Quick Answer

Yes - california trailing tax liability can continue after you move when income remains California-source, especially compensation tied to services performed in the state. Your filing position depends on facts, not an address change: classify resident and nonresident periods, validate equity and bonus allocation logic, and maintain dated records that support Form 540NR treatment when required.

The California Exit Strategy: Your 3-Step Guide to Trailing Tax Liability#

Quick answer: After you leave California, you can still owe California tax on income that remains California-source. California taxes residents on worldwide income, but as a nonresident, you are taxed on California-source income.

That distinction is the filter for the decisions that follow. California does not impose a universal enacted wealth-based "exit tax" on everyone who moves, and separate wealth-tax proposals are a different issue from income sourcing. In practice, the real risk is usually compensation sourcing: income connected to services you physically performed in California, including some stock-option compensation.

| Common belief | Operational reality | What to do now |

|---|---|---|

| "Once I change my address, California is done with me." | Address changes alone do not end filing or sourcing exposure. | Separate resident-period income from nonresident California-source income. |

| "If I move before payout, California cannot tax it." | Payout timing alone does not control sourcing. | Gather grant, vest, bonus, and workday records before you move. |

| "This is basically a wealth tax." | Usually, this is an income-sourcing issue. | Focus on compensation history and residency facts, not headlines. |

You may have meaningful exposure if you have compensation tied to California work, especially equity compensation or bonuses linked to services performed in California. Exposure can be narrower when post-move income is tied to services performed outside California and your residency change is well documented. If your facts are mixed, such as multi-state remote work, equity compensation spanning your move, or a possible employment-related safe-harbor case, get personalized advice before filing.

The next three phases tackle three separate problems: what income can trail, how to time your move and compensation events, and how to document your nonresident position. By the end, you should know what is still exposed, what is not, and what records you need if the Franchise Tax Board asks questions. If you are still comparing destinations, use the California to Texas tax comparison for that next decision.

Phase 1: The Non-Negotiable Pre-Move Audit#

Before you lock a move date, build an audit file that separates what California can still tax from what it likely cannot. Here, trailing tax liability means post-move California exposure only for income California still treats as California-source. Follow this order: first inventory income, next validate sourcing and allocation inputs, then pressure-test residency facts, and last check business nexus.

Start with the income that can follow you#

California taxes part-year residents on worldwide income during the resident period, and on California-source income during the nonresident period. For services, California-source income turns on where you physically performed the work, not where you lived, signed, or were paid. Use this checklist before you model tax:

| Income type | Records to gather now | Missing-document audit risk |

|---|---|---|

| Salary, bonus, commission, severance | Offer letter, plan terms, pay stubs, YTD payroll, W-2, memos defining earning/performance period | Post-move payment with no proof of the service period |

| Equity (RSUs/options) | Grant notices, plan docs, vest schedules, exercise confirmations, brokerage statements, work-location history for each grant period | Missing grant/vest dates or location history, so payout cannot be reliably allocated |

| Deferred comp / retention | Plan agreement, payout schedule, terms showing past vs future services | No support for what services the payment is tied to |

| Other multi-year payouts (for example, installment payments tied to prior transactions) | Agreement terms, closing or settlement records, prior-year returns | Weak support for source characterization |

| Pass-through income | All Schedule K-1s plus California/everywhere property, payroll, and sales data | Incomplete factor data for sourcing or doing-business analysis |

If a grant was modified, accelerated, refreshed, or partially canceled, flag it immediately.

