Quick Answer

Use a decision-first process for argentina exchange rate hacks: choose the route by urgency, risk, and documentation needs, then verify with a small transfer before scaling. The article’s core recommendation is to compare Western Union, banks, cards, street cash, and crypto by final usable ARS and traceability, not headline spread. Keep a backup channel active, and log timestamp, reference ID, and final amount received on every conversion.

Why most Argentina exchange advice breaks for freelancers#

Most exchange advice breaks for freelancers because it is built around one lucky conversion, not a repeatable result. Your real target is not the prettiest quoted rate. It is usable ARS after each client payment, on the timetable your life actually runs on, with records you can explain later if anyone asks.

That is why so much tourist advice falls short. Tourist tips are usually written for short stays, one-off cash needs, and a simple question: where do I get the best deal today? Freelancer decisions have to survive invoice cycles, rent dates, recurring bills, and reconciliation. A route can show a better quote and still be the wrong choice if payout is delayed, access is blocked, or the paperwork is too thin to defend later.

Treat each channel as its own risk profile. Cash exchanges, banks, cards, transfer services, and crypto do not just produce different rates. They break in different ways. If you compare only the headline quote, you miss what usually causes the real damage: settlement delays, holds, reversals, weak proof, and uncertainty about when the money became usable.

So the process matters more than the anecdote. A smooth report from one traveler or freelancer only proves that something worked once, under one set of conditions. It does not prove you can rely on it next week when rent is due or when a provider suddenly wants more checks. For recurring income, the question is always the same: can I get from invoice to spendable ARS in a way that still makes sense when conditions shift?

Before you move money, use the same sequence every time.

- Define the job for this invoice: speed, cash need, record quality, and amount at risk.

- Pick one primary rail and one backup rail before you initiate anything.

- Run a small verification transfer first, then measure the actual ARS received.

- Save evidence immediately: timestamp, receipt or reference ID, quoted amount, final amount, and where funds became usable.

That verification step is where a lot of forum advice falls apart. Someone can truthfully say a route worked well for them and still give you bad guidance, because what they are describing is a moment, not a dependable process. A route that worked once can fail later because counterparty behavior changed, a compliance review was triggered, or payout conditions shifted.

For recurring income, a slightly weaker quote is often the better choice if settlement is traceable from start to finish. This guide follows that logic: classify the path, compare the real outcome, choose the route by invoice, execute with checks, and log the result while the details are still fresh. For a deeper inflation-specific lens, read Handling Hyperinflation: A Financial Guide for Nomads in Argentina.

