Quick Answer

The best choice for a UK sole trader is usually a three-layer setup, not one account. Use a UK bank account as your core transactional hub, add an international revenue gateway if overseas clients pay you, and connect a compliance and automation layer for tax-ready records. For the UK hub, the article compares Starling, Mettle, Monzo Business, Tide, and NatWest.

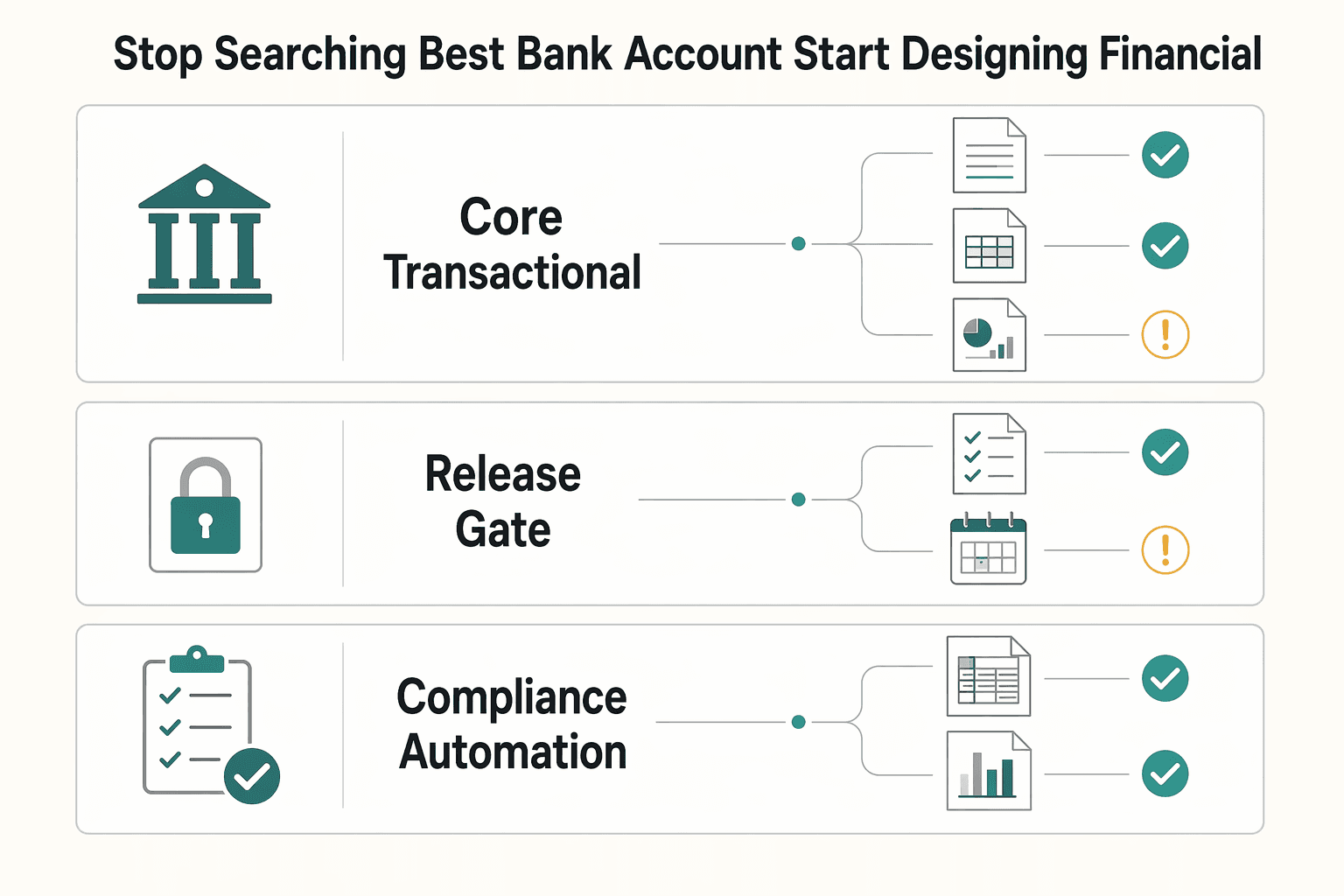

Stop Searching for the "Best" Bank Account. Start Designing Your Financial Stack.#

