Quick Answer

Use a three-phase control process for SEIS angel investing: verify the funded entity and deal terms before money moves, build one complete and internally consistent file after payment and share issue, and keep monitoring changes through filing. Check your Self Assessment status early, and claim only when names, dates, amounts, and supporting records all reconcile.

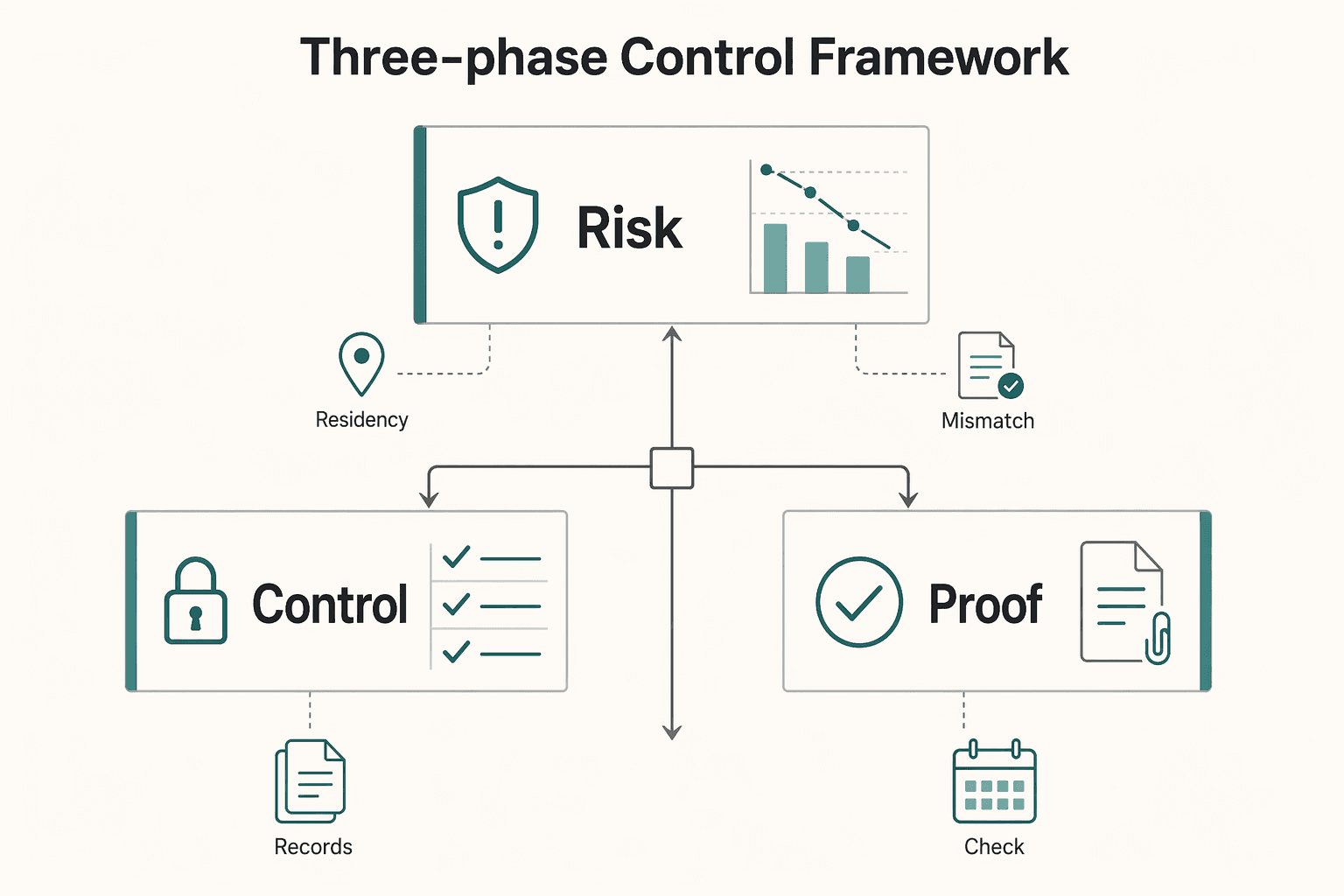

UK SEIS Investor Guide: Three-Phase Control Framework#

Treat UK SEIS investing as an operations workflow, not a one-time tax form. Your practical sequence is simple: verify the deal identity before money moves, build a claim-ready evidence file after share issue, then monitor changes through your filing window.

According to HMRC venture-capital guidance, SEIS outcomes depend on eligibility and records, not on informal assumptions. In 2026 planning, many investors run downside cases at 25%, 50%, and 75% capital loss before they commit so they understand risk if growth assumptions fail.

Use this guide together with your broader angel investing playbook, your residency checklist, and a live tax residency tracker so your SEIS claim process stays aligned with your overall tax position.

Guide Step 1: Seed enterprise investment scheme eligibility screen#

Before funding, verify that the company and transaction are being run inside the current SEIS application process. The first avoidable failure mode is paying before names, terms, and entity identity are final.

