Quick Answer

Start with two finalists and pick the one that holds up in both your typical month and your busiest month. TD Basic Business Plan ($5.00, 5 transactions) and BMO Business Start ($6.00, 7 transactions) show why low sticker fees can still miss your pattern. Confirm transfer limits, export quality for CRA review, and one backup receiving rail before you rely on it for bills. If you invoice outside Canada, keep domestic banking for local operations and use Wise Business only after checking live Canada terms.

Start with how your money actually moves#

Pick the account setup that protects how you actually get paid, not the one with the lowest headline fee. Predictable deposits, clear limits, and clean records matter more than a cheap monthly number if they help you avoid delays, surprise charges, and month-end cleanup.

That is the main tradeoff in this category. A low sticker price can still cost more if the plan caps out quickly, transfer rules are vague, or reconciliation turns into manual repair work. A slightly higher base fee can be the cheaper choice in practice if it keeps payments moving and reduces the time you spend sorting transactions later.

Use four checks before you shortlist anything: fees, transaction limits, interest rates, and perks. In that order. Product pages naturally pull attention toward extras, but extras do not help if the payment path itself is weak. Start with cost behavior, then confirm limits, then look at how idle cash sits between invoices and payouts, and only after that decide whether the extras matter.

The guide works best if you start in the lane that matches how you work right now:

- Solo side hustler: You are unincorporated, invoice part-time, and want cleaner separation between client income and personal spending without adding much admin. The first question is whether a dedicated personal account can handle your current volume without creating confusion later.

- Full-time independent: You bill regularly, pay recurring tools or contractors, and need month-end review to stay easy. The first question is cost behavior, because monthly fees plus transaction structure can change your real total faster than most people expect.

- Small team with cross-border clients: You receive foreign currency and care about settlement timing and FX leakage as much as domestic convenience. The first question is whether you can receive, hold, and convert funds in a way you can verify before the first payment lands.

Each lane tends to break in a different place. Side hustlers usually lose clarity first. Full-time independents usually lose cost control first. Cross-border operators usually lose margin first. If you know your likely failure mode, the rest of the decision gets much easier.

A simple domestic setup can work early. Weak choices usually start showing seams when volume rises, payment timing gets uneven, or foreign currency becomes part of the month. That is why transfer rails, pricing clarity, and terms you can confirm on live pages matter more than a polished ranking table.

Read this actively. Keep one note open while you go and track three things: your current monthly transaction count, your most common incoming payment methods, and the one payment failure that would hurt most in a tight week. By the time you reach the checklist, you should know what to test first, what to ignore, and which accounts deserve a real look.

One final operator point before you start: the right choice is rarely the account that looks best in isolation. It is the setup that keeps your actual payment path stable when volume rises, a client pays late, or you need fast reconciliation before tax and contractor deadlines. That logic drives the shortlist below.

If two options still look equally good after the first pass, choose the one that gives you cleaner verification and fewer assumptions. When money is moving under pressure, clarity usually beats theoretical upside.

How this list picks winners and who it is for#

This list ranks accounts by fit at your actual usage level, not by the lowest advertised fee. The job here is simple: help you build a credible shortlist quickly, then test that shortlist against how money actually moves through a month.

It is built for people who need options that hold up in live use, not just in roundup tables. That includes part-time freelancers trying to keep overhead light, full-time independents who need tighter controls, and small teams whose payment mix has outgrown basic chequing.

The scoring uses four lenses:

- Real-volume cost score: Compare the fields that change outcomes, especially monthly fees, free transaction allowances, and relevant rate or perk terms. The same method can still produce different winners. A plan listed at $6 with 10 free outgoing Interac transfers can beat a lower-fee plan when your activity sits near that lower plan's cap.

- Account-type fit score: Account type comes before fine-tuning. If you are unincorporated or a sole proprietor, a business account is not always required on day one.

- Category-consistency score: Compare like with like instead of forcing one winner across personal side-hustle and business-banking use cases.

- Bias and failure-risk score: Vendor pages and third-party rankings can help you discover options, but final decisions should rely on live pricing and limits on provider pages.

The labels matter less than the order of operations. First, map your last 30 days of inflows, outgoing payments, and transfer frequency. Then run two or three finalists against that pattern. If usage is low and stable, a simpler setup may be enough for now. If count is rising, clearer allowances usually matter more than saving a small amount on the headline price.