Validate your sourcing inputs before you model anything#

If equity is in scope, validate the inputs before you estimate anything. For some equity fact patterns, FTB chief counsel describes a grant-to-vest workday allocation: California workdays from grant to vest, divided by total workdays everywhere in that same period, multiplied by the compensation received. Use it carefully. It is not a universal rule for every instrument or fact pattern.

| Allocation piece | Input needed | Common error | Decision use |

|---|---|---|---|

| California workdays in grant-to-vest period | Calendar, timesheets, employer records, travel logs showing days physically worked in California | Counting calendar days instead of workdays; assuming all pre-move days were California workdays | Builds numerator |

| Total workdays everywhere in same period | Complete workday count across all locations for the exact grant-to-vest window | Inconsistent date windows; excluding remote days; mixing payroll and vest periods | Builds denominator |

| Compensation tied to the grant/tranche | Grant detail, vest/event data, exercise records, payout amount | Applying ratio to the wrong amount or tranche | Produces dollar estimate for timing/withholding decisions |

Checkpoint: rebuild one grant timeline from source documents only. If the grant notice, HR records, payroll, travel logs, and brokerage events do not align, fix the record before you estimate anything.

Also, do not assume post-move wages are automatically outside California. If you physically perform services in California after moving, that portion can still be California-source.

Pressure-test residency as a separate issue#

Residency is separate from sourcing and is fact-intensive. The questions are your closest connections and whether your California presence is temporary or transitory. Address changes help, but none of them ends residency exposure by itself.

Build a dated timeline covering your move date, housing, family location, office location, days in and out of California, bank and mailing changes, vehicle registration, and where you regularly worked. Then test that timeline against the return position you plan to file.

If an employment-related safe harbor might apply, treat it as a possible path that still has to be verified against your facts and any exceptions.

Check business nexus last, but do not skip it#

Once you sort out personal sourcing and residency, check whether any business activity still keeps you in California's orbit. For owner-operators, trailing nexus risk means personal relocation does not automatically end California business exposure. You can still be "doing business" if you engage in California transactions for financial gain, and being below one numeric threshold does not automatically remove exposure.

| Item | Amount / rule | Context |

|---|---|---|

| California sales | $757,070 | Published 2025 doing-business threshold |

| California property | $75,707 | Published 2025 doing-business threshold |

| California payroll | $75,707 | Published 2025 doing-business threshold |

| Related percentage tests | 25% | Mentioned with the published 2025 thresholds |

| Nonresident withholding | 7% when California-source payments or distributions exceed $1,500 in the calendar year | For qualifying partnership or S corporation situations |

For 2025, published doing-business thresholds include $757,070 California sales, $75,707 California property, and $75,707 California payroll, with related 25% tests. Keep those numbers in view, then test the actual facts: California transactions for financial gain, California people or property, and California-source pass-through income.

Cash-flow flag: if you expect California-source partnership or S corporation distributions after the move, check nonresident withholding. California shows 7% withholding in qualifying situations when California-source payments or distributions exceed $1,500 in the calendar year.

Escalate to a qualified tax professional before filing if you have complex equity history, multi-state workdays, pass-through apportionment issues, incomplete K-1 factor data, disputed residency facts, or safe-harbor criteria that still need legal verification. Keep your return and supporting records, usually at least 4 years, so you can substantiate your position if reviewed later.

Phase 2: Strategic Exit Timing#

After Phase 1, this becomes mostly a sequencing problem: set the move date, plan equity events, lock compensation terms, then run a rule check before filing.

Timing matters because classification can change even when cash does not. California taxes worldwide income while you are a resident, and California-source income while you are a nonresident. That means your dates and service-period facts drive the result.

1) Anchor the timeline with move-date planning#

Use the move date as the control point, not the payout date. The practical question is whether you can complete the move before the next earning period, grant date, or other compensatory event starts.

For options, keep the terms straight:

- Grant date: date the company grants the option.

- Vesting date: date the option becomes exercisable.

Before you rely on a return position, make sure your HR effective date, payroll address, travel log, and actual work locations all match the same timeline.

2) Decide before exercise or sale#

Do not treat an equity event as a clean break just because it happens after the move. What matters is how the service period lines up with your California workdays.

For NSOs, FTB Pub. 1004 shows a California workday allocation example using:

California workdays from grant date to exercise date / total workdays from grant date to exercise date

Pub. 1004 also says NSO wage income is generally recognized at exercise, and the ordinary-income amount is FMV at exercise minus option price. Do not assume a post-move exercise removes California exposure if California workdays exist in that grant-to-exercise period.