Your first legal check is entity identity. If documents are inconsistent about company name or legal form, pause. You are investing in a specific legal entity, not in an email thread.

Evidence packet checklist#

Build one version-controlled folder before funding and keep every final document there. This is where many SEIS investor files improve from "probably fine" to auditable.

- signed subscription agreement with final share terms

- payment instructions that match the funded entity

- cap table snapshot dated before transfer

- board or issue records expected after completion

- clear note of open assumptions requiring verification

| Pre-funding control | Target state | Stop condition | Why it matters for SEIS investors |

|---|---|---|---|

| Entity identity | Company name and registration details match every file | Any mismatch between contract and payment destination | Wrong-entity funding can undermine later claim logic |

| Share economics | Share class, count, and price align across docs | Late changes not reflected in all records | Inconsistent economics create filing friction |

| Payment details | Bank details and amount are confirmed in writing | Pressure to send funds before final confirmation | Payment evidence must reconcile cleanly |

| Tax assumptions | Open tax points are explicitly marked for verification | A key rule is being treated as settled without evidence | Prevents overconfidence at claim stage |

When teams skip this pre-funding reconciliation, they usually pay for it later with rework. The most common failure pattern is not fraud; it is document drift across versions. One person updates the share count, another updates pricing, and the final payment confirmation still references an older draft. Your quality bar is to make every critical number traceable from subscription terms to payment evidence to issue records without interpretation.

Guide Step 2: SEIS claim file build and timeline checks#

After funding, switch from deal selection to records control. For investors, this is where claim quality is won: names, dates, and amounts must reconcile across subscription paperwork, payment proof, and company-issued SEIS documents.

| Step | Company action | Investor action | Reconciliation check before claim |

|---|---|---|---|

| Before funds move | Issue final subscription paperwork and payment details | Confirm investor name, amount, and funded entity | Entity, share terms, amount, and bank details match |

| After payment and share issue | Provide dated issue evidence and compliance documents | Store signed paperwork, payment evidence, and issue records | Payment amount and date match issue records |

| Before return filing | Confirm final SEIS documents provided to investors | Confirm Self Assessment account status and readiness | No missing names, dates, or amount fields |

Claim calendar controls#

According to HMRC process guidance, file timing still matters even when your documents are strong. Keep one dated investor timeline and pin every claim milestone to it.

| Calendar checkpoint | Typical timing marker | Investor control action | Record retained |

|---|---|---|---|

| Self Assessment registration check | By 5 October when registration is required | Verify whether your account needs registration or reactivation | Registration confirmation and UTR details |

| Online filing window opens | From April in the next filing cycle (for example 2026/27) | Review claim folder before drafting return | Dated filing-prep checklist |

| Payment deadline checkpoint | By 31 January for the relevant tax payment cycle | Reconfirm filing and payment plan | Payment plan confirmation |

| SEIS document readiness | Before claim submission | Verify SEIS3 certificate workflow | Final claim-ready packet |

Treat this table as a recurring control cycle, not a one-time checklist. If the company sends updated documents after your first review, rerun every numeric field. If your accountant or adviser flags one mismatch, reopen the file end-to-end. According to HMRC workflows, a complete and consistent file is easier to file, easier to explain, and easier to defend if questions come later.

If one date slips, update the whole claim plan. A clean SEIS file is not static; it is an actively maintained sequence.

- review the investment folder immediately after funds move

- reconcile again when SEIS paperwork arrives

- run a pre-filing audit before submission

- check annual updates in your investor planning notes

Guide Step 3: Monitoring through the three-year holding period#

SEIS risk does not end when you file. Keep a monitoring log for the holding period and track any event that could change claim assumptions, ownership facts, or filing strategy.

- Ownership changes: new rounds, restructures, or control shifts.

- Business model changes: material pivots that may affect eligibility assumptions.

- Filing-readiness changes: missing documents, account access issues, or unresolved mismatches.

| Monitoring event | What to capture | Escalation threshold | Action owner |

|---|---|---|---|

| Cap table update | Date, new ownership table, related notices | Any impact on facts used in your claim file | Investor + adviser |

| Company structural change | Board communication and supporting records | Unclear effect on the original investment terms | Investor + counsel |

| Filing issue discovered | Exact mismatch and impacted form fields | Claim cannot be filed with confidence | Investor tax preparer |

If you run multiple deals, keep a shared operational checklist in Tools and a separate per-investment evidence folder. That keeps one bad record set from contaminating the rest of your pipeline.

