant, confirm the Member State of identification and keep the registration, return, and record-keeping pages. If the cross-border SME scheme may matter, keep your MSEST prior-notification note, Union turnover worksheet, and a reminder to confirm when an EX number can actually be used. -

Build one folder that another person could understand fast. Keep your official verification records, relevant tax-scheme notes, and a short note on open questions in one place. If a threshold or program metric is still pending official verification, treat that as unresolved, not as a detail to fix later.

-

Spend only after your pause triggers are cleared. Do not pay a deposit, sign a long lease, or lock flights while a core legal or tax assumption is still open. Once money is committed, small errors get expensive fast.

If your checklist is complete and you still have unresolved country or program questions, Talk to Gruv as the escalation step, not the first one.

Frequently Asked Questions

What should you decide first before choosing a digital nomad city in Eastern Europe?

Decide your legal and tax path before you rank neighborhoods or rent prices. Check first whether OSS, a VAT Cross Border Ruling (CBR), or the cross-border SME route could even apply to your setup, then save the official page screenshots and a one-paragraph case note in your evidence folder. If any core point is still pending an official rule-change reference or current threshold, postpone flights and keep using the shortlist method from the comparison section.

How should you compare Prague, Budapest, and Warsaw for a 3 to 9 month stay?

Compare them by unresolved dependencies, not by online momentum or aesthetics. Start with the city that leaves you with the fewest open items on housing terms, insurance proof, income traceability, and any VAT path in scope. If OSS is relevant, remember registration is in one Member State of identification. If two cities look equal, pick the one with the cleaner fallback and delay any long lease until your checklist section is fully closed.

Which documents should you prepare before booking flights?

Start with one narrow folder: identity, income, insurance, accommodation terms, official screenshots, and unresolved items. If OSS might matter, keep proof of the current registration route, the filing cadence that applies to your case, and a note that OSS returns are additional to domestic VAT returns, not a replacement. If the cross-border SME route is relevant, keep your prior-notification note, Union turnover working paper, and a reminder to confirm when an EX number is actually usable. Do not turn this into a huge document dump. Do not pay deposits until another person could open that folder and understand it in about two minutes.

What are the most common delays that derail relocation timelines?

A common delay is treating old tax guidance as current, especially after the 1 July 2021 EU cross-border B2C e-commerce VAT changes. Another common failure mode is assuming timing is fixed. For example, cross-border SME registration should not take longer than 35 working days, but it can take longer if extra investigations are needed, so save the date of your last official check and keep a buffer note. If you are considering a CBR, verify first that your transaction is actually complex and cross-border, then file only in the participating EU country where you are VAT-registered and only under that country’s national ruling conditions.

When should you choose Bratislava, Vienna, or Debrecen instead of your first choice city?

Switch when your first-choice city is blocked by timing, budget, or unresolved evidence, not when you are simply tired of waiting. Check first whether the move changes anything material in your legal path. This matters especially if you are choosing an OSS Member State of identification in a case where that choice can bind you for the calendar year plus the two following calendar years. Keep a short fallback memo showing what stays the same and what must be rechecked. If the block is still unresolved after your verification checkpoint, change city before you change legal assumptions.

How much should you trust city advice from Reddit, r/digitalnomad, and Facebook threads?

Treat community advice as a lead, not as evidence. Check first whether the post gives you something testable, such as a named authority page, a filing term, or a document label, then save the thread as context but keep only official screenshots and your own dated notes in the real evidence pack. If a comment cannot be tied back to an official source, do not let it drive deposits, deadlines, or your final choice.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Indonesia B211A Visa for Bali Remote Professionals in 2026

Get the route right before you book anything expensive. Your entry path sets the document load, sponsor coordination, extension pressure, and how much timing risk you carry into the move.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.