Quick Answer

Start with the treaty in force for your country pair, not model labels. In an un model tax convention vs oecd comparison, use the models to triage risk, then confirm whether wording around technical services, service PE, or royalty elements can change withholding and filings. Before signing, lock net-pay mechanics, separate services from license rights, and keep residency proof plus a day-by-country log. If the client cannot show a clear withholding basis, pause pricing and escalate before the first invoice.

A Global Professional's Guide to the UN vs. OECD Tax Models: De-Risking Your International Contracts#

If you invoice a foreign client, start with one question: can the client's country tax your fee at source? The answer changes your expected net pay, your contract terms, and how much compliance work follows.

Use this rule throughout. The UN Model and OECD Model are directional templates, not the enforceable rulebook for your engagement. Your outcome comes from the treaty in force for your country pair and how it is applied locally. Both models are widely used in treaty practice, but neither one decides your case on its own.

| Practical cue | UN model direction | OECD model direction | What to verify next |

|---|---|---|---|

| Core posture | Generally preserves greater source-country taxing rights | Different balance that can diverge from the UN approach in important areas | Read the signed bilateral treaty text |

| Real-world use | More often relied on by developing countries | Used by OECD members and non-members as a basis for negotiating, applying, and interpreting treaties | Do not infer the result from country reputation alone |

| Current text status | Published UN Model edition: 2021 | OECD Model updated in 2025 (approved on 18 November 2025) | Check whether current local guidance reflects later commentary or updates |

Treat "UN-leaning" or "OECD-leaning" as an early signal, not a conclusion. Before you price or sign, verify the treaty in force for your country pair and test your facts against that text. Skipping that step is how avoidable payment and compliance surprises show up later.

How to use this guide#

Work through the next three steps in order: classify treaty posture, map exposure, then build contract protection before signature. For a broader refresher on treaty basics and residency decisions, see our digital nomad tax guide.

| Step | Focus | What to confirm |

|---|---|---|

| Step 1 | Classify treaty posture | Confirm the treaty in force and whether it lets the client's country tax this payment type, or mostly reserves taxing rights to your residence country unless local taxable presence is triggered |

| Step 2 | Map exposure | Turn services withholding, Service PE exposure, and royalty reclassification into a clear trigger, likely impact, and immediate next action before the first invoice |

| Step 3 | Build contract protection | Document net-pay terms, fee classification, and treaty-plus-local implementation checks before signature |

Step 1: The Litmus Test - Is Your Client in an OECD or UN-Leaning Country?#

Country labels help you frame the issue, but they do not answer it. Before you price or send a proposal, confirm the treaty in force. Then answer one practical question: does that treaty let the client's country tax this payment type, or does it mostly reserve taxing rights to your residence country unless local taxable presence is triggered?

That treaty-first check controls the risk. "OECD-leaning" or "UN-leaning" tells you where to look, but your outcome still depends on the signed treaty text in force and how your fee is classified. If you want a quick refresher on country-pair treaty context, see how freelancers can legally avoid double taxation with tax treaties.

Your pre-proposal checklist#

Use this sequence before you quote net numbers.

- Confirm treaty status first. Verify that a treaty is in force for your country pair using an official competent-authority or government source.

- Flag the clauses tied to your deal. Check wording relevant to services, royalty or license elements, and PE-style exposure where activity could create local tax obligations.

- Classify friction before pricing. If source-country taxing rights appear limited on your facts, treat the deal as lower-friction. If the wording could support source taxation, withholding, or local filing exposure, treat it as elevated-friction until your terms and pricing reflect that risk.

| Decision cue | Lower-friction read | Elevated-friction read | What to verify before pricing |

|---|---|---|---|

| Treaty status | Treaty in force and clearly usable for your country pair | No treaty found, status unclear, or text version uncertain | Confirm current status from an official source and save the record |

| Services income | No clear clause supporting source-country taxation for this fee type on current facts | Clause language may support source-country taxation for service fees | Record the exact article and test facts against local implementation |

| Royalty or license element | Scope is supportably services-only | Deliverables or rights language could be read as royalty or license income | Separate service scope from IP rights and re-check treaty wording |

| Local presence risk | Facts do not indicate local taxable presence | Travel, on-site work, repeated visits, or local personnel may create PE-style exposure | Confirm who will be where, for how long, and whether subcontractors affect the analysis |

Before you move to Step 2, capture the evidence while it is still fresh: treaty article notes, an assumption log for fee classification, and your initial withholding view. If treaty status or classification is uncertain, keep the deal in elevated-friction mode until the contract language and pricing catch up.

