Quick Answer

Avoiding double taxation starts with the right order: lock your filing-year residency facts, confirm treaty coverage for each income type, and then choose FTC or treaty relief based on documented eligibility. Keep one evidence pack that ties every claimed amount to contracts, invoices, payment records, and foreign tax proof, and make sure your return, FBAR, and Form 8938 disclosures stay consistent.

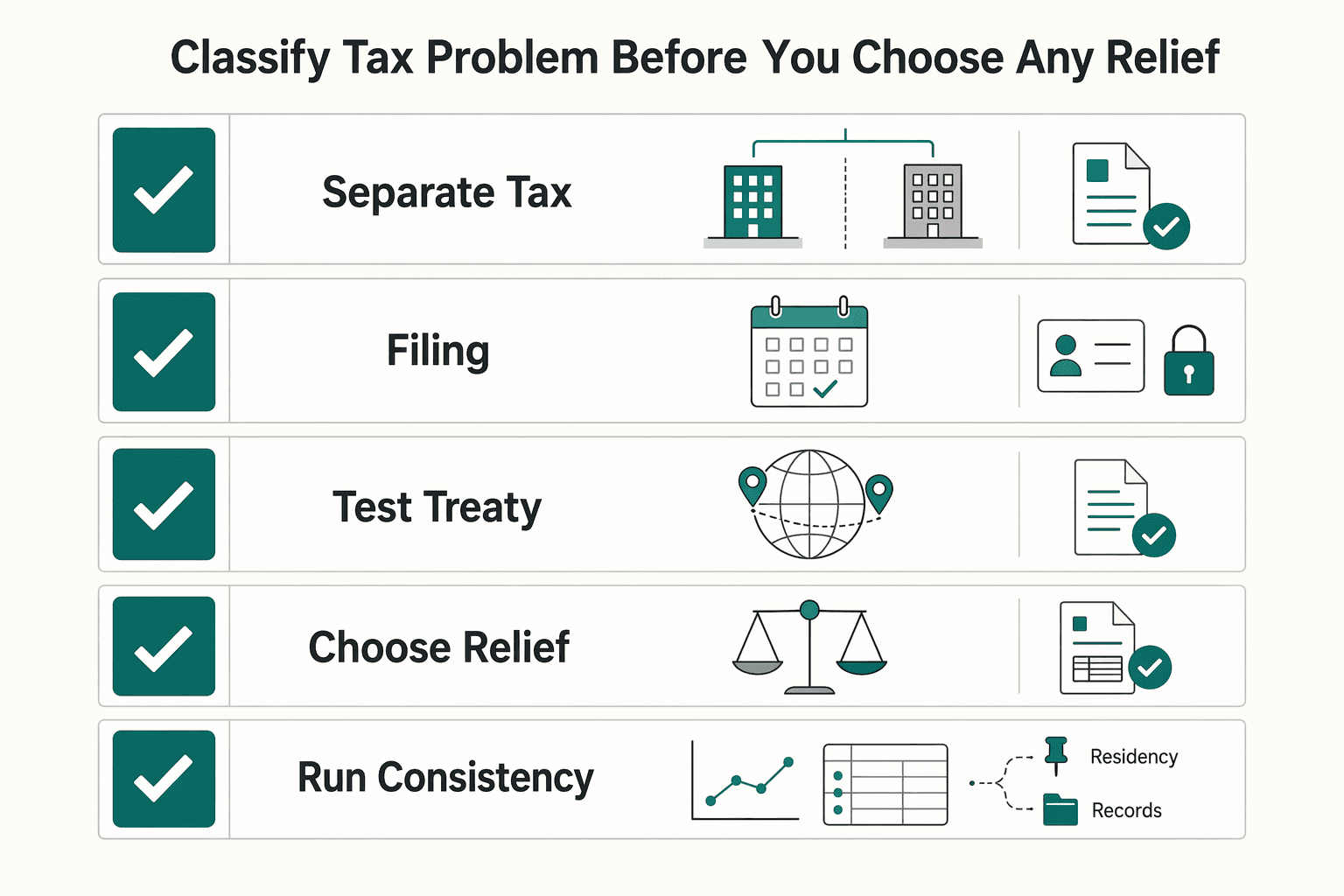

Classify your tax problem before you choose any relief#

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.

