Quick Answer

Yes. Start with setup, not brand: confirm ABN entitlement, then check whether GST registration is required and act within 21 days when triggered. From there, narrow to two or three options using hard pass/fail limits on fees, transfer handling, and reconciliation. The strongest choice is usually the one that keeps business activity separate, supports payment tracing with reference IDs, and fits your actual invoice pattern. Before switching, keep the provider’s written terms and your ATO GST notice with its effective date.

You are choosing a bank setup, not just a bank#

For an Australia-based sole trader, the first decision is not the bank brand. It is how money comes in, how GST is handled, and how clearly business activity is tracked separately from personal spending.

- Start with your operating structure

A sole trader is the only owner of the business and is legally responsible for all of it, including debts. Build your banking setup around that responsibility before you compare providers.

- Check ATO registration checkpoints early

The ATO states that you need an ABN before you register for GST. If you become required to register for GST, the ATO says you must do so within 21 days.

- Plan for GST handling in your cashflow process

Australia's GST rate is 10%. If GST applies to you, your setup should make it easy to identify and set aside the GST component as you get paid.

- Keep the scope clear

This guide focuses on practical banking decisions for freelancers, creators, and small teams. It is not legal or tax advice, and it does not assume every sole trader is legally required to open a separate business bank account.

This pairs well with our guide on A Guide to Setting Up a Business Bank Account for a New LLC.

Run a 30-minute shortlist before comparing providers#

Shortlist first. Cut obvious misfits before you spend time comparing features that will not matter once your real payment flow, GST admin, and record-keeping needs are clear.

- Map your operating profile

Write down whether your income is local only or cross-border, your typical monthly invoice volume, and whether you want one operating account or a transaction-plus-savings split. Add your GST checkpoint now: you need an ABN before GST registration, and once registration is required, you must complete it within 21 days. Penalties may apply if you fail to register when required. If GST applies, your setup should make the 10% (1/11th) component easy to identify and set aside.

- Set pass/fail criteria

Define your limits for monthly fees, transfer costs, and the operating features you consider non-negotiable. Treat these as hard requirements, not nice-to-have features. If non-resident GST administration is relevant, factor that burden into your shortlist. Under standard GST registration, BAS lodgment and GST payment are monthly or quarterly, electronic lodgment from outside Australia is not available, and you may need an Australian registered tax agent.

- Add compliance checks before feature comparisons

Confirm your ABN entitlement early. If you are engaged as an employee for an activity, you are not entitled to an ABN for that activity. Check your GST turnover against the registration threshold (A$75,000, or A$150,000 for non-profit organisations) so you know whether GST registration is required.

- Apply a strict filter and keep only finalists

Use one rule consistently to cut options fast, then keep only two or three for deeper review. Before moving on, confirm that your ABN and GST status are clear. If you are GST-registered, keep the ATO written confirmation, including the effective date, with your shortlist notes so your payment setup stays aligned with your GST process.

Legal baseline: required vs recommended in Australia#

The legal baseline for a sole trader is narrower than many people assume. Based on the material here, the confirmed legal points are your structure, your ABN, and your GST timing, not a mandatory bank-account type.

| Item | Status | Grounded detail |

|---|---|---|

| Sole trader setup and ABN | Required first | A sole trader is the only owner of the business and is legally responsible for it, including debts; you need an ABN before GST registration. |

| GST registration | Required when triggered | If you are required to register, you must do it within 21 days; the cited turnover thresholds are A$75,000, or A$150,000 for non-profit organisations. |

| Separate account for business operations | Recommended | The material here does not support saying that sole traders are legally required to open a separate business bank account; separation is described as cleaner for bookkeeping and reconciliation. |

- Required: confirm your sole trader setup and ABN first

A sole trader is the only owner of the business and is legally responsible for it, including debts. Before GST registration, you need an Australian business number (ABN). Keep the sequence clear: structure and ABN first, then GST registration.

- Required when triggered: register GST on time

Not every business needs GST registration. If you are required to register, you must do it within 21 days, and penalties may apply if you do not. The cited turnover thresholds are A$75,000, or A$150,000 for non-profit organisations. ATO guidance also states GST registration details are issued in writing with an effective date. If you collect GST, the GST rate is 10% (1/11th).