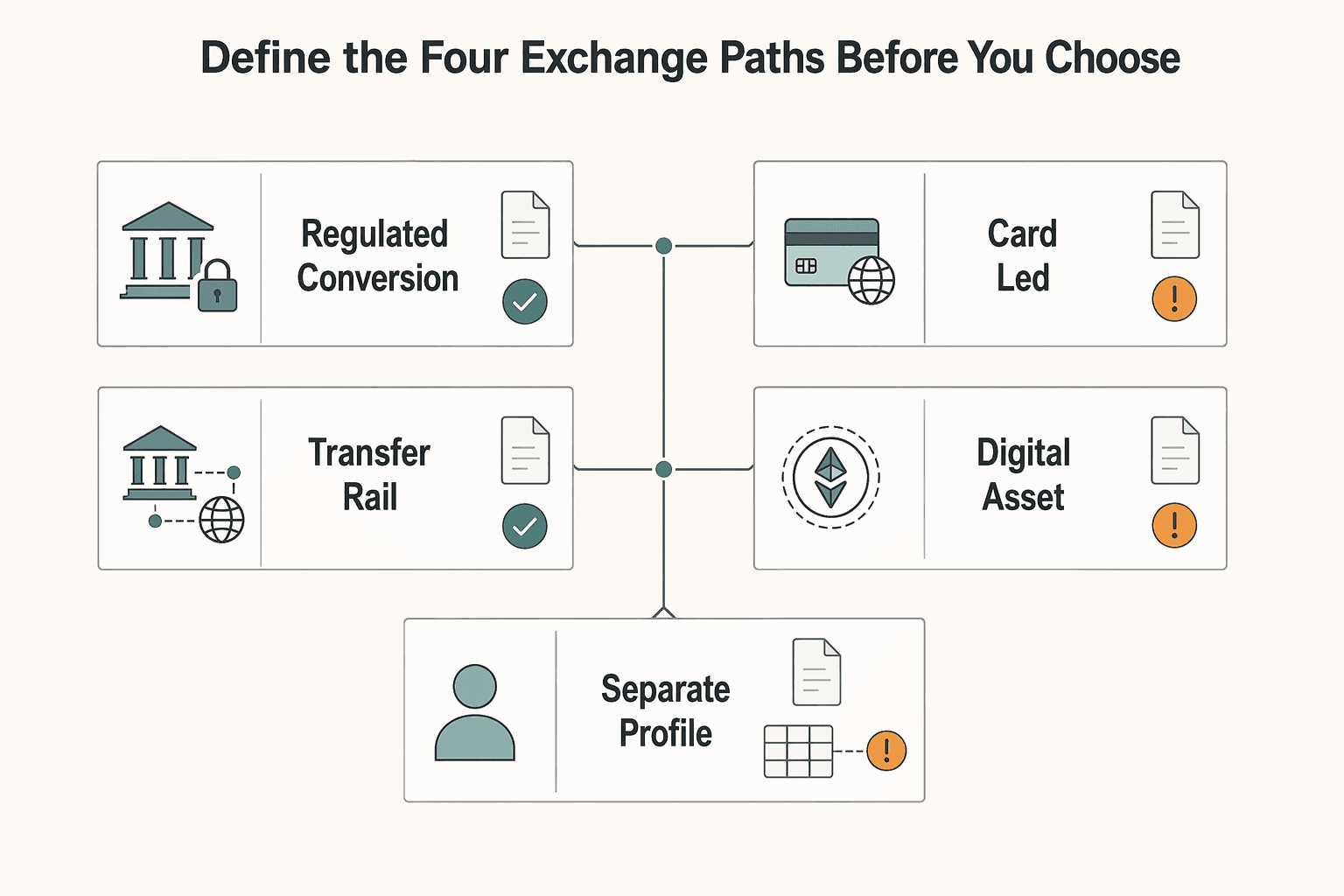

Define the four exchange paths before you choose#

Name the path first, or the comparison goes wrong. Argentina can show multiple exchange rates at the same time, including official and alternative rates, and the result changes depending on how you move the money. If you skip that classification step, you end up comparing things that are solving different jobs.

Use this map to classify options, not to rank them:

| Path | What it is | Risk framing |

|---|---|---|

| 1. Regulated conversion | Banks and official exchange houses converting into ARS | Regulated route with its own controls and constraints |

| 2. Card-led spend | Credit cards and debit cards used directly for purchases | Card-based route with a different use case than cash conversion |

| 3. Transfer rail | Western Union sender-to-recipient transfer flow | Transfer route with its own access and process constraints |

| 4. Digital-asset route | Cryptocurrency or stablecoin route into ARS | Alternative route with a distinct risk and control profile |

| Separate profile: street cash | Informal in-person cash exchange, including areas like Calle Florida | Separate risk profile, not just another rate line |

The big mistake is treating every quote like it belongs on one simple price list. It does not. Card-led spend solves a different problem than cash conversion. It helps you pay merchants directly and can reduce how much cash you need to carry, but it is not the same thing as converting a larger payment into ARS for broader use. Street cash is not just another rate line either, because it changes both the handoff risk and the quality of the record you keep.

That distinction matters operationally. If you do not separate merchant spending from cash access, or regulated conversion from informal handoff, you will make bad comparisons from the start. A quote that looks strong in a screenshot may still be the wrong tool if the path is slow, hard to document, or exposed to avoidable risk at pickup.

Choose based on risk tolerance, timeline, legal exposure, and capital controls, not on the headline quote alone. Once an option is in the right bucket, run a small checkpoint before you scale it. Then log the rate category, timestamp, confirmation reference, and final ARS received. That gives you something real to compare later: execution, not folklore. You might also find this useful: How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Compare Western Union, crypto, banks, cards, and street cash on what actually matters#

What matters is not the posted quote. It is the channel that turns into spendable ARS on time, with proof you can keep and risk you can live with.