If you compare accounts on monthly fee alone, you are optimizing the wrong decision. What matters is a connected setup that improves payment reliability, keeps fees visible, and gives you clean records if HMRC checks your tax position.

| Layer | Role | Handles |

|---|---|---|

| Core Transactional Hub | Day-to-day UK money movement | GBP in, GBP out, and routine cash holding |

| International Revenue Gateway | Controls how overseas clients pay you before funds land in your UK setup | Overseas client payments |

| Compliance & Automation Layer | Makes records defensible | Transaction evidence, bookkeeping flow, and tax-ready records |

Core Transactional Hub#

Your Core Transactional Hub is your operating account for UK cashflow. Payment rails matter here. The Faster Payment System runs day and night, 365 days a year, with real-time payments up to £1m. CHAPS is same-day but usually operates 6am to 6pm, Monday to Friday.

International Revenue Gateway#

Your International Revenue Gateway is where cross-border payment friction is either removed or allowed to build up. If clients pay from abroad, this layer can matter more than small differences in domestic account fees. Providers such as Wise offer local account details so clients can pay by local transfer, but you should still verify current fees and settlement terms before deciding.

Compliance & Automation Layer#

Your Compliance & Automation Layer is what makes your records defensible. HMRC requires sole traders to keep business income and expense records for Self Assessment, and to retain them for at least 5 years after the 31 January submission deadline.

This is also where bank feeds matter. Xero can import transactions daily, and QuickBooks Online can auto-download recent bank and card transactions once connected.

| Common risk | Practical fix |

|---|---|

| Weekend client payment does not arrive when expected | Use the Core Transactional Hub and confirm which payment rail is being used |

| Overseas client payment loses value in FX or correspondent fees | Route collection through the International Revenue Gateway |

| Tax return relies on messy exports or incomplete records | Build the Compliance & Automation Layer first |

Before you compare providers, confirm the protection regime. FSCS covers eligible deposits at UK-authorised banks, building societies, and credit unions up to £120,000 per eligible person, per authorised firm, from 1 December 2025, but it does not cover failure of the payments firm itself. Some payment and e-money firms safeguard client funds instead, which is a different protection regime.

With that structure in place, move to Pillar 1. Your UK account should be the hub, not the whole setup. If you want a deeper dive, read The Best Business Bank Accounts for Australian Sole Traders.

Pillar 1: Your UK Bank Account is the "Core Transactional Hub," Not the Entire System#

Your UK account should be your domestic operating hub, not your full finance strategy. Its job is to receive UK client payments, pay suppliers and tax bills, give you clear cashflow visibility, and produce records your bookkeeping software and accountant can use. Aim for a setup that does not need routine manual cleanup every month.

If you are still trying to choose a sole trader account in the UK, start with the bookkeeping handoff, not the headline fee. Check four things before you switch: whether the feed is direct, whether it stays in sync in your workflow, how usable the transaction categorization is after import, and whether your accountant can work from that feed without chasing statements every month.

This is not optional admin. HMRC expects sole traders to keep proof such as bank statements and sales invoices, so your hub needs to stand up as a record system, not just a polished app. A practical failure mode is choosing on UX alone, then finding you still need feed reconnects or manual CSV exports.

Protection is the other hard requirement. From 1 December 2025, FSCS deposit protection is £120,000 per eligible person, per authorised firm for eligible deposits. FSCS also states temporary high balances can be protected up to £1.4 million for six months if requirements are met. Check the authorised firm behind the account, because brand diversification does not help if licences are shared.

| Provider | Accounting and bookkeeping fit | Support and access | Fee model | Cash handling | Operational limitation to notice |

|---|---|---|---|---|---|

| Starling | Integrates with Xero, QuickBooks, and FreeAgent | Verify current support channel before opening | Zero monthly fees stated for the business account | Post Office cash deposits at 0.7% fee (£3 minimum) | Low fixed-cost option, but cash deposits add cost quickly |

| Mettle | FreeAgent included with the account | In-app chat is available, but not 24/7 | FreeAgent inclusion can outweigh small account-fee differences | Verify current cash deposit options and fees before relying on them | Only one owner can access the account |

| Monzo Business | Bank-feed integrations with FreeAgent, Sage, and Xero on Pro or Team | Verify current support model and plan terms | Accounting feeds require paid Pro or Team. Recheck current pricing because Monzo pages conflict | Cash deposits at PayPoint or Post Office | Feed-led bookkeeping may require a paid tier |