- Recommended: use a separate account for business operations

The material here does not support saying that sole traders are legally required to open a separate business bank account. You can still separate business and personal money for cleaner bookkeeping and reconciliation. Treat this as an admin-control decision, not a confirmed legal requirement.

If you want a deeper dive, read A Guide to Tax Residency in Australia for Digital Nomads.

Pick the right account types before you pick a brand#

Choose the account mix before you get attached to a provider. These account types are operating choices, not stated legal requirements in the provided ATO/ABR excerpts.

| Account type | Primary use | Grounded notes |

|---|---|---|

| Business transaction account | Day-to-day business inflows and outflows | Optional operating account. |

| Business savings account or high interest savings account | Reserve account for amounts you do not want mixed into everyday spending | Optional; if GST applies, the GST rate is 10%, often tracked as 1/11th. |

| Multi-currency account | If you handle non-AUD payments | Optional setup choice; the provided excerpts do not set a legal trigger for when this account is required. |

| Merchant account | Based on how you want to accept payments | Optional setup choice; the provided excerpts do not state it is legally required. |

- Business transaction account

Optional operating account for day-to-day business inflows and outflows.

- Business savings account or high interest savings account

Optional reserve account for amounts you do not want mixed into everyday spending. If GST applies, the GST rate is 10%, often tracked as 1/11th of the amount charged. For standard GST registration, keep the ATO written notice of your GST effective date with your records.

- Multi-currency account

Optional setup choice if you handle non-AUD payments; the provided excerpts do not set a legal trigger for when this account is required.

- Merchant account

Optional setup choice based on how you want to accept payments; the provided excerpts do not state it is legally required.

Keep the sequence straight. Get your ABN first, then GST registration when required, including the 21-day timing once triggered. Then finalize your account structure around those obligations. For a country comparison, see The Best Bank Accounts for Freelancers in Canada.

Score accounts with a sole-trader decision matrix#

A weighted matrix is usually more reliable than brand familiarity. It forces you to check eligibility, cost, and failure handling before your first payment lands.

- Build the scorecard first.

Score each option from 1 to 5, then multiply by weights based on how you actually get paid.

| Criterion | What to verify before scoring | Weight higher if... |

|---|---|---|

| Fees | Current fee page, monthly charges, exception fees | margins are tight or volume is high |

| Transfer speed | Provider-stated timing for your payment method, plus your own pilot test | urgent payouts or deadlines are common |

| FX spread | Same-time conversion checks across options | you invoice or pay outside AUD |

| Accounting integrations | Current connection docs and your own MYOB test | you reconcile frequently and want less manual work |

| Branch and cash support | Branch availability, cash handling terms, deposit process | you handle cash or want in-person fallback |

| Card controls | Freeze controls, spend limits, team-card options, product terms | you run recurring card spend |

| Support quality | Support channels, hours, escalation path, written responses | tracing or failed-transfer risk matters |

- Set weights from your workflow, not generic rankings.

If you work cross-border, weight FX, transfer execution, and multi-currency support higher. Use bank and fintech options as shortlist signals, but keep scores provisional until you verify current Australian terms, limits, and receiving options. Exact transfer-speed, FX-spread, integration, and support comparisons are not established here, so keep those rows provisional until you verify them directly.

Wise's public pricing shows why checking each route matters. It states there are no subscriptions or plans, fees vary by currency, and sending or conversion fees start from 0.57%. The same page also shows receiving details in 24 currencies and a 6.11 USD fee for some USD wire or SWIFT receipts. Treat that as a variable-fee example, not Australia-specific pricing.

If most of your work is local and in AUD, raise the weight on branch or cash support and support quality, and lower FX weighting.

- Require evidence for every score.

Put eligibility checks ahead of any "best" conclusion. A sole trader is legally responsible for business debts, and ABR states that not everyone is entitled to an ABN.

Keep an evidence pack with your matrix. Include ABN confirmation, proof you started or took steps to start the enterprise, current fee pages, sole trader eligibility wording, transfer-limit terms, and support-channel details. Save ABN confirmation when it is issued. ABR also notes that if an application needs additional checking, it aims to review it within 20 business days, and refused applications are confirmed by letter within 14 days.