You can do this in one focused session. Pull the last month of activity, highlight where you came close to limits, and test each finalist against that same pattern. Using one consistent activity pattern across all finalists keeps the comparison clean and stops the goalposts from moving as you research.

Treat these lenses as a filter, not a finish line. A plan can look strong in a table and still fail if the limits do not match your invoice and payout pattern. Fit here is concrete. Month-end should get easier under uneven volume, not harder.

One documentation habit makes the whole process more reliable: do not compare marketing claims against memory. Compare live terms against recent activity, save what you checked, and note the date. That takes a few minutes now and saves repeat work later if terms shift or your volume changes.

If two plans still look close after that pass, pick the one with fewer unknowns. Fewer assumptions usually means fewer surprises once client money starts moving. With that filter in place, the quick table below works as a fast cut, not a final verdict.

Quick comparison table you can scan in two minutes#

Use this table to narrow your shortlist, not to make the final decision. In the material behind this draft, Wise is the only option with concrete pricing details available here. Treat the other rows as candidates that still need direct checks on current provider pages.

If you are scanning quickly, start with the Watchout column. That is usually where fit breaks after opening, even when the headline positioning looks strong.

| Account | Best for | Verified data point in this section | Watchout before shortlist | Use when |

|---|---|---|---|---|

| RBC Digital Choice Business Account | Digital-first business-account candidate | No verified fee or limit number in the material behind this draft | Confirm current fees, transaction limits, and export format directly on provider pages | You want it in your final shortlist after verification |

| TD Basic Business Plan | Low-volume business-account benchmark | No verified fee or limit number in the material behind this draft | Verify included transaction rules before assuming fit | You want a baseline business option to compare |

| BMO Business Start | Low-volume benchmark with a different allowance mix | No verified fee or limit number in the material behind this draft | Check overage pricing and how it maps to your monthly activity | You want a second baseline option in your shortlist |

| National Bank of Canada Hybrid Package | Traditional-bank comparison candidate | No verified fee or limit number in the material behind this draft | Validate fit against your actual incoming and outgoing payment mix | You want a traditional-bank option in side-by-side review |

| Wealthsimple Cash | Side-hustle personal-account candidate | No verified fee or limit number in the material behind this draft | Confirm account boundaries for business activity before committing | You want to keep it in scope while validating account-type fit |

| Simplii Financial High Interest Savings Account | Savings-led side-hustle candidate | No verified fee or limit number in the material behind this draft | Verify whether it can support day-to-day operating needs | You want to test it after checking practical operating limits |

| EQ Bank Personal Account | Personal-account candidate for early-stage usage | No verified fee or limit number in the material behind this draft | Verify account constraints before scaling payment volume | You want another personal-account comparison option |

| Alterna Small Business eChequing Account | Additional business-account candidate | No verified fee or limit number in the material behind this draft | Confirm transfer behavior and support expectations directly | You want broader business-account coverage in the shortlist |

| Scotiabank Select Account for Business | Branch-access business-account candidate | No verified fee or limit number in the material behind this draft | Check total cost against expected monthly activity | You want branch-capable support in the shortlist |

| TD Every Day Business Plans | Higher-activity branch-capable candidate | No verified fee or limit number in the material behind this draft | Verify plan rules and cost structure before assuming fit | You want a second branch-capable option to compare |

| Wise Business | Cross-border invoicing and FX-pricing checks | Wise Business pricing shows 31 USD all-in, send fees from 0.57%, discounts above 25,000 USD monthly sends, and use of the mid-market exchange rate | Pricing pages shown are for U.S. residents, and method-level fees can vary, so verify live terms with the calculator before deciding | You receive foreign-currency payments and want explicit FX-pricing checks |

If two candidates are close on price, keep the one with clearer transfer-limit wording and cleaner records for bookkeeping. In practice, clarity removes operational friction more reliably than a tiny difference in headline fees.

A practical way to use the table is to choose one baseline business option, one branch-capable option if in-person support matters, and one cross-border option if foreign invoices are part of your month. Then run the same payment path through each candidate on paper.

As you score each row, write one line for why it stays or drops. That small note prevents memory drift later and makes the final decision easier to explain to a partner, assistant, or future you. It also forces you to separate choices based on evidence from choices based on convenience.

Close the exercise with one blunt question: where do the unknowns still sit? The option with fewer unknowns is usually the one that is easier to operate when deadlines tighten.

