Quick Answer

Freelancers usually keep Tax Court issues remote by maintaining records that clearly show income and expenses, using dedicated business accounts, and saving receipts, invoices, proof of payment, and business-purpose notes. Review your books before each estimated-tax payment, avoid deductions you cannot substantiate, and if a Notice of Deficiency arrives, calendar the petition deadline immediately and protect your filing rights first.

If you work as a business-of-one, autonomy is not just creative freedom or flexible hours. It also means keeping the business financially resilient. For many freelancers, a tax dispute with the IRS is a constant source of anxiety. It pulls attention away from clients and the work itself.

You do not need to become a tax law expert. You do need a business that is clear, organized, and easy to defend if questions come up. This guide lays out a three-stage approach: put clean records in place, run a repeatable review process, and know exactly what to do if a serious notice arrives. The goal is simple: turn compliance from a year-end scramble into an operating discipline that keeps Tax Court remote and manageable.

Stage 1: The Audit-Proof Foundation - Building Your Financial Fortress#

Start with the basics. Tax trouble often begins with ordinary record gaps, not complicated tax strategy. If you want us tax court for freelancers to stay theoretical, fix the setup first.

At this stage, your job is simple: keep records that clearly show income and expenses, and keep support for what you claim. If questions come up, the burden of proof is on you.

The four controls to put in place first#

| Control | Prevents | Creates if questioned |

|---|---|---|

| Separate business identity | Blurred lines between you and the business | A clearer ownership and structure record for your business activity |

| Dedicated banking | Commingling that makes records harder to trust | A cleaner transaction trail that matches your books |

| Accounting system | Uncategorized transactions, missed income, and year-end guesswork | A usable ledger tied to account activity |

| Substantiation vault | Unsupported deductions and confusion between business and personal costs | Documentary evidence that supports the claim |

- Separate business identity

Decide whether you are operating as a sole proprietor, which is the default if you do business without registering another structure, or forming an LLC. The point is to reduce blurred lines and create a clearer ownership and structure record if questions come up.

- Dedicated banking

Route business income and business spending through business accounts instead of mixing them with personal spending. This reduces commingling and gives you a cleaner transaction trail that matches your books. (Separate accounts are a strong recordkeeping practice, not a universal legal mandate.)

- Accounting system

Use a consistent method, whether software or another system, that clearly shows income and expenses. This reduces uncategorized transactions, missed income, and year-end guesswork, and leaves you with a usable ledger tied to account activity.

- Substantiation vault

For each deductible expense, keep the receipt or invoice plus core details such as amount, date, place, and essential character. For mixed-use costs, note the business and personal split when the expense happens. This reduces unsupported deductions and confusion between business and personal costs. For category-specific documentation rules, verify the current requirements before relying on a simplified standard.

Choose your entity on purpose#

Choose an entity for clarity, not because it sounds more sophisticated. A simple way to decide is:

- Stay sole proprietor for now if you are testing a low-risk business idea.

- Move to LLC if you want a more formal entity structure, knowing a single-member LLC is usually treated as a disregarded entity for federal income tax unless you make an election.

- Escalate to a tax or legal professional before filing if liability exposure is rising or you are considering tax elections.