- Pressure-test support before opening.

Send the same two questions to each provider and score the quality of the response, not the tone.

Ask these two questions:

- "If an inbound payment is missing, what reference IDs and documents do you need to run a trace?"

- "If a transfer fails, what is the escalation path, and which support channel handles it?"

Stronger answers name the required evidence up front, for example payer name, amount, date, remittance advice, invoice ID, and bank reference. Generic replies are a useful warning sign for future admin drag.

You might also find this useful: Sole Trader vs. Company: A Guide for Australian Freelancers.

Before you lock a provider, run your real transfer mix through the payment fee comparison tool and save the result with your shortlist notes.

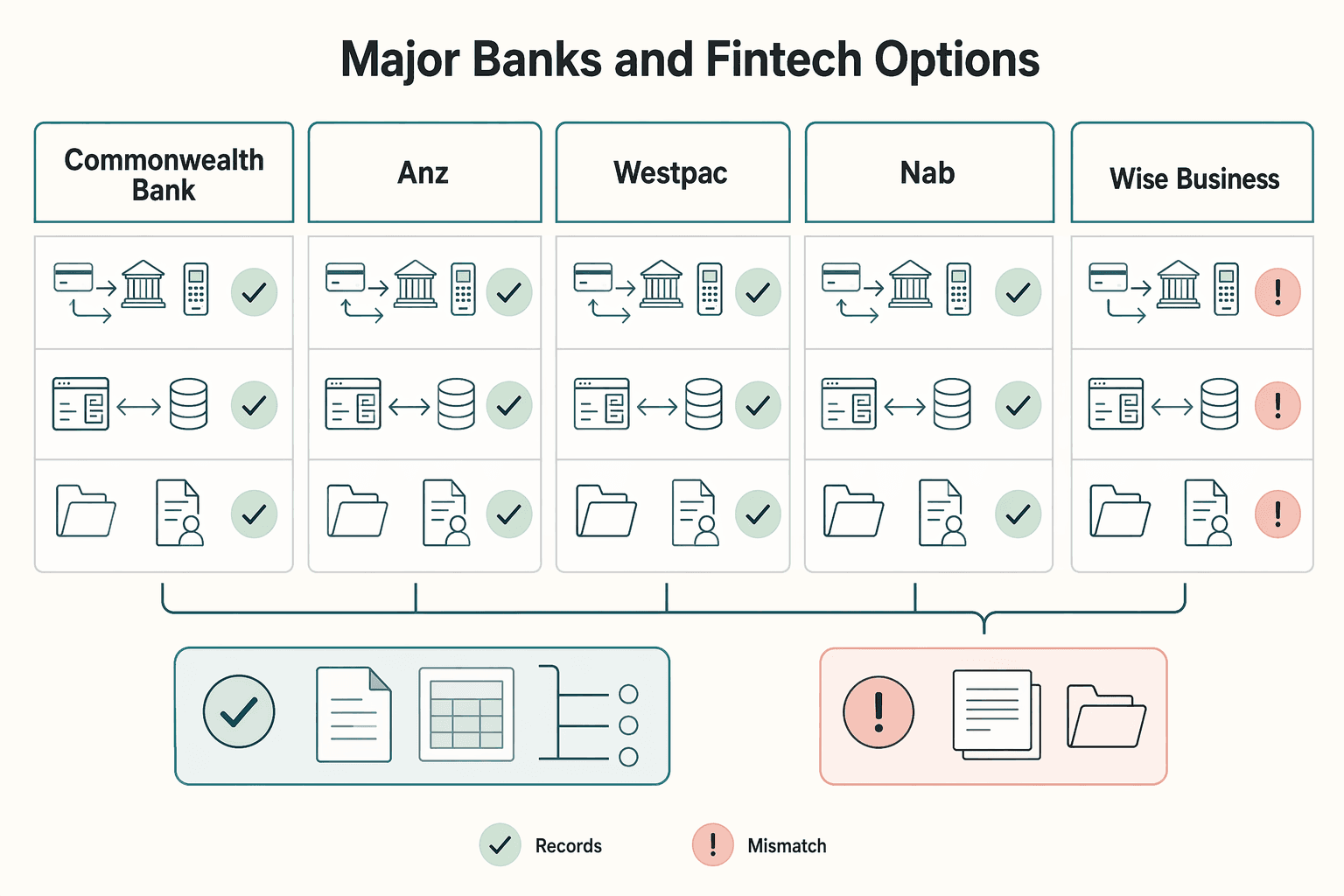

Market map: major banks and fintech options#

Use this map to rule out weak fits quickly, not to crown a winner. The first question is simple: can this option prove it fits your payment routes, your MYOB process, and your sole-trader documentation right now?