You can also tag each row as verify now, verify later, or drop. That simple pass keeps the shortlist from drifting into endless research. Once you have that first cut, the next sections show what each option is actually good at and where it tends to fail.

RBC Digital Choice Business Account for digital-first freelancers#

Keep RBC Digital Choice Business Account in the running, but do not assume it wins by default. The real test is whether the package structure matches how you receive and move money each month.

RBC positions Digital Choice as a distinct business chequing package and lists it alongside Flex Choice. That matters because you are comparing package structures, not interchangeable labels. If you pull details from the wrong package, your math goes bad quickly and you end up comparing a plan that does not really exist.

Before you commit, work through these checks:

- Package identity check: Confirm that the details you collect apply to Digital Choice itself, not another RBC package.

- Pre-decision fee check: Use RBC's Estimate Business Account Fees tool with your expected monthly activity.

- Payment-rail check: If billing depends on bank transfer or Interac e-Transfer, confirm current transfer details on RBC account pages before opening.

- Support model check: If in-person support matters, compare that experience across finalists before naming your default account.

A concrete use case here is a consultant with recurring domestic invoices and a separate CRA reserve. Run the estimate with expected activity, save your assumptions and the date checked, then confirm how statements and exports will work for month-end review. Those last two checks are easy to skip because they do not affect the first invoice, but they matter once you are reconciling a full month under time pressure.

When you run the estimate, test at least two activity levels: a normal month and a busier month. You are not trying to predict perfectly. You are trying to see where cost behavior changes and whether that shift still fits your margins. That is usually where a digital-first plan proves itself or falls short.

Save the estimate output with your notes, then compare the estimate with the first real statement after opening. That short feedback loop makes re-evaluation much faster if charges or activity differ from your assumptions. It also gives you a clean basis for switching later if the fit is weaker than it looked on paper.

Add one review checkpoint about 60 days after go-live. Confirm that posted charges, transfer behavior, and export quality still match what you checked during selection. Early correction is much easier than discovering a mismatch at tax season.

If two finalists sit in the same price range, choose the one that asks you to assume less. In day-to-day use, lower ambiguity is usually safer than a small theoretical upside.

If this account still looks good after the paper test, set a simple go-live timeline: opening date, first invoice date, and first statement review date. Clear timing prevents setup drift. And if Digital Choice feels like more structure than you need, the low-volume plans in the next section give you a better control group.

TD Basic Business Plan, BMO Business Start, and National Bank Hybrid for low-volume operators#

For low-volume freelancers, monthly fee and included transactions have to be judged together. Splitting those two is how cheap-looking plans turn expensive as soon as activity brushes the cap.

NerdWallet's comparison lens is useful here because it segments by business size, transaction volume, and business type. That framing holds up when billing is uneven and your choice needs to survive both slow weeks and busy ones.

| Plan | Monthly fee | Included transactions | Practical read |

|---|---|---|---|

| TD Basic Business Plan | $5.00 | 5 | Lowest listed fee in this set, with the tightest included activity |

| BMO Business Start | $6.00 | 7 | Slightly higher base fee, with the highest included count in this set |

| National Bank of Canada Hybrid Package | $8.00 | 6 | Highest listed fee here, with included count between TD and BMO |

The decision rule is simple. If your activity stays consistently low, the lowest monthly-fee option can work. If your count often approaches the included limit, paying a little more for headroom can produce the lower real cost.

Before you decide, run one fast checkpoint: estimate transactions in a typical month and a high month, then score each plan against both. Save the assumptions, the date checked, and the included-transaction details so you can revisit the choice quickly if volume changes. That record matters because low-volume plans often look stable until one busy month exposes how little room they actually give you.

A good sequence keeps this grounded. First, choose the plan that fits your normal month without strain. Second, test whether a late-week spike would push you past included activity often enough to matter. Third, decide whether a slightly higher base fee buys enough room to reduce that risk in a meaningful way.

If your transactions vary a lot based on client payment timing, this two-scenario test matters even more. A plan that only works in your calm month is not really a low-risk choice. You want something that still behaves acceptably in the month when two or three payments bunch together and a few extra outgoing transfers land at the same time.

Watch how close your normal month sits to the cap. Plans that look cheap right at the edge of their limit usually become unstable when one client pays on a different day or you make two extra transfers you did not plan for. That is not bad luck. It is just the wrong plan operating exactly as designed.