Step 2: Pinpoint the Hidden Risks to Your Cash Flow and Compliance#

In elevated-friction deals, the real exposure often comes through three routes: services withholding, Service PE exposure, or royalty reclassification. Your job in Step 2 is to turn each one into a clear trigger, likely impact, and immediate next action before the first invoice goes out. If a trigger appears, do not quote a clean net number until the treaty text, local implementation, and role ownership are clear.

Use the UN and OECD models as a triage pattern, not the answer. Countries use model texts as starting points in negotiation, and those texts change over time. That includes the OECD update approved on 18 November 2025, with revised editions in 2026. Use those model-style signals to spot risk quickly, then confirm the treaty in force and the local rules before you act.

Risk map for fast triage#

| Risk type | Early warning signals | What to verify in the treaty and local rules | Immediate mitigation action |

|---|---|---|---|

| Withholding on services | Client says tax will be deducted; scope uses technical-service wording; remote delivery is assumed tax-neutral | Whether treaty wording includes Article 12A-style technical-services taxation, or equivalent; whether local withholding procedures require forms or residency proof before treaty treatment is applied | Confirm withholding basis in writing before invoicing; confirm required forms and timing; hold net pricing until deduction responsibility is agreed |

| Service PE exposure | Onsite delivery, repeat visits, rotating personnel, extensions, or phased work that may be treated as one engagement | Whether treaty wording includes Article 5(3)(b)-style service-PE language; timing test (verify the current treaty threshold before using a number); whether same-or-connected-project aggregation applies | Start day-log tracking at kickoff by person, country, and project phase; pause scope or travel expansion until threshold and aggregation treatment are verified |

| Royalty reclassification | Contract grants use rights, source-code access, template reuse, know-how, data rights, or broad IP terms | Royalty definition based on use or right-to-use wording; whether local practice could classify part of the fee as royalties; whether software characterization is unsettled on your facts | Separate service and license economics; tighten IP language to intended rights only; remove accidental know-how transfer language unless intended |

Services withholding#

If your fee may be treated as technical services under the treaty wording, withholding can hit cash flow immediately. Article 12A was added to the UN Model in 2017, and that pattern allows source taxation on a gross basis at a treaty-negotiated rate. Remote delivery does not automatically remove this exposure.

In practice, the sequence is straightforward: verify the treaty wording, then verify the withholding mechanics with the client. Confirm what residency evidence, forms, and submission timing are required before payment. If the withholding basis is disputed, escalate before signature. MAP exists for competent-authority consultation, but it is a dispute channel, not instant relief.

Service PE exposure#

Service PE risk can turn a pricing issue into a local filing and compliance issue. A common treaty pattern is Article 5(3)(b)-style language tied to duration. One familiar UN pattern is more than 183 days in any twelve-month period, but do not assume that exact test applies in your treaty. Use the verified treaty threshold only after you confirm the actual treaty or protocol wording.

The common failure mode is weak tracking. If related phases, associated personnel, or renewals could be treated as the same or a connected project, counting only your own travel days is not enough. Keep a disciplined day log from day one. Use this Service PE compliance setup guide for freelancers if you need an operating checklist.

Royalty reclassification#

Royalty risk is often driven by contract language rather than intent. Royalty treatment turns on payments for the use of, or right to use, IP or know-how. In more UN-leaning treaty contexts, that can preserve source-country taxing rights. If service scope and IP rights are blended, part of the fee may be pulled into royalty treatment.

Escalate early when software or IP characterization is unclear. Separate service deliverables from license rights in both scope and pricing so your invoice language matches what you are actually selling.

Escalate now if any of these are true#

The right time to escalate is before the first invoice, not after a deduction shows up. Raise the issue now if any of these apply:

| Trigger | Why it needs escalation | Immediate focus |

|---|---|---|

| In-country delivery is planned, even for an initial short phase | Service PE risk can turn a pricing issue into a local filing and compliance issue | Raise the issue before the first invoice |

| Project phases, renewals, or related entities raise same-or-connected-project aggregation risk | Related phases may be treated as the same or a connected project | Verify aggregation treatment before the first invoice |

| Contract wording mixes services with software, license, or know-how reuse rights | Part of the fee may be pulled into royalty treatment | Separate service and license economics |

| You and the client do not agree on withholding basis before the first invoice | Withholding can hit cash flow immediately | Escalate before signature |

Before you move to Step 3, prepare a minimum handoff file:

- Clause asks: gross-up language, pre-withholding notice, and cooperation on treaty forms.

