Quick Answer

When you are self-employed, benefits are protections you choose and fund yourself, not perks set by an employer. A practical approach is to build an Autonomy Stack: first verify health, disability, and backup protections, then choose retirement mechanics such as a one-participant 401(k) or SEP IRA, and finally pre-fund time off with separate cash buckets for emergencies, PTO, and skill upkeep.

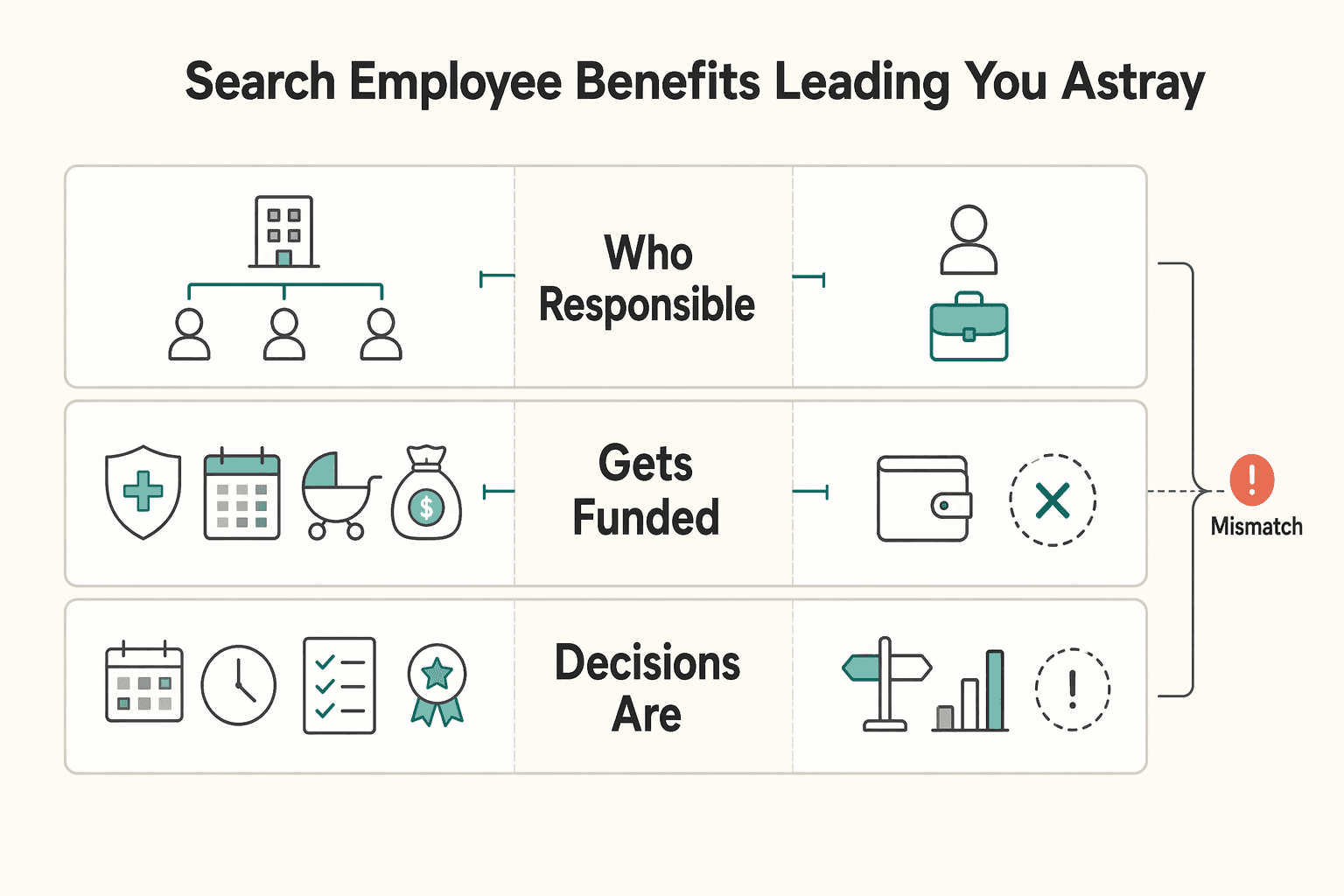

Your Search for "Employee Benefits" Is Leading You Astray#

You are not getting useful answers because guidance on "employee benefits" often assumes an employer-run setup, not a business you run yourself. In that model, the employer defines the role, sets the schedule, and offers extras around the job.