If volume is changing quickly, schedule a short review after one billing cycle. You do not need to rebuild the whole comparison. Update your transaction count, re-check the limits, and confirm the fit against actual behavior. If even these low-volume business plans still feel heavier than you need right now, a disciplined personal-account bridge can be the cleaner move for the current stage.

Wealthsimple, Simplii, and EQ for side hustlers not ready for business banking#

If business banking still feels premature, a personal-account setup can be a reasonable bridge while you remain unincorporated. The goal is not perfection. It is clean separation now and a lower-friction move later if the work becomes more regular.

Start by answering two questions in writing: do you need a business account now, and what documents will you need when you switch? Writing them down sounds minor, but it prevents the most common side-hustle drift, where a temporary setup quietly becomes a messy long-term one.

Use these checks for the personal-account candidates:

- Wealthsimple Cash: Decide whether you need a business account now before committing.

- Simplii Financial High Interest Savings Account: Map the documents you will need if you transition to business banking later.

- EQ Bank Personal Account: Apply the same two checks before committing so your switch path stays clear.

One Canadian ranking labels Wealthsimple Save for Business as best for incorporated businesses, which reinforces the broader point: structure fit matters when you plan the transition. A temporary bridge only works if you know what would make it stop working.

A common failure mode is assuming income will scale quickly, then spending funds that should have stayed reserved. Side hustles also absorb startup costs easily because money lands in the same mental bucket as personal cash. Conservative reserve behavior reduces pressure when cashflow gets uneven.

Keep the bridge disciplined from day one. Route all client inflows through one path, move reserve money on a repeat schedule, and avoid mixing side-hustle spending with personal purchases in the same stream. You are not trying to build a full business-banking setup with a personal account. You are trying to preserve records that stay usable as volume grows.

It helps to build a simple transition packet while activity is still manageable. Keep account notes, recurring payment methods, and your reserve routine in one place so the later move to business banking is procedural instead of stressful. The more organized this bridge is, the cleaner the eventual handoff becomes.

Set one switch trigger before you begin. If reconciliation starts taking too long or payment volume rises consistently, move before a hard month forces the decision. That one rule prevents the usual trap, where the setup is obviously out of fit but still gets one more month because switching feels annoying.

When the switch point arrives, move deliberately with your document list and account history already organized. That preparation makes the handoff much smoother. A personal-account bridge can work for early domestic activity, but once foreign currency becomes meaningful, the next set of tradeoffs usually matters more than simplicity.

Wise Business for cross-border freelancers who care about FX leakage#

If cross-border invoices are part of your month, treat Wise Business as a conversion-control layer. Collect in the client's currency first, then convert on purpose instead of accepting whatever conversion happens at payout.

Wise presents pricing as usage-based with no subscription plans, states pricing is shown upfront, and says conversion uses the mid-market rate. Wise also states receiving account details in 24 currencies. Keep the product boundary clear: this is a cross-border money tool, not automatically a full replacement for every domestic banking need.

That distinction matters because a good cross-border tool solves one problem very well while leaving others untouched. If you blur those roles, you can end up overestimating what the account will handle on the domestic side and underchecking the parts that drive cost on the foreign-currency side.

Before you send international invoices, run this pre-send check:

- Price checkpoint: Pull a live quote for the exact currency pair and amount, then save the fee lines with the invoice note. Wise lists send fees from 0.57%, but final cost depends on transfer details.

- Document checkpoint: Open the regulator-standardized fee format and compare it with the quote you are about to accept.

- Method checkpoint: Build margin math around method-level receiving costs. Published examples include a fixed 6.11 USD charge for receiving USD wire and Swift payments.

- VAT checkpoint (EU cross-border): If your business is EU-based and buying or selling across borders, verify counterpart VAT registration in VIES and keep documentation complete, because weak documentation can create VAT reimbursement problems.

Those figures come from Wise pricing pages, so check live Canada terms before making pricing-sensitive decisions. Also confirm account features directly before you rely on them in live operations. That matters even more here because the pricing pages referenced above are scoped to U.S. residents.

A common operating pattern is a designer billing U.S. and EU clients who collects in client currency, converts in planned batches, and ties each conversion back to invoice IDs before month-end. The strength of that setup is not only cost visibility. It also turns conversion into a deliberate operating decision instead of a hidden side effect of getting paid.

Two habits do most of the work here. First, tie conversion timing to invoice timing instead of reacting to every incoming payment. Second, store quote details with each invoice record so later review stays clean. Those habits are small, but they usually separate a manageable cross-border setup from one that becomes hard to audit a few months later.

