Quick Answer

Start by deciding which path applies: Green Card Test or Substantial Presence Test under IRC Section 7701(b). Then run the three-year weighting only after separating raw U.S. days from excluded days, and verify each exception with records. Use the 31-day current-year minimum and 183 weighted total as gates, then escalate if first-year election or residency-start-date timing could change the return.

What the look-back rule means for a US residency call#

If you searched for "look-back rule us tax residency," the goal is practical: take a U.S. tax residency position you can defend under IRS rules with records that hold up.

For non-U.S. citizens, the IRS framework starts with two tests for the calendar year, January 1 to December 31, under Internal Revenue Code section 7701(b): the Green Card Test and the Substantial Presence Test. Start there, not with travel folklore or a single headline number.

That classification has real tax consequences. U.S. residents are taxed like U.S. citizens on worldwide income. Nonresidents are generally taxed only on U.S.-source or effectively connected income.

Use this sequence each year:

- Identify which test path applies.

- Count days of U.S. presence using IRS rules.

- Remove days the IRS says do not count.

- Check whether a special rule changes the result, for example, first-year choice, closer connection, or a treaty tie-breaker.

Your first checkpoint is day-count defensibility. For the Substantial Presence Test, any day you are physically present in the United States generally counts unless a specific exclusion applies, so keep raw presence days separate from excluded days.

Your second checkpoint is documentation. Keep a short annual status memo with the test used, assumptions, and any escalation flags. If you rely on first-year choice, treat it as a formal filing position. Meet the conditions, including a 31-day continuous period and the 75% follow-on presence test, and attach the required statement to Form 1040.

The objective is not to outsmart the rules. It is to classify your status correctly, document the logic once, and know when to escalate before filing.

Define the look-back rule in plain English#

People often use the "look-back rule" as informal shorthand for the Substantial Presence Test. It determines whether you are a U.S. resident for tax purposes using a weighted three-year U.S. day count.

To meet the test, you generally need both:

- At least 31 days in the current year.

- At least 183 days across the three-year formula: all current-year days + 1/3 of days in the first prior year + 1/6 of days in the second prior year.

That is why the headline "183 days" shortcut is risky. In the IRS example, 120 days in each of three years adds up to 180 weighted days, so the test is not met.

This test is separate from the Green Card Test, which is based on lawful permanent resident status. If you were a lawful permanent resident at any point in the calendar year, that is an independent path to U.S. tax residency.

Handle it in this order: choose the test path first, run the calculation second, and document the result third. Keep raw U.S. presence days separate from days that may be excluded, then reconcile your day log to your records before you apply the weighting.

Stop treating this as a simple 183-day rule#

If your position is "I was under 183 days," stop and recalculate. In U.S. tax law, that shortcut is incomplete. Residency can come from either the Green Card Test or the Substantial Presence Test, so you need the right path before you decide anything.

For the Substantial Presence Test, the 183 number is a weighted three-year result, not a simple current-year count. The IRS generally requires both 31 days in the current year and 183 days over the three-year formula: all countable current-year days, plus 1/3 of the first preceding year, plus 1/6 of the second preceding year. The IRS also lists exceptions, so not every U.S. day counts. That is why the IRS 120/120/120 example totals 180 weighted days and does not meet the test.

That shortcut also fails because day count is not the only route. If you are a lawful permanent resident, the Green Card Test is a separate path to U.S. tax residency. The IRS also notes that elections can change the outcome in some cases.

Use this operating rule: if a travel plan, departure date, or filing position depends on one headline number, stop and run the IRS framework from start to finish. Then verify your full three-year day history against your own records so you do not miss prior-year days in the calculation.

Choose your status path before you calculate anything#

Start by deciding whether the Green Card Test or the Substantial Presence Test applies to your facts.

| Path | How it is triggered | Key next step |

|---|---|---|

| Green Card Test | Lawful permanent resident at any time during the calendar year | Confirm from your records and timeline when lawful permanent resident status started or ended |

| Substantial Presence Test | Green Card Test does not resolve the result | Count current-year days and apply the three-year weighting, the 31-day condition, and the 183-day threshold |

| Both tests may be met | Same-year dual-test case is possible | Flag the year early and determine the residency starting date under the earlier-of rule |

For non-U.S. citizens, the IRS baseline is nonresident status unless you meet either test. Start by asking whether you were a lawful permanent resident at any time during the calendar year, January 1 to December 31. Once that is clear, the rest of the analysis gets much cleaner.

Check green card status first#

If you were a lawful permanent resident at any time during the year, you meet the Green Card Test and are a U.S. tax resident for that year. In that case, substantial-presence day counting may not be the key first step.

Before working the 31-day and 183-day thresholds, confirm from your records and timeline when lawful permanent resident status started or ended. That keeps your residency determination tied to the right test from the start.

Use Section 7701(b) as your framework#

Internal Revenue Code Section 7701(b) is the legal framework for these rules, and the Treasury regulations split the determinations: 301.7701(b)-1(b) for lawful permanent resident status and 301.7701(b)-1(c) for substantial presence.

In practice, map your facts to the right status concept first, then calculate days if the Green Card Test does not resolve the result.

Flag same-year dual-test cases early#

If both tests may be met in the same year, treat that as a review flag. The IRS says the residency starting date is then determined under an earlier-of rule, and one possible date is the first day you were present in the United States during the year you pass the Substantial Presence Test. Mark dual-test years early so residency-start-date treatment gets handled deliberately.