| Tide | Integrates with Xero, QuickBooks, Sage, FreeAgent, Kashflow, Crunch, and ClearBooks | Verify live support route and hours | Plan-dependent. Verify current pricing directly | Post Office: £2.50 up to £500, then 0.99% over £500 on Lite or 0.5% on other plans; PayPoint 3%, £10 minimum, £500 maximum per day | Tide is not a bank; FSCS-protected bank accounts are provided via ClearBank Ltd |

| NatWest | Bank feed can move transactions into FreeAgent automatically | 24/7 online, telephone and app banking | 2 years' free banking on everyday transactions when a switch is completed | Cash deposits at the Post Office with a barcoded paying-in slip or debit card and PIN | Strong high-street option; check post-offer tariff before switching |

Use this checklist before opening or switching your core hub:

- Test a demo or live bank feed into your bookkeeping tool and confirm transactions import cleanly.

- Confirm FSCS eligibility and identify the authorised firm, not just the brand name.

- Pressure-test your biggest edge case first: cash deposits, accountant access, or out-of-hours support.

- Keep this account in scope: Pillar 1 is UK operations only; international payments sit in Pillar 2 and tax calculation sits in Pillar 3.

For a related comparison, see The Best Business Bank Accounts for Canadian Sole Proprietors.

Pillar 2: The "International Revenue Gateway" to Capture Global Income#

Once your UK hub is stable, solve the next cost-sensitive problem: how foreign-currency income reaches it. Use your UK account as the final GBP destination, not the first stop for foreign-currency invoices. In many cases, the practical path is simple: the client pays locally, funds arrive in that currency, you convert when you choose, then you move GBP to your UK hub.

That flow helps you control three common cost leaks:

| Cost leak | Definition | Context |

|---|---|---|

| Fee erosion | Value lost during cross-border processing | One of the three common cost leaks |

| FX spread | Margin added on top of the mid-market exchange rate | Applies when you convert currency |

| Intermediary fees | Charges taken by banks in the SWIFT chain before funds reach you | Can arise in the SWIFT chain |

In practice, cross-border transfers can route through intermediary banks. SWIFT charging choices can reduce what the recipient gets, and correspondent deductions can reduce the amount received. SWIFT can take 1 to 6 working days. Wise estimates 15 to 50 USD or equivalent for correspondent deductions.

Use the local route first, not SWIFT by default#

Default to domestic payment rails in your client's country whenever possible. Here, domestic payment details means account details used between financial institutions in the same country via local payment networks.

If a client pays by SWIFT with SHA charging, sender and recipient fees are split after transfer completion, so you may receive less than the invoice amount. That can create a collection gap and extra reconciliation work. If SWIFT is unavoidable, confirm the charging method before you issue the invoice.

Choose the gateway by client mix and accounting fit#

Pick this layer based on payment route and bookkeeping handoff, not brand preference. The real question is whether your clients can pay you through local rails in their currency and market, without forcing SWIFT unless it is genuinely unavoidable.

| Selection point | Wise Business | Revolut Business | What that means for you |

|---|---|---|---|

| Local receiving details by market | States receiving account details in 24 currencies. | For UK-registered customers, non-GBP/EUR currency accounts use SWIFT details, not local details. | If you need wider local receiving coverage, Wise may be worth checking first. If overseas work is mostly GBP/EUR, Revolut may still fit. |

| Holding and conversion control | States you can hold 40+ currencies and convert when needed. | States inbound funds can land in the matching currency account without automatic FX conversion; above plan allowance, states 0.6% FX fee. | If your model is "receive now, convert later," compare plan and rate mechanics before deciding. |

| Transfer to UK hub | States you can send funds to external bank accounts; publishes speed claim, 70% in 20 seconds, 95% under 24 hours, accurate Q3 2025. | Supports transfers out. Help includes example £5 fee for certain international transfers. | Validate the exact route you will use rather than relying on headline product claims. |

| Accounting workflow | Lists direct connections for Xero and QuickBooks. | Xero feed posts completed transactions every few hours. | If you need tighter bookkeeping handoff, compare sync behavior before rollout. |

| Invoicing and setup complexity | Invoicing requires account details in at least one currency. | Invoice currency availability depends on payment method and account setup. | Confirm supported invoice currencies before promising payment options to clients. |

Implement this pillar with four checks#

A common mistake is rolling out payment options before testing how money actually arrives, converts, and posts into your books. Run the setup in a small, controlled way first.