Keep client communications separate from your conversion decisions. Quote your pricing to clients in the currency you plan to collect, then decide when to convert based on your own obligations and timing. That separation helps prevent margin drift when payments land on different days.

Before each conversion batch, compare the planned amount with the obligations due in the same period. Matching conversion size to near-term needs can reduce unnecessary churn and make reconciliation cleaner. It also gives you a simple way to check whether you are converting because you need to, not just because money arrived.

If cross-border volume matters, add one more control: keep a basic conversion log with quote time, applied fee, and related invoice ID. This is not admin for the sake of admin. It preserves evidence for reconciliation, especially in busy months with several smaller conversions that are hard to untangle later.

If send volume changes meaningfully, re-check pricing before quoting new work. Most avoidable FX leakage comes from stale assumptions, not from one obviously bad transfer. And if international flows are only part of your operation, you still need to decide whether domestic branch support is worth paying for.

Scotiabank and TD Every Day plans for branch-dependent operations#

Pay for branch-heavy plans only when in-person banking is a recurring operating need, not just because it feels safer. The real test is simple: do you repeatedly need branch support for deposits, paper-and-electronic exceptions, or cash handling?

If the answer is yes, keep these on your shortlist:

- Scotiabank Select Account for Business: Included in one side-hustle comparison, and another comparison lists a monthly range of $20 to $120.

- TD Every Day Business Plans: Included in the same side-hustle comparison and described as branch-friendly for higher activity, with cash handling and nationwide branches. Another comparison lists a monthly range of $19 to $125.

The tradeoff is access versus ongoing cost. In that same framing, some traditional unlimited plans are shown around $65 to $125 monthly, while some digital-first options are presented at $0. If branch usage is only occasional, confirm what you are actually paying for before treating access as a default need.

A practical example is a small studio that still deposits occasional cheques and wants in-person escalation when a payment issue turns urgent. In that case, branch access may justify the higher cost because it can shorten time to resolution when something important fails. If you rarely use a branch, the same monthly fee can just become dead weight.

Before you choose, list the branch tasks completed in the last quarter and the tasks you expect in the next one. If most activity is already digital, a branch-heavy plan may be more capacity than you need. If branch exceptions happen often and delays carry real cost, paying for access can be reasonable.

Also confirm the basics that shape day-to-day use: location, hours that fit your schedule, and how often your team would realistically use that access. Convenience you never use is still a cost, and branch-based support only has value if it is available when you actually need it.

Document one escalation path while you are deciding. If a payment issue becomes urgent, decide in advance who contacts the branch, what account details are needed, and how your team tracks resolution. That turns branch access into real operating value instead of a vague comfort signal.

A clear branch preference still does not settle the structural question by itself. You still need to decide whether to stay on personal rails for now or move to a business setup that matches your current volume and complexity.

