Quick Answer

Choose a debit card with no foreign transaction fee by verifying current issuer terms before you rely on it abroad. Check whether the no-fee claim covers purchases, ATM withdrawals, or both, then review ATM operator fees, monthly account fees, exchange-rate spread, dispute handling, replacement steps, and your backup plan. Discovery pages can help you build a shortlist, but issuer documents should decide the final choice.

What to Compare Before You Choose#

Pick your card stack with a verification-first process, not rankings. If you run freelance or small-team cashflow across borders, this article helps you build a debit card no foreign transaction fee setup that is more predictable in practice.

Use this filter before you switch cards.

- Claim Check: Start with issuer terms and account documents. Use directory pages to find options, then verify final terms with the issuer.

- Scope Check: Separate headline claims from what is explicitly covered. A listing can highlight credit-card terms without confirming debit-side costs or cash access behavior.

- Failure Check: Confirm what happens when a card is blocked, disputed, or replaced, and define a fallback before you rely on one card.

- Cashflow Check: Evaluate total monthly impact, not one label. If terms are unclear, treat that as risk.

Discovery pages still help as starting points. Mastercard's no-foreign-transaction-fee credit card category says users can compare partner offers and apply online, and at least one listed offer states $0 annual fee and no foreign transaction fees. Use that to build a candidate list, then validate your final choice in issuer documents.

Before you treat any card as primary, write a short pass list in your notes. Note what fee scope must be explicit, what ATM behavior must be explicit, and what fallback must be tested. That one page keeps comparisons consistent when you review multiple products quickly and helps you catch setup gaps early.

Who This List Is For and Who Should Skip It#

Use this list if you manage cross-border cashflow and want to separate payment-processing costs from debit-card costs. Skip it as your main decision tool if rewards optimization is your top priority.

- Best fit: Global freelancer invoicing internationally. If you collect through Stripe and need predictable cash access while moving between countries, this list is built for you. Stripe pricing lists

2.9% + 30¢for domestic cards, plus1.5%for international cards and1%for currency conversion, so card-side costs should be evaluated separately. - Best fit: Small team handling frequent Stripe Connect payouts. Connect pricing varies by model, including a path with no platform fees and another with

$2per monthly active account plus0.25% + 25¢per payout. A monthly active account is active in any month payouts are sent to its bank account or debit card. - Best fit: Reader who verifies terms, not rankings. Discovery pages are useful for options, but placement can be promotional. WalletHub states

Featuredproducts are ranked by advertiser status. - Skip as a primary tool: Rewards-first spender. If your main objective is maximizing credit-card rewards, a credit-led strategy can matter more than debit selection. WalletHub also notes many international travelers carry both a no-foreign-transaction-fee credit card and a debit card without foreign surcharges.

- Use as one layer only: High-volume, compliance-heavy business. Debit choice should support your payout setup, not replace it. Treat unclear ATM or monthly account fee terms as unresolved risk until verified with the issuer.

A practical boundary helps here. If you cannot explain your expected total monthly card cost in two or three lines using current issuer documents, your comparison is incomplete. Pause, collect missing terms, then continue.

If you match the first three groups, continue and compare options by total monthly impact. If you match the last two, treat this list as a support layer while credit and payout choices lead decisions.

The Fee Stack That Decides Your Real Cost Abroad#

Real international cost comes from a fee stack, not a single no-fee label. Compare every option on the same four line items, and reject any card where one recurring charge can erase expected savings.

| Fee item | What to verify | Why it matters |

|---|---|---|

| Foreign Transaction Fee | Whether no-fee wording applies to purchases only, ATM withdrawals only, or both | One source describes a common 1% to 3% range |

| ATM Operator Fee | Whether international withdrawals trigger a fee per transaction and whether the local bank adds its own charge | Cash access can still be expensive even if purchase fees look low |

| Monthly Account Fee | Whether a recurring charge applies | A recurring charge can erase expected savings |

| Exchange-Rate Spread | Whether conversion cost sits inside the rate, separate from listed fees | One comparison frames combined fee and exchange drag in a 3-5% range |

- Foreign Transaction Fee: Usually a purchase surcharge, with one source describing a common

1% to 3%range. You should confirm whether no-fee wording applies to purchases only, ATM withdrawals only, or both. - ATM Operator Fee: International withdrawals can trigger a fee per transaction, and the local bank may add its own charge. A card can still be expensive for cash access even if purchase fees look low.

