Quick Answer

UK companies do not charge UK VAT on every sale to a US client; the treatment depends on whether the sale is goods, B2B services, or a B2C or special-rule service. Goods exported from the UK can be zero-rated if the conditions are met and export evidence is obtained within 3 months of sale, while B2B services to a US business are typically outside the scope of UK VAT under the general rule.

Expanding your UK business into the US market is a real milestone. It also brings up a question early, and often more than once: how do you handle UK VAT correctly?

Cross-border VAT rules are not always intuitive. When the treatment is unclear, that uncertainty can turn into invoice delays, client friction, and unnecessary HMRC risk.

You do not need to become a tax specialist overnight. You need a repeatable way to decide each sale, keep the right evidence, and report it consistently. The simplest approach is to work through the same three steps every time: Classify, Document, and Report. Done properly, that turns VAT from a background worry into a routine part of selling to US clients.

Step 1: Classify Your Supply - Goods or High-Value Services?#

VAT treatment starts with classification. Before you invoice, decide whether the contract is for goods, B2B services, or a B2C/special-rule service. That decision drives the UK VAT treatment from the start.

Use this first-pass route:

- Goods: You are shipping physical items from the UK to the US. These can be zero-rated if you meet the conditions and get export evidence within 3 months of sale.

- B2B services: You are supplying services to a US business. Under the general rule, services are taxed where the customer belongs, so this is typically outside the scope of UK VAT.

- B2C or special-rule services: If the customer is not in business, the default B2C rule is where the supplier belongs, unless a special rule applies, including some digital services.

| Supply type | VAT treatment label | Charge UK VAT? | Invoice implication | Why it matters later |

|---|---|---|---|---|

| Goods exported UK to US | Zero-rated export | No, if zero-rating conditions are met | Treat as zero-rated export, not a standard-rated UK sale | You must hold export evidence and apply the correct goods treatment |

| B2B services to a US business | Outside scope of UK VAT | No | Do not add UK VAT if B2B status is evidenced and the general rule applies | Outside-UK place of supply affects VAT treatment and taxable-turnover calculations |

| B2C or special-rule services | Depends on the rule that applies | Do not assume | Pause and verify before invoicing | Misclassification can change the VAT treatment completely |

For service businesses, the practical checkpoint is proving that the US customer is in business. HMRC allows non-VAT-number evidence routes for non-EU customers, so build a basic pre-invoice pack such as:

- Contract documents showing the customer's business identity and address

- Business letterhead or commercial website

- Publicity material showing business activity

- Fiscal certificate or other business tax documentation

If you cannot support business status, the default treatment is B2C.

Pause before invoicing when the facts are mixed, such as goods and services in one bundle, an unclear contracting party, or a service that may fall under a special rule. Verify the contracting entity, confirm business status, and check whether an exception overrides the general rule. If it still is not clear, get VAT advice before you lock in the treatment.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Step 2: Document Everything - Your Bulletproof Evidence for HMRC#

Documentation is where compliance either stands up or falls apart. HMRC says you should keep records, for example bank statements or receipts, so you can fill in your tax return correctly. Build each file so another reviewer can follow the transaction without needing extra context.

From the material here, the confirmed points are mostly around recordkeeping and filing admin. Keep those clean, and treat VAT-specific evidence rules as items to verify separately.

| Evidence track | What to collect | Why it matters | Where teams usually fail |

|---|---|---|---|

| Self Assessment records | Bank statements, receipts, and other return records | HMRC expects records so you can complete your return correctly | Keeping partial records and relying on memory later |

| Registration and account access | National Insurance number, Self Assessment registration status, UTR, and reactivation status for older accounts | First-time filers must register before online filing, and filing without reactivating an existing account can delay the return | Trying to file first-time without registering, or using an inactive account |

| Filing and payment timing | The dates for telling HMRC, filing, and paying | Late notification can lead to a penalty, and timing mistakes can delay completion | Treating fixed HMRC dates as flexible |

| VAT-specific evidence rules | Mark as "verify separately" | This material does not confirm VAT export/client-status proof requirements | Assuming VAT proof rules are confirmed here when they are not |

Goods export proof#

The material here does not establish VAT export-proof requirements, including whether purchase orders, transport evidence, or customs departure confirmations are required. Treat those items as unconfirmed here and verify them separately before you rely on them.

B2B service client-status proof#

The material here also does not establish VAT client-status proof requirements for B2B services to US clients. Keep your case file clear, but do not treat any specific VAT proof list as confirmed from these excerpts.