- Open the gateway account

Verify the receiving details shown for your UK business profile, and confirm which currencies use local details and which use SWIFT details.

- Set invoice currency rules

Issue invoices in the client's paying currency where your receiving setup supports it.

- Map settlement rules to GBP

Define what you hold, when you convert, and when you sweep to your UK hub. Before relying on the route, check the provider's current conversion and transfer fee schedule.

- Test accounting handoff before full rollout

Run a small live test from receipt through conversion and transfer to your UK account, then verify the entries in your accounting workflow.

We covered this in detail in The Best Bank Accounts for Freelancers in France. Before you choose your international payment route, run your usual invoice amounts and currencies through this payment fee comparison to spot where conversion and transfer costs quietly reduce margin.

Pillar 3: The "Compliance & Automation Layer" for Total Peace of Mind#

Once money lands cleanly, the next job is turning it into records you can defend. This pillar is your control layer: bank data in, categorized records out, a running liability view, and books that are ready when filings are due. A tax pot can hold money, but it cannot calculate obligations or prove your numbers.

For your UK setup, verify current tax bands, contribution rules, registration thresholds, and filing deadlines before you act. This section does not set UK rates or deadlines.

Automate the parts that actually reduce risk#

Automate the controls that lower your error rate and cut avoidable cleanup. The point is not to automate everything. It is to make sure routine transactions are handled consistently and exceptions get reviewed before they cause filing problems.

| Control | Action | Review |

|---|---|---|

| Transaction categorization | Apply rules so repeat income and recurring costs are treated consistently | Run a monthly check on uncategorized or miscategorized items before closing the period |

| Expense evidence capture | Tie each claim to its source document | If an expense has a transaction but no receipt or invoice, treat it as incomplete |

| Liability estimation | Use categorized records to keep a live estimate of what you may owe | If categorization is wrong, the estimate is wrong |

| Reminders for filing and advance-payment milestones | Build reminders into the process | Manage deadlines before they become problems |

Set those controls up early, then review the exceptions before they turn into filing problems.

Choose software by control quality, not brand comfort#

Choose software for the controls that affect filing quality, not for the logo you already know. In practice, four checks are useful:

- Bank-feed reliability: imports that stay stable enough for timely review.

- Rule-based categorization controls: clear rules you can review, override, and audit.

- Accountant collaboration workflow: shared access and visible change history for handoffs.

- Audit-trail quality: traceability from return line item to transaction to supporting document.

Use cross-border obligations as a stress test#

Cross-border obligations are where weak recordkeeping shows up fastest. If you are a non-resident dealing with Australian GST obligations, the ATO's two pathways are a good example of why automation and evidence discipline matter.

| Checkpoint | Standard GST registration | Simplified GST registration |

|---|---|---|

| Core setup | Includes ABN registration steps | No ABN required |

| Lodgment/payment flow | BAS lodgment and GST payment monthly or quarterly | Register, lodge, and pay GST through ATO non-resident online services |

| Operational constraint | If you are outside Australia, you cannot lodge electronically and may need an Australian registered tax agent | Online access is available through ATO non-resident services |

| Registration artifact | ATO written notice with registration details and effective date | ARN issued after registration (12-digit identifier) |

| Tradeoff | ABN-linked obligations and BAS lodgment/payment obligations | Limited registration entity: cannot claim GST credits and cannot issue tax invoices |

| Access credential | - | AUSid for account access |

Keep this pillar separate from the other two#

Keep the roles clean, or tool decisions start bleeding into the wrong part of the stack:

- Pillar 1: where your UK money lands and your core records begin.

- Pillar 2: how foreign-currency income is received, converted, and moved to your UK hub.

- Pillar 3: categorization, evidence, liability tracking, and filing readiness.

If a feature does not improve those compliance controls, it should not drive your decision in this pillar. You might also find this useful: A Guide to Setting Up a Business Bank Account for a New LLC.

Conclusion: You Are the Architect of Your Financial Freedom#

The right setup is usually not one account. It is a three-layer structure you can run consistently: clean domestic operations, clean international collections, and clean compliance records.