Your goal is to avoid double taxation without taking positions you cannot defend later. Use a practical sequence: lock in tax residency facts for the filing year, apply the right treaty rules for each income type, and keep records that support each claim from start to finish.

Keep one core reality in view: U.S. citizens and U.S. treaty residents are generally taxed on worldwide income. Relief depends on correct claim mechanics, not guesswork. If two countries can both treat you as resident, you may need treaty tie-breaker analysis.

Run the same sequence each filing cycle.

- Separate the tax type. Confirm you are solving personal income overlap, not corporate tax design.

- Set residency first. Map where you lived and worked, then lock your filing-year position.

- Test treaty coverage. Check that a treaty exists and that it covers the income category.

- Choose the relief path. Compare available relief options only after eligibility is clear.

- Build proof before filing. Tie contracts, invoices, payment records, and tax-paid evidence to each claim.

- Run consistency checks. Make sure returns and disclosures tell one coherent story.

This guide gives you decision checkpoints, recovery steps, and a reusable checklist. It is not about clever tax engineering. It is about filing a position that is clear, defensible, and hard to misread.

What should you prepare before you start?#

Build one evidence pack before you analyze relief options. You want a clear trail from income to taxes paid to required disclosures.

| Prep item | Keep | Verification |

|---|---|---|

| Core income records | Client contracts, invoices, payment confirmations, and prior returns tied to your cross-border work | For each material income line, you can trace contract -> invoice -> payment |

| Residency evidence by country | A folder for each jurisdiction where you lived or worked | Your residency timeline matches the addresses and dates used in filings |

| Account-disclosure inputs | A dedicated set for FBAR and Form 8938 data | One account list can feed both filings without conflicts in owner, balance, or account details |

| Foreign tax proof | Proof of foreign taxes paid or accrued, plus year-specific summaries linked to the related income stream | Each foreign tax amount ties to a date, jurisdiction, and income category |

| Self-employment records | Net self-employment earnings clean for Schedule SE and aligned with any FTC or treaty position you plan to claim | Schedule SE inputs, foreign-tax records, and disclosures reconcile to the same books |

- Collect core income records. Gather client contracts, invoices, payment confirmations, and prior returns tied to your cross-border work. Keep support for every income, deduction, and credit item.

Verification point: For each material income line, you can trace contract -> invoice -> payment.

- Map residency evidence by country. Keep a folder for each jurisdiction where you lived or worked, with records that support your filing position.

Verification point: Your residency timeline matches the addresses and dates used in filings.

- Separate account-disclosure inputs. Maintain a dedicated set for FBAR and Form 8938 data. Form 8938 does not replace FBAR, and FBAR is filed with FinCEN, not the IRS.

Verification point: One account list can feed both filings without conflicts in owner, balance, or account details.

- Document foreign taxes before credit decisions. Gather proof of foreign taxes paid or accrued, plus year-specific summaries linked to the related income stream.

Verification point: Each foreign tax amount ties to a date, jurisdiction, and income category.

- Isolate U.S. expat self-employment records. Keep net self-employment earnings clean for Schedule SE and align them with any FTC or treaty position you plan to claim.

Verification point: Schedule SE inputs, foreign-tax records, and disclosures reconcile to the same books.

Final prep check: keep records long enough to substantiate your return positions. Track FBAR timing separately (annual due date is April 15), and keep required FBAR records for five years from the FBAR due date.

Are you solving corporate double taxation or freelancer treaty double taxation?#

Start by routing the issue. Corporate dividend double tax and freelancer cross-border personal income are different tracks with different first steps.

A C corporation can face tax at the entity level and again when profits are distributed as dividends. If you operate as a sole proprietor, business income is generally reported on Schedule C, so the practical focus is your residency position, treaty coverage, and relief mechanics like the foreign tax credit (FTC) or treaty relief.

Use this decision rule: if your income is mainly fees for your own labor, start with residency and treaty analysis before you redesign the entity.

| Decision check | Corporate track | Freelancer treaty track |

|---|---|---|

| Main issue | Entity profit and shareholder dividends | Personal service income on an individual return |

| First records to review | Entity structure, distributions, compensation | Residency timeline, income records, foreign tax paid |

| First technical question | How corporation income and distributions are taxed | Whether treaty terms or FTC apply to the same income |

Then run three quick checks:

- Identify the income layer. Separate entity profit from personal service income.

Verification point: You can state in one sentence where any overlap occurs.

- Route to the right filing lane. Keep personal-income analysis separate from corporate planning.

Verification point: Your working file is either personal-return focused or corporate focused, not mixed.

- Test relief mechanics after routing. For freelancer income, compare FTC and treaty relief on the same income stream.

Verification point: Any credit or treaty position matches foreign tax actually paid or accrued (including any treaty-reduced amount).

If this classification takes more than a page, simplify before moving on. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Step 1 decide your tax residency position before choosing any relief#

Set your residency position first for each filing year, then choose relief. If you start with credits or treaty claims before residency is clear, your filings can conflict.

Treat residency as a year-specific fact pattern, not a label you carry forward. A dual-resident taxpayer is treated as resident by both countries under domestic law, and treaty residence is then determined by the applicable treaty tie-breaker rules.

- Map your year by jurisdiction. Build a timeline of where you lived and worked, then write a short residency memo in plain language.

Verification checkpoint: Your memo, address history, and supporting records match.

- Flag dual residency early. If two countries can each treat you as resident, start the DTA tie-breaker analysis immediately.

Verification checkpoint: You can state whether you are single-resident or dual-resident before running any relief calculation.

- Prepare treaty disclosure when required. If you take a dual-resident treaty-based return position, disclose it on Form 8833 and keep that disclosure aligned with your residency memo.

Verification checkpoint: Your return language and Form 8833 use the same country pair and rationale.

- Keep disclosure channels aligned. Form 8938 and FBAR are separate obligations, and FBAR is filed with FinCEN rather than with the IRS.

Verification checkpoint: Address, account ownership, and country details are consistent across filings.

Red flag: your residency memo points to one treaty residence, but your account or address disclosures point somewhere else. Fix that before Step 2.

Step 2 check treaty coverage and apply the tie-breaker rule correctly#

Check treaty coverage for your country pair and income type first. If no treaty article applies to that income item, domestic tax treatment applies.

Confirm the treaty is in force for the filing year, then map each major income stream to the relevant article. Review the Independent Personal Services article where it applies, but do not assume every treaty uses the same structure or scope.

In dual-resident cases, apply the tie-breaker tests in treaty order and document why each step points where it does. Common tests include permanent home, center of vital interests, habitual abode, and nationality.

- Confirm treaty availability and article-level coverage.

Verification point: You can identify the exact treaty article for each income stream, or clearly document that domestic rules apply.

- Classify income before claiming relief.

Verification point: Every major income line has a defined treatment path.

- Apply tie-breaker tests sequentially.

Verification point: Your treaty-residence conclusion is traceable step by step in treaty order.

- Reconcile treaty position with disclosures.

Verification point: Your treaty disclosures and information returns tell the same residency story.

A frequent failure mode is treating tie-breakers as automatic day-count rules; they are not. Another is claiming treaty relief while residency evidence conflicts across filings.

Red flag: inconsistent residency evidence. Pause and fix the tie-breaker documentation before Step 3. You might also find this useful: Understanding the 'Independent Personal Services' Article in Tax Treaties.

Step 3 should you claim FTC or treaty relief?#

Choose between FTC and treaty relief only after you verify what foreign tax was paid or accrued and how treaty terms affect that same income stream.

| Check | What to confirm | Verification |

|---|---|---|

| Foreign tax evidence | Match tax amount, jurisdiction, income item, and payment or accrual records | Every claimed amount has a document trail |

| Treaty impact | Whether treaty terms reduce source-country tax or change taxing rights | Your file states whether treaty treatment changes the creditable amount |

| FTC worksheet | Use treaty-reduced tax where treaty terms apply | Your FTC worksheet ties to adjusted amounts, not gross withholding |

| Self-employment interaction | Review treaty language alongside Schedule SE before finalizing your position | Schedule SE inputs align with the same income records used in your relief analysis |

| Social-tax overlap | Keep social-contribution analysis separate from income-tax relief | Your file shows separate decisions for income tax and social contributions |

If foreign tax is clearly documented and the U.S. taxes the same income, FTC is often the cleaner path. If treaty language directly assigns taxing rights or reduces source-country tax, treaty relief may be stronger. When treaty terms reduce the foreign tax, the creditable FTC amount follows that reduced amount, not higher withholding. In savings-clause contexts, you would typically rely on the Foreign Tax Credit to offset U.S. taxes on that same income.

Use this order:

- Verify foreign tax evidence. Match tax amount, jurisdiction, income item, and payment or accrual records.

Verification point: Every claimed amount has a document trail.

- Test treaty impact on the same income. Confirm whether treaty terms reduce source-country tax or change taxing rights.

Verification point: Your file states whether treaty treatment changes the creditable amount.

- Model FTC with treaty-adjusted figures. Use treaty-reduced tax where treaty terms apply.

Verification point: Your FTC worksheet ties to adjusted amounts, not gross withholding.

- Check self-employment interactions. For U.S. expat filings, review treaty language alongside Schedule SE before finalizing your position.

Verification point: Schedule SE inputs align with the same income records used in your relief analysis.

- Handle social-tax overlap separately. Keep social-contribution analysis separate from income-tax relief.

Verification point: Your file shows separate decisions for income tax and social contributions.

Decision rule: if you cannot prove foreign tax paid or accrued, do not default to FTC. Pause and fix the documentation first. Related: FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

Step 4 build the evidence pack that survives an audit#

If a reviewer cannot trace each number back to a source record, your position is weak. Build one filing-year pack that maps every claim to the exact supporting document.

- Map each claim to evidence. Keep an index that lists the claim, return or form line, and document reference. For FTC amounts, tie each figure to records showing the tax was imposed on you and paid or accrued.

- Reconcile account reporting end to end. Keep statements and transaction trails that support return reporting and account disclosures. Where account reporting overlaps, check consistency across the return, Form 8938, and FBAR. If aggregate foreign account value crossed $10,000, include your FBAR threshold worksheet.

- Keep a yearly claim memo as an internal control. Summarize your residency conclusion, relief method, and the documents behind each assertion. It is a control record, not a separate legal filing requirement.

- Store traceable records. Keep timestamped exports with stable IDs, and use masked working copies for sensitive data.

Two final checks prevent common audit problems: retain required FBAR account records for generally five years from the FBAR due date, and if you later find an FBAR error, file an amended FBAR and update your memo. Red flag: a clean narrative with no transaction-level proof. If a number cannot be traced, treat the claim as unproven.

Step 5 file in the right order and run post-filing checks#

When you file, your job is to present one consistent story across the return and disclosures, with no contradictions.

| Item | Action | Timing or note |

|---|---|---|

| Form 8938 | Attach Form 8938 when required | File it by the return due date, including extensions |

| FBAR | File FBAR separately through FinCEN | April 15 due date and automatic extension to October 15 |

| Cross-form consistency check | Verify names, addresses, residency claims, and foreign account reporting details do not conflict | Form 8938 and FBAR are separate filing regimes, so overlap does not require identical account populations |

| Form 1040-X | For return errors, file Form 1040-X and include changed forms/schedules plus supporting documents | If a refund is part of the correction, confirm you are within the 3-year/2-year amendment window |

| Delinquent FBAR | File according to FBAR instructions and include a statement explaining why the filing is late | If you find a mismatch after filing, document it immediately and start the correction path |

- Finalize your residency position for the year. Make sure it still matches your evidence pack.

- Lock the relief path. Confirm treaty relief, FTC, or mixed treatment before you finalize numbers.

- File the annual return package. Attach Form 8938 when required and file it by the return due date, including extensions.

- File FBAR separately through FinCEN. Track the April 15 due date and the automatic extension to October 15.

- Run a cross-form consistency check. Verify names, addresses, residency claims, and foreign account reporting details are not conflicting.

Check for consistency, not identical form content. Form 8938 and FBAR are separate filing regimes, so overlap does not require identical account populations. Keep a dated filing calendar for each obligation: deadline, submission date, confirmation receipt, and any follow-up task.

If you find a mismatch after filing, document it immediately and start the correction path. For return errors, you may need to file Form 1040-X and include changed forms or schedules plus supporting documents. For delinquent FBARs, file according to FBAR instructions and include a statement explaining why the filing is late. If a refund is part of the correction, confirm you are within the 3-year/2-year amendment window.