Minimum defensible evidence pack#

If one document is missing, do not guess. Start from the minimum file you can defend:

| File element | Include |

|---|---|

| Records | Bank statements, receipts, and related return documents |

| Access | National Insurance number and UTR details needed for registration/filing |

| Timing | The dates that govern when to tell HMRC, file, and pay |

| Gap note | What is missing, what you checked, and who is responsible for closing the gap |

| Mixed or ambiguous cases | A short written rationale for the treatment you chose |

Add an internal note that states what is missing, what you checked, and who is responsible for closing the gap. For mixed or ambiguous cases, include a short written rationale for the treatment you chose.

File it so you can report from it#

A consistent folder structure saves time later and makes review easier. Use one folder per case with a fixed structure: 01-registration, 02-records, 03-filing, 04-correspondence, 05-reporting-note. Keep a one-page summary with the entity name, key dates, and any open items.

Key checkpoints: tell HMRC by 5 October for the relevant previous tax year, file on or after 6 April following the end of the tax year, and pay by 31 January. Late notification can result in a penalty.

This record discipline also helps with Self Assessment admin. Keep your UTR accessible, and make sure an existing account is reactivated before filing so you avoid delays.

You might also find this useful: A Guide to VAT for UK Freelancers.

Step 3: Report with Confidence - Perfecting Your Invoice and VAT Return#

Once the classification is right and the evidence file is complete, reporting should be as mechanical as possible. Your invoice, VAT code, and return entry should all follow the file you already built, not a last-minute judgment call.

Build the invoice from the treatment, not from habit#

Invoices should reflect the treatment you decided, not whatever your last template happened to say.

| Invoice control | Requirement |

|---|---|

| Invoice number | Use a unique sequential invoice number |

| Time of supply | Keep this core field correct |

| Cross-border B2B wording | Use invoice wording checked against current HMRC guidance or qualified tax adviser records |

| Wording placement | Place it directly under line items or immediately above totals |

| Party mismatch | Pause and reconcile if the contract party, invoice party, and paying entity do not match |

For B2B services, start with place of supply. Under the general rule, if your business customer belongs outside the UK, UK VAT is not chargeable. Do not apply that automatically to every service sale to a US client, because special rules can apply in some cases.

When you build the invoice, make sure the basics are right first, especially the unique sequential invoice number and the time of supply. For cross-border B2B services, use invoice wording checked against current HMRC guidance or qualified tax adviser records, and place it directly under line items or immediately above totals so the client's AP team can process it quickly.

If the contract party, invoice party, and paying entity do not match, pause and reconcile that before you issue the invoice.

Route each sale into the return deliberately#

Do not post first and rationalize later. Start with the Step 1 classification, then confirm that the Step 2 evidence supports it before you code the sale.

| Sale type | VAT treatment | Return destination | If classification is uncertain |

|---|---|---|---|

| Goods export from the UK | Zero-rated only if export evidence is obtained and retained | Include net value in Box 6 where your return mapping requires it; confirm your software mapping before filing | Do not assume zero rating; hold for review if export proof is missing or inconsistent |

| B2B services under the general rule (customer belongs in the US) | Outside scope of UK VAT when place of supply is outside the UK | Box 6 is commonly used for net value; verify the live Notice 700/12 position before filing | Recheck whether a special rule applies before coding outside scope |

| Unclear or mixed case | Do not force a code from memory | Pause posting or use a temporary review code outside final return flow | Escalate with contract, invoice draft, and evidence pack attached |

Keep registration logic separate from return logic. Supplies with place of supply outside the UK are excluded from taxable turnover for VAT registration calculations, including against the £90,000 test.

Add hard controls before submission#

Two controls are worth prioritizing before you file: export-evidence timing for goods, and accurate digital filing.

For goods exports, make the 3-month export-evidence deadline non-negotiable. If the proof is not in the file within 3 months from the time of sale, treat it as an exception for active review.

For filing, rely on digital controls. VAT-registered businesses are generally required to file through functional compatible software and pay electronically, so invoice setup, coding, and tax-point accuracy are all part of compliance.