For ISOs, the key fork is disposition type:

- Qualifying disposition: no sale within 2 years from grant and no sale within 1 year after exercise.

- Disqualifying disposition: those holding-period rules are not met.

FTB materials indicate sourcing can differ on the qualifying path based on residence at sale, so keep your holding-period and trade records complete.

| Event | Tax exposure risk | Preferred timing posture | Records to retain |

|---|---|---|---|

| Move date vs new grant/bonus cycle | Income stays tied to resident period or California-linked earning period | If controllable, complete move before the next grant or earning period begins | Move timeline, HR address change, travel log, housing docs |

| NSO exercise | California allocation from grant-to-exercise workdays | Model first; do not assume post-move exercise avoids California tax | Grant notice, exercise confirmation, FMV support, option price, workday log |

| ISO sale | Qualifying vs disqualifying disposition can change characterization or sourcing path | If facts and portfolio risk allow, evaluate waiting until both holding periods are met and nonresidency is established | Grant, exercise, sale confirms, holding-period worksheet |

| Severance/deferred comp payout | Unclear terms can create later characterization disputes | Finalize allocation language before signing and payroll coding | Signed agreement, drafts, HR memo, approval record, payroll coding support |

| Employment-related absence | Safe-harbor reliance fails if disqualifiers apply | Screen eligibility before relying on safe harbor | Employment contract, CA day count, intangible-income support |

3) Negotiate compensation terms for audit clarity#

If severance, retention, or deferred compensation is involved, clean drafting can matter as much as timing. You want the documents to say what the payment covers before anyone has to defend it later.

| Checklist item | What the document should say or show |

|---|---|

| Allocation language | State what each payment covers; avoid one undifferentiated lump sum |

| Service-period mapping | Tie each payment to a specific earning, milestone, or retention period |

| Documentation consistency | The signed agreement, HR memo, approvals, and payroll coding should all match |

Before you sign, make sure those points line up across the agreement, HR records, approvals, and payroll coding.

If the agreement only says "for services rendered" but the payment actually covers multiple periods or purposes, treat that as potential dispute risk.

4) Treat safe harbor as a rule check, not a shortcut#

Safe harbor is an eligibility screen, not an automatic result. California also states that residency is a question of fact.

| Screen item | What to verify |

|---|---|

| Employment-related contract | You were domiciled in California but outside California under an employment-related contract |

| Time outside California | You were outside California for 546 consecutive days |

| California days in a covered tax year | You were in California 45 days or fewer in any covered tax year |

| Intangible-income limit | Verify the current-year booklet threshold before filing; 2024 booklet language shows $200,000 |

Check those items in order.

If any answer is mixed, or your facts include equity complexity, post-move California workdays, or overlapping sourcing issues, escalate to a tax professional before filing.

Phase 3: The "Audit-Proof" Documentation Protocol#

Once the move happens, your job changes from planning to proof. You need a dated record that can survive review: when you stopped treating California as home, when you established your new home, and why later California presence was temporary or tied to California-source work. Residency is a facts-and-circumstances determination. The FTB does not issue written residency opinions for a specific period, and no single factor controls the result.

Define the terms before you collect documents#

Use these definitions consistently across your file:

- Domicile: physical presence plus intent to make a place your permanent home.

- Residency evidence: the pattern and strength of your California ties compared with your ties elsewhere.

- Temporary or transitory presence: a brief, pass-through, or vacation-type California presence when your home is elsewhere.

- Contemporaneous records: records you maintain as events happen to document transactions and support your position during review.

Run the immediate post-move checklist#

Start with the records that establish the move itself, then track anything that could blur the story later.

- Sever California ties in key systems. Update mailing address in payroll, tax, banking, brokerage, and client records. If your mailing address changes, file FTB Form 3533 and keep confirmation.