- Scope cleanup: explicit separation of services from any license rights.

- Documentation pack: treaty article notes, residency proof, day log, signed scope, and invoice support.

For a step-by-step walkthrough, see Understanding the Independent Personal Services Article in Tax Treaties.

Step 3: Fortify Your Contracts & Protect Your Profits#

Do not sign until three things are documented: net-pay terms, fee classification, and treaty-plus-local implementation checks. If you cannot point to the treaty in force, the client's withholding workflow, and a named client-side tax or finance owner, the deal is not ready to sign.

That applies whether the treaty feels UN-leaning or OECD-leaning. Model texts are starting points for negotiation, application, and interpretation, not substitutes for the signed agreement. Your contract should match the tax position you are relying on, and your deal file should show how that position will actually be carried out.

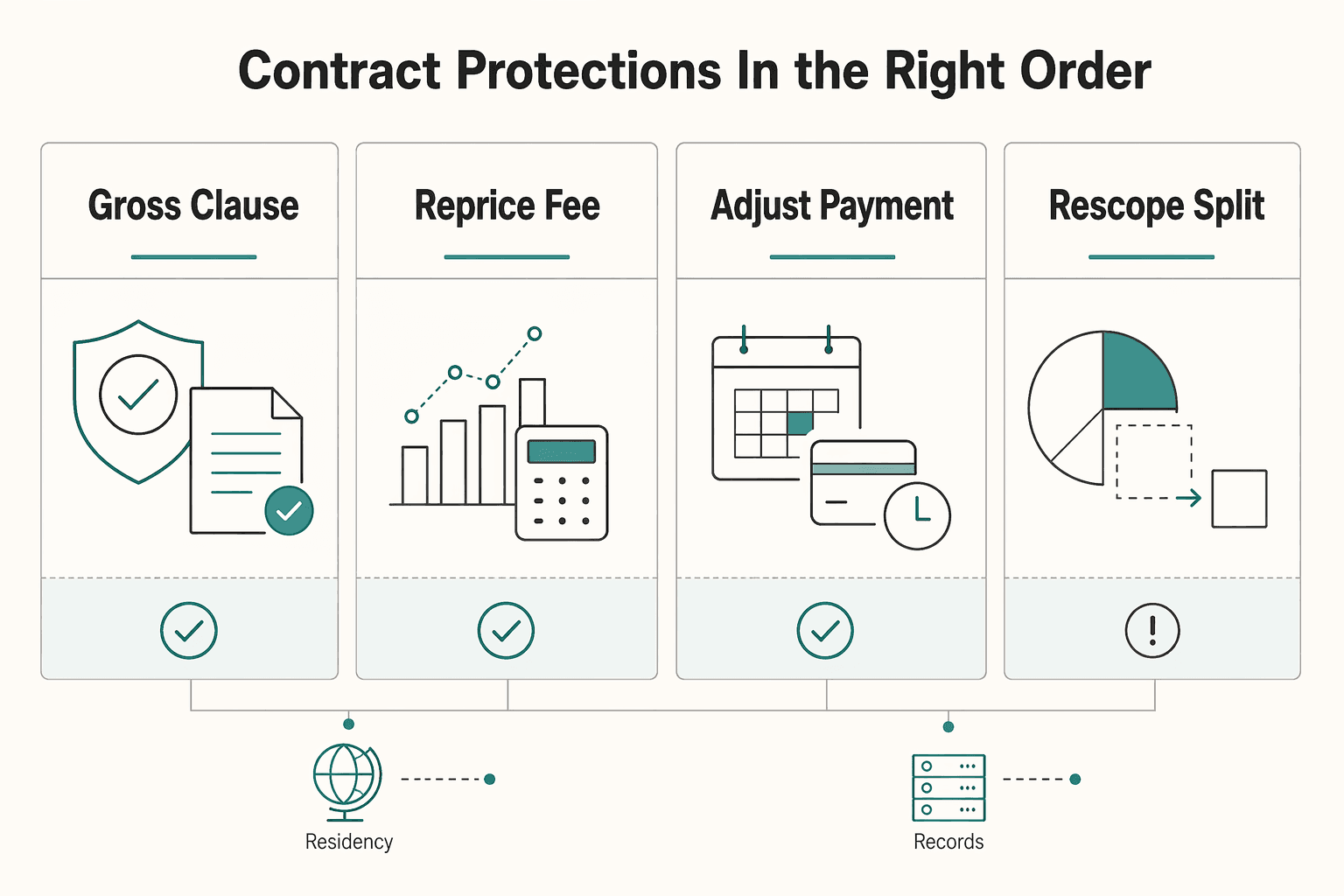

Contract protections in the right order#

Start with the margin-protection term first, then move down only when the prior option is unavailable and your evidence is complete.

| Contract option in sequence | Proceed only if this is true | Evidence required before signature | Main failure mode |

|---|---|---|---|

| Gross-up clause | Withholding risk is real and the client accepts net-fee intent | Signed gross-up language, written withholding responsibility, required residency proof or treaty forms, named payables or tax contact | Clause is vague, or payables withholds anyway because no one owns implementation |

| Reprice fee | Gross-up is refused, but you still want the engagement | Written pricing assumptions tied to the treaty text and local process you verified | Repricing is based on assumptions, then under-collects if classification changes |

| Adjust payment structure | Classification is reasonably clear, but timing can still compress cash flow | Final milestone, deposit, or invoice timing terms and form-submission ownership before payment dates | First invoices are delayed or paid short because documentation is not operational |

| Rescope or split rights | Tax risk is concentrated in a specific deliverable, right, or in-country phase | Revised SOW, separate rights annex, deliverables map, travel or presence assumptions | Services and rights stay blended, increasing royalty or local-presence risk |

If gross-up is available, ask for it first. If it is not, do not sign just because the deal still looks commercially attractive. Repricing, timing changes, and scope reduction only work when they rest on verified treaty text and workable local mechanics.