Use a simple US sales-tax risk screen#

A clean UK VAT position does not tell you whether the US side is clear. US indirect tax exposure is state-level, not federal, so screen risk by state:

| Risk level | When it applies |

|---|---|

| No action | No verified state trigger met based on your current facts |

| Monitor | Repeated sales into specific states, or sales approaching a state threshold and measurement period verified from current official state records or a qualified tax adviser |

| Escalate to advisor | Any potential state presence or a verified trigger crossed |

State rules differ, so check each relevant state directly. For example, published $500,000 thresholds in Texas and California operate under different state rules.

Operator checklist before you file#

Use a short pre-submit check so filing stays tied to the underlying evidence:

- Confirm each sale still matches Step 1 classification: goods export, general-rule B2B service, or exception-for-review.

- Confirm Step 2 evidence is complete for that classification.

- Check invoice output: sequential number, correct time of supply, and verified cross-border wording in the correct location.

- Validate accounting or VAT code against evidence, not memory.

- For goods, confirm export evidence was obtained within 3 months of sale.

- Run a pre-submit review of Box 6 postings, unresolved exceptions, and any live-guidance points that still need verification.

Related: Understanding the UK's Statutory Residence Test (SRT).

Before you send your next US invoice, use the free invoice generator to help standardize wording and keep records consistent for your return workflow.

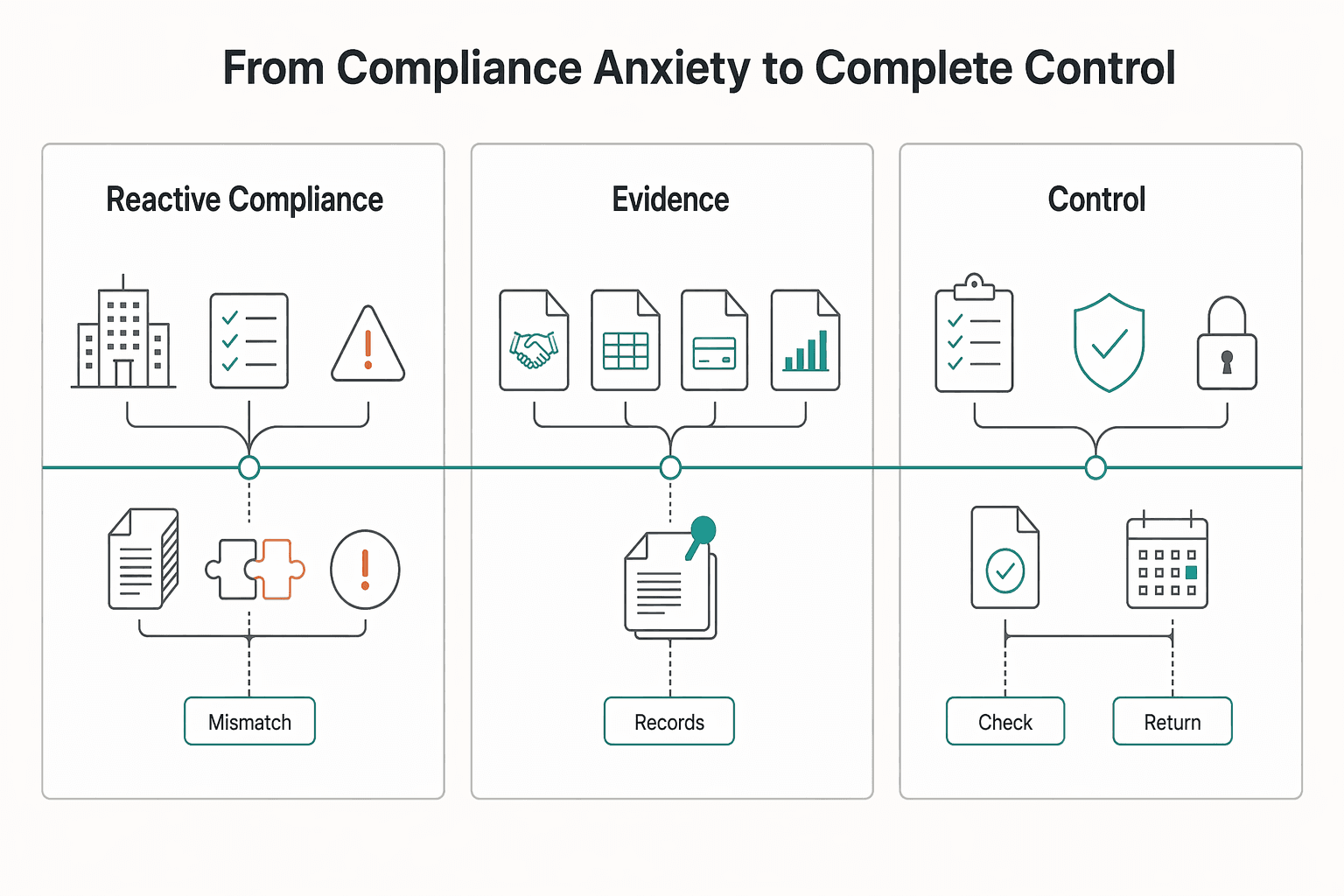

From Compliance Anxiety to Complete Control#

Control comes from running the same Classify -> Document -> Report loop on every engagement, then repeating it at month end.