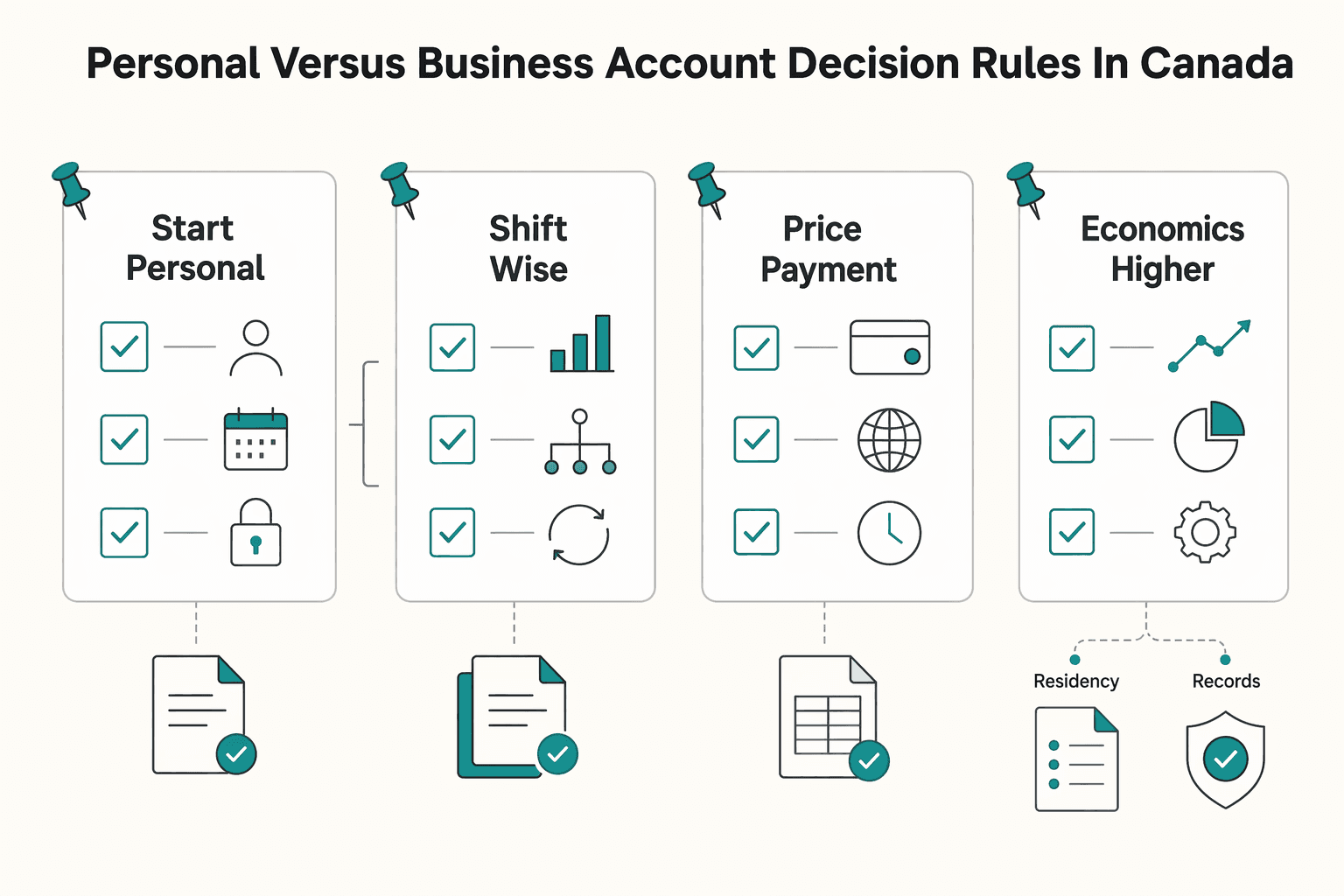

Personal versus business account decision rules in Canada#

Use personal rails while demand is still being tested, then move to business rails when volume and complexity become repeatable. The switch should follow operating reality, not labels.

The pricing signals below come from Wise pages scoped to U.S. residents. Treat them as directional and confirm live Canada terms before the first client payment that depends on them.

- Start personal for low-commitment testing: Wise personal pricing is shown as pay-for-usage with no subscriptions or plans, which can keep fixed overhead lower while demand is uneven.

- Shift to Wise Business for recurring cross-border operations: Wise Business highlights a one-time setup price of 31 USD, and Wise pricing pages also list receiving details in 24 currencies.

- Price by payment rail, not account label: Fees shown from 0.57% can vary by currency and method. Some faster receiving methods include fixed fees, while a free receiving path is also stated.

- Re-check economics at higher volume: Wise says discounts start above 25,000 USD monthly sends, so re-price when transfer volume grows.

Before final selection, confirm method-level pricing with the calculator and review the regulator-standardized fee-format view for the account type you plan to use.

This is mostly a timing decision. If current volume is light, a simpler setup can keep fixed costs low while you learn your payment pattern. Once cross-border invoicing or reconciliation strain becomes routine, a business setup often removes avoidable friction.

Use a short switch-trigger list: recurring cross-border invoices, repeated month-end reconciliation strain, or frequent manual workarounds in your payment flow. If two or more are true, the temporary setup has probably outlived its role.

To reduce switch friction, migrate in stages. Keep existing invoice rails active while you test new rails with lower-risk transactions, then move default invoicing only after your reconciliation process is stable. A staged move lowers the chance of payment confusion during the transition and gives you a clean way to compare expected versus actual behavior.

After switching, add a recurring review. A 90-day check of volume, method mix, and fee behavior is usually enough to confirm whether the new structure is delivering what you expected. You are looking for fewer workarounds, cleaner records, and cost behavior that still makes sense under real activity.