Because multiple rate lines and channels can exist in parallel, use the same scorecard each time:

| Channel | Net received in ARS | Time to usable funds | Reversal or hold risk | Documentation quality | Personal safety |

|---|---|---|---|---|---|

| Banks and official exchange houses | Check final ARS against the quoted line you used | Confirm when funds are actually usable | Confirm process interruptions before relying on timing | Keep every receipt or reference for reconciliation | Prefer formal locations and procedures |

| Western Union | Compare quoted amount versus final payout | Verify pickup timing and availability | Confirm transfer and pickup status before assuming access | Keep transfer references end to end | Use formal pickup points, not ad hoc handoffs |

| Credit cards and debit cards | Compare merchant charge outcome to other options | Usually usable at point of sale when accepted | Card-side checks can interrupt a payment | Statements are typically easy to retain | Reduces need to carry cash for routine spend |

| Street cash, including blue dollar areas | Headline quote can differ from final outcome | Timing depends on completing an in-person exchange | Counterparty risk is concentrated in the handoff | Records are often limited | Highest caution needed during in-person exchange |

| Cryptocurrency or stablecoin | Verify the full path into ARS before judging net result | Timing depends on each step in the path | Access can fail at on-ramp or off-ramp points | Record quality depends on platform and your process | Safety depends on where and how conversion completes |

Use the table like a job sheet, not a ranking. A route can be strong on one criterion and weak on another. If a payment needs to cover near-term obligations, time to usable funds matters more than squeezing out a slightly better quote. If a payment might need explaining later, documentation quality moves to the top. If you are trying to reduce personal risk, the handoff itself becomes part of the economics.

In practice, each option earns its place for different reasons. Banks and official exchange houses are easiest to justify when you want a more formal process and cleaner receipts. Western Union can be useful when you need a sender-to-recipient flow that is easy to track, but you still have to verify pickup timing and cash availability instead of assuming the quote alone solves the problem. Cards are often the cleanest tool for routine merchant spend because they reduce the need to carry cash, though they are only as good as acceptance in the moment. Street cash can look attractive on paper, but it concentrates the rate decision, the counterparty decision, and the safety decision into one handoff. Crypto only earns its place once you have tested the entire path into ARS and know where it can stall.

That is why "best rate" is the wrong frame. The better question is: which channel gives me the right mix of net value, timing, proof, and friction for this specific payment? Once you compare the options on those terms, the next step gets much easier. You stop hunting for a universal winner and start routing each invoice according to its actual job.

Use decision rules to pick the route for each invoice#

Do not look for one permanent winner. The right route can change with timing, amount, record requirements, and whether you need cash or simply need to spend. What should stay fixed is the way you decide.

| Decision factor | What to check | Default action |

|---|---|---|

| Urgency | Shortest verified time to usable ARS from your own recent transfers | Use the channel with the fastest verified settlement time |

| Amount at risk | Whether the invoice is large and availability is uncertain | Lean toward Western Union or banks and stage the amount if needed |

| Record requirement | Whether the payment may be reviewed later | Require a receipt or reference ID before relying on the path |

| Handoff exposure | Whether the route depends on an in-person exchange, for example around Calle Florida | Limit the amount to what you can afford to delay |

| Continuity | Whether one failure would freeze your week | Keep one fallback active, such as card spend plus a secondary cash option |

Predictability should usually outrank headline rate when an invoice has to cover near-term obligations. That does not mean ignoring the quote. It means putting the quote in its proper place, behind settlement certainty and your ability to explain what happened later.

Run this routing check every time:

- Urgency: Use the channel with the shortest verified time to usable ARS from your own recent transfers. Your log is more useful than a posted estimate.

- Amount at risk: For larger invoices, lean toward channels that give stronger transfer records, such as Western Union or banks. If availability is uncertain, stage the amount instead of assuming one large move will land cleanly.

- Record requirement: If the payment may be reviewed later, require a receipt or reference ID before you rely on that path.

- Handoff exposure: If the route depends on an in-person exchange in Buenos Aires, for example around Calle Florida, limit the amount to what you can afford to delay.