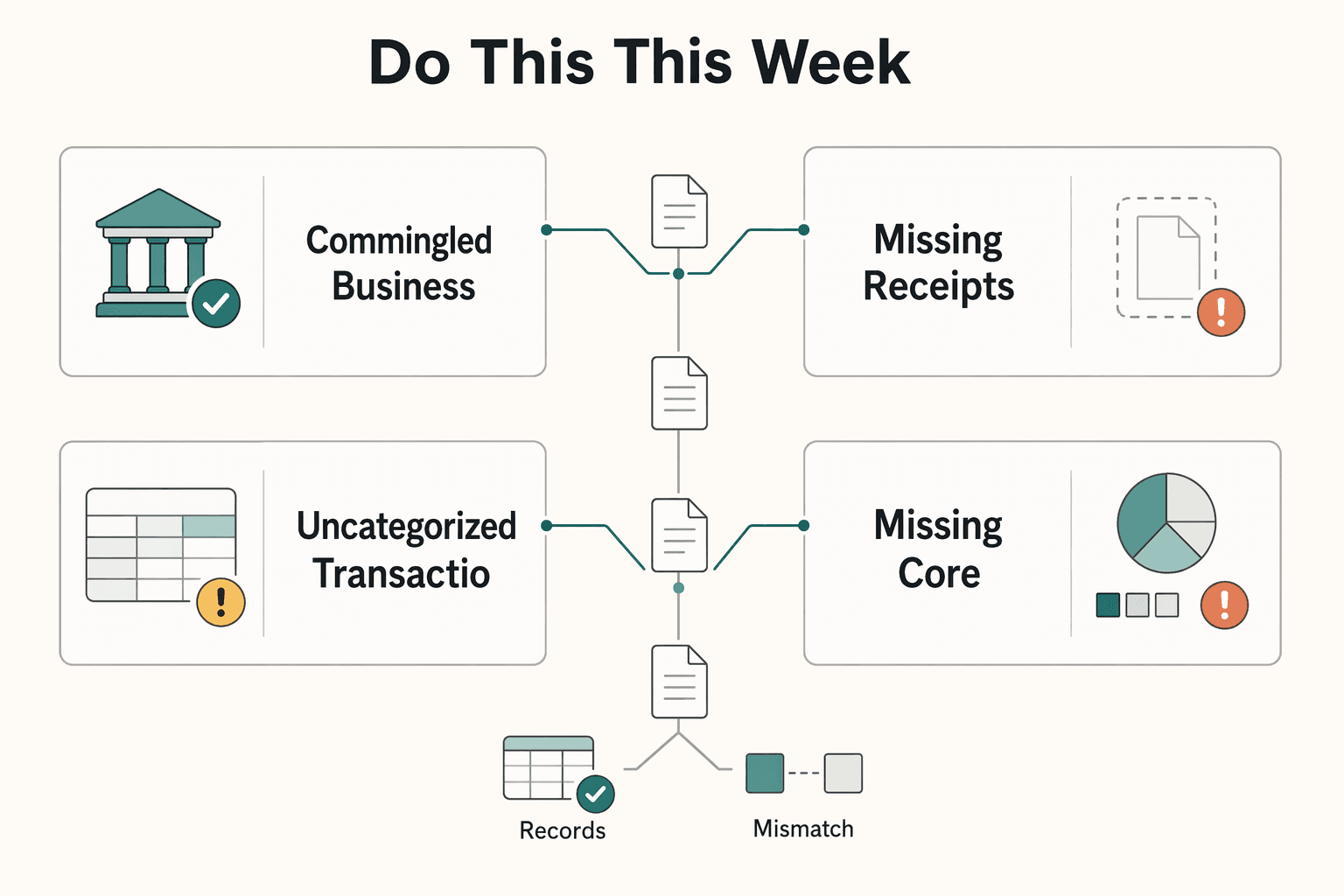

Do this this week#

For most freelancers, this is the shortest path to a setup you can defend:

- Open business banking and route client income and business expenses there.

- Create a short chart of accounts, for example: income, software, contractors, travel, meals, supplies, professional fees.

- Start document capture: keep the receipt or invoice with key expense details.

- Add mixed-use allocation notes when the expense happens.

- Run a monthly reconciliation cadence as an operating control, not an IRS-required frequency.

| Common mistake | Preventive control | Audit-defense value |

|---|---|---|

| Commingled business and personal spending | Dedicated banking | Clearer separation of transaction activity |

| Missing receipts or invoices | Substantiation vault | Documentary support for key expense details |

| Uncategorized transactions | Accounting system | Records that clearly show income and expenses |

| Missing core expense details | Substantiation vault | Stronger support for expense substantiation |

Get these controls working now, and the later stages become much easier. Record gaps can create disputes even when the tax issues themselves are straightforward.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Stage 2: Neutralizing Threat Vectors - Your Active Defense System#

Once the foundation is in place, the next job is consistency. Your active defense system is a repeatable review rhythm, not a one-time setup.

To make disputes less likely and easier to defend, record transactions while they are fresh, review before each estimated-tax payment, and avoid deductions you cannot substantiate. If a position is challenged later, the burden of proof is still on you.

SOP 1. Quarterly estimated tax review#

Estimated tax is how you pay income tax and self-employment-related taxes when no employer is withholding. Because the U.S. system is pay-as-you-go, waiting until filing season can create underpayment risk even if your annual return is otherwise accurate. Run the same three-step process each cycle:

| Step | Action | What to keep |

|---|---|---|

| Review | Pull your year-to-date P&L, prior-year return, and Form 1040-ES materials; confirm that business deposits and payout activity match booked income; clear uncategorized or duplicate entries | Year-to-date P&L, prior-year return, and Form 1040-ES materials |

| Reconcile | Match major expense categories to receipts or invoices and proof of payment; compare your tax-reserve cash to your expected liability | Receipts or invoices and proof of payment |

| Pay | Submit payment, save the confirmation, and store it with that cycle's calculation note; schedule the next cycle using the current estimated-tax payment calendar | Payment confirmation and that cycle's calculation note |

If income is steady, making four equal payments is generally the default to reduce penalty risk. If income is uneven, evaluate whether the annualized installment method is a better fit. Keep penalty guardrails in view, for example common Topic 306 tests like the $1,000 threshold and 90% and 100% tests. Still, do not let those guardrails replace a current-year reality check.