Common mistakes that trigger double-tax pain and how to recover#

Most painful cases come from using the wrong framework or filing without a defensible evidence trail.

- Mistake: using C corporation dividend advice for freelancer filings.

Recovery: reframe the case as individual cross-border service income, then return to residency and treaty analysis.

- Mistake: claiming FTC or treaty relief without proof of foreign tax.

Recovery: rebuild your support from tax payment records to return line items, then recheck eligibility before refiling.

- Mistake: dual-residency facts with no tie-breaker analysis.

Recovery: document each tie-breaker factor and keep every related form aligned to one residency position.

- Mistake: treating FBAR and Form 8938 as interchangeable.

Recovery: review both obligations separately, file fixes in the correct channel, and use delinquent FBAR procedures when eligible.

- Mistake: delaying escalation when facts are disputed.

Recovery: involve a qualified cross-border professional early when residency is contested, treaty interpretation is unclear, or more than one country is taxing the same income. Form 8938 failures can trigger material penalties, including a $10,000 failure-to-file penalty and up to $50,000 in additional penalties after IRS notification.

Conclusion and copy paste checklist#

In practice, this is usually a sequencing and documentation problem, not a search for a clever election. Strong filings come from one coherent residency position, correct treaty or FTC treatment, and forms that do not conflict.

Use this checklist every filing year.

- Confirm the problem type: individual treaty or FTC overlap versus separate corporate or shareholder issues.

- Set and document your filing-year tax residency position.

- Check tax treaty coverage by income type, and apply treaty tie-breaker tests only when dual residence exists.

- Choose FTC or treaty relief based on eligibility and evidence quality.

- If claiming FTC, file Form 1116 and remove taxes tied to excluded foreign earned or housing income.

- Assemble support files: residency records, contracts, invoices, payment records, and foreign tax proof.

- Reconcile disclosures: Form 8938 does not replace FBAR, and both may be required.

- Track FBAR threshold and deadlines: over $10,000 aggregate foreign account value, due April 15, automatic extension to October 15.

- For self-employment income, confirm Schedule SE treatment before final filing.

- Escalate to a qualified cross-border professional when facts conflict or treaty interpretation is uncertain.

If one line fails, pause and fix it before filing.

Frequently Asked Questions

What is double taxation for freelancers working across borders?

It is the same income being taxed by more than one country for the same period. For freelancers, this can mean one country taxes you as a resident while another taxes the same income under its rules.

How can I legally avoid double taxation without creating audit risk?

Start with residency facts, then confirm treaty coverage and relief eligibility for each income type. Keep one evidence pack that ties each claim to contracts, invoices, payments, and filed forms.

What is a tie-breaker rule in a tax treaty and when does it apply?

It is the treaty mechanism used when both countries treat you as a resident under their domestic rules. Apply the tests in order (starting with permanent home, then center-of-vital-interests logic if needed) and document the result against the treaty text for that country pair.

FTC vs treaty relief for a U.S. expat freelancer: how do I choose?

Choose based on eligibility and evidence for the same income stream. The annual FTC-versus-deduction choice applies across all qualified foreign taxes, and income you exclude generally cannot support an FTC claim.

What documents do I need to support a Double Taxation Agreement claim?

Keep residency records, foreign tax payment proof, contracts, invoices, and payment trails tied to each claim amount. Treaty-based return positions may require Form 8833 with treaty country and article details, and some cases may also require residency certification (Form 8802 request process).

When should I talk to a cross-border tax professional?

Escalate early when residency is disputed, treaty interpretation is unclear, or filings conflict. Escalate when more than one country taxes the same income.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

FEIE vs Foreign Tax Credit for High-Earning US Expats

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing `Form 1040`, first confirm what you can actually claim and support, then compare the tax result.

Understanding the Independent Personal Services Article in Tax Treaties

Treaty relief is not something a payer simply turns on automatically. It is a [claim process](https://www.irs.gov/individuals/international-taxpayers/claiming-tax-treaty-benefits), and for a nonresident alien (NRA), compensation for personal services performed in the United States is generally subject to 30 percent withholding unless an exception applies. Relief can reduce that withholding, but only when your facts support the position and the filing steps are handled correctly.