- Continuity: Keep one fallback active, such as card spend plus a secondary cash option, so a single failure does not freeze your week.

The working question is not "what was the posted quote?" It is "did the funds become usable on time, and can I trace the path from start to finish?" That shift sounds small, but it changes behavior. It pushes you to measure actual results instead of trusting public chatter, and it keeps you from scaling a route before you have seen it work under your own conditions.

Log each transfer with the invoice ID, rail, timestamp, expected receive window, actual receive time, and final ARS received. Once you do that for even a short period, the noise starts to clear. Some options that looked strong in theory will reveal slow settlement or weak proof. Others that looked slightly less attractive on rate will prove more dependable cycle after cycle.

Do not scale a channel just because the first pickup went smoothly. A Feb 2024 anecdote reported Western Union self-transfers working at first, then more friction above around USD 100 because cash availability varied across shops. Treat that as a caution signal, not a rule, and stage larger amounts. The lesson is not about one provider alone. It is about size and assumptions. Larger moves deserve more caution because a small operational snag becomes a bigger cashflow problem.

Apply the same discipline to card rails. Some travelers report tourist card treatment that can be closer to informal market levels in some periods, but that can change. Test a real merchant transaction and record the settled ARS before you depend on it for a critical cycle. Card behavior is only useful to you once you have seen the posted charge turn into a settled outcome you can compare.

A simple way to think about it is this: urgent invoices go first to the route with the shortest verified settlement time; larger or more sensitive invoices go first to the route with the strongest records; messy or uncertain routes only get smaller amounts until they prove themselves. It is not glamorous, but it is how you keep one bad afternoon from turning into a bad month.

If timing and records matter most, start with the more traceable channels and accept a weaker nominal quote. If speed matters but certainty is lower, split between a primary and a backup so one failure does not freeze cashflow. If you want cleaner invoice inputs before you start converting, try the free invoice generator.

These decision rules work much better if you prepare the rails before you arrive. Setup is what turns a good rule into something you can actually use under pressure.

Set up your money flow before you land in Buenos Aires#

Do the setup before you travel. Arrival day is the worst time to discover that a backup card fails, account details do not match, or a provider wants an extra check before releasing access.

The goal is simple: a tested chain from payment receipt to ARS access on day one. Build that chain in order. Start with your primary receive method. Add your primary conversion method into ARS. Then add a backup spend method, such as an internationally working ATM card or a reliable card spend path. Finally, define one emergency arrival cash fallback. Do not make airport currency exchange booths your default backup.

Use this pre-departure check:

- Confirm your receive rail can take payments now, not just in account settings.

- Verify that account details match across rails, including name, ID, and access.

- Test your backup spend method with a small real transaction.

- Write down one emergency cash option and its access requirements before you fly.

- Save support contacts and recovery steps offline.

Be clear about what each test actually proves. A receive-rail test only shows that the payment can arrive. A backup card test only shows that you can still spend if a transfer slows down. Neither proves the full chain will work. That is why the steps should be tested separately and logged separately. If you only test the first leg, you can still get stuck at the point where you need ARS.

Set your invoice and conversion rules before you send invoices so you are not improvising under pressure. That is especially important when you first land, because fatigue and urgency make people accept weaker evidence, weaker terms, and weaker backup plans than they normally would. A good setup cuts down those forced decisions.

Then use one evidence template for every transfer: confirmation, FX snapshot at decision time, receipt or reference ID, final ARS received, and where funds became usable. That gives you a consistent record from the beginning and makes later reconciliation much easier.

If you do this work before landing in Buenos Aires, physical cash becomes an exception instead of the center of the plan. Related: Buenos Aires, Argentina: The Ultimate Digital Nomad Guide (2025).

Execute cash exchange safely when you must use physical currency#

If you have to use physical cash, treat the handoff as the main risk, because it is. A strong informal quote does not help if the amount changes at the last moment, the terms get vague, or you walk away unable to prove what happened.

The material behind this guide does not support reliable, universal claims about informal execution, hotel desk matching, or predictable bill treatment. That alone is a good reason to treat cash exchange as a fallback, not a default. Use it to solve a specific gap, not as the whole operating plan.

Use a simple pre-handoff check:

- Confirm the exact amount you will give and receive.

- Recalculate the final ARS total yourself before completing the exchange.

- Verify what you received immediately and log the transaction details.

Small mistakes compound quickly in cash because there is usually less paperwork to fix them later. In practice, the danger point is the moment you stop checking because the quote sounds good. Do the math yourself. Confirm the amount in hand before you leave. Log the result while it is still fresh. If the amount, timing, or terms become vague, stop and use a more trackable channel instead.

That is also why unsupported shortcuts are risky. Claims such as hotel desks matching informal rates or larger USD bills always getting better treatment are not confirmed here. They may be reported from time to time, but they are not solid enough to run a recurring cashflow plan around. For routine operations, keep leaning on channels that leave stronger records and fewer open questions.

Keep records that survive disputes, taxes, and compliance checks#

Records are part of the conversion, not paperwork you clean up later. If you cannot explain a payment path after the fact, you did not really control it when it happened.

Use one ledger-friendly log with one row per conversion so each invoice maps to one conversion event and one final ARS outcome. That structure sounds simple, but it matters. The moment you cannot tie a payment to a specific conversion quickly, the process is already too loose. A good log is boring on purpose. You should not need memory, screenshots scattered across apps, or half-remembered messages to reconstruct what happened.

Use this minimum record set each time:

- Invoice ID and client name

- Origin currency and amount, for example USD or EUR

- Channel used, for example Western Union, bank, or crypto off-ramp

- Conversion timestamp and the timestamp when funds became usable

- Receipt or reference ID

- Final ARS received

- Short note on where funds landed, for example bank account, cash, or card balance

Treat reconciliation as a standing checkpoint, not end-of-month cleanup. On a regular schedule, tie invoice totals, conversion records, and spend entries together. If something does not match, pause new conversions until you can explain the gap instead of letting small errors stack up. That discipline is especially useful when you are mixing methods, because the more channels you use, the easier it is for one missing reference or one delayed entry to distort the picture.

Keep personal and business flows separate from the start, using separate labels, folders, and, where possible, separate destination accounts or wallets. That one habit reduces confusion later more than most people expect. It also makes it easier to answer basic questions from an accountant, a provider, or a client without digging through unrelated personal activity.

Before moving larger sums, confirm current corridor-specific checks with each provider. Regulatory treatment is not uniform across jurisdictions: one source describes a U.S. approach that places crypto within existing legal structures, while another describes China banning certain fiat-to-crypto exchange or financing activities in 2017. The practical point is not to master every rule. It is to avoid assuming that one provider experience or one country setup carries over cleanly to the next.

That same restraint applies to compliance data. Keep what you need for KYC/AML review and avoid oversharing unrelated personal data. Good records are not the same thing as handing over everything you can think of. The goal is to keep enough proof to show the route, the timing, and the amount, without creating new problems through sloppy document handling.

If you already know which fields you save every time, audits and reviews become much less dramatic. They turn into a retrieval problem, not a memory problem. That is where clean process pays off.

Red flags that turn a good rate into a bad outcome#

Bad outcomes rarely start with the rate. They usually start with vagueness, time pressure, or missing proof. By the time the spread looks disappointing, the real mistake has already happened upstream.

A quote is only good if settlement is provable from start to finish. If you cannot show the counterparty, settlement time, reference ID, and final ARS received, treat the result as bad no matter how attractive the spread looked. Use a hard gate: no receipt, no reference ID, no exchange.

Use this screen before converting:

- The quote looks attractive, but the payout path or timing stays vague

- Pickup or access terms are unclear until after funds are handed over

- You are being pushed to decide quickly in Buenos Aires without time to verify

- The quote depends on old blue dollar snapshots instead of executable current terms

- Your ledger cannot tie the invoice amount, conversion event, and final ARS together

A second red flag is repeated ad hoc decision-making. If every payment turns into a fresh guess, you do not have a process, you have exposure. Use tested fallback channels for small urgent needs, and require full documentation before larger conversions. A route can still be useful in a narrow role without becoming your default.

