Quick Answer

Choose a primary debit card plus a funded backup as your default for the best debit card for international travel decision. Confirm foreign transaction fees, ATM charges, and decline-recovery steps in your own account, then test both cards with small withdrawals before departure. For Charles Schwab, verify current terms in the Schwab Bank Debit Card Benefits Guide instead of relying on roundup claims.

What to Look for in a Debit Card for International Travel#

If reliable cash access is the priority, do not evaluate this like a perks list. Treat it like continuity planning. Give one card the everyday ATM job, fund a second card for disruptions, and decide that split before you leave.

That choice removes the most common failure point. When a card is blocked, lost, or suddenly more expensive than expected, you are not standing in front of an ATM trying to improvise. You already know which card is for normal withdrawals, which card is for disruptions, and how much each one needs to cover essentials.

Keep that split simple. Your primary card handles routine withdrawals. Your backup card exists for interruptions, not convenience spending. In practice, that distinction protects emergency capacity and makes troubleshooting much faster when something goes wrong abroad.

This guide stays focused on debit and prepaid debit options for international cash access. Prepaid options can help with spending limits and overdraft control, but they come with a hard constraint. Once the balance is depleted, withdrawals and purchases stop until you top up. That can be useful for control, but it becomes a problem if you mistake a capped spending tool for a full continuity plan.

Multi-currency cards can add real control when a trip crosses currencies. The operating sequence is straightforward: top up, convert, then withdraw. That can make costs easier to read, but only if you check live terms for your own plan tier and country before you rely on them. If those terms change between trips, old assumptions can fail even when the app still looks familiar.

Before comparing brands, confirm these mechanics in your own app and account documents:

- Foreign transaction fee and any conversion markup

- ATM withdrawal fee at the card-program level

- Whether ATM reimbursement exists and where limits apply

- Freeze, unblock, and support steps if a transaction fails abroad

Those checks usually matter more than the marketing label on the card. Combined fee drag and exchange slippage can still land around 3% to 5% in some setups, and prepaid availability varies by country. For a plain-language baseline on foreign transaction fees, use the CFPB explainer. Therefore, no single option is cheapest for every travel pattern.

The bigger mistake is over-optimizing one visible fee while ignoring recovery behavior. A card that looks cheaper in a static comparison can still cost more overall if support is slow, block handling is vague, or the fallback card was never funded.

Use what follows as a practical filter. First verify cost mechanics. Then verify what happens when something breaks. After that, assign each card a role and test those roles under low stress before departure.

Who this list is for and not for#

This list is for travelers who care most about predictable cash access and fewer fee surprises. It is not a rewards ranking, and it is not trying to name one universal winner.

If continuity is your first concern, the priorities here are in the right order. Some debit products still apply foreign transaction fees, and ATM operators can add their own charges even when issuer-side terms look attractive. The useful question is not what the product page suggests, but what happens on a real withdrawal in the destination where you will actually use the card.

If rewards matter more to you than continuity, use this process as the base layer and add points optimization only after the cash-access checks are done. You can still chase rewards, but it should not come at the cost of having no cash plan when a card fails. Reliability should be the floor.

If tighter spending control matters, multi-currency options deserve a serious look. Wise positions its Multi-Currency Card for travel spending, but plan details, thresholds, and limits still need live confirmation in your own account before you make it part of your core setup.

This guide is especially useful if losing one card would materially disrupt your week. In that case, backup planning is not optional. Set fallback access before departure, keep both cards funded for essentials, and recheck pricing and limits for each trip. Terms can change by date, country, and plan tier, so old screenshots are not enough.

Who this is not for: travelers who want a single-card setup and are comfortable absorbing occasional fee surprises, or readers focused mainly on rewards and lounge perks. That approach can still work, but it sits outside the risk posture this guide is built for. If you choose it anyway, at least keep a basic fallback method so one block event does not turn into a full cash interruption.

Read this as an operating guide for disruption risk and cost clarity. If your goal is uninterrupted access to money while traveling, start here. If your goal is rewards yield, keep the same order of operations and add the rewards filter later.

The next step is to score cards the same way every time. Once you do that, product selection gets much more straightforward.

How to score travel debit cards before you pick one#

Start with repeatable costs, then look at recovery. A card can sound cheap in marketing copy and still fail at the moment you need cash.

| Criterion | Verify | Grounded note |

|---|---|---|

| Foreign transaction fee | Current fee in your account terms | A commonly cited range is 1% to 3%. |

| ATM withdrawal fee at both layers | Issuer-side charges and ATM operator charges | Repeated small withdrawals can quietly increase total drag. |

| ATM reimbursement policy | Whether reimbursement language is current and explicit | Delayed reimbursement may still be useful, but it does not solve immediate liquidity pressure. |

| Foreign conversion mechanics | Current plan terms, timing, and weekend behavior | Revolut Standard is described as no exchange fee Monday to Friday for 25+ currencies, then 1% on weekends, with a $1,000 monthly exchange limit that includes card spending. Wise says spending converts at the mid-market rate, with $100 per month in overseas ATM withdrawals before a 2% fee, plus possible ATM network charges. |

| Reliability and continuity checks | Block behavior, fraud controls, support access, and dispute clarity | Reported examples include country-level transaction blocks and cases where a travel notice did not restore card use. |

Score options in a fixed order, cost first and continuity second:

- Foreign transaction fee

Start here because this fee can apply across eligible purchases abroad. A commonly cited range is 1% to 3%, and even small differences add up across multiple transactions. If your spending pattern includes frequent small purchases, this line item can quietly outrun your ATM savings.

- ATM withdrawal fee at both layers

Do not model only issuer fees. One withdrawal can include issuer-side charges plus ATM operator charges. Withdrawal frequency matters too, since repeated small withdrawals can quietly increase total drag. Compare options using your likely withdrawal cadence, not an idealized one-withdrawal month.

- ATM reimbursement policy

Reimbursement improves net cost only when the language is current and explicit. If terms are vague, conditional, or hard to verify, treat reimbursement as uncertain. Also check timing. Delayed reimbursement may still be useful, but it does not solve immediate liquidity pressure.

- Foreign conversion mechanics

Use current plan terms, not memory. Revolut Standard is described as no exchange fee Monday to Friday for 25+ currencies, then 1% on weekends, with a $1,000 monthly exchange limit that includes card spending. Wise says spending converts at the mid-market rate, with $100 per month in overseas ATM withdrawals before a 2% fee, plus possible ATM network charges. This is where many comparisons go wrong, because they ignore plan tier, timing, or weekend behavior.

- Reliability and continuity checks

Fee math matters, but it is not enough. Confirm block behavior, fraud controls, support access, and dispute clarity. Reported examples include country-level transaction blocks and cases where a travel notice did not restore card use. A low-cost card that is hard to unblock under stress is not a strong primary choice.

For each score item, add one proof note. Record the terms page, app screen, or official document that supports the number or condition, and note the date checked so stale assumptions are easy to catch before the next trip.

A simple scoring method keeps this practical:

- Mark each criterion as clear, unclear, or conditional.

- Attach one source note and one date to each mark.

- Flag anything unclear as secondary-use only until resolved.

After scoring, compare candidates on one sheet and assign roles, not just ranks. If pricing is strong but recovery is weak, that card should not be your only cash path. If scores are close, break the tie in favor of clearer support access and simpler recovery steps.

That scorecard is what makes the comparison table useful. Without it, the table is just a list of brand names.

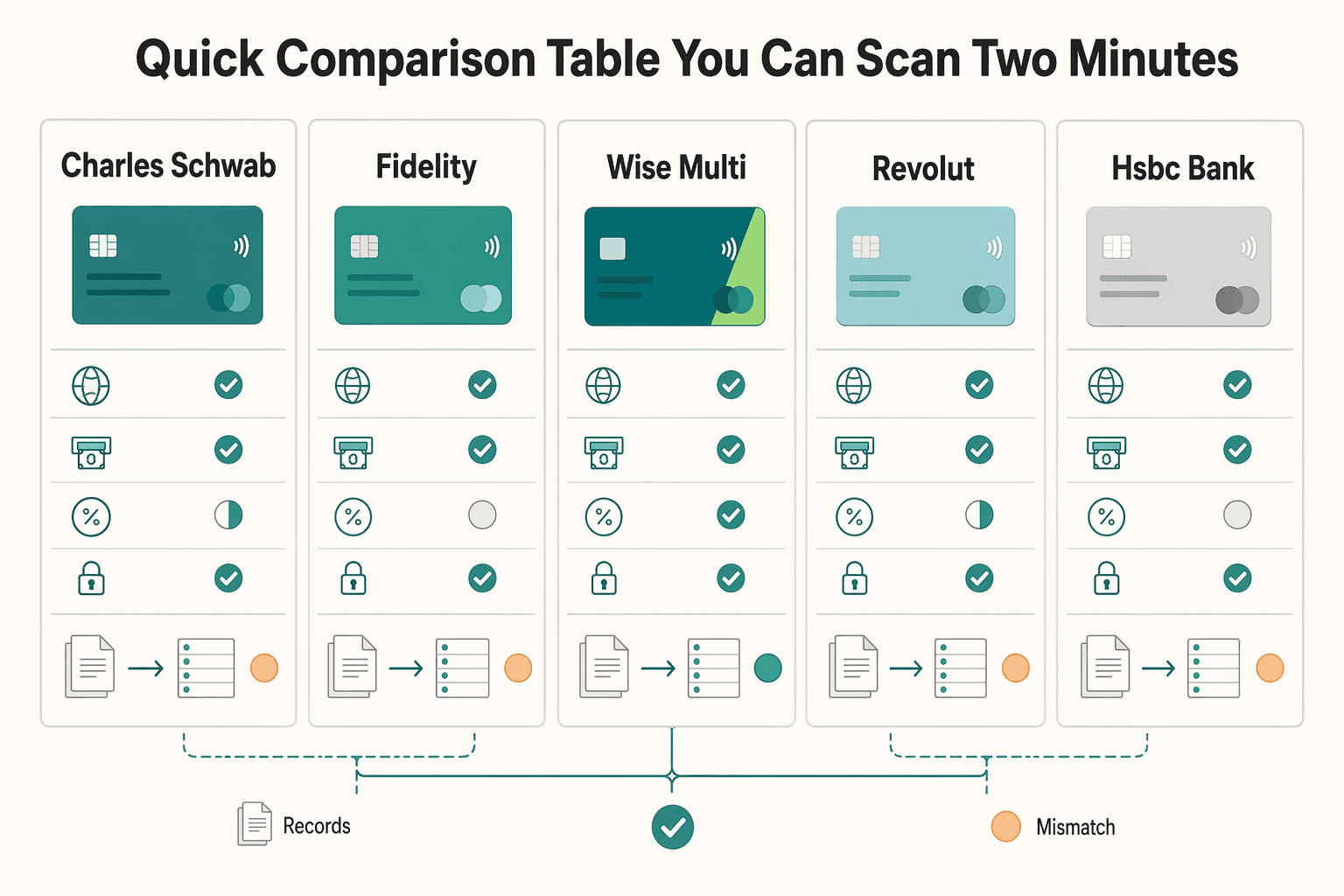

Quick comparison table you can scan in two minutes#

Use this table to build a shortlist, then validate each row against your live account details. Think of it as a decision screen, not a final answer.

| Card or account | Best for | Fee focus to verify | Reliability checkpoint | Best role in stack |

|---|---|---|---|---|

| Charles Schwab | Bank-led primary cash access | Verify ATM and foreign-use terms in live account documents. Unknown or variable by account setup and date. | Confirm support contacts and card-control steps before travel. | Primary cash card candidate after term verification |

| Fidelity | Low-friction backup access | Verify ATM withdrawal fee, foreign-use terms, and account conditions. Unknown or variable by account type and date. | Confirm fallback access if your first card fails abroad. | Backup travel card candidate |

| Wise Multi-Currency Card | Multi-currency budgeting with transparent published pricing | Verify current card costs: 9 USD card fee, ATM allowance of 100 USD per month and up to 2 withdrawals, then 2% plus 1.50 USD per withdrawal. | Use the Wise calculator and regulator-standardized fee document to confirm current numbers before travel. | Currency buffer card, or primary for some profiles |

| Revolut | App-led secondary spend control | Verify plan-dependent conversion and ATM withdrawal rules for your exact tier. Unknown or variable by plan and region. | Confirm card controls, support path, and recovery steps for a block event. | Secondary operational card candidate |

| HSBC Bank | Broader banking footprint | Verify account fee structure, foreign transaction fee, and ATM withdrawal terms. Unknown or variable by country and account tier. | Confirm help-channel access for your account before travel. | Primary for some profiles if verified |

| Netspend | Emergency prepaid layer | Verify reload mechanics, withdrawal costs, and cross-border fee terms. Unknown or variable by program details. | Confirm backup access if your main bank path is unavailable. | Emergency prepaid layer candidate |

Among the options here, Wise has the clearest published numeric checkpoints. The other rows are role hypotheses until you complete account-level verification.

Treat unknown terms as real risk. If a row stays unclear after you try to verify it, keep that product in a secondary role until you can get the details in writing. Uncertainty is not a small inconvenience to ignore. It is a decision input.

A quick scenario test makes the table more useful. For each row, ask how it performs on a normal day with one withdrawal and routine spending, on a high-cash day with multiple withdrawals, and on a disruption day with a blocked transaction or card failure. Meanwhile, if you need a fast model, run those assumptions in the payment fee comparison tool. If you cannot explain likely outcomes from saved terms, do not make that option primary.

It also helps to keep a compact evidence pack:

- Screenshot foreign transaction fee language, ATM withdrawal terms, and ATM reimbursement terms where available

- Save one fee-calculator snapshot for your expected cash usage and withdrawal count where a calculator exists

- Store support contacts and card-control steps outside your main phone session

Use one simple decision rule. If pricing looks attractive but continuity checks are weak, do not rely on that card as your only cash-access path. For Wise specifically, if you expect to exceed 100 USD in monthly withdrawals or go past two withdrawals, include the additional 2% plus 1.50 USD per withdrawal before assigning it primary status. However, if your pattern changes mid-trip, rerun the same check before you increase cash withdrawals.

The table is most useful when your notes are traceable, so attach the account type and verification date to each row. The best-looking option on paper is not automatically the best fit for your real withdrawal pattern. In practice, the row with fewer unknowns is often the safer primary choice.

With that screen in place, the individual recommendations below are easier to use. The question is no longer which card sounds best, but which role each card can safely hold.

Best overall for global ATM access with Charles Schwab#

If you want a bank-led main cash card, Charles Schwab is the strongest candidate in this set, but only after document-level verification. This is not a card-only choice. The Schwab Bank Visa Platinum Debit Card depends on an active Schwab checking account.

- Name: Charles Schwab

- Brief description: A checking account paired with the Schwab Bank Visa Platinum Debit Card for day-to-day cash access

- Key differentiator to verify: Review the Schwab Bank Debit Card Benefits Guide before travel so your decision reflects current language

- Best role in stack: Primary cash card paired with a separately funded backup such as Wise Multi-Currency Card

The appeal is simple: one main withdrawal card, integrated alerts, familiar controls, and a cleaner day-to-day pattern than juggling several tools for the same job. The risk is assuming those benefits still apply exactly as remembered from older documents or secondhand summaries.

If the benefit language is unclear, treat that as real risk and keep a separately funded backup ready. The point of a layered setup is not perfect certainty. It is having a second path when certainty is incomplete.

A practical pairing is Schwab as primary and Wise as backup. Wise positions its card for spending and withdrawals worldwide and publishes a threshold model: up to 100 USD monthly and two or fewer withdrawals, then 2% plus 1.50 USD per withdrawal, with a listed 9 USD card fee.

Before a longer trip, verify the Schwab documents, run one low-stress withdrawal test, and confirm your support path from outside your normal network context. That sequence catches setup friction before it matters.

If Schwab performs cleanly in testing, keep it in the lead role and leave the backup funded but quiet. That is the right standard for any card you want to trust with routine cash access.

Best low-friction backup option for US freelancers with Fidelity#

For many US freelancers, Fidelity is most useful as continuity insurance, not as the center of the whole travel cash setup. Its value is highest as a backup path when your primary card is blocked, delayed, or temporarily unavailable.

- Name: Fidelity

- Brief description: A separate account-and-card path held behind your primary card for emergency access

- Key differentiator to verify: Current withdrawal terms, fee language, and block-resolution steps in official account and card documents

- Best role in stack: Backup card behind a tested primary setup

Keep this backup deliberately simple. Hold backup funds apart from routine trip spending, and store the physical card separately from your primary wallet. A backup in the same pocket as your main card is weaker than it looks.

Use this pre-trip verification sequence:

- Download current account and card terms from your logged-in area and save a dated copy.

- Confirm current international withdrawal behavior, fee language, and block-clearing steps.

- Store support contacts and saved terms outside your main phone session.

- Run one small live withdrawal test, then return the card to backup-only status.

That last step matters. A common failure mode is spending from the backup during normal days and realizing too late that the emergency cushion is gone. Set one usage rule in advance and stick to it.

If activation or support feels slow during testing, fix that sequence before you travel. A backup helps only when you can reach it quickly under stress.

It also helps to decide in advance when backup use ends and normal use resumes. Without that checkpoint, temporary fallback use can turn into routine drift, and the clean separation between primary and backup gets lost.

Once you have a dependable backup in place, it becomes easier to add a more specialized tool for currency control without asking one card to do everything.

Best multi-currency operations choice with Wise Multi-Currency Card#

Wise Multi-Currency Card is strongest as a planned-spend and currency-buffer card, not as a full replacement for a primary checking setup. It is a good fit when your income and expenses cross currencies and you want more control over when conversion happens.

- Name: Wise Multi-Currency Card

- Brief description: A multi-currency card for converting and spending across currencies with in-app controls

- Key differentiator to verify: ATM pricing is threshold-based at 100 USD per month per account and two or fewer withdrawals before overage terms apply

- Best role in stack: Planned-spend card layered behind your primary bank card and backup card

Its biggest advantage is pricing clarity. Wise says personal pricing is usage-based with no subscription plans, uses the mid-market rate for conversion, and presents variable conversion fees starting from 0.57%.

The tradeoff shows up when cash withdrawals become frequent. After the threshold, Wise lists overage costs of 2% plus 1.50 USD per withdrawal, and independent ATM operators can still add their own charges. If a trip relies heavily on cash, that can change the math quickly.

Account type matters too. Personal and business schedules differ. Wise Business shows a one-time setup fee of 31 USD, while the card page shows a one-time card order fee of 9 USD. Recheck the pricing table tied to your active profile before every trip, especially if your use crosses personal and business activity.

A safer operating pattern is staged funding. Load planned spending into Wise, keep deeper reserves in your bank account, and leave freeze controls plus transaction alerts enabled. If you convert too late, you can end up making rushed withdrawals under pressure. Plan high-cash days in advance, convert when practical, and keep enough balance to cover your first days after arrival.

Role discipline matters here. If Wise becomes your daily spend card, emergency cash card, and deep reserve all at once, both continuity and cost control get harder. Keep the job narrow so the card remains easy to reason about.

Pre-trip checklist:

- Confirm whether your account is on personal or business pricing.

- Recheck current ATM threshold and overage terms.

- Check conversion pricing for the currencies you will actually use.

- Run one small purchase and one small withdrawal test.

Used this way, Wise is often one of the clearest tools in the stack. Its strength is transparency, not trying to do every job.

Best app-first secondary option with Revolut#

Revolut works best as a controlled secondary spending card, not as your only answer for cash abroad. Keep core ATM withdrawals on a bank debit card, and use Revolut for day-to-day spending continuity where the app controls actually help.

- Name: Revolut

- Brief description: A plan-based app and card setup for spend control and backup payment continuity abroad

- Key differentiator to verify: If fee summaries conflict, the Cardholder Agreement governs

- Best role in stack: Secondary purchase card, with primary cash withdrawals kept on your bank card

The practical upside is real-time visibility. The app can show exact add-money fees before top-up, which gives you a live cost check instead of relying on stale notes.

The tradeoff is plan sensitivity. Standard plan descriptions include no exchange fee Monday to Friday for 25+ currencies, then 1% on weekends, with a $1,000 per month exchange limit that includes card spending. Standard terms also state out-of-network ATM withdrawals can incur fees up to 2%, while ATM operators or networks may add separate charges on the same withdrawal.

Funding method can change costs quickly as well. Revolut discloses possible add-money fees up to 3% for domestic personal credit-card loads and up to 3% for debit cards issued outside the USA, based on fees charged to it. That makes an in-app fee check worth doing before larger loads.

Paid tiers need separate review. Revolut also states that paid plan terms apply for Metal and Premium, and Premium exchange features may trigger fair-usage fees after $10,000 within a 30 day period. If your notes predate the Standard Plan page update of November 18, 2025, refresh them before travel.

Keep the role intentionally narrow. If this card starts carrying routine spending and emergency cash at the same time, you lose the separation that protects you when fee logic or ATM conditions shift. It is much easier to troubleshoot one clear role than three mixed ones.

When app summaries and formal documents disagree, pause and resolve the conflict before departure. That is usually much easier than fixing funding problems from another country.

Pre-trip checklist:

- Confirm your active plan tier and open matching fee terms.

- Read the Cardholder Agreement and treat it as controlling if wording differs.

- Recheck out-of-network ATM terms, including the up to 2% trigger.

- Run one small add-money test and confirm the displayed fee before larger loads.

- Refresh saved notes if they predate November 18, 2025.

If you treat Revolut as a tightly scoped secondary card, its app strengths are useful. If you expect it to absorb every travel-money job, the plan complexity gets expensive fast.

Best for expats needing broader banking footprint with HSBC Bank#

HSBC Bank can make sense for some expats, but this is a verify-first decision, not an automatic upgrade. Confirm pricing, limits, eligibility, and support outcomes with HSBC directly for your specific account profile.

- Name: HSBC Bank

- Brief description: A bank-led option some expats consider for international banking and card use

- Key differentiator to verify: Exact account-tier terms for foreign transaction fees, ATM withdrawals, and eligibility in the countries where you plan to use the card

- Best role in stack: Primary only after full document verification, otherwise keep your current setup and use Wise as a currency buffer

Use Wise as your clarity baseline in a side-by-side comparison. Wise states usage-based pricing with no subscription plans, publishes feature-level pricing pages, provides a regulator-standardized fee format, and says it uses the mid-market rate. It also lists ATM allowance and overage terms of 100 USD per month and two or fewer withdrawals, then 2% plus 1.50 USD per withdrawal, with conversion fees shown as variable from 0.57% and a listed card cost of 9 USD.

If HSBC documentation is incomplete or hard to compare line by line, do not switch your primary card yet. Unknown terms usually create more operational risk than a simpler structure with transparent pricing and clear fallback behavior.

Use this decision lens before switching:

- Verified fee terms

- Verified withdrawal behavior

- Verified support path

- Verified continuity test with your backup card

If any check is unresolved, keep HSBC in evaluation mode and hold your current setup. A delayed switch is usually less painful than an avoidable mid-trip failure. Move only when the terms are clear enough to defend line by line.

That same logic leads to the next operating rule. Even after you choose the right debit card, purchases should usually live on a separate path.

Debit for cash access and credit for purchases#

For most travelers, the cleanest split is simple: use debit for ATM cash and credit for eligible purchases. That keeps your cash card focused on withdrawals while purchases follow separate fee and agreement terms.

The practical benefit is straightforward. If one card fails, the other can still cover part of the trip while you sort it out. You are not forced to solve every problem at the point of sale.

A workable operating setup looks like this:

- Debit for ATM cash: Use debit for withdrawals, choose local currency, and decline dynamic currency conversion to reduce avoidable conversion costs. Assume withdrawal costs can stack because issuer and ATM operator charges may both apply.

- Credit for eligible purchases: Route day-to-day purchases to credit where appropriate, and confirm foreign transaction fee language in your own account terms.

- Pre-trip controls: Set card-type defaults before departure and recheck current pricing pages on every trip.

Do not treat travel notice status as guaranteed protection. Reported examples show a submitted notice does not always prevent a block event. If one blocked debit card would disrupt your week, carry a second debit card and keep it physically separate.

Even when ATM reimbursement exists, posting timing can vary and may land later, including month-end timing in some cases. Plan liquidity around what you can use now, not what might be reimbursed later.

This split also makes disputes easier to manage. When you separate cash withdrawals and purchases by card role, transaction review is cleaner and recovery actions are easier to prioritize.

The split only works well if you set it up before departure and document what you are relying on.

Build a fail-safe travel money stack before you fly#

Set this up before departure, while you still have stable connectivity and time to fix problems. The goal is not perfect prediction. The goal is faster recovery when a payment path fails.

| Checkpoint | Action | Grounded detail |

|---|---|---|

| Primary and backup cards | Assign one primary cash card and one backup card; run a small local-currency withdrawal test on each before travel | A successful test lowers risk, but it does not guarantee future acceptance, so keep the backup funded anyway. |

| Evidence pack | Save current account terms, fee language, and support instructions from each issuer portal | Organize them by trip month. |

| Cashflow log | Record amount, date, destination, and purpose when moving planned travel funds into your travel-card setup | Reconcile that log to statements monthly. |

| FEIE physical presence | Count 330 full days in any 12 consecutive months | A full day is 24 consecutive hours. |

| FBAR | Check whether a single foreign account or aggregate maximum account value exceeds $10,000 during the year | Use periodic statements to approximate maximum value, round up to whole U.S. dollars, and use a verifiable exchange-rate source if no Treasury rate is available. |

| Incident script | Write first move, second move, and support contact order | A practical sequence is switch to the backup card, capture transaction details, contact support, and log what changed. |

| Day-before-departure check | Confirm both cards are present and physically separated, evidence pack is stored in at least two accessible places, support paths are reachable without search, and planned-spend amount matches current balances | Keep it boring. |

Start with clear role separation. Assign one primary cash card and one backup card, and, if practical, run a small local-currency withdrawal test on each before travel. A successful test lowers risk, but it does not guarantee future acceptance, so keep the backup funded anyway.

Next, build a dated evidence pack. Save current account terms, fee language, and support instructions from each issuer portal. Organize them by trip month so you can see which terms informed each decision. That matters later, especially when pricing or card behavior changes and you are trying to work out whether the change came from your setup or from updated terms.

Then separate cashflow records from card controls. If you route client income through Gruv where supported, move planned travel funds into your travel-card setup with a simple log: amount, date, destination, and purpose. Reconcile that log to statements monthly so operating cash, travel spending, and tax records stay distinct.

If your travel pattern overlaps with freelance or expat tax obligations, keep a compliance checkpoint in the process. For FEIE physical presence, the test is 330 full days in any 12 consecutive months, and a full day is 24 consecutive hours. If the count is missed, the test fails regardless of reason, though minimum-time relief may apply in cases such as war or civil unrest. Use the IRS FEIE guidance as the controlling baseline. If you claim FEIE, you still file a U.S. return reporting income.

For FBAR, filing is required when a single foreign account or aggregate maximum account value exceeds $10,000 during the year. Use periodic statements to approximate maximum value, round up to whole U.S. dollars, and use a verifiable exchange-rate source if no Treasury rate is available. For filing mechanics, verify details against FinCEN FBAR guidance.

After your records are organized, write a short incident script so you do not improvise under pressure. Keep a note with first move, second move, and support contact order. A defined sequence reduces decision lag when a card is blocked mid-trip.

A practical incident sequence can look like this:

- Switch to the backup card for immediate spending continuity.

- Capture transaction details while they are still fresh.

- Contact support through official channels in your saved order.

- Log what changed so your next trip setup improves.

Also keep an offline copy of critical terms and support steps in case your main phone session fails. This is not paperwork for its own sake. It keeps the recovery steps available when app access is limited.

Do a day-before-departure check and keep it boring:

- Confirm both cards are present, active, and physically separated.

- Confirm your evidence pack is stored in at least two accessible places.

- Confirm support paths are reachable without search.

- Confirm planned-spend amount matches current balances.

If a two-card setup still leaves material client-payment risk, add a separate get-paid path with clearer payout visibility where enabled using Gruv for freelancers.

After each trip, run a short review while the details are fresh. Note what fees appeared, which controls worked, and which support steps were slower than expected. Use that review to update your next-trip checklist so the setup improves over time instead of repeating the same weak points.

Failure handling should be boring and repeatable, not complicated, so one card problem does not derail your cashflow for the week.

Final recommendation and next step#

The strongest setup is not one perfect product. It is a layered arrangement with one primary cash card, one funded backup card, and clear usage rules set before departure.

Treat rankings as a starting point, not a verdict. This research set includes mixed source quality, and one roundup explicitly notes advertiser influence on placement. Even recent roundups, including March 2026, are checkpoints rather than proof of your live account terms.

Aim for boring reliability. When each card has one clear job and the supporting terms are saved, you spend less time troubleshooting payment failures and more time getting through the trip.

Use this action sequence now:

- Pick your top two cards and assign fixed roles: primary and backup.

- Confirm foreign transaction fee language, ATM rules, and support paths in official issuer documents for your exact account.

- Run one small test withdrawal before departure and keep dated records.

- Keep travel-card choices separate from business-account choices so your personal spending setup does not blur business finance decisions.

If you already use Gruv, keep client payment records traceable there so card issues do not spill into broader cashflow tracking. Once primary and backup roles are locked, tighten your process with Gruv tools before your next trip. If your cross-border cashflow documentation is still messy, also review Decoding International Wire Transfers.

Then keep the discipline going. Re-verify terms after travel periods, update your evidence pack, and preserve the role split so the setup stays reliable when conditions change.

Frequently Asked Questions

What is the best debit card for international travel if I care most about ATM access and predictable fees?

Pick the option with the clearest published ATM limits, over-limit charges, and terms you can verify before each trip. Wise Multi-Currency Card publishes 100 USD per month per account and 2 or fewer withdrawals, then 2% plus 1.50 USD per withdrawal over that limit. For Charles Schwab, treat exact fee outcomes as unconfirmed here until you verify your current account terms directly. If two options look close, prioritize the one with clearer published terms and feature-level fee checks before use.

Should I use debit or credit for purchases when traveling internationally?

Use debit mainly for cash access, then choose your purchase card based on your own account terms. Confirm fee rules and the controlling card agreement before you rely on either card type. If you keep this split consistent, your statements are easier to review and disputes are easier to isolate.

Are prepaid debit card options better than a traditional checking account debit card for freelancers?

There is no universal winner. Prepaid or multi-currency setups can make spending limits and separation easier, while checking-account debit can be simpler for day-to-day cash access. Also do not assume personal and business pricing are identical, since Wise Business includes a one-time 31 USD setup fee. A practical approach is to assign prepaid or multi-currency tools to planned spend and keep your bank debit card for continuity.

How many cards should I carry on one trip to avoid a single point of failure?

No fixed number fits everyone. A practical setup is one primary card plus one backup rail, both tested before travel. If one card is blocked, you still have a live path for cash access and payments. The key is not quantity alone. The cards should have separate funding and clear role separation.

Which fees matter most when comparing Charles Schwab, Wise Multi-Currency Card, and Revolut?

Focus first on published ATM withdrawal rules, conversion-related charges, and add-money fees. Wise publishes ATM thresholds and over-limit charges, and lists receiving-fee cases like 6.11 USD for USD wire and Swift receipts. Standard plan terms for Revolut say out-of-network ATM withdrawals can be charged up to 2%, some add-money methods up to 3%, and third-party ATM operators may charge even for balance inquiries. If fee pages conflict, the Cardholder Agreement governs. For decisions under time pressure, prioritize charges you are most likely to trigger repeatedly, especially ATM and conversion charges.

What should I do first if my card transaction block happens while I am abroad?

Move spending to your backup rail first so the trip does not stall. Then contact your issuer through its official support path and document the blocked transaction details. Exact resolution steps and timelines can vary by provider. Capture the time, location, and transaction amount while details are fresh, then follow your issuer’s instructions.

How do I handle a cash withdrawal dispute without freezing my operating cashflow?

Protect liquidity first by shifting active spend to your backup card or other available funds while you open the dispute through your provider’s official process. Keep records of withdrawal details and account/app notices, and do not assume funds return immediately. Treat the dispute as a documentation task first and follow required provider steps, since timing and outcomes can vary.

Watch

Best Debit Cards for International Travel

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/ask-cfpb/what-is-a-foreign-transaction-fee-e...trusted

- federalregister.gov/documents/2011/07/20/2011-16861/debit-card-i...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- occ.treas.gov/publications-and-resources/publications/comp...trusted

- wise.com/us/blog/best-debit-card-for-international-tr...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

The Best Digital Nomad Cities for LGBTQ+ Travelers

Pick a city only if the country behind it fits your stay, your work, and your risk tolerance. If you are comparing the **best lgbtq nomad cities**, treat each option as one commitment decision: city plus country, not city alone.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.