- Monthly Account Fee: Some options are marketed with no monthly fee, but that is not universal. If a recurring charge offsets your expected savings, remove the card.

- Exchange-Rate Spread: Conversion cost can sit inside the rate, separate from listed fees. One comparison frames combined fee and exchange drag in a

3-5%range, so low visible fees alone are not enough.

Keep the review simple: verify fee terms in current issuer disclosures and confirm whether limits or conditions apply. If a supporting page is old, such as a page last updated January 4, 2025, treat the terms as stale until you recheck them.

Use one comparison sheet so each card is judged the same way. Put fee scope in one column, ATM behavior in one column, recurring account charges in one column, and unresolved wording in one column. If unresolved wording remains after document review, that card is still a maybe, not a yes.

Track card options in separate rows and confirm issuer wording before assuming the same outcome. If purchase-vs-ATM language is vague, move the card to your watchlist.

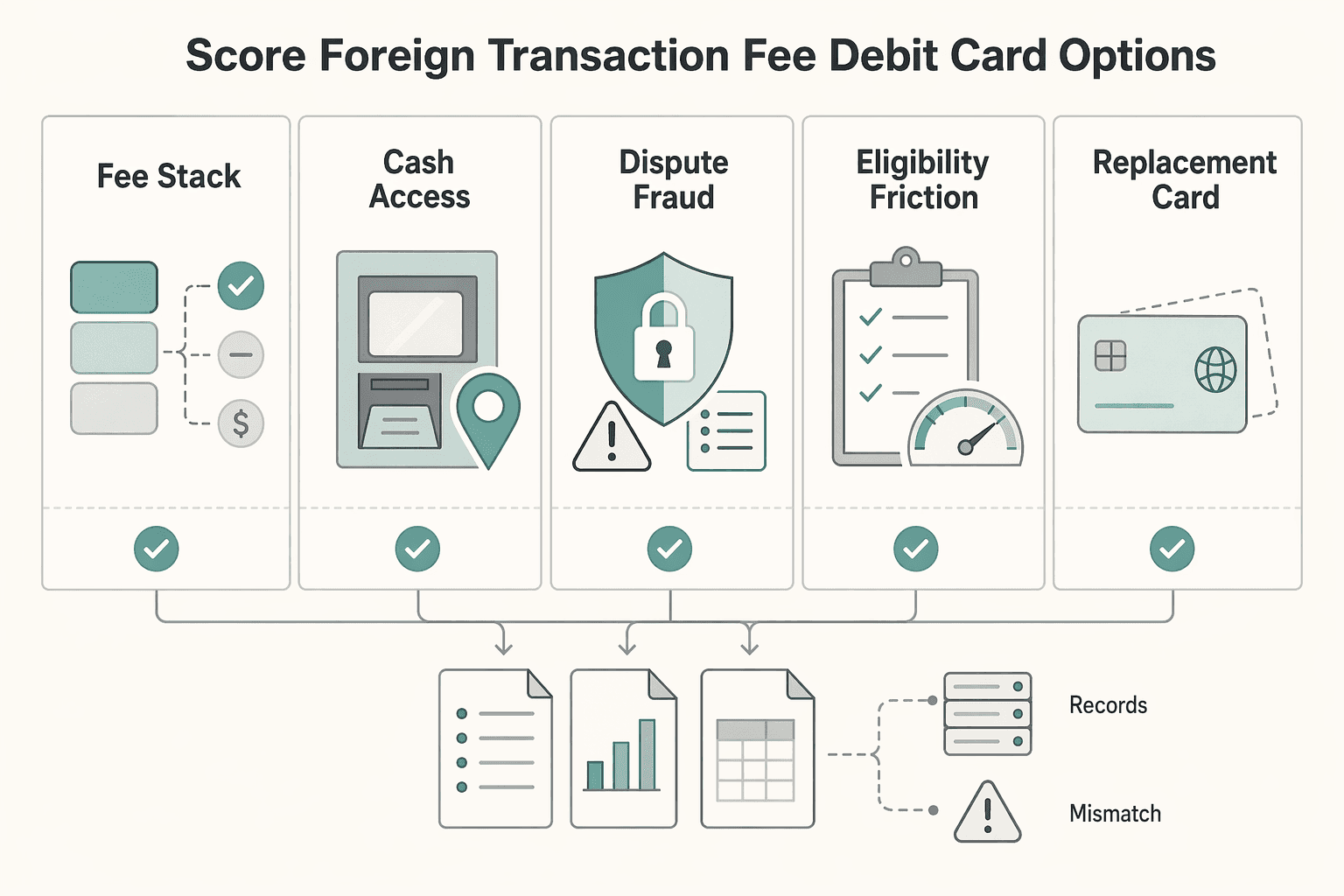

How We Score No Foreign Transaction Fee Debit Card Options#

A card is recommended only when terms are clear enough to predict likely cost and failure handling before travel, and when supporting documents are current and primary. Scoring is weighted across five areas and then checked against a strict evidence gate.

| Area | Weight | Pass condition |

|---|---|---|

| Fee stack transparency | 35% | Terms clearly cover Foreign Transaction Fee, ATM Operator Fee handling, Monthly Account Fee, and Exchange-Rate Spread |

| Cash-access reliability | 25% | Withdrawal rules are explicit enough for normal travel use |

| Dispute and fraud handling | 15% | Reporting and resolution steps are clear and verifiable in current account documents |

| Eligibility friction | 15% | Qualification and ongoing conditions are not difficult to track when status affects fees |

| Replacement-card practicality | 10% | Replacement steps are realistic for someone abroad |