Red-flag scan for SOW language#

Service-versus-royalty outcomes can turn on a few words about use, reuse, or the right to use IP or know-how. Before you sign, scan for language that could reclassify part of the fee:

| SOW wording | Why it matters | Response |

|---|---|---|

| client reuse rights for templates, methods, datasets, or tools | can reclassify part of the fee | separate the rights grant from the service delivery terms and align pricing and invoice lines with that split |

| access rights to source code, proprietary materials, or technical documentation | can reclassify part of the fee | separate the rights grant from the service delivery terms and align pricing and invoice lines with that split |

| know-how transfer or ongoing methodology-use rights | can reclassify part of the fee | separate the rights grant from the service delivery terms and align pricing and invoice lines with that split |

| perpetual, exclusive, or sublicensable rights inside a services clause | can reclassify part of the fee | separate the rights grant from the service delivery terms and align pricing and invoice lines with that split |

If those rights are intentional, separate the rights grant from the service delivery terms and align pricing and invoice lines with that split. If they are not intentional, remove the language.

Verification checkpoint and escalation triggers#

Your control point is the treaty in force and local withholding practice. Keep a current-position check in the deal file for relevant commentary, local guidance, and model updates without assuming those materials automatically changed the signed treaty.

Escalate before signature if any of these are unresolved: the withholding workflow is unclear, connected-project presence risk is still open, service-versus-royalty classification is disputed, or no client-side tax-process owner is named. For Service PE, you may see the UN workstream phrase periods on the same or connected project aggregating more than 183 days. That same workstream records both views on physical presence, so rely only on the treaty wording and local interpretation you verify.

If travel, renewals, or rotating personnel are in scope, tighten the contract and run this Service PE contract-check guide before kickoff. If net pay, classification, and implementation ownership are not evidenced before signature, pause the deal. Reprice it, narrow it, or escalate it, but do not sign around unresolved tax uncertainty.

You might also find this useful: Using DTA Tie-Breaker Clauses to Resolve Dual Tax Residency. Before signature, pressure-test your treaty assumptions and documentation workflow with the Tax Residency Tracker.