That employee lens is clear in the source material. It shows preset shifts like 9 AM to 5 PM or 11 PM to 7 AM, defined job descriptions, and benefits such as health insurance, paid leave, maternity leave, and performance bonuses. If you are self-employed, the risk is different: if you do not work, or cannot find clients, you do not get paid.

Use this quick filter when you read advice. If it assumes an employer selected the plan, your role is predefined, or time off exists because an employer grants it, it is probably the wrong framework for you.

| Question | Employee benefits mindset | Self-employed safety-net system |

|---|---|---|

| Who is responsible | Employer designs and funds part of the package | You choose, fund, and maintain each protection |

| What gets funded | Salary plus employer-provided extras like health insurance or leave | The protections you decide to fund yourself |

| How decisions are made | Based on what the employer offers | Based on your risks, cash flow, and business priorities |

The practical reframe is simple. Stop asking, "What benefits should I get?" and start asking, "What protections do I need to fund myself?" Here, we call that structure the Autonomy Stack: three working buckets you can build and review over time.

We will follow that order. First protect downside risk, then build retirement mechanics, then fund recovery time so time off does not turn into a revenue shock.

For a step-by-step walkthrough, see How to Hire Your First Employee in Germany.

Pillar 1: The Foundation - Mitigating Catastrophic Risk#

Protect downside risk first. Before you optimize retirement or time off, document the failure points that could interrupt care access, claims payment, or business continuity.

Use this section as an execution pass. Verify documents, capture decisions in writing, and set backups before you move to Pillar 2.

Health coverage#

Start with verification, not labels. If you are using terms like domestic plan, travel policy, and global health plan, treat them as placeholders. The grounding here does not verify exact product definitions, eligibility rules, or coverage limits for private plans.

| Plan label you are evaluating | What to confirm in writing | Common gap to check before purchase |

|---|---|---|

| Domestic plan | Enrollment eligibility, territory, routine and specialist care scope, claims method, provider rules | Brochure language that does not match contract wording |

| Travel policy | Enrollment eligibility, territory, routine and specialist care scope, claims method, provider rules | Assumptions based on category name instead of policy text |

| Global health plan | Enrollment eligibility, territory, routine and specialist care scope, claims method, provider rules | Missing written confirmation on geography or provider access |

A useful process cue comes from FECA Part 3. Its chapter list includes 3-0600 (Requirements for Medical Reports) and 3-0800 (Exclusion of Medical Providers). That supports one practical point: claims workflows depend on documentation quality and provider-status checks. It does not, by itself, establish private-plan rules for self-employed readers.

Action: pick your current best-fit label. Then build a one-page verification sheet listing territory, care scope, claims method, provider rules, and a placeholder for current eligibility and coverage terms after contract review.

Disability coverage#

The grounding here does not verify disability policy definitions, trigger rules, waiting periods, benefit duration, exclusions, or portability terms for self-employed readers. Treat this as a contract-review checklist only until you confirm live policy language.

| Policy term to verify | What to capture from the policy file |

|---|---|

| Definition of disability | Full clause text plus any rider language |

| Benefit trigger | Exact conditions that must be met before payment |

| Waiting period | Contract section that sets the delay before benefits |

| Benefit duration | Clause that defines how long benefits may continue |

| Exclusions | Full limitations and exclusions section, not highlights |

| Portability | Written terms for business-structure or location changes |

Action: request the full policy set, pull these six clauses into your notes, and list unresolved questions for broker or carrier follow-up before you move on.

Single point of failure audit#

A solo operation can still have a weak link that stalls the business faster than expected. The goal here is not perfection. It is making sure one broken dependency does not take everything down with it.

- Identify the dependency: list single points such as client concentration, bank, device, software, login path, or lead source.

- Assess impact: note what breaks in 24 hours, 7 days, and 30 days.

- Assign a backup path: choose a practical fallback for each critical dependency.

- Set review cadence: recheck quarterly and after major revenue, tool, or location changes.

Action: complete one backup action per critical dependency, then move to Pillar 2 only after your downside risks are documented and mitigation steps are active.

If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

Pillar 2: The Growth Engine - The Real 401(k) for a Business-of-One#

Once Pillar 1 is in place, the next priority is steady asset building. For a business of one, the practical choice usually comes down to this: use a one-participant 401(k) when you want contribution flexibility, and use a SEP IRA when you want simpler administration.

Choose the account that fits how your business actually behaves#

A one-participant 401(k) follows regular 401(k) rules for an owner-only business, or owner plus spouse, with contributions possible in both employee and employer roles. A SEP IRA is employer-funded only, which is simpler to run but gives you fewer contribution levers. SEP plans also do not permit elective salary deferrals or catch-up contributions.

| Decision point | SEP IRA | One-participant 401(k) |

|---|---|---|

| Setup complexity | Generally simpler setup and maintenance | Generally more setup and plan administration |

| Contribution mechanics | Employer contributions only | Employee and employer contributions |

| Annual limit | Verify the current annual limit from IRS guidance and the plan document before use | Verify the current annual limit from IRS guidance and the plan document before use |

| Roth availability | No | May include a designated Roth account if the plan allows it |

| Loan flexibility | No participant loans | Loans may be allowed if the plan document permits them |

| Admin burden | Lighter; IRS SEP guidance notes no employer filing requirement | More admin once plan assets reach the Form 5500-EZ filing trigger ($250,000 at year-end) |

Use business stage as the tie-breaker. If cash flow is uneven and you want to contribute in stages, a one-participant 401(k) is usually the better fit. If you want the lightest setup or need late-year establishment flexibility, SEP is often the cleaner choice.

Watch the hiring inflection point. SEP rules require equal-percentage employer contributions for all eligible employees, and that can materially change cost once you add staff. The one-participant 401(k) is for an owner with no employees, or that owner and spouse.

Build your own employer match protocol#

Retirement contributions work better when they follow a rule instead of depending on leftover cash. Pick a repeatable trigger and make the transfer part of how money moves through the business.

- Trigger

Pick one event that always happens, like client payment clearing or your monthly owner-pay transfer.

- Transfer rule

Move a preset amount or formula-based amount on that same day into a dedicated tax-and-retirement holding account.

- Account structure

Keep retirement-destined cash in its own business savings bucket so it does not blend into operating cash.

- Review cadence

Check monthly for consistency, then run a year-end true-up after books and compensation are finalized.

Before you fund anything, verify plan terms directly. Confirm whether a designated Roth account is included, whether loans are allowed, and whether year-end assets are approaching the $250,000 Form 5500-EZ filing trigger.

Expat tax lens#

For U.S. expats, FEIE versus FTC is a planning decision, not a checkbox. Start by confirming whether you are using FEIE, FTC, or a combination by rule, then map retirement contributions to that tax posture.

| Topic | What the article says | Boundary |

|---|---|---|

| FEIE posture | Start by confirming whether you are using FEIE, FTC, or a combination by rule | Do not assume excluded income is always contribution-eligible across account types |

| Physical presence test | FEIE eligibility can depend on tests such as physical presence | 330 full days in a 12-month period |

| FTC | The IRS generally requires Form 1116, with limited exceptions | You cannot claim a foreign tax credit for taxes on income you exclude |

| IRA calculations | IRS guidance says excluded FEIE and housing amounts are added back | Used when determining compensation for IRA limits |

If you claim FEIE, do not assume excluded income is always contribution-eligible across account types. FEIE eligibility can depend on tests such as physical presence, with 330 full days in a 12-month period. Verify the applicable income threshold from IRS guidance or adviser records before use.

If you use FTC, the IRS generally requires Form 1116, with limited exceptions. Keep this boundary clear: you cannot claim a foreign tax credit for taxes on income you exclude. For IRA calculations, IRS guidance says excluded FEIE and housing amounts are added back when determining compensation for IRA limits.

Common mistakes to avoid#

The errors here are usually procedural, not conceptual. People pick a reasonable account, then get tripped up by timing, plan features, or assumptions carried over from a different setup.

| Mistake | What it involves |

|---|---|

| Missing setup timing | Assuming all plans use the same deadline |

| SEP timing | Forgetting that SEP can be established up to the business return due date, including extensions |

| 401(k) adoption timing | Assuming post-year-end section 401(k) adoption timing applies the same way to every entity type |

| Cash handling | Contributing inconsistently because retirement cash was never separated from operating cash |

| Plan features | Assuming every one-participant 401(k) includes Roth or loan features without checking the plan document |

| FEIE assumptions | Assuming FEIE-excluded income is always contribution-eligible |

For more on plan selection, see A Guide to Choosing a 401(k) Investment Plan.

If you are deciding how much taxable earned income to preserve for retirement contributions, run a quick scenario in the FEIE calculator.

Pillar 3: The Resilience Fund - Architecting Paid Time Off#

Your resilience plan is simple: if you are not billing, your system should still carry you. Paid time off is usually something you fund yourself, since federal law does not require paid vacation, paid sick leave, or paid holidays, and FMLA leave is unpaid for covered employees. Use this funding order so you are not guessing:

- Stabilize your War Chest (cash buffer for shocks and payment gaps).

- Fund your PTO Sinking Fund (planned non-billing time).

- Fund your Sharpen the Saw Fund (skill upkeep tied to current work).

| Fund | Purpose | How to set the target | Where to hold it | Review trigger |

|---|---|---|---|---|

| PTO Sinking Fund | Replace income during planned time off | Planned non-billing days x required daily owner draw + ongoing essential business overhead. Verify any target range you use if you price PTO into rates. | Separate business savings or MMDA at an FDIC-insured bank | When pricing changes, workload shifts, or leave is scheduled |

| War Chest | Cover unplanned expenses and income interruptions | Start from essential personal + business expenses and build toward a target you have verified for your situation. | High-liquidity deposit account, separate from operating cash | Monthly until stable, then quarterly |

| Sharpen the Saw Fund | Pay for education that maintains or improves current-work skills | Budget known renewals, courses, and conferences tied to present services. Verify any target range you use if you apply a revenue formula. | Dedicated savings subaccount or reserve bucket | Before renewals, registrations, and annual planning |

Fund in the right order#

Start with the War Chest. Emergency savings are for unplanned bills and financial shocks, not routine monthly spending, so this bucket protects decision-making when cash flow slips.

Keep reserve cash clearly separate from operating cash. For storage, use liquid deposit accounts at an FDIC-insured bank when you want deposit insurance coverage, up to $250,000 per depositor, per insured bank, per ownership category. Keep the product type straight. A bank money market deposit account is a deposit product, while a money market mutual fund is an investment product and is not FDIC-insured.

Build the PTO Sinking Fund like a real operating cost#

Treat PTO as a planned business expense, not leftover cash. Set a target from planned time off plus the pay and essential overhead that continue while you are away.

Use realistic averages if your revenue is uneven. Then keep PTO funds in a separate bucket so they are not consumed by taxes, equipment, or short-term dips.

Use the Sharpen the Saw Fund with tax rules in mind#

Use this fund for skill-building that supports your current work. For self-employed readers, education expenses may be deductible when they maintain or improve skills needed in present work, and qualifying amounts are reported on Schedule C.

| Scenario | Treatment stated | Detail |

|---|---|---|

| Education that maintains or improves skills needed in present work | May be deductible | Qualifying amounts are reported on Schedule C |

| Education that is part of qualifying for a new trade or business | Does not meet this rule | Do not assume all training qualifies |

| Travel where the trip is primarily vacation | Trip cost is personal | Only business-related costs at the destination may still be deductible |

Do not assume all training qualifies. If education is part of qualifying for a new trade or business, it does not meet this rule. For travel, if the trip is primarily vacation, the trip cost is personal. Only business-related costs at the destination may still be deductible.

Implementation checklist for this week#

The point of this step is to get the buckets live, even if the starting amounts are modest. Once the structure exists, it is much easier to adjust targets and automate funding.

- Create or label three separate buckets: War Chest, PTO Sinking Fund, Sharpen the Saw Fund.

- Verify each account type and institution, especially where you expect FDIC deposit coverage.

- Calculate one target per bucket using your actual expenses, planned time off, and known education costs.

- Set one automatic transfer per bucket, even at a modest starting amount.

- Set a monthly review date and a quarterly PTO-pricing check.

Once these buckets are live, the edge cases get easier to handle. The FAQ covers those next. Related: A Deep Dive into FinCEN's Beneficial Ownership Information (BOI) Reporting.

Conclusion: You're a CEO. Build Your Safety Net Accordingly.#

Treat your benefits like part of how you run the business, not a perk. The Autonomy Stack gives you three outcomes you should be able to verify at any time.

- Protection is in place. Your coverage is active, usable for your real care pattern, and documented if you claim the self-employed health insurance deduction (Form 7206; Schedule 1 (Form 1040), line 17).

- Retirement is active. If you use a one-participant 401(k), run it intentionally in both your employee and employer roles, track earned-income-based contribution calculations, and stay on top of admin triggers such as the $250,000 Form 5500-EZ filing threshold.

- Resilience funds are operational. Keep emergency reserves and operating cash in separate buckets. If you pre-fund time off, keep that separate too, and use automatic transfers so the plan keeps working when revenue timing gets messy.

Next step: write a short benefits policy, match it to your account structure, and define the contribution process you will run every time revenue arrives. If you live abroad, validate setup and contribution decisions against current IRS treatment before execution, including FEIE rules and the latest Pub. 54 updates. The goal is lower volatility, better decisions under pressure, and stronger long-term control.

We covered this in detail in How to Offer Competitive Benefits to a Global Team of Contractors.

Before you finalize your autonomy stack, use the Gruv tools hub to turn health, retirement, and PTO decisions into a working operating plan.

Frequently Asked Questions

How do you get health insurance when you work for yourself?

You get health coverage by verifying plan terms directly rather than relying on labels like domestic plan, travel policy, or global health plan. Before enrolling, confirm eligibility, territory, routine and specialist care scope, claims method, provider rules, and the current contract terms in writing.

What is the closest thing to a 401(k) if you are self-employed?

A one-participant 401(k) is the self-employed version of a regular 401(k) for an owner-only business, or owner plus spouse. The article also presents a SEP IRA as another common option, but says you should verify current IRS rules and provider requirements before opening or funding either plan.

How do you create a PTO policy for yourself?

Create your own PTO policy by treating time off as a funded business expense. Set a PTO Sinking Fund target from planned non-billing days, required daily owner draw, and essential business overhead, and keep that cash separate from operating funds.

What is the right retirement approach if you are a U.S. expat freelancer?

The right approach starts with your tax posture: confirm whether you are using FEIE, FTC, or a combination by rule, then map retirement contributions to that setup. If you claim FEIE, do not assume excluded income is always contribution-eligible across account types. If you are using the physical presence test, it requires 330 full days in a 12-month period.

How do you budget for benefits when your income is irregular?

Budget for benefits with rules and separate buckets, not leftover cash. Use dedicated buckets for retirement, a War Chest, planned time off, and skill upkeep, and recheck your assumptions as revenue changes.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

Choose Your 401(k) Investment Plan in 30 Minutes

Treat this as a cash flow and behavior decision first, and a fund-picking exercise second. The goal is to help you make a workable choice from a real plan menu without guessing, chasing what is hot, or changing course every time markets move.