For sole traders, eligibility comes before features. ABR says a sole trader is one person and the only owner of the business, and not everyone is entitled to an ABN. A sole trader can employ other workers, but cannot employ themselves. Keep your 11-digit ABN confirmation and evidence that you commenced, or took steps to commence, your enterprise. ABR can review entitlement, and incomplete application information can delay ABN issuing.

| Option | Best-fit workflow | Likely weak point | International capability | MYOB compatibility | Verification items | Who should skip this |

|---|---|---|---|---|---|---|

| Commonwealth Bank (CommBank) | Option for same-scorecard comparison | Brand familiarity can hide unchecked terms and support gaps | Treat as unverified until you confirm current options for your account type | Treat as unverified until you test your exact feed or import path | Sole-trader application wording, ABN and ID requirements, current fees and terms, missing-payment trace process, failed-transfer escalation path | Skip if you need confirmed cross-border handling first |

| ANZ | Option for same-scorecard comparison | Assumed parity with other providers can cause setup churn | Verify current send and receive options and support evidence requirements | Confirm exact setup method, then run a sample reconciliation test | ABN and ID requirements, current terms, transfer conditions shown for your account, support channel details | Skip if your shortlist depends on pre-verified international routes |

| Westpac | Option for same-scorecard comparison | Weak fit if monthly and exception cost patterns are not validated for your transaction mix | Confirm current route availability and trace requirements before scoring | Keep unverified until you run a real MYOB test | Sole-trader onboarding requirements, fee and terms pages, trace evidence checklist, escalation contacts | Skip if you want a no-verification setup path |

| NAB | Option for same-scorecard comparison | Support quality is often assumed instead of tested in writing | Confirm current sending and receiving conditions that apply to your tier | Require a tested MYOB workflow, not a generic claim | ABN and ID requirements, fee and terms pages, written trace and failed-transfer handling steps | Skip if cross-border execution is your primary requirement |

| Wise Business | Option for same-scorecard comparison | Rework risk if used as a full replacement without edge-case checks | Verify current routes, conversion conditions, and receiving setup on live terms | Do not assume compatibility, test reconciliation with real sample data | Entity eligibility in your setup, required documents, fees and limits shown, trace and escalation process | Skip for now if local AUD operations are your only immediate priority |

| Airwallex Global Account | Option for same-scorecard comparison | Wrong-fit risk if capability is assumed before account-level checks | Verify current supported routes, conditions, and limits for your setup | Run a MYOB test with sample transactions before relying on it | Sole-trader eligibility requirements, onboarding documents, current fees and limits, delayed or failed transfer support steps | Skip if you want one provider without separate domestic and cross-border testing |

| OFX | Option for same-scorecard comparison | Weak fit if you need one provider without additional verification steps | Verify live transfer routes and support trace requirements before use | Assume manual work until your own MYOB check proves otherwise | Eligibility, current fee disclosures, transfer rules, support contacts, trace and amendment requirements | Skip for now if your immediate priority is a provider you have already verified for local invoicing and bill-pay |

How to use this map#

Think in three buckets: core operations, international routes, and edge-case transfers. That makes elimination easier and avoids false "best" conclusions.

Keep support quality as a hard gate. Ask each provider what they require to trace a missing inbound payment and how failed transfers escalate. If the answer is vague, mark support as unverified and score conservatively.

Final decision rule#

Do not finalize from this table alone. Before opening, save the current terms, fee pages, sole-trader eligibility wording, and written support responses so your decision is backed by evidence.

Related reading: The Best Business Bank Accounts for Canadian Sole Proprietors.

When a traditional bank is the better core account#

If a traditional bank will be your core account, validate the setup against your own records instead of assuming every major bank will behave the same way. Treat provider feature comparisons as unverified until you test them in your workflow.

- Use major banks as candidates, not defaults.

Start with a shortlist of major-bank options, then test fit against your actual payment routes and admin flow. Keep your sole-trader setup clean first: you need an ABN before registering for GST, and ABN entitlement does not apply to activity performed as an employee.

- Price the full cost pattern, not just the headline fee.

Check the total of account fees, transaction charges, ATM or cash handling charges, and exception-handling charges. Save current terms and fee pages before opening so you can compare what you were shown with what you are charged.

- Require reconciliation proof in your MYOB flow.

Do not rely on generic compatibility claims. Run sample invoices through your real process and confirm that references and amounts reconcile cleanly in practice, so bookkeeping and BAS preparation stay under control.

- Keep cross-border expectations realistic.

A domestic core account may be a weak fit for frequent international receipts, so test that path before relying on one account for everything. For GST compliance, not every business must register, but if registration is required you must complete it within 21 days, and penalties may apply if you do not. Keep the written GST registration confirmation, including the effective date, with your records.

For a country comparison, read The Best Bank Accounts for Freelancers in France.

When a bank + fintech split is the better setup#

A bank plus fintech split can make more sense when foreign-currency invoices are common. Keep one domestic account for Australia, and add a multi-currency account for cross-border receipts.

- Split by payment lane, not by provider brand.

Use your domestic account for Australian bills, tax reserves, and local client payment details. Use a multi-currency account for foreign-currency intake so local operations and cross-border receipts stay separate and easier to reconcile.

- Confirm ABN readiness before changing invoice rails.

Your ABN is an 11-digit identifier, and entitlement applies to enterprise activity, not work done as an employee. Incomplete applications can delay issuance. Extra checks can take up to 20 business days, and outcome letters are sent within 14 days after processing. Set your account-routing rules once your business details are settled.

- Receive first, then convert using your own rule.

Route inbound foreign currency to the multi-currency account, then convert on a planned threshold or timing rule that you apply consistently. That keeps FX decisions deliberate instead of reactive.

- Use published Wise pricing as a checkpoint, then verify with a live test.

Wise states that it uses the mid-market rate, uses pay-as-you-go pricing with no subscription plans, and lists sending or conversion fees from 0.57%, depending on currency. The same page also lists receiving details for 24 currencies and a 6.11 USD fee for receiving USD wire or SWIFT payments. Treat those figures as a checkpoint, not a guarantee for every Australian use case.

- Benchmark contractor payouts before committing.

For offshore contractor payments, compare routes on total conversion cost and actual arrival time, then keep records from a small test transfer. Use that evidence to choose the payout path, and keep the domestic bank as your anchor for Australian payments and local trust signals.

For a step-by-step walkthrough, see The Best Business Bank Accounts for UK Sole Traders.

Build a two-account cashflow system you can enforce#

For most sole traders, two accounts are enough if each one has a fixed job. The structure is simple, but the discipline is applying the same rule to every payment.

- Give each account one job

A common setup is a business transaction account for receipts and day-to-day spending, plus a separate business savings account for GST, tax, and buffer reserves. This matters more as turnover approaches A$75,000, where GST registration is required once you meet the threshold. If registration is required, the ATO says you must register within 21 days, and you need an ABN first. If GST applies, the rate is 10% (1/11th), which is the core amount your reserve logic should protect.

- Sweep reserves before treating cash as available

If you choose to sweep reserves when client money arrives, set a rule you can justify and maintain. The exact percentage and timing are operational choices, not a fixed rule in this guidance. If you are GST-registered, include the GST component at minimum, then add tax and buffer needs. Test the flow with live payments so timing, labels, and reconciliation visibility are clear before volumes increase.

- Use a review cadence you can sustain

A weekly reconciliation cycle is a control choice, not an ATO mandate, but it helps keep invoice matching and internal transfers clean. Then run a monthly statement review for fees, charges, and FX-related deductions so avoidable leakage does not compound.

- Define buffer and override rules in writing

Set a minimum operating buffer, either a fixed amount or an expense-based rule, and document when reserves can be touched. As a sole trader, you are legally responsible for the business, including debts, so override authority should be explicit even if someone else helps with admin. Keep your ABN details and GST registration confirmation, including the effective date when provided, with the same cashflow policy. That keeps reserve rules aligned with your current status.

Failure modes that create delays, disputes, and admin drag#

Most problems start with registration timing or poor record handover. They usually show up when GST timing is unclear, ABN paperwork lags, or the GST effective-date record is not carried into operations.

- GST required, but registration steps are not ready

As you approach the A$75,000 turnover threshold, treat GST readiness as operational, not optional. If registration becomes required, you need to register within 21 days, and you need an ABN before you can register for GST.

- ABN timing risk is ignored, especially for non-residents

If you are applying as a non-resident, plan for extra identity-proof requirements that may increase ABN processing time. Do this early to reduce timing risk before GST registration.

- No clear GST cutover record

Keep the ATO's written GST registration notice, including the effective date, with your operating records. This gives a concrete checkpoint for pre- and post-registration treatment.

- Post-registration GST process is not documented up front

After registration, make sure GST treatment reflects 10% (1/11th) where applicable. In the standard GST system, plan for BAS lodgment and GST payment monthly or quarterly.

Verification pack and cutover plan before switching#

Do not switch accounts until your verification pack, GST checkpoint, and fallback plan are ready. The main risk is changing client payment details before terms, tax timing, and records line up.

- Build a live verification pack first

Confirm the provider's current fee schedule, product terms, sole trader eligibility wording, transfer limits, and multi-currency rules from live pages or PDFs, and save dated copies. Treat written terms as the decision record, not sales chat or comparison summaries.

- Set a clear tax and bookkeeping cutover point

Before updating client-facing payment instructions, lock your internal bookkeeping updates. For non-resident standard GST registration, keep one dated cutover note tied to the ATO written GST registration notice and effective date. If GST registration becomes required, register within 21 days, and remember that you need an ABN before you can register. If GST applies, keep treatment aligned to 10% (1/11th) rather than estimates.

- Use a staged cutover, then migrate fully

Consider starting with one pilot client payment, checking settlement and reconciliation, and then moving the rest. For that pilot, keep a complete record including invoice ID, expected amount, received amount, and payment reference so issues are caught before they scale.

- Keep a rollback path during transition

Keep the old account monitored during overlap so late or misdirected payments are still visible, and prepare client messages for both the initial switch and stray payments to old details. The goal is continuity while clients and payables teams update saved instructions.

- Do not set a switch date ahead of registration checkpoints

If you are a non-resident, allow extra time because additional proof of identity can increase processing time. Under standard GST registration, you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. If your registration notice or effective date is still pending, delay full migration.

Choose the setup that matches your payment reality#

For most readers, there is no single verified best account for a sole trader in Australia. Choose the setup that keeps payments traceable, reserves controlled, and records easy to defend. Start by shortlisting 2 to 3 options, then verify live terms before you open anything.

| Setup | Best when | Key checkpoints |

|---|---|---|

| Simple domestic payer setup | Most clients pay in Australia, in AUD, and you need low admin overhead | Check current product terms, sole trader eligibility, and operating conditions before deciding. |

| Reserve-first setup for GST and tax pressure | Turnover is rising and you want tighter GST and tax readiness | A$75,000 is a key turnover figure; if registration is required, you must register within 21 days, and you need an ABN before registering. |

| Documentation-heavy setup for multi-activity or non-resident cases | Documentation strength matters more than convenience, including multi-activity sole trader operations | The ATO says you register for GST once, even if you operate more than one business; for standard non-resident GST registration, you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. |

1. Simple domestic payer setup#

Use this when most clients pay in Australia, in AUD, and you need low admin overhead. One business transaction account can work early on if you keep business and personal spending separate and can match each payment to an invoice or client reference.

Check current product terms, sole trader eligibility, and operating conditions before deciding. A common failure mode is choosing on headline price, then losing time later because payment records are hard to reconcile.

2. Reserve-first setup for GST and tax pressure#

Use this when turnover is rising and you want tighter GST and tax readiness. Keep one account for day-to-day business cashflow and a second account for reserves so tax money stays visible and harder to spend.

In the ATO GST registration context, A$75,000 is a key turnover figure. If registration is required, the ATO says you must register within 21 days, and you need an ABN before registering. Keep your ABN record, dated banking cutover note, and the ATO written GST notice, including the effective date, together. This reduces cleanup risk when applying 10% GST, or 1/11th of the charged amount where applicable.

3. Documentation-heavy setup for multi-activity or non-resident cases#

Use this when documentation strength matters more than convenience, including multi-activity sole trader operations. If you are non-resident, use the GST workflow checkpoints below. The ATO says you register for GST once, even if you operate more than one business, so your setup needs a clear trail across all income streams.

For standard non-resident GST registration, the ATO says you cannot lodge electronically from outside Australia, you may need an Australian registered tax agent, and extra identity proof may increase processing time. Avoid switching payment rails too early. Keep existing instructions in place until your written GST notice is issued and test payments reconcile cleanly.

If two options are close, choose the one that makes traceable payments, controlled reserves, and clean weekly records easiest to maintain. For related reading, see The Best Bank Accounts for Freelancers in Germany. If you invoice internationally and want clearer payment status tracking, review Virtual Accounts to check fit and market coverage.

Frequently Asked Questions

Do sole traders in Australia need a separate business bank account?

Not as a blanket legal rule in the material here. ABR describes a sole trader as the only owner of the business and personally responsible for business debts, but that does not by itself create a separate-account mandate. In practice, separation is mainly about cleaner records and easier GST and tax tracking.

What is the difference between a business transaction account and a high interest savings account?

The material here does not support a universal feature-by-feature distinction. Treat account choice as a provider-specific operating decision, and verify current terms, fees, limits, and sole trader eligibility before opening or switching. Use written product terms as the decision record.

When does a multi-currency account become necessary for freelancer workflows?

There is no supported Australia-wide threshold that makes it mandatory. A practical trigger is when cross-border payments start creating avoidable friction in cashflow, settlement timing, or payment tracing. If that pressure is increasing, review whether your current setup still supports reliable reconciliation.

Which should I prioritize first: low fees, MYOB integration, branch access, or FX support?

There is no single fixed order supported for every sole trader. Prioritize the factor most tied to your real payment flow and reconciliation risk, then confirm the tradeoffs in current provider terms. Avoid choosing on headline price alone if it weakens day-to-day payment reliability.

Can I start with a personal account and migrate later without creating tax-reporting issues?

The material here does not confirm that this is automatically issue-free. If you migrate later, keep a dated cutover note and clear records so business transactions remain traceable for reporting.

What is the minimum setup to stay ready for GST and income tax obligations?

The material here does not set a required number or type of bank accounts. Keep records that clearly separate business income and support GST turnover checks. If GST registration becomes required, the ATO says you must register within 21 days, and you need an ABN before registering. Where GST applies, keep treatment aligned to 10%, or 1/11th of the charged amount, and retain the ATO written notice with your registration details and effective date.

Does having more than one business change GST registration?

Not in the way many people assume. The ATO says you register for GST once even if you operate more than one business. The operational priority is accurate turnover and payment tracking across all activities.

What if I am a non-resident selling into Australia?

For standard GST registration, non-resident businesses may need to lodge BAS and pay GST monthly or quarterly. The ATO also states that you cannot lodge electronically from outside Australia and may need an Australian registered tax agent. Because of that, complete the registration steps and keep the written effective-date notice as part of your GST records.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- abr.gov.au/business-super-funds-charities/applying-abntrusted

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- jewell.edu/sites/default/files/pdf/25-26-jewell-catalog...trusted

- wise.com/us/pricingtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

The Best Bank Accounts for Freelancers in Canada

Pick the account setup that protects how you actually get paid, not the one with the lowest headline fee. Predictable deposits, clear limits, and clean records matter more than a cheap monthly number if they help you avoid delays, surprise charges, and month-end cleanup.

Sole Trader vs. Company: A Guide for Australian Freelancers

**In a sole trader vs company decision in Australia, you are choosing a system, not just a label. Your structure affects contracts, tax, personal asset protection, and investment readiness.**