- Establish new-state ties with dated proof. Keep occupancy records, first utility starts, local invoices, and account updates.

- Document intent in writing. Create a dated move memo with your move date, new address, move reason, and intent to make the new location your permanent home.

- Track every California return visit. Separate personal presence from days you physically performed services in California, because service income sourcing follows where services are performed.

Use an operational tracker, not a document pile#

A pile of PDFs is not enough. Use a tracker that shows what was done, what is missing, and where the proof lives.

| Action | Owner | Completion status | Example storage location | Audit relevance |

|---|---|---|---|---|

| Update mailing address, including Form 3533 if needed | You | Not started / In progress / Done | Residency File/Admin/Address Changes | Shows prompt, consistent record updates |

| Save occupancy proof and first local bills | You | Not started / In progress / Done | Residency File/New Home/2026 | Supports physical presence and non-California ties |

| Draft and sign move-intent memo | You | Not started / In progress / Done | Residency File/Intent/2026 Move Memo | Supports domicile and timeline |

| Maintain California travel log with attached proof | You | Weekly | Residency File/Travel Log/2026 | Supports temporary-presence position and workday sourcing |

Consistency is the control point. Your move memo, address records, travel log, payroll location, and calendar should align.

Apply document control and retention rules#

Use a residency-defense folder structure that works for you (for example, by year and topic). Prioritize third-party records such as receipts, cancelled checks, and bills. A sortable naming format, for example YYYY-MM-DD_Source_Topic.pdf, can make review easier, along with an index showing why each item matters.

Add a retention note, but verify it before setting a destruction date. The usual FTB review window is 4 years from the return due date or filing date. Exceptions can extend to 12 years in abusive tax-avoidance cases. Confirm the current rule for the tax year, then record that verified retention period in your file.

Run a repeatable travel-log protocol#

Your travel log is doing two jobs at once: supporting your residency position and supporting income sourcing. That only works if you keep it current.

For each California day, record arrival and departure dates, city, purpose code (WORK, FAMILY, VACATION, TRANSIT), and whether you performed services in California. Attach supporting proof on a regular cadence (for example, weekly), then reconcile monthly against your calendar, expenses, and payroll.

Escalate before filing Form 540NR if:

- dates conflict across records,

- payroll sourced post-move wages to California, or

- your log shows California workdays you did not model earlier.

Related: How to Properly Sever Ties with a 'Sticky' Tax State Like California or New York.

Before you finalize your evidence file, run your timeline through the Tax Residency Tracker so your move records and return-visit logs stay consistent.

Conclusion: You Are the CEO of Your Exit#

You are in control of your exit when you do three things deliberately: take a defensible residency position, source each income item under the actual rules, and keep records that prove both. Control here means reducing ambiguity before filing, not assuming a move alone ends California exposure.

That standard matters because California residency is fact-driven. The FTB applies a closest-connections analysis, treats residency as a question of fact, and does not issue written residency opinions for a specific period.