SOP 2. The ordinary and necessary screen#

The safest time to test deductibility is before you book the expense. Use this screen: can you show the expense is ordinary, meaning common and accepted in your industry, and necessary, meaning helpful and appropriate, even if not indispensable? For ambiguous expenses, ask:

- Would another freelancer in your field recognize this as a normal business cost?

- Can you tie it to a client, project, deliverable, or revenue activity?

- Would your file clearly show a business reason later, not just personal preference?

If any answer is weak, treat the item as personal or mixed-use until you have stronger support.

A short same-day note can help. Keep it simple:

- Business purpose: what the purchase was for

- Client or project link: which engagement or internal activity it supported

- Expected business benefit: what result you expected

Pair that note with the core records: payee, amount, proof of payment, date, and what was purchased or received. Recording it the same day is the safer default.

SOP 3. No-value labor confirmation#

Use this control where IRS guidance is explicit: for business-use-of-home repairs, deductible labor excludes your own labor. More generally, keep deduction entries tied to actual amounts paid and documented proof of payment, not internal estimates of what your hours were worth.

| Do | Don't |

|---|---|

| Record third-party invoices you paid and can substantiate (for example, contractor repair invoices) | Book a deduction for your own labor on business-use-of-home repairs |

| Record outside-provider fees with proof of payment and business purpose | Replace third-party payment records with an internal estimate of your time |

| Keep your internal hourly value for pricing and profitability decisions | Put that internal value into tax deduction entries |

This separation matters most where IRS guidance is explicit that deductible repair labor excludes your own labor.

| Red flag | Exact SOP control | Evidence the control should produce |

|---|---|---|

| Estimated payments based on guesswork | SOP 1 quarterly estimated tax review | Current P&L, prior-year return and Form 1040-ES workpapers, payment confirmation, cycle calculation note |

| Large purchase with no clear business rationale | SOP 2 ordinary and necessary screen | Receipt or invoice, proof of payment, dated note with business purpose, client or project link, expected business benefit |

| Mixed personal and business use with no allocation | SOP 2 ordinary and necessary screen plus same-day allocation note | Record showing item, date, amount, and documented business-use split |

| Labor deductions without third-party payment evidence | SOP 3 no-value labor confirmation | Third-party invoices and proof of payment for claimed labor costs; no self-valued labor deduction entries where IRS rules exclude own labor |

For a related recordkeeping angle, see A Guide to 'Making Tax Digital' for UK Freelancers. Before you lock your compliance checklist, map your travel and filing footprint in the Tax Residency Tracker so your records stay consistent year-round.

Stage 3: The Contingency Protocol - Your "In Case of Emergency" Plan#

If a serious notice pushes you toward Tax Court territory, treat it as a deadline problem first. Protect your filing rights before you spend time debating the tax merits.

Lock the trigger and deadline first#

Your first job is to identify the notice and lock the deadline. A Statutory Notice of Deficiency (often called a 90-day letter, including CP3219N) is the trigger. It proposes additional tax and starts your Tax Court petition rights.

| Trigger or deadline | Rule |

|---|---|

| Statutory Notice of Deficiency (90-day letter, including CP3219N) | Proposes additional tax and starts your Tax Court petition rights |

| Petition window if the notice is addressed inside the United States | Generally 90 days from the date shown on the notice |

| Petition window if the notice is addressed outside the United States | Generally 150 days from the date shown on the notice |

| E-file receipt deadline | The Court must receive the petition by 11:59 pm Eastern Time on the last day |

Your petition window is generally 90 days from the date shown on the notice, or 150 days if the notice is addressed to a person outside the United States. That deadline is statutory. The Tax Court cannot extend it, and IRS calls or negotiations do not pause it. If you e-file, the Court must receive the petition by 11:59 pm Eastern Time on the last day.

Once you confirm the notice, do this immediately:

- Read the notice and confirm the tax year, adjustments, and proposed amount.

- Calendar the last filing day the same day you open the notice.

- Create one working folder for the notice, filed return, IRS letters, bookkeeping reports, receipts, invoices, proof of payment, estimated-tax confirmations, and your business-purpose notes.

- Split files into:

- Petition documents: required court forms plus a copy of the IRS notice. - Evidence documents: receipts, tax forms, and supporting records for later stages, not filed with the petition.

- Decide your forum plan before informal back-and-forth with the IRS.

Avoid this common mistake: spending weeks trying to clear it up informally while the 90-day or 150-day clock keeps running.

Choose your forum before you argue facts#

Before you spend energy arguing facts, decide where the dispute belongs. Tax Court is generally a prepayment forum in deficiency disputes, so you can challenge first and pay later. After you file a petition, payment of the underlying tax is ordinarily postponed while the case is pending.

A refund forum works differently: you generally pay first, file a timely refund claim with the IRS, then sue in U.S. District Court or the U.S. Court of Federal Claims.

A practical rule applies here. If you want to dispute the proposed liability without full prepayment, protect the Tax Court deadline first.

Make your case election deliberately#

The right case track depends mainly on the amount in dispute and whether appeal rights matter to you. Your case election is your choice between small tax case and regular case procedure, made on the petition form (paragraph 4 of Form 2).

Small tax case eligibility is tied to the disputed deficiency, including additions to tax and penalties, being $50,000 or less for any one year. Small tax cases are generally less formal and faster, but the decision cannot be appealed.

| Decision factor | Small tax case | Regular case |

|---|---|---|

| Eligibility | Disputed deficiency, additions, and penalties are $50,000 or less for one year | No small-case cap |

| Procedure | Less formal, generally faster | More formal |

| Appeal priority | Decision is final (no appeal) | Appeal rights preserved |

| Cost or time tolerance | Usually lower-friction | Usually more process-heavy |

Use this as a practical screen, not a court scoring test.

Know when to call a pro#

This is where self-help should stop if the facts, stakes, or procedure start to widen. Escalate quickly if any of these apply:

- You received a Statutory Notice of Deficiency and have not filed a petition.

- The amount at stake could materially affect cash flow or settlement posture.

- The notice spans multiple years, penalties, foreign issues, entity issues, or legal positions you cannot explain clearly.

- Your records are incomplete, mixed personal and business, or internally inconsistent.

- You are leaning toward regular case procedure because appeal rights matter.

- Cost is a barrier and you may qualify for a Low Income Taxpayer Clinic.

Keep the role split clear:

- Your job: organize the timeline, facts, and records.

- Counsel's job: legal strategy, petition framing, and court-facing communications.

For a notice-first triage checklist, use How to Handle an IRS Notice of Deficiency (90-Day Letter). Also see A Deep Dive into the UAE's Corporate Tax for Freelancers and LLCs.

Conclusion: From Anxiety to Empowerment#

The point of this framework is not perfection. It is control. Prevention is still your best lever: keep your tax operations clear, current, and documented so disputes are less likely and easier to manage if they do happen.

You already have the structure. Build the foundation with clean separation and organized records. Run recurring SOPs with regular reviews and timely documentation. If tax questions come up, work from complete documents, not memory.

What to do next:

- Consolidate your records into one system and keep periods clearly separated.

- Run one repeatable monthly check on income, expenses, and tax admin items.

- Save support for material positions at the time of the transaction.

- If a tax-related notice or question comes in, centralize related documents in one working file and use your existing process.

Choose the level of support that fits your situation. For legal or tax interpretation, consult a qualified professional.

The practical outcome is straightforward: less compliance stress, better documentation quality, and better preparation if a return position is challenged.

For related reading, see A Guide to Capital Gains Tax for UK Freelancers.

If you want cleaner invoice, payout, and transaction records before a dispute ever starts, contact Gruv to confirm the right setup for your workflow.

Frequently Asked Questions

How can you avoid the us tax court for freelancers?

Keep records that clearly show business income and allowable business expenses. Save receipts, invoices, and proof of payment so deductions are substantiated, and reconcile your return to payer statements, bank records, invoices, and receipts before filing.

What are the biggest IRS audit red flags for freelancers, and what should you do now?

The biggest practical red flags are income you cannot tie to records and deductions you cannot substantiate. Reconcile payer statements to your books before filing, keep support for each income and expense entry, and replace estimates with actual amounts from receipts, statements, or accounting records.

Do you have to pay the IRS before going to Tax Court?

Usually no. In a deficiency dispute, the U.S. Tax Court generally lets you challenge the proposed adjustment before paying the disputed tax after a Notice of Deficiency. You generally have 90 days from the notice date to petition, or 150 days if the notice is addressed to you outside the United States, and the court cannot extend that deadline.

What is the difference between a small case and a regular case in Tax Court?

The main differences are formality, appeal rights, and eligibility. Small tax cases are generally less formal, but the decision is final and cannot be appealed. In deficiency cases, small-case eligibility depends on the disputed deficiency, additions, and penalties being $50,000 or less for one year.

What does “deductible” mean for a freelancer?

A deductible expense is an amount you subtract from income on your return so you do not pay tax on that amount. For freelancers, it must be ordinary and necessary for the business, and you must be able to substantiate what you paid, when you paid it, and the business purpose.

Can you deduct your own labor as a freelancer?

No, not in the home-office context discussed here. In that same context, building-supply costs may be recoverable through depreciation. Keep labor and materials separated in your records so you do not overclaim.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Handle an IRS Notice of Deficiency (90-Day Letter)

Contain first, solve second. Your immediate job is to lock the deadline, identify the exact issue, and assemble a clean packet.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.