The goal is not to look more formal. It is to remove avoidable failure points as the operation matures. Once account type is clear, the next step is avoiding the specific mistakes that create fee creep and payment delays.

Red flags that create payment delays and fee creep#

Most payment delays and fee creep are seeded during account selection. They usually look small at the start and then become expensive because no one checked them directly before opening.

- Headline-fee trap on business accounts

Choose on effective monthly cost, not the sticker price. Compare live fee schedules against your real activity, including transaction terms and excess-item pricing, so total cost is visible before you switch. A plan with a lower monthly fee is not automatically cheaper if your normal month keeps touching the cap.

- Borrowed-verdict trap from community threads or vendor pages

Community threads and vendor pages are useful for discovery, but they are not proof of fit for your payment pattern. Check date relevance, topic match, and disclosure quality. If your research starts surfacing unrelated material, tighten the filter before you use that input for a banking decision.

- Single-rail risk during payment-heavy weeks

If most inflows depend on one rail, one delay can disrupt bill timing. Keep a backup receiving rail active and tested. For fintech-branded options, confirm who provides the banking service and what protection is stated. Some disclosures explicitly say the fintech is not a bank, services are provided by a named partner bank, and pass-through FDIC coverage is up to $250,000 per qualified account with coverage limited to partner-bank failure.

The practical rule is simple: if one delayed client payment would force you to defer tax, contractor pay, or rent, the setup is too tight.

Use a short pre-open script: check the fee schedule, check the limits, check the backup rail, then write down what you confirmed. Repeatable beats perfect here. You do not need a long process. You need one you will actually use.

If you cannot explain your backup rail in one sentence, treat that as a warning sign and tighten the setup before go-live. A backup that only works in theory does not really reduce risk.

Run the same script again after your first billing cycle. That quick second pass catches mismatches between expected and actual behavior while changes are still easy to make. It is much easier to fix the setup after one month than after a quarter of messy transactions.

Most of these failures are preventable. A one-page pre-decision check now is usually easier than months of cleanup later. The 30-day checklist below turns those warnings into concrete actions.

30-day setup checklist to lock in a reliable get-paid system#

Use this checklist to verify payment rails, fee behavior, and fallback paths before client cashflow depends on them. You are not trying to make this complex. You are trying to build a setup that works in normal weeks and still works when something breaks.

- Week 1: choose account roles and map payment paths

Pick one primary operating account for inflows and bills, plus one reserve account for buffer cash. Build a one-page map showing how each client pays, where funds land first, and the default path to reserves. If Wise Business is in scope, note the one-time setup fee of 31 USD and that the pricing pages shown here are for U.S. residents, then confirm Canada-specific terms before go-live. Before week 1 closes, confirm who owns each task if more than one person touches billing, payments, or reconciliation.

- Week 2: set invoice rules and fallback instructions

Set one default payment method on invoices, then one backup method if payment does not post as expected. Keep backup instructions clear enough to send in one client email. Price both rails before invoices go out: some methods are free, while others include fixed per-payment fees. Published examples include 6.11 USD for USD wire or Swift, 2.16 GBP for GBP Swift, and 2.39 EUR for EUR Swift. At the end of week 2, test your fallback message once so you are not drafting it under pressure.

- Week 3: validate records and month-end checks

Run a dry month-end close with your records. Confirm each paid invoice matches a bank line item, and keep categories stable month to month. Save the current fee view in regulator-standardized format for your selected account variant so you can compare later if charges change. Treat this as internal control, not a substitute for accounting or tax review. If you spot category drift, fix naming and mapping immediately so the next month does not compound the cleanup.

- Week 4: stress-test domestic and cross-border flows

Send one low-value domestic payment and one low-value cross-border payment using the exact rails you plan to use. Record total fee, conversion details, and settlement visibility. If Wise is part of your stack, include a volume-pricing check: pricing is shown from 0.57%, discounts auto-apply above 25,000 USD equivalent across transfers, and the discount window resets on the first of the month. Week 4 is also the right time to confirm your backup rail can be used quickly without new setup steps.

By day 30, you should have one primary rail, one tested backup rail, and a monthly review routine you can repeat without guesswork.

To make that routine stick, set one recurring review date each month. On that date, compare planned versus actual activity, re-check pricing for your most-used rails, and update fallback instructions if anything changed. This turns the setup into a maintained operating habit instead of a one-time project you forget until something fails.