- Your UK core account

Use this for day-to-day UK operations: GBP income, UK bills, card spend, and cashflow visibility. Its main job is keeping business transactions separate enough to support Self Assessment records. Before you hold larger balances, confirm provider type. FSCS deposit protection applies to UK-authorised banks, building societies, and credit unions, and the deposit limit rose to £120,000 on 1 December 2025. FSCS does not protect e-money or payment services firms.

- Your international collections route

Add this when clients pay in non-GBP currencies or need local receiving details. Its job is to reduce collection friction and avoid poor FX handling. For example, Wise Business states it provides receiving account details in 24 currencies and does not inflate the mid-market exchange rate. Keep this layer focused on collections, and re-check protection type before leaving larger balances there.

- Your compliance and automation layer

This is your accounting sync plus your record discipline. Its job is to turn transactions into usable tax records, not rough estimates. You must keep records of business income and expenses for Self Assessment, and you also need records of personal income. If you are in scope for Making Tax Digital for Income Tax, software must maintain digital records and send quarterly updates. Key dates are 6 April 2026 for turnover above £50,000, 6 April 2027 for turnover above £30,000, and 6 April 2028 for turnover above £20,000.

- Quick self-check before you change anything

Your setup likely needs work if any of these are true:

- You still mix personal and business money flows. * You cannot clearly tell overseas clients how to pay you. * Your bookkeeping feed is unreliable or mostly manual. * Your account terms do not match business use, for example, Monzo says personal current accounts are for personal payments only.

Take 30 minutes this week to map your three layers, name the provider for each, and fix the biggest risk first. If you want the next decision step, compare options in The Best Bank Accounts for Freelancers in the UK. You can also review structure tradeoffs in Sole Trader vs. Limited Company: A Guide for UK Freelancers.

For a step-by-step walkthrough, see The Best Bank Accounts for Freelancers in Canada.

If you want to run this stack as one workflow for invoicing, collections, and payout operations with clear records, review Gruv for freelancers.

Frequently Asked Questions

1. Do you legally need a business bank account as a sole trader in the UK?

No. A sole trader may be able to use either a personal or business account, but a dedicated business-only account makes records much easier to manage. HMRC expects clear records and proof documents, and records must be kept for at least 5 years after the 31 January submission deadline.

2. Which UK bank should you use for international payments?

Use your UK bank as your core hub, then add an international revenue gateway when clients pay in other currencies. This lets you receive payments through domestic details or SWIFT details depending on the route. Before keeping larger balances there, check whether the provider is a bank with FSCS deposit protection or a non-bank provider using safeguarding.

3. How should you set money aside for tax as a sole trader?

A tax pot can help, but the stronger control is accounting integration. Your bank feed should sync into software so you can keep the books current, review uncategorized items, and treat expenses without matching proof as incomplete. Verify current HMRC values and timelines before acting on VAT, MTD, and filing obligations.

4. How do Starling, Monzo, and Tide differ for a sole trader?

Starling is positioned as a no-monthly-fee UK core hub with direct Xero, QuickBooks, and FreeAgent connections. Monzo Business offers a free entry plan with paid upgrades, and some accounting feeds sit on Pro or Team plans. Tide suits app-led admin and flexible pricing, but it is not a bank and its accounts are provided via ClearBank Ltd.

5. Is your money safe in a bank account like Starling, or in an app-based payment provider?

Safety depends on provider type, not on whether it is app-based. Check whether you are using a bank account with FSCS deposit protection or a non-bank provider using safeguarding. Re-check current FSCS deposit limits and temporary high-balance rules before holding larger balances.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- makingtaxdigital.campaign.gov.uk/get-ready-for-making-tax-digitaltrusted

- wise.com/help/articles/5zoKjEdRMag0F7IsGBA8sK/how-you...trusted

- wise.com/us/business/receive-moneytrusted

- bankofengland.co.uk/payment-and-settlement/chapsexternal

- fca.org.uk/publication/policy/ps25-12.pdfexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

The Best Bank Accounts for Freelancers in the UK

Confirm with each provider directly, as UK bank product details and eligibility requirements can change. Always verify the current terms on official provider pages before applying.

Sole Trader vs Limited Company UK for Freelancers

If you need a practical starting rule, choose sole trader for a faster start and lighter admin. Choose a limited company when legal separation and company-level compliance are worth the extra work.