- Fee stack transparency (35%): Terms must clearly cover Foreign Transaction Fee, ATM Operator Fee handling, Monthly Account Fee, and Exchange-Rate Spread, including whether no-fee language applies to purchases, withdrawals, or both. If a fee category is missing or scope is vague, the card moves to watchlist.

- Cash-access reliability (25%): Withdrawal rules must be explicit enough for normal travel use. If limits or conditions are unclear, the card does not pass.

- Dispute and fraud handling (15%): Reporting and resolution steps must be clear and verifiable in current account documents. If the process is hard to find, confidence drops.

- Eligibility friction (15%): We score how hard it is to qualify and stay qualified when status affects fees. If ongoing conditions are difficult to track, the card loses points.

- Replacement-card practicality (10%): Replacement steps must be realistic for someone abroad. If replacement terms are unclear, we treat that as direct cashflow risk.

Directory rankings can help you build a candidate list, but they are discovery inputs only. Final scoring requires issuer-level documents and a date check.

The evidence gate stays conservative on purpose. eCFR content is labeled authoritative but unofficial, and FederalRegister.gov says its web version is not the official legal edition and should be verified against official publications. One cited CFPB item is a proposed rule (12/23/2014) with a correction (02/05/2015). Unrelated material such as a Medicare drugs and biologicals manual chapter is excluded.

Apply this scoring in sequence, not all at once. First remove cards with missing fee scope. Then remove cards with weak cash-access language. Then compare only the survivors on dispute and replacement practicality. That order keeps you from spending time polishing choices that never had complete terms.

Decision rule: if terms are not clear in plain English, or evidence is outdated, unofficial-only, proposal-only, or off-topic, the card is watchlist, not recommended. Want a quick next step if you're comparing a debit card with no foreign transaction fee? Try the free invoice generator.