In practice, that means doing the work in sequence. Before you file, confirm your business structure, for example sole trader or limited company, check whether you need first-time registration or account reactivation, and note any VAT points that need separate advice. Then build one file for the engagement with the contract, invoice, payment record, and supporting records. Finally, report from that file, not from memory. That usually cuts down avoidable rework and leaves you with a clearer HMRC trail if questions come later.

| Approach | What happens in practice | Common failure point | Safer default |

|---|---|---|---|

| Reactive compliance | You file first and review filing status later | First-time registration or account reactivation is missed, and filing can be delayed | Confirm registration/reactivation status and filing route before you file |

| Partial documentation | You keep only one or two records | You cannot clearly support what was filed | Keep one engagement file with key records and decision notes |

| Controlled workflow | You run the same checks each time and log decisions | Deadlines and filing windows are checked too late | Check current-year HMRC deadlines and filing windows before submission |

Keep the HMRC process checkpoints in view as well. Register for Self Assessment before first-time online filing, keep your UTR ready, and reactivate an existing account before filing again if needed. Keep records such as bank statements or receipts so your return can be completed accurately. If you cannot use the online filing service, use the alternative filing routes HMRC provides.

Use this quick checklist each cycle:

- Verify internally: business structure, filing status (register or reactivate), UTR, filing route, and supporting records.

- Record your decision notes and supporting records when the invoice is raised.

- Pause and get specialist advice if VAT treatment is unclear.

For a step-by-step walkthrough, see A Guide to VAT MOSS for UK Freelancers Selling Digital Services to the EU.

If your client mix spans multiple countries and VAT treatment feels unclear, run a quick decision check with the VAT reverse charge checker.

Frequently Asked Questions

Do you charge VAT on consulting services to a US company?

Maybe, but do not assume the answer from the client location alone. The result depends on the exact service and whether a special rule applies. Recheck the Step 1 classification, verify the current HMRC VAT treatment for that service type, then issue the invoice.

What wording should you put on a UK invoice to a US client for services?

Use verified wording, not copied wording from an old template. Use wording checked against current HMRC guidance or qualified tax adviser records, place it directly under line items or immediately above totals, and log when you last checked it.

What documents count as proof of export for physical goods?

Use an evidence pack, not a single-document file. Keep related sales, shipment, and customs records together where relevant. Verify the exact required documents and timing against current HMRC VAT guidance before you rely on them.

How do you prove a US client is a business for VAT purposes?

Treat business-status evidence as a verification step, not an assumption. Keep the contract, onboarding details, and business-identity evidence in one file. Pause if the legal entity on the contract does not match the entity on the invoice.

Do you need to register for VAT in the UK if you only sell to US clients?

Maybe. It depends on what you sell and how current VAT rules treat those sales for registration. Verify the exact threshold, assessment period, and sale-type treatment against current HMRC records or a qualified tax adviser before using them. Keep VAT registration separate from Self Assessment, because a sole trader earning more than £1,000 in a tax year can still need Self Assessment registration.

Does “no UK VAT” mean you do not have to worry about other taxes or filings?

No. VAT is only one part of your compliance workload, and Self Assessment can still require an active account, your UTR, and records such as bank statements or receipts. Keep separate checklists for VAT, profit taxes, and any US-side review. If you previously stopped filing Self Assessment, reactivate before filing again.

What if one contract includes services plus a deliverable, licence, or physical item?

Treat it as a review case, not a routine invoice. Document the contract terms, pricing, and deliverables clearly, then verify the current VAT treatment before invoicing. Escalate if your file cannot clearly support the approach.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

VAT for UK Freelancers Without Filing Surprises

If you want a low-stress approach to **vat for uk freelancers**, start with an HMRC-first baseline. Think of compliance as a series of decisions backed by records, not a setting inside your invoicing tool.