One practical stress test catches a lot of weak setups: explain the trail in under one minute using the origin currency, counterparty, timestamp, reference number, and final ARS outcome. If that explanation is messy, the process is too fragile for reliable cashflow. Good routes are not just executable. They are explainable.

Build a repeatable system that protects rate and cashflow#

The durable edge here is not chasing every better quote. It is making the same good decision under changing conditions.

Use a channel mix with a primary path, a backup path, and a tightly limited exception path. Default to the lower-risk options, and treat informal cash exchange as a narrow tool for specific gaps rather than everyday operations. The point is not to predict every shift. It is to stop any one shift from breaking rent timing, access, or reconciliation.

Apply one decision card each payment cycle:

- Objective first: choose the priority for this conversion, speed, net value, or traceability

- Entry check: confirm route availability now, not from old assumptions

- Evidence check: capture the timestamp, quote snapshot, receipt or reference, and final amount received

- Exception rule: if you need a higher-risk path, cap the amount and reconcile the same day

- Stop rule: if a required field is missing, pause and reroute

Then review the results on a fixed cadence. When markets are noisy and terminology is inconsistent, observed outcomes beat confident claims. A common failure mode is drift: an old default stays in place after conditions changed. Prevent that by comparing planned versus actual time to usable funds, total received, and missing documentation count, and change one variable at a time so cause and effect stay visible.

If you handle multiple clients, standardize invoice intake, conversion logging, and reconciliation templates, then reuse them every cycle. That reduces mental load and makes weak spots easier to spot. If a teammate cannot reconstruct a conversion quickly from your log, simplify the process until they can. If you cannot explain a route clearly to yourself, it is probably too fragile to trust with important money.

The goal is not perfection. It is steady, explainable execution. Once you have that, rate decisions become easier because they sit inside a process that protects both cashflow and proof.

Frequently Asked Questions

Is the blue dollar still worth using in 2026 for freelancers?

It can still matter, but not as a default route. Card conditions changed in April 2025, and one travel source says credit cards are processed at the MEP rate and can sit close to blue in some periods. Treat old screenshots as history and compare executable options today.

What is the safest option in Argentina between official exchange houses, banks, and street exchange?

Whichever route you choose, verify the final terms and handoff in real time, and keep clear records of each transaction.

Should I choose Western Union or cryptocurrency for faster access to ARS?

There is no universal speed winner. Choose the route with the shortest verified time to usable funds in your own recent logs.

Do larger USD bills usually get better exchange treatment in Buenos Aires?

Some people report this, but it is not reliable enough to plan around. Any difference can vary by counterparty and timing. Confirm final ARS before handing over cash.

Can hotels reliably match blue dollar rates?

Do not assume they do. Check a live quote and calculate the net amount you will receive before accepting convenience.

When should I use credit cards or debit cards instead of converting more cash?

Use cards for routine merchant spend when acceptance is working, and keep a backup path for cases where card acceptance fails. One forum commenter says foreign credit cards work almost always in person and at most online sites, but not all. Avoid airport ATMs and exchange bureaus when possible because fees are often higher.

What proof should I keep for each conversion to handle compliance or accounting reviews?

Keep one row per conversion with origin amount, channel, timestamp, receipt or reference ID, and final ARS received. Also record where funds became usable. For ATM cash access, log fee details because costs can include a flat fee and a percentage charge.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Navigating Hyperinflation: A Financial Guide for Nomads in Argentina

Argentina can still work well for freelancers and small teams, but 2026 is not a cheap rerun of 2023. The question is not just what a city looks like on a cost comparison page. It is whether your money arrives when you expect it, holds enough value to stay useful, and stays accessible when rent, payroll, or vendor invoices come due in Buenos Aires.

Buenos Aires Digital Nomad Guide for Remote Professionals (2026)

You can make Buenos Aires work well if you treat the move as a verification phase first, not a lifestyle commitment. How well it works depends less on the city's reputation than on your execution. Confirm your entry path, keep your documents ready, and make sure your money access can survive a bad week.

How to Get Paid in Multiple Currencies Without Forced FX

If you want to **get paid in multiple currencies** while protecting margin, separate collection from conversion. Receive the client's currency first, then decide if, when, and where to convert it.