Quick Comparison Table and Decision Snapshot#

Use this table to eliminate weak options quickly, not to make a final selection. Keep each row on watchlist until issuer documents confirm fee scope and account conditions in plain English.

Cross-border spend can stack conversion markups, foreign transaction charges, and ATM withdrawal fees. Hidden international costs can materially raise total spend, so every row below is a verify-first checkpoint. Some roundups in this space are credit-card focused, so they are not proof for debit-card decisions.

| Card/Account | Best For | Foreign Transaction Fee | ATM Operator Fee handling | Monthly Account Fee | Network (Visa/Mastercard) | Key Caveat | Not a fit if... |

|---|---|---|---|---|---|---|---|

| Charles Schwab | Potential ATM-use case (verify issuer terms) | Verify current issuer terms for debit purchases and withdrawals | Verify how third-party ATM fees are treated, including limits and timing | Verify current account terms | Verify current debit card variant | Terms can change and may depend on account details | You need fixed terms without periodic rechecks |

| Capital One 360 Checking | Potential general-use case (verify issuer terms) | Verify exact foreign-use wording for purchases, withdrawals, or both | Verify international ATM behavior and local fee treatment | Verify current account fee policy | Verify current debit card variant | Scope language can be narrower than the headline | You rely on frequent cash withdrawals and cannot absorb possible ATM fees |

| HSBC Premier Checking | Potential fit to evaluate (verify issuer terms) | Verify current foreign-use fee terms | Verify ATM fee handling and any conditions | Verify whether any monthly fee applies and any waiver conditions | Verify current debit card variant | A recurring monthly charge can erase expected fee savings | You cannot absorb potential recurring fees |

Run the table in two passes. In pass one, mark any unclear cell as unresolved and do not fill gaps with assumptions. In pass two, check whether current issuer documents clear those cells. If not, keep the row on your watchlist. This keeps speed without sacrificing accuracy.

Decision snapshot: remove any option where recurring charges erase expected savings or fee wording stays unclear. Keep only rows with current issuer terms you can verify, then compare finalists.

Charles Schwab Option for ATM-Heavy Freelancers#

If you rely on ATMs often, keep Charles Schwab on your watchlist until you've verified current issuer terms on your own account. The support here is anecdotal: one travel writer says they have used a Schwab debit card since 2018, says they initially used it to avoid ATM fees, and says the endorsement is personal opinion.

Treat that as discovery input, not pricing proof. Before you rely on this row, confirm debit purchase and withdrawal fee scope. Verify ATM operator fee treatment, including reimbursement or pass-through language, and check any monthly account fee exposure. Also confirm the active network and replacement process for your travel footprint.

Verification sequence matters. Start with the account terms, then the fee schedule, then support pages for replacement and dispute handling. If wording conflicts across those pages, use the strictest interpretation for planning until support clarifies in writing.

Capital One 360 Checking for Mainstream Simplicity#

Keep Capital One 360 Checking in the convenience category, but only as a watchlist option until your current account documents clearly define the full fee stack. This row works only when foreign-fee scope, ATM operator fee handling, and any monthly account fee conditions are explicit and current.

Again, the problem is documentation quality. The available documentation does not confirm Capital One 360 Checking debit terms.

Do one pre-reliance check before travel. Confirm whether any foreign-fee wording applies to purchases, withdrawals, or both. Confirm how any ATM operator fees appear on statements, including limits and timing. Confirm any monthly fee triggers and waivers, then confirm lock, replacement, and support steps.

For a freelancer paid through Stripe who uses occasional cash withdrawals, unclear withdrawal language can erase expected savings. If purchase terms are clear but withdrawal terms are vague, keep this row on your watchlist and carry a backup debit card.

If support can only point you to general marketing language and cannot identify the exact cardholder terms, that is a hard stop for primary use abroad. Clarity is part of cost control here, not a paperwork preference.

HSBC Premier Checking for Premium Users Who Can Justify the Monthly Account Fee#

Start with the economics. If your local Premier Checking variant includes a Monthly Account Fee, it fits only when that cost is consistently justified by your real usage. If that fixed cost hits during low-activity months, fee savings elsewhere can disappear.

The tradeoff is fixed monthly cost versus variable international fees. Many UK debit cards can still charge up to three per cent in foreign transaction fees. Some cards may add withdrawal costs after limits, so headline no-fee wording is not enough on its own.

The clearest HSBC-specific details available are for the HSBC UAE Global Money Account, not Premier Checking terms. That FAQ says Global Money can hold up to 21 currencies and is only available in the HSBC UAE app. It also says direct cheque or cash deposits are not allowed, and that instant multi-currency transfers to other HSBC customers can be supported without fees. Treat those details as product context, not proof of Premier Checking pricing, waiver thresholds, or ATM policy in other markets.

Before you commit, decide what monthly value would need to be true if a fee applies in your market. Then test that assumption against one higher-use month and one lower-use month. If the low-use month fails your own threshold, a fixed charge is probably too fragile for your baseline setup.

Checkpoints before you commit#

- Pull the current Premier Checking fee schedule for your country and confirm exact Monthly Account Fee wording (if any), including any waiver conditions and review timing.

- Separate purchase terms from withdrawal terms, then verify how any ATM Operator Fee is handled for cash withdrawals abroad.

- Check whether any feature you value depends on a specific app, geography, or account variant, so you do not map UAE Global Money terms onto your local Premier account.

- Run a two-month test with your real behavior, including one higher-spend month and one lower-spend month, and compare total fees.

A likely fit is a high-balance consultant who uses global banking features regularly and can meet any local account conditions without changing normal behavior. A poor fit is uneven travel usage, where low-activity months can turn a fixed charge into avoidable overhead. Keep this as a candidate only after local documents are clear and your cost check holds up. Related: The Best Debit Cards for International Travel.

Fintech Options and the Verification Checks Before You Trust Them#

With fintech options, issuer-term verification has to come first. Comparison posts and community threads can help you build a shortlist, but they are not policy evidence for a final card choice.

Treat discovery content as a starting point:

- Holafly includes promotional language, such as a discount-code prompt, so use it to find options, not confirm terms.

- Nomadgate-style fee commentary can surface risks, but it is still editorial framing.

- A third-party Visa collaboration announcement can describe partnerships or security positioning without proving debit-card fee policy.

Regulatory pages provide context, not a shortcut around issuer terms. FederalRegister.gov shows a Proposed Rule entry on 11/14/2023 (88 FR 78100) and an earlier Rule on 07/20/2011 (76 FR 43394), with related later entries noted on each page. It also states its XML/prototype rendering is unofficial and should be verified against an official edition before legal reliance.

Use a three-tier evidence check when you compare fintech claims:

- Tier 1: Issuer fee schedule and cardholder terms.

- Tier 2: Issuer support pages for disputes, replacement, and regional service.

- Tier 3: Directory pages, community posts, and commentary.

Only Tier 1 and Tier 2 can move a card from watchlist to primary use.

Pre-switch checks for fintech claims#

- Fee disclosure page: confirm exactly how foreign transaction fees are described.

- ATM policy page: require explicit ATM Operator Fee handling.

- Dispute path: verify how a dispute is opened and tracked.

- Card replacement path: confirm replacement steps and timelines.

- Regional support coverage: confirm where support is actually available.

- Document control: save dated copies of key terms before switching.

Cross-check claims from community forums and comparison pages against primary issuer terms. If a claim cannot be matched to explicit policy text, treat it as unverified.

Decision rule: if an option does not publish explicit ATM Operator Fee handling, keep it out of your primary card stack.

Pairing Debit With a No Foreign Transaction Fee Credit Card#

A practical setup is a split stack: keep a debit card with no foreign transaction fee for ATM cash access, and use a no-FTF credit card for everyday purchases.

- Cash rail: debit for ATM withdrawals.

Use debit as a cash tool, not your primary spend card. Even with no foreign transaction fee, ATM costs can still change based on limits and thresholds. One published debit example shows free ATM use up to 2 withdrawals and 100 USD per month, then 1.5 USD + 2% after that.

- Spend rail: credit for card-present and online purchases.

Route travel and merchant charges to a no-FTF credit card, and keep debit focused on cash access. If an issuer page is temporarily unavailable, pause and verify terms in current cardholder documents before relying on that card abroad.

- Verification rail: shortlist first, then verify line by line.

Discovery pages can help you find options, but they are not policy evidence. A page labeled ADVERTISER DISCLOSURE is your cue to confirm terms directly with the issuer. If your shortlist includes specific cards, verify foreign transaction fee language, ATM cash treatment, and replacement-card logistics in writing.

This split setup gives you a fallback path if one rail is disrupted. If debit cash access is interrupted, purchases may still clear on credit. If credit has a temporary fraud block, debit may still cover urgent local cash needs. The point is one fallback path that you test before travel.

Keep one rule in front of you: if either card has unclear international fee wording, do not put it in your primary travel stack yet.

Red Flags That Turn a No-Fee Card Into a Cashflow Problem#

A no-fee headline is not enough on its own. Fraud is still a real risk, so keep a card out of your primary stack until fraud controls and recovery steps are clear in writing.

- Unusually large transactions that are not system-flagged

An unusually large order is a practical red flag. If your system is not set up to flag that pattern, treat it as unresolved risk and avoid relying on that card setup for critical spend.

- Assuming only online fraud matters

Online fraud may be more common, but in-store purchases also carry risk. If your checks only cover one channel, your protection is incomplete.

- Unclear process for suspicious activity

Fraud can surface in multiple channels and needs fast handling. Confirm, in writing, how suspicious charges are flagged and how issues are reported and escalated. If those steps are not explicit, the card is not ready for your core setup.

Treat unresolved as binary, not partial. If one red flag stays open after document review and support follow-up, do not downgrade the risk because the other areas look strong. A single unresolved failure point can still interrupt access at the wrong time.

Decision rule: if any one of these red flags remains unresolved after checking documents and support, do not use that card in your primary travel stack yet.

30-Minute Setup Checklist Before You Fly or Invoice International Clients#

Use one timed setup pass to verify current terms, test real transactions, and document fallback steps before this card becomes part of your primary setup.

- Capture current terms before you transact

Save dated screenshots of your issuer's exact wording for Foreign Transaction Fee, ATM Operator Fee (if shown), and Monthly Account Fee (if any). If Stripe is part of your flow, save its current baseline too: Standard pricing says there are no setup fees, monthly fees, or hidden fees.

- Run one purchase test and one ATM test, then log outcomes

Make one small live purchase and one ATM withdrawal, then record timestamp, currency, and posted amount in your finance tracker. If you process payments with Stripe, compare results against current listed pricing (2.9% + 30 cents domestic, plus 1.5% for international cards, plus 1% when currency conversion is required) so mismatches are visible quickly.

- Set backup rails and write recovery steps

Keep one debit card and one credit card active. In the same note, document freeze and unfreeze steps, replacement path, and who to contact if access is interrupted.

- Map payout-fee ownership before volume scales

If you use Stripe Connect and handle pricing, assign one owner to review monthly active account and payout charges each month ($2 per monthly active account and 0.25% + 25 cents per payout sent), and define an escalation contact for unexpected fee movement.

- Revalidate monthly because terms can move

Set a recurring monthly check to re-read fee pages and compare against your latest test logs. Stripe's gateway-fee guidance states costs are subject to change, so treat every fee assumption as time-sensitive and re-confirm it.