Keep review notes short and consistent. A brief monthly log with date, volume, and pricing checks gives you early warning when the setup no longer matches reality. If you work with a partner or assistant, assign one owner for each checkpoint. Shared responsibility without explicit ownership usually creates gaps.

Before locking anything in, run your real payment mix through the payment fee comparison tool to catch overage and transfer-cost surprises. Once that pass is complete, most remaining questions are edge cases, which is exactly where the FAQ helps.

Conclusion#

Choose for operating fit first, then test the choice against your real payment pattern. The best account for a freelancer in Canada is not the one with the prettiest feature list. It is the setup that supports your transaction volume, payment rails, and cross-border needs with clear rules and fewer unknowns.

Start with two finalists, apply the decision rules above, and compare how each one handles your actual flow of incoming and outgoing money. Then re-check the fit as volume changes, and confirm live terms before any pricing-sensitive decision. That keeps the decision tied to evidence instead of a static snapshot from a roundup.

If you take one action today, make it this: map recent inflows and outgoing payments, then run that map through your top two candidates. A short, evidence-based comparison now can prevent fee creep and payment friction later.

Make the decision easy to audit by documenting why you picked it, what assumptions you used, and when you will review again. That single note helps future you adjust quickly as volume or client mix changes. Put the review date on your calendar so this stays a living decision instead of a one-time pick that drifts out of fit.

If one finalist needs repeated caveats just to feel safe, drop it. The right setup should still make sense in a busy month, with clear pricing checks, clear limits, and a backup rail you can explain in plain language. That is what keeps the decision useful when conditions change.

If you want a more controlled way to invoice clients and manage compliant payouts with clear status tracking, explore Gruv for freelancers.

Frequently Asked Questions

Do freelancers in Canada need a business bank account, or can they use a personal account?

Not always. MoneySense indicates some sole proprietors and side hustlers can use a regular chequing or savings account instead of a business account. A business account can become more useful as transaction volume and operational complexity grow. If your current setup still keeps records clean and payment handling simple, you may not need to switch immediately. Once that stops being true, move early rather than waiting for month-end confusion.

What matters more for freelancers, low monthly fees or transaction allowances?

Treat this as one decision. MoneySense's comparison lens is fees, transaction limits, interest rates, and perks, so a low monthly fee alone is not enough. If activity sits near the cap, higher allowances can be the cheaper real-world choice. A useful check is to compare your typical month and busiest month side by side. That quick test shows whether your low-fee option still holds up when activity spikes.

What is the best account setup if I invoice in CAD and foreign currencies?

A split setup can be practical: one domestic account for local operations plus a cross-border provider for foreign-currency flows. Wise describes support for holding and managing over 40 currencies, local account details in 10 currencies, and sending to 160+ countries. It also states it is an MSB provider, not a bank, and flags no cash deposits. Keep domestic and cross-border roles clear so each tool handles what it does best. That can reduce conversion surprises and keep reconciliation cleaner.

How can I compare accounts to reduce payment delays and cashflow risk?

Use fit-first comparison, not single-winner thinking. NerdWallet frames fit by business size, transaction volume, and business type, then states the best account is the one that helps operations run efficiently. After shortlisting, pressure-test each option with your own payment pattern. At minimum, test one standard month and one high month before deciding. If a plan only works in ideal conditions, it is not a reliable choice.

What is the difference between side-hustle banking and full-time freelance banking?

Side-hustle setups often prioritize simplicity and lower fixed cost, including personal account options in some cases. Full-time freelance banking often needs tighter alignment to transaction volume and payment complexity. The practical shift is from lowest base cost to best operating fit. In practice, the shift happens when admin effort and payment complexity start to outrun the savings from a simpler setup.

Which account features make tax filing and recordkeeping easier for **CRA**?

This grounding does not provide a CRA-mandated feature list or legal threshold for account selection. A practical approach is to choose an account structure that keeps business activity easy to track and review. Keep comparisons anchored to documented factors such as fees, transaction limits, interest rates, and perks. The safer move is consistency: stable categories and clear, repeatable transaction tracking month to month.

What key details are often unknown before choosing a "best" account?

Three details are easy to overlook: transaction limits, regional pricing scope, and provider type. MoneySense explicitly calls out transaction limits in comparisons, and Wise says to verify current regional terms before relying on listed pricing. Wise also identifies itself as an MSB provider, not a bank, which affects how you design your setup. Check these details before you open, not after the first invoice cycle. Early verification prevents most avoidable rework.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: