Quick Answer

For a small international business with related entities, transfer pricing mainly means documenting each related-party charge as it happens, using the most reliable method you can support, and keeping the file ready before filing. Keep the agreement, invoice, payment or accrual trail, ledger support, and a short method memo aligned. Get specialist help if facts change, IP or risk shifts, losses persist, or you cannot produce a complete file promptly.

The Solopreneur's Guide to Transfer Pricing: Protecting Your Global Business Structure#

For a business of one operating across related entities, transfer pricing is mostly about execution. Document each related-party charge when it happens, choose the most reliable method you can actually support, and have the file ready before you file your return. If you wait until year-end, the evidence can be harder to rebuild and your method support can be easier to challenge.

This is not about producing a long, polished report. Your goal is an arm's-length result supported by what each entity actually did, what assets were used, what risks were borne, and who received the benefit.

That means treating transfer pricing as part of how you run the relationship between entities, not as a memo written after the fact. When the agreement, invoice, payment trail, and books all line up while the transaction is still fresh, the support is usually straightforward. If you wait and try to reconstruct the story from memory, even routine charges can start to look uncertain.

Build the transaction map first#

Start with a live transaction map as soon as one entity charges another. Get the facts on paper before you argue about method.

For each line, record enough detail that another person could follow the file without relying on your memory. Include the parties, what was transferred, what each side actually did, who benefited, the governing agreement, the pricing logic, invoice timing, payment status, and where the support sits. If a line says only "management services" or "support fee," it is often too vague.

Use this control test: can you trace a single charge from the agreement to the invoice, to payment, to the ledger entry, to the method memo? If not, the file is not ready.

| Area | Minimum viable control | Stronger control |

|---|---|---|

| Transaction inventory | One row per related-party charge with date, parties, description, amount, and agreement reference | Add who performed key functions, who bore risk, who benefited, billing cadence, and support-folder link |

| Pricing support | Short memo stating the selected method and why it fits the facts | Add comparable-data search notes, rejected alternatives, and key assumptions |

| Evidence pack | Signed agreement, invoice, proof of payment, and ledger tie-out | Add time records, cost-allocation workpapers, scope-change approvals, and a year-end refresh note |

| Review cadence | Review before return filing | Quarterly review plus trigger reviews when facts change midyear |

A live map works best when it is detailed enough to answer basic review questions without forcing you to open five folders just to understand one line. If a charge recurs, keep the row stable and refresh the fields that changed, such as amount, invoice date, payment status, or support link. If the nature of the work changed, treat that as a new fact pattern instead of quietly rolling it into an old description.

It also helps to write descriptions in plain operating language. "Content editing performed by Entity A for Entity B website operations" is easier to defend than "admin support." The point is not style. The point is that the description should let a reviewer see what happened, why one entity paid, and how that lines up with the agreement and books.

People often lose control not in the spreadsheet itself but in the gaps around it. A row may reference an agreement that was never finalized, an invoice that uses different wording, or a payment that cleared through a different account than expected. The map should expose those gaps early enough that you can fix them while the facts are still easy to verify.

Keep legal labels aligned with actual conduct. If the documents say one entity provides routine support but real control and risk sit elsewhere, the file has already drifted from economic substance.

Choose the method you can defend, not the one that sounds smartest#

Once the transaction map is clear, method selection becomes a reliability question. Use the best method rule as your standard. Pick the method that gives the most reliable arm's-length result based on the data and methods actually available to you. This is about fit, not complexity.

| Fact pattern | Response | Article note |

|---|---|---|

| You have a truly comparable third-party price | Use a price-based approach | It may be easier to defend. |

| External pricing is weak, but one entity provides routine services and you can support the cost base | Use a cost-based approach | It may be more workable. |

| Functions, assets, and risks are still unclear | Do not pick a method yet | Resolve that before picking a method. |

| Facts changed during the year | Re-test the selected method | The selected method has to fit the facts that actually existed when the charges were made. |

Use four questions:

- How strong is comparability?

- What usable data do you have now?

- Can you apply this consistently during the year?

- Can you defend it with evidence, not assertions?

If you have a truly comparable third-party price, a price-based approach may be easier to defend. If external pricing is weak but one entity provides routine services and you can support the cost base, a cost-based approach may be more workable. Do not choose a method first and then force the facts into it.

A practical way to make this decision is to compare the method against the evidence pack you can actually assemble. If your support depends on clean cost records, test the cost records before you commit to the method. If your support depends on comparability, make sure the comparability analysis is something you can explain without hand-waving. A method is only as defensible as the data underneath it.

Common failure points include inaccurate inputs and a weak information search. If the cost base is wrong, time records do not tie out, or material facts were not adequately considered, the documentation can still fail even if the memo looks complete.

Another common mistake is mixing facts from different periods. You may choose a method based on how the entities worked at the start of the year and then leave it untouched after the work moved, the customer relationship shifted, or the invoicing flow changed. That is not a drafting problem. It is a reliability problem. The selected method has to fit the facts that actually existed when the charges were made.

When you test a method, ask yourself what an examiner or reviewer would attack first. Would they question the cost pool? The benefit received? The assumption that a routine service was really routine? The answer usually tells you where to strengthen the file. Sometimes the right move is not to write more. It is to fix the underlying evidence, update the description of the transaction, or stop using a method that no longer fits.

If functions, assets, and risks are still unclear, stop there and resolve that before picking a method. For a practical walkthrough, use How to Conduct a Functional Analysis for Transfer Pricing.

Keep the file ready before filing#

Timing is a real control point, not an administrative detail. For U.S. taxpayers, with certain exceptions, documentation must exist when the return is filed. You must also be able to provide it within 30 days if requested during examination. If the relevant Section 482 adjustment thresholds are met, avoiding the net adjustment penalty generally depends on satisfying these documentation requirements.

| Item | What to confirm | Common breakpoint |

|---|---|---|

| Timing | Documentation exists when the return is filed and can be provided within 30 days if requested during examination | Waiting for a year-end cleanup turns the package into a reconstruction task |

| Core file | Keep the agreement, method memo, invoices, proof of payment, ledger support, and calculation workpapers together | Invoice descriptions do not match the agreement |

| Description check | The transaction description is consistent across the agreement, invoice, and ledger | An invoice says "advisory support" while the agreement says "software services" |

| Amount check | The amount in the workpaper matches the amount billed | The books show an accrual but the support folder only contains bank records |

| Method check | The method memo still fits the year-end facts rather than outdated assumptions | The memo refers to one entity as bearing risk even though the year-end conduct shows something else |

Treat that as the core of the Section 6662(e) documentation requirements: reasonably select and apply a method, maintain sufficient documentation, and furnish it promptly. Documentation rules are similar, but not identical, between specified and unspecified methods.

Keep the principal documents together in one place: the agreement, method memo, invoices, proof of payment, ledger support, and calculation workpapers. Common breakpoints are often simple ones, such as invoice descriptions that do not match the agreement or invoices with no payment evidence.

The easiest way to stay ready is to build the file as each charge happens instead of waiting for a year-end cleanup. That does not mean writing a long memo each time. It means making sure the agreement or written terms are settled, the invoice language matches those terms, the payment or accrual trail is captured, and the workpaper supporting the charge is saved where the transaction map points to it. If you do that consistently, the filing-time package is mostly a review task rather than a reconstruction task.

Before filing, run a short verification pass on each material line:

- confirm the transaction description is consistent across the agreement, invoice, and ledger

- confirm the amount in the workpaper matches the amount billed

- confirm the billed amount ties to payment or accrual support

- confirm the method memo still fits the year-end facts rather than outdated assumptions

That review often catches the most avoidable problems. Maybe an invoice says "advisory support" while the agreement says "software services." Maybe the books show an accrual but the support folder only contains bank records. Maybe the memo refers to one entity as bearing risk even though the year-end conduct shows something else. None of those issues are hard to fix when you find them early, but they become much harder once the return is filed and the file is expected to be complete.

Documentation by itself does not guarantee penalty protection. The file still has to be reasonable and adequate based on how you selected and applied the method, and an unreasonable method selection or application can still fail penalty protection. If you operate outside the U.S., keep local filing-time documentation requirements in a pending column until each item has been verified against current local rules and the source or official records you will use to support it.

Know when to stop DIY#

A common DIY problem is that the facts change but the pricing does not. Escalate before the next billing cycle when the structure shifts or timing risk appears.

| Trigger | What happened | Guidance |

|---|---|---|

| IP or intangible charges | You move or license IP, or begin charging for brand, software, content, or know-how | Get specialist support before filing |

| Reorganization | You reorganize customer contracting, employment structure, or risk ownership | Escalate before the next billing cycle |

| Persistent losses | One entity has persistent losses while another captures upside | Get specialist support |

| Authority contact or file gap | A tax authority contacts you, or you cannot produce a complete file within 30 days | Get specialist support |

| Method change | You need to change method midyear because facts changed | Pause the pricing change, preserve the drafts and approvals, and get advice before filing |

Get specialist support if any of these occur:

- You move or license IP, or begin charging for brand, software, content, or know-how.

- You reorganize customer contracting, employment structure, or risk ownership.

- One entity has persistent losses while another captures upside.

- A tax authority contacts you, or you cannot produce a complete file within 30 days.

- You need to change method midyear because facts changed.

If one of those triggers appears, pause the pricing change, preserve the drafts and approvals that explain the business change, and get advice before filing.

The handoff goes better if you organize the file before asking for help. A specialist usually needs the transaction map, current agreements or written terms, invoices, payment support, ledger extracts, method notes, and a dated explanation of what changed. If you give them a clean chronology instead of a pile of disconnected files, they can focus on the risk issue rather than spending time reconstructing the basic record.

It also helps to separate routine cleanup from structural change. If one invoice description is sloppy, fix the invoice process. If work, control, or risk moved to a different entity, that is no longer a small admin repair. It affects the pricing logic itself, and that is exactly where DIY tends to stop being efficient.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025. If you need a cleaner paper trail for related-party charges, use the Free Invoice Generator to standardize invoice detail before filing.

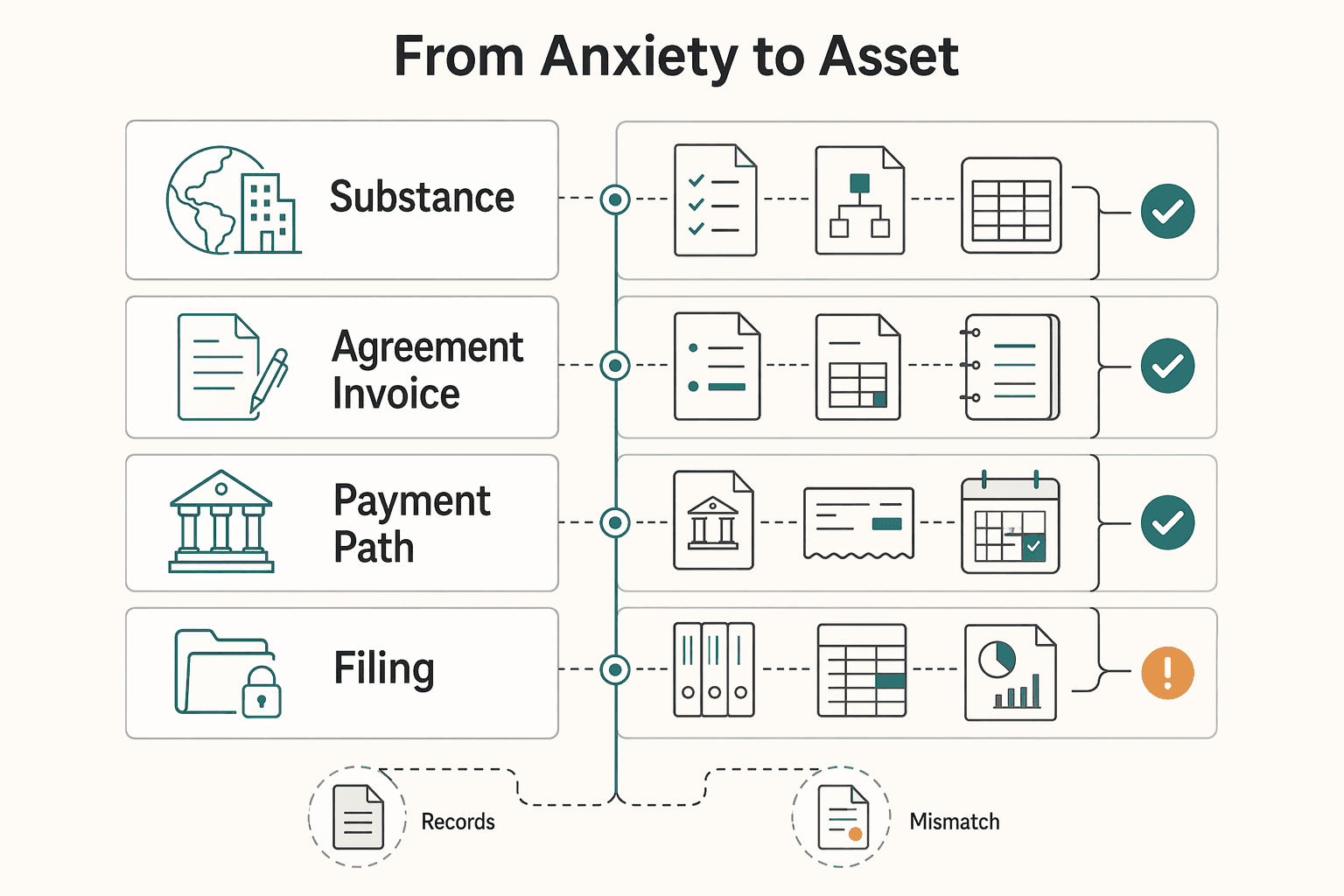

From Anxiety to Asset#

The work gets manageable once you treat transfer pricing as an operating control on every related-party charge, not a year-end cleanup. The practical goal is straightforward: make each transaction traceable from real conduct to the tax position you file. Use the same cycle every time:

- Confirm substance: who performed the work, who benefited, and whether current conduct still matches your documented charge rationale.

- Align agreement and invoice: make sure both describe the same service, goods, or charge.

- Verify payment path: tie the invoice to either cash movement or accrued entry, then to the ledger.

- Archive support: keep one file that an informed reviewer can follow on its own.

That file should typically include written terms, the invoice, proof of payment or accrual entry, a ledger tie-out, and a short pricing memo. As a control check, match one line item word for word across the agreement, invoice, bank or accrual record, and ledger description. In practice, a common breakdown is missing or misfiled receipts, contracts, or transaction records.

| Control point | Routine maintenance | Escalate when |

|---|---|---|

| Substance | Confirm who performed, who benefited, and what changed since the last charge | Functions, risks, or entity roles changed and the existing logic no longer fits |

| Agreement and invoice | Match service description, pricing basis, and invoicing terms | Agreement language and actual conduct diverge |

| Payment path | Trace invoice to cash or accrual and then to ledger posting | Cash, accruals, and books do not reconcile |

| Filing scope and archive | Keep one traceable file and review U.S. reporting scope early | Filing scope is unclear or penalty risk is increasing |

What makes this manageable is repetition. Use the same file structure, the same naming logic, and the same review questions each time a related-party charge is created. The more standardized your process is, the less likely you are to miss one support item that later turns into a filing problem.

A good archive should let someone else answer a basic chain of questions without contacting you. What happened? Why was there a charge? How was the amount determined? Where is the agreement? Where is the invoice? Where is the payment or accrual evidence? Where does it hit the books? If the answer to any of those depends on your memory, the archive is not finished.

If U.S. filing could apply, review the Form 5472 instructions (12/2024) early. That includes Who Must File, foreign-owned U.S. DEs, Accrued Payments and Receipts, Record Maintenance Requirements, and Penalties for failure to file Form 5472. Do not guess on scope, including 25% foreign-owned fact patterns. Do not include a penalty dollar amount unless the current amount has been verified in the latest instructions.

If the risk is now structural or the filing scope is uncertain, get specialist support before filing. If your main issue is entity design, start with How to Choose a Jurisdiction for Your European Subsidiary. Related: How to Get a German Tax ID (Steuernummer and Identifikationsnummer).

If your setup now involves structural changes across entities or countries, contact Gruv to validate a compliant operating workflow for your case.

Frequently Asked Questions

Do I need transfer pricing if I am the only worker?

Likely yes if your related entities transact with each other. Headcount alone does not remove documentation expectations. For U.S. taxpayers, with limited exceptions, documentation should exist when the return is filed and be ready within 30 days if requested.

What does arm's length mean in plain English?

It means your entities should price and behave as unrelated parties would under comparable facts. In practice, use the best method rule and support why your selected method is the most reliable measure given your data. If you cannot clearly explain the functions, assets, risks, or who benefited, resolve that first.

What counts as a good-enough file if my budget is small?

For U.S. taxpayers, with limited exceptions, documentation should exist when you file and be producible within 30 days if requested. If non-U.S. rules are in scope, confirm local timing before relying on any deadline. For routine related-party services, a minimum viable file is written terms, charge support in your books, and a short method explanation. Add time or cost support and a brief functional analysis when needed, and escalate if the file does not align with the books or you cannot support the cost base, benefit, or method choice.

Does documentation automatically protect me from penalties?

No. Documentation alone does not automatically protect you, because adequacy and reasonableness still control the outcome. You still need to select and apply the method reasonably, keep sufficient support, and be ready to furnish it promptly. A neat folder is not enough if the assumptions or inputs are wrong.

What should an intercompany agreement say?

An intercompany agreement should match actual conduct, not just read well. It should make clear what was provided, who benefited, and how the pricing method was applied. If the agreement language and real behavior diverge during the year, that is the point to escalate.

When does DIY stop being reasonable?

DIY usually stops being reasonable when timing or method-governance risk appears. Escalate if you are under examination, cannot produce a complete file within 30 days of request, need to change method, or cannot support that your method remains the most reliable given the facts. Build a dated chronology of what changed, when it changed, and which documents support each change.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-45/subtitle-A/subchapter-C/par...trusted

- elibrary.imf.org/view/journals/001/1992/077/article-A001-en.xmltrusted

- irs.gov/businesses/international-businesses/transfer...trusted

- irs.gov/instructions/i5472trusted

- jec.senate.gov/reports/85th%20Congress/The%20Relationship%2...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- pa.gov/agencies/revenue/forms-and-publications/pa-p...trusted

- uscc.gov/sites/default/files/2025-11/2025_Annual_Repo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Choose a Jurisdiction for Your European Subsidiary

Pick your European subsidiary jurisdiction as an operating decision first, then map VAT administration around that choice. The aim is simple: one primary incorporation country and one fallback you can activate without restarting discovery. If your fallback depends on Estonia setup speed, map banking steps in [How to Open a Business Bank Account for Your Estonian Company](/blog/estonian-company-bank-account).

How to Get a German Tax ID as a Freelancer Without Mix-Ups

Define the task before you open any form. In Germany, mix-ups usually start when a request goes out for the wrong number type or to the wrong office.