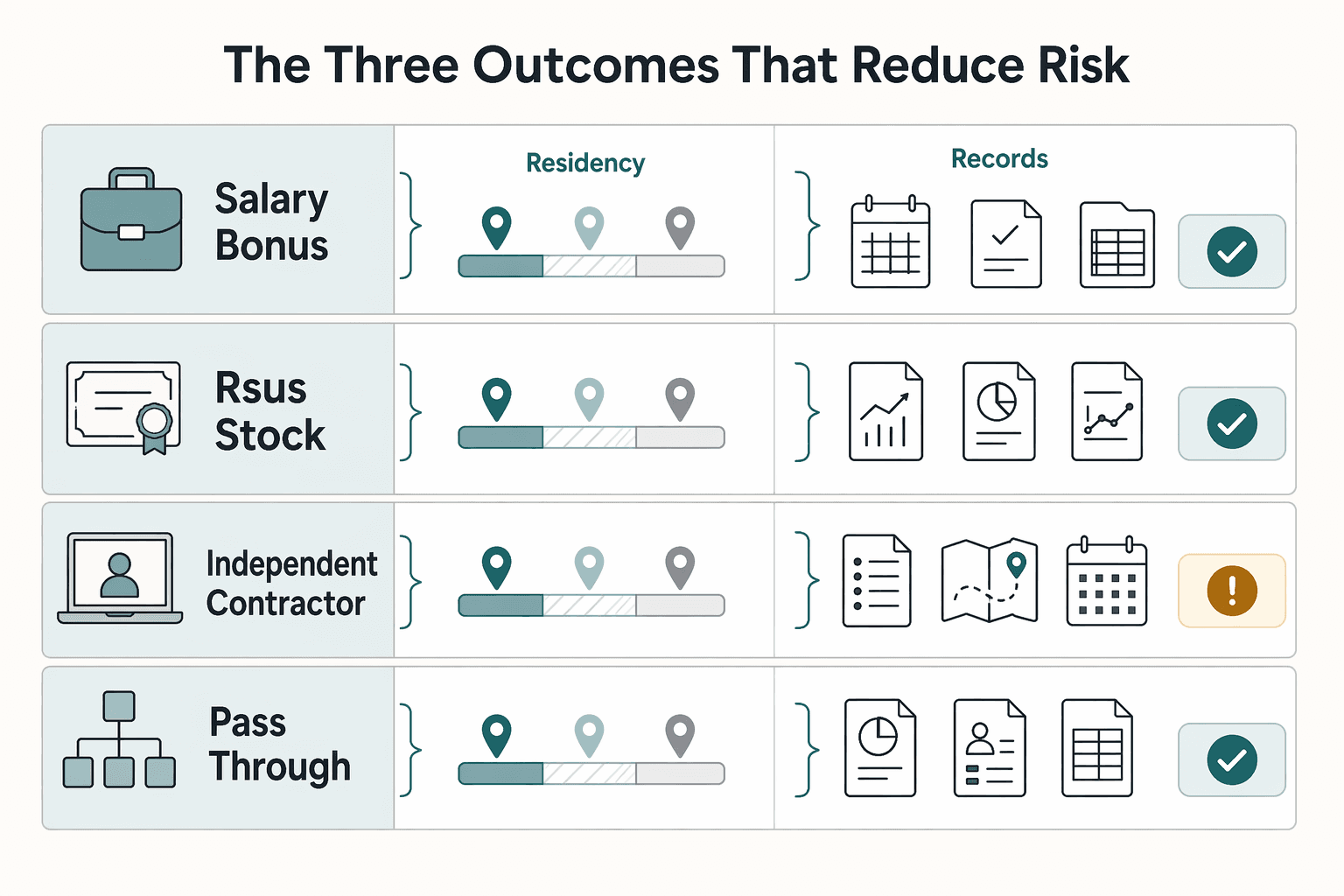

The three outcomes that reduce risk#

- Phase 1 (audit): You decide which items may still be California-source after the move. This reduces the risk of missing a Form 540NR trigger or misclassifying post-move income.

- Phase 2 (timing): You decide what to do before the move, after the move, or only after sourcing is verified. This reduces avoidable sourcing errors from poor sequencing.

- Phase 3 (documentation): You document your new base and the narrowing of California ties as events happen. This reduces the risk of a weak position in a fact-intensive review.

Use this checkpoint before you file: for each material income item, can you answer both "why is this treatment correct?" and "which records prove it?" If either answer is unclear, that item is not filing-ready.

Your filing posture should match the facts: resident, part-year resident, or nonresident. If you lived inside and outside California during the year, part-year treatment may apply, and Form 540NR is generally used to report worldwide income while resident and California-source income while nonresident. For personal services, source follows where services were physically performed. California may apply a workday ratio for multistate service periods.

| Income type | Sourcing question to answer | Records to retain |

|---|---|---|

| Salary, bonus, severance, deferred compensation | Where were the underlying services physically performed, and if the service period spans states, what is the California workday ratio? | Compensation memo, payroll detail, calendar, travel log, workday allocation worksheet |

| RSUs, stock options, ESPP, other equity compensation | What part of the earning or service period ties to California workdays, and does payroll sourcing match that allocation? | Grant docs, vest/exercise records, employer equity reports, payroll detail, grant-level workday log |

| Independent contractor or consulting income | Where were services actually performed, and was California nonresident withholding applied where relevant? | Contracts, invoices, dated work calendar, travel log, payment records, Forms 1099, Form 587 if applicable |

| Pass-through/business income tied to your own services | Did you continue physically performing services in California after the move, or otherwise have California-source business income? | Engagement records, allocation workpapers, client/location support, invoices, entity and meeting/travel records |

Keep return-support records through the normal FTB review window, usually 4 years from the due date or filing date, and longer when special situations may apply.

Proceed on your own when the facts are clean and the records are consistent across payroll, calendar and travel history, and your residency timeline. Escalate to a state tax professional when you have meaningful equity complexity, mixed-state service history, or unclear sourcing facts. If you want a next-step comparison for a move to Texas, see A Deep Dive into the Tax Implications of Moving from California to Texas.

If your facts are mixed across equity, deferred compensation, or multiple work states, use Contact Gruv to sanity-check your compliance plan before filing.

Frequently Asked Questions

Is there a California exit tax?

California guidance focuses on California-source income after your move, rather than a standalone net-worth “exit tax.” That can include compensation tied to services performed in California and some equity-based compensation. If you still have California-source pay, you may need to file Form 540NR.

How are RSUs taxed after I move?

RSUs can still be partly California-source after your move because California sourcing can use a California-workday ratio. California-source: the share tied to California workdays in the relevant earning period. Not California-source: the share tied to non-California workdays outside that ratio. Ask for a grant-level workday allocation review if you moved between grant and vest, worked in and out of California during the period, or payroll sourcing does not match your calendar and travel log.

How do you prove nonresidency?

You generally support nonresidency with records that back your residency timeline and California-source income allocation. Keep records contemporaneously, including move timing and a dated California-day work log, especially if you are filing as a part-year resident or nonresident on Form 540NR.

What is the 546-day safe harbor?

The 546-day safe harbor is a condition-dependent nonresident test for some taxpayers domiciled in California but working outside the state under an employment-related contract. It requires at least 546 consecutive days outside California, can disregard return visits of 45 days or less in a taxable year, and can fail if facts show tax-avoidance purpose or if intangible income exceeds $200,000. Escalate to a state tax professional if your contract terms are unclear, your return days are near the limit, or your income includes large stock or investment amounts.

Are ISOs still exposed after a move?

ISOs remain condition-dependent after a move. Exercise may trigger AMT, and missing the holding-period rules can create a disqualifying disposition. Common issues include assuming ISO exercise is AMT-free or timing exercise and sale in ways that change treatment. Get a state tax review if you expect a large spread, plan to exercise and sell in different tax years, or have grants earned during California work periods.

Which official guidance should you read first?

Start with FTB Publication 1100 (Revised: 10/2024) for residency and move-out rules, then FTB Publication 1004 (Revised: 01/2015) for equity-based compensation, and the FTB part-year/nonresident page for sourcing and Form 540NR triggers. For deeper agency interpretation, use the Residency and Sourcing Technical Manual index (Last updated: 09/24/2025) as a starting point, but treat it as guidance rather than controlling law. If your move also includes cross-border facts, start with The Ultimate Digital Nomad Tax Survival Guide for 2026.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

Moving From California to Texas and Building a Defensible Tax Residency Record

Moving from California to Texas is one of the bigger financial decisions a high-earning professional can make. It is not just a change of address. It resets your tax position, your records, and the facts that will define your filing story. The appeal is obvious, and so is the risk. California's Franchise Tax Board can scrutinize residency changes closely, and a sloppy move can turn into a long audit and an expensive dispute.