Guide choice: Direct deal or pooled route for SEIS investors#

Choose the route that matches how much operational control you can execute consistently. Direct deals usually provide more company-level visibility; pooled routes usually reduce single-company concentration and administrative load.

| Option | Control profile | Admin load | Diversification | Cost visibility | Claim-handling responsibility |

|---|---|---|---|---|---|

| Direct deal | Higher investor control over company selection | Higher | Lower unless you build a wider portfolio | You directly track each ticket (for example 20,000 GBP to 100,000 GBP) | Mostly investor-led |

| Pooled route | Lower company-level control | Lower for individual investor | Higher by design | Manager fees and allocation terms should be explicit | Manager-led with investor oversight |

| Syndicate-style participation | Shared control depending on lead structure | Medium | Medium to high | Follow-on funding expectations should be pre-modeled | Shared process, verify responsibilities in writing |

If you invest across several deals, track allocation limits and liquidity constraints explicitly. For example, many operators cap single-deal exposure at 20% to 30% of their annual angel budget and keep reserve cash for follow-ons. This does not remove risk, but it prevents one attractive narrative from dominating your portfolio decisions.

- Choose direct when you want hands-on due diligence and can run documentation controls.

- Choose pooled when you prefer diversification and manager-led execution.

- Use the same filing discipline either way: complete files, reconciled numbers, clear dates.

For cross-border investors, map this decision against your residency and filing context with UK residency guidance and your tax residency tracker before committing capital.

Guide numbers for 2026 SEIS investor decisions#

A practical SEIS guide should include numeric scenarios, not only process notes. Model realistic investment sizes and relief assumptions so your liquidity and downside decisions are intentional.

| Scenario | Investment | Illustrative income-tax relief at 50% | Net capital at risk before other relief assumptions | Planning note |

|---|---|---|---|---|

| Starter ticket | 20,000 GBP | 10,000 GBP | 10,000 GBP | Useful for first-cycle process testing |

| Core allocation | 50,000 GBP | 25,000 GBP | 25,000 GBP | Requires tighter evidence controls |

| Large single deal | 100,000 GBP | 50,000 GBP | 50,000 GBP | Concentration risk should be explicit |

Model your decision with at least two currency views if your income is not GBP-native. A freelancer billing in USD can still evaluate a UK SEIS deal by converting the same scenario at 20,000 GBP, 50,000 GBP, and 100,000 GBP, then comparing the position against a 25,000 USD to 125,000 USD opportunity set. This keeps portfolio decisions grounded in comparable risk rather than headline relief alone.

Validate assumptions against current HMRC investor guidance before filing, including investor relief conditions and current venture-capital forms and helpsheets.

- If the draft return references figures from an old workbook, refresh every amount.

- If any source document was replaced, invalidate earlier reconciliations and rerun checks.

- If timeline changes push filing into a new tax cycle, update your 2026/27 process notes and payment planning.

SEIS investor FAQ for 2026 filings#

Use these answers as operational defaults, then confirm the exact legal treatment for your case with professional advice.

Can you claim SEIS relief before you receive compliance documents?#

Most investors treat compliance documentation as the practical claim trigger. Build and reconcile your file first, then submit. If the document chain is incomplete, pause and close the gap before filing.

Does advance assurance guarantee investor relief?#

No. Advance assurance helps with planning, but it is not an investor guarantee. Your claim still depends on final facts, timing, and supporting records.

What Self Assessment dates should investors track?#

Operationally, track three dates first: registration checks around 5 October where required, filing from April in the next cycle, and payment by 31 January. Keep these dates in your claim calendar and update them as your case evolves.

How long should you keep your SEIS records?#

Keep records through the holding window and until your filing and review risk periods are clearly closed. In practice, investors retain a complete package so they can answer follow-up questions without reconstructing the deal.

Should you invest directly or through a pooled route?#

Choose direct deals when you want more control and can manage administration. Choose pooled routes when you want broader diversification and manager-led operations. Either way, run the same evidence discipline.

Next actions for this investor guide#

If you want to operationalize this guide today, start with your current investment folder, run the three-phase checklist, and fill any missing fields before the next filing deadline. Then connect your broader planning stack using A Freelancer's Guide to Angel Investing and Venture Capital, UK Statutory Residence Test guidance, and Gruv Tools.

Frequently Asked Questions

Can you claim SEIS relief before you receive a compliance certificate?

Investors normally claim from the compliance documents supplied after the company completes the SEIS process, using a reconciled file with subscription paperwork, payment evidence, and issue records.

Does advance assurance guarantee investor relief?

Advance assurance is not an investor guarantee. Relief still depends on final eligibility conditions, timing, and records at claim time.

What dates matter most for Self Assessment filing readiness?

Operationally, investors should check whether they must register by 5 October, prepare filing from April in the next tax cycle, and plan payment deadlines by 31 January.

How long should you keep SEIS investor records?

Maintain a full investment record through the holding period and until filing and review risk windows are closed.

Should investors choose direct or pooled SEIS routes?

Direct routes generally offer more company-level control with higher admin load, while pooled routes typically improve diversification and delegate more operational handling.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

A Freelancer's Guide to Angel Investing and Venture Capital

**Build a decision system that protects your operating cash first, then treat angel investing as an optional use of true surplus.** If you are considering angel investing as part of broader wealth building, you need controls that keep "startup investing" from quietly raiding rent, taxes, or payroll. Knowledge feels productive, but constraints keep you solvent. As the CEO of a business-of-one, your job is to protect the operating cash that keeps the machine running.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.