Conclusion: From Compliance Anxiety to Contract Confidence#

The practical way to close cross-border deals is a repeatable path: Assess, Identify, Fortify. Use the UN and OECD models to frame the risk, then make the real call from the treaty in force, any protocol amendments, and the local implementation and effective-date rules that apply when you invoice.

| Point to decide | Pre-sign decision | Concrete action |

|---|---|---|

| Source vs residence taxing rights | Will source-country withholding change your net pay under the in-force treaty? | Pull the treaty article and any protocol text, then confirm the client's finance owner, forms, and withholding workflow before pricing is final |

| Technical services classification | Could your fees be taxed under technical-services wording, or because the scope mixes services with rights? | Split services from license, IP, or know-how language in the SOW and keep invoice lines matched to that split |

| Service PE or local presence | Could your cross-border delivery footprint create local filing or tax exposure under the treaty and local rules? | Start a day-by-person, day-by-country log before kickoff and review expansion requests before approving them |

To keep execution clean, use this pre-sign checklist:

- Decide whether you have the operative text: save the bilateral treaty, all protocols, and a note on entry into effect in the deal file.

- Decide whether the payment outcome is clear: if not, ask for gross-up or reprice before signature.

- Decide whether classification is clean: keep contract, invoice, and tax support pack aligned.

- Decide whether remote delivery changes treatment: if the in-force treaty has Article 12A-type wording, do not assume physical absence from the client country removes source-taxation risk.

- Decide who owns the evidence: keep residency proof, treaty excerpts, withholding correspondence, and your day log together.

That is the practical takeaway from the UN versus OECD comparison. The models help you ask better questions, but they do not settle your contract. If your residency position still needs work, start with what "permanent home" means in a tax treaty. If the treaty answer is already clear, move the same evidence pack into your Gruv workflow so payment, invoicing, and compliance stay aligned.

When treaty wording is unclear, classification is contestable, or local-presence risk remains unresolved, escalate before signature or invoicing. For related residency tie-breaker context, see What Is a Habitual Abode in a Tax Treaty?. If you want a cleaner operating flow from invoicing to cross-border payout tracking, see Gruv for freelancers.

Frequently Asked Questions

What does residence taxation mean for your contract?

Treat residence taxation as a planning input, not an automatic payment outcome. Verify the ratified treaty, any protocol, and the exact residency document the client says it will accept, then keep those details consistent across your contract, invoice, and tax records. Before signing, lock down who provides documents, expected timing, and what happens if they are late. Escalate if documents conflict or the client cannot state the treaty basis for relief.

When does source taxation become your cash-flow problem?

It becomes a contract problem as soon as it can change what you actually receive or when you receive it. Verify the treaty text and local implementation together with the client’s withholding workflow, required forms, and named finance owner. Before signing, treat net-pay protection as an execution item, not a verbal assumption. Escalate if ownership, forms, or withholding logic are still unclear.

What counts as service PE risk?

Treat service PE as treaty-specific and tie the review to your delivery footprint. Verify the treaty wording in force, whether connected work is aggregated, and any applicable threshold that still needs confirmation. Before signing, track days by person and country and include renewals, subcontractors, and follow-on phases in the same log. Escalate when staffing or travel plans could change the outcome. Use this services PE guide before kickoff if needed.

What are fees for technical services in practice?

In practice, this is a fee-classification question that can affect withholding and compliance steps. Do not assume the outcome from model language alone. Verify the treaty in force, any protocol, and how the client classifies your scope. Before signing, split services from IP, know-how, or license rights and keep invoice lines aligned to that split. Escalate if the SOW still mixes services with reuse or rights terms.

Are the UN and OECD models the same thing as your treaty?

Do not assume so for contract execution. Use model language as context, then confirm the treaty in force, any protocol, and local implementation before relying on a clause for pricing or payment mechanics. Escalate if anyone cites model language but cannot point to the treaty article and workflow that will control payment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- desapublications.un.org/publications/united-nations-model-double-tax...trusted

- financing.desa.un.org/document/un-model-double-taxation-convention...trusted

- irs.gov/pub/irs-lbi/table-3-list-of-tax-treaties.pdftrusted

- oecd.org/en/about/news/press-releases/2025/11/oecd-up...trusted

- un.org/esa/ffd/wp-content/uploads/2017/03/14STM_CRP...trusted

- gov.uk/hmrc-internal-manuals/international-manual/i...external

- tax-platform.org/sites/pct/files/Examples%20of%20Entry-into-F...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Spain Autonomo System for Freelancers Who Want Compliance Control

Low-stress compliance comes from predictable execution, not tax-shortcut bets. Keep filings clean, document decisions, and set escalation triggers before deadlines.