Use a simple logging format so monthly reviews stay fast: date checked, document reviewed, what changed, and whether your primary stack still passes. Fast reviews are more likely to happen, which is what protects you from stale assumptions.

Conclusion and Next Step for a Reliable Get-Paid System#

Your next move is simple: choose the option you can verify, not the one with the strongest headline.

- Decide on total cost and reliability together. Use the same table and checklist criteria from this article, then keep only options you can confirm in issuer terms.

- Test before you depend on it. Run a small purchase first, and confirm posted results match what your terms say.

- Document your operating steps. Keep one short note with support, replacement, and emergency actions so your next trip or client cycle starts from a tested process.

- Expand only when card-only setup no longer fits. Add another payment rail only when terms, controls, and recordkeeping expectations are clear.

If a key term is unclear, pause and confirm it before treating that card as part of your primary stack.

Frequently Asked Questions

What does 'no foreign transaction fee' on a debit card actually cover?

It covers the foreign transaction surcharge itself, not every possible international cost. The article notes that when this surcharge is charged, it is generally in the 1% to 3% range. Check purchase terms and ATM withdrawal terms separately so you know what the label actually covers.

Can I still pay ATM fees even if my debit card has no foreign transaction fee?

Yes. A no-foreign-transaction-fee label does not by itself explain ATM operator fees or local bank charges. Check your issuer's ATM and fee disclosures, and treat cash costs as unknown until the terms are explicit.

Is one no-FTF debit card enough, or should I pair it with a no-FTF credit card?

One card can work, but the article recommends a split stack if you want a backup rail. Use debit for ATM cash access and a no-foreign-transaction-fee credit card for everyday purchases. Verify the foreign transaction fee terms on both cards before you rely on either one.

What is the fastest way to compare debit cards without missing hidden international costs?

Use one comparison sheet and verify the same four line items for every card: foreign transaction fee scope, ATM operator fee handling, monthly account fee, and exchange-rate spread. Read issuer fee disclosures instead of relying on summary pages. If any fee category is missing or unclear, keep the card on your watchlist.

Which single fee most often cancels out no-FTF savings?

The article does not name one universal fee. Its point is that no foreign transaction fee removes one surcharge, not all possible costs. Review the full fee stack against your own usage before choosing.

What checklist should freelancers use before choosing an international debit card?

Use a short checklist: confirm whether a foreign transaction fee exists, whether the terms apply to debit transactions, and what the fee scope covers. Then verify ATM operator fee handling, monthly account fee, exchange-rate spread, dispute steps, replacement steps, and your fallback card. Keep dated notes so rechecks stay fast.

How often should I re-check card terms after I choose one?

The article does not give a fixed interval. It recommends re-checking before you depend on the card internationally, revalidating monthly because terms can move, and checking again if your usage changes. If wording is unclear, pause and confirm with the issuer before transacting.

Watch

Best Debit Cards With No Foreign Transaction Fees

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- fdic.gov/system/files/2024-06/2023-regulatory-capital...trusted

- federalregister.gov/documents/2023/11/14/2023-24034/debit-card-i...trusted

- federalregister.gov/documents/2011/07/20/2011-16861/debit-card-i...trusted

- ftc.gov/sites/default/files/documents/federal_regist...trusted

- bankrate.com/credit-cards/travel/best-no-foreign-transact...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

The Best Debit Cards for International Travel

If reliable cash access is the priority, do not evaluate this like a perks list. Treat it like continuity planning. Give one card the everyday ATM job, fund a second card for disruptions, and decide that split before you leave.

OFAC Sanctions Screening for Global Businesses

Treat **OFAC sanctions screening** as a payment control, not a formality. If your business touches cross-border counterparties or transactions that may fall under U.S. jurisdiction, screening can help protect your ability to move money when pressure is high. The Office of Foreign Assets Control (OFAC), within the U.S. Treasury, can block property, freeze assets under U.S. jurisdiction, and prohibit certain transactions involving sanctioned parties, countries, or regions.