Keep a one-page status memo#

A one-page status memo helps you and your preparer keep a clear, consistent position. Include:

- the tax year and calendar-year facts used

- whether the Green Card Test applies, and which record supports that call

- whether a Substantial Presence Test calculation is needed

- whether both tests may apply in the same year

- any escalation flags, especially residency starting date questions

Calculate your weighted day count the same way every year#

Consistency matters more than cleverness here. If you are using the Substantial Presence Test under IRC Section 7701(b)(3), use one repeatable worksheet and the same order every year: count raw U.S. presence days, apply the look-back weights, then test the result.

Use one repeatable calculation sheet#

Track three years: current year, first prior year, and second prior year. The test requires both at least 31 days in the current year and at least 183 weighted days across the three-year period.

Apply the weights the same way every time:

- current year: count 100% of days

- first prior year: count 1/3 of days

- second prior year: count 1/6 of days

A compact format helps prevent mixing raw and weighted counts:

| Look-back year | Raw days of presence in the United States | Weighted treatment | Weighted days used | Provisional effect |

|---|---|---|---|---|

| Current year | enter total | count 100% | raw total | Must be at least 31 days |

| First prior year | enter total | count 1/3 | raw total x 1/3 | Adds to 183-day test |

| Second prior year | enter total | count 1/6 | raw total x 1/6 | Adds to 183-day test |

Then sum the weighted days. If current-year days are under 31, this test is not met. If current-year days are 31 or more, compare the weighted total to 183.

Use the IRS example as a quick check: 120 current-year days, plus 40, which is 1/3 of 120, plus 20, which is 1/6 of 120, equals 180, which does not meet the test.

Keep the outcome provisional until inputs are verified#

The formula is simple, but mistakes usually happen in the input count. Before you use the result in a filing position, reconcile your day totals against your records and resolve any mismatch.

The IRS baseline is that physical presence at any time during a day is a day of presence, subject to exceptions. Keep the result provisional until you review excluded days, and use Publication 519 for additional exclusion details beyond the listed examples.

Common failure points to avoid:

- checking 183 before confirming the 31-day current-year condition

- blending raw and weighted counts in one running total

- using rough estimates instead of day-by-day records

- finalizing the result before exclusions are reviewed

If your total is close to the threshold, rerun it from your records using the same worksheet method instead of making the call from a rough count.

Related reading: A Guide to the UK's 'Split Year Treatment' for Tax Residency.

Exclude non-countable days carefully and keep proof#

Do not finalize your Substantial Presence Test from raw travel days alone. Exclude only days that clearly fit an IRS exception, and if you cannot support an exclusion with records, count the day until you can.

The baseline rule is broad: if you were physically present in the United States at any time during a day, that day generally counts. Exclusions come after that baseline count.

Know what the IRS is actually excluding#

Do not misread exempt individual. For this test, it is a technical day-counting category, not a statement that you are exempt from U.S. tax.

Visa class can matter. Foreign government-related individuals may fall into this category under A visa or G visa, except A-3 and G-5. Teachers or trainees temporarily present under J visa or Q visa can also fall into an exempt-individual category. When excluded-day treatment is unclear, check Publication 519 (U.S. Tax Guide for Aliens) before you finalize the count.

Handle commuting and transit days narrowly#

These exclusions apply only when the facts cleanly match the rule. Days commuting to U.S. work from a residence in Canada or Mexico can be excluded when you regularly commute. Transit days are excluded only when you were in the U.S. for less than 24 hours while traveling between two non-U.S. locations. Days in the U.S. as a crew member of a foreign vessel can be excluded. Days you could not leave the U.S. because of a medical condition that developed while you were in the U.S. can also be excluded.

If the facts are unclear, treat the day as countable until you can document the exception.

Build an exclusion log, not just a final number#

Do not stop at a final total. Keep a second table next to your day-count worksheet so each excluded day has a reason and supporting proof. The examples below are a practical log format, not a full IRS-required evidence checklist.

| Claimed exclusion | Example records to keep | Common challenge if reviewed |

|---|---|---|

| Exempt-individual day (A, G, J, or Q category) | Records showing visa class/status and date in question | Visa category is applied incorrectly |

| Regular commute from Canada or Mexico | Records showing recurring commute pattern and residence location | Commuting pattern is not regular |

| Transit under 24 hours between two non-U.S. locations | Itinerary/timing records showing transit facts | Timing or routing does not match the rule |

| Crew member of a foreign vessel | Records showing crew role and date | Crew role or vessel facts are unclear |

| Unable to leave due to medical condition developed in the U.S. | Records showing timing of condition and travel disruption | Timing of the condition is unclear |

Before you apply the 31-day and 183-day thresholds, reconcile each excluded date to source records. When treatment is ambiguous, use Publication 519 as your consistency check.

Set the residency starting date without guessing#

Once you determine that you are a U.S. resident for the year, set the residency starting date by rule, not by estimate. Under Treasury Regulation 26 CFR § 301.7701(b)-4, the date follows the test path you met.

This section applies to the first year of residency: you were not a U.S. resident during the preceding calendar year and are a U.S. resident for the current year.

| Test path | Residency starting date under 26 CFR § 301.7701(b)-4 | What to verify |

|---|---|---|

| Substantial Presence Test | The first day during the calendar year on which you are present in the United States | Your first U.S. presence date in the calendar year |

| Green Card Test | The first day during the calendar year you are physically present in the United States as a lawful permanent resident | A date where both physical presence and LPR status are true |

| Both tests met | The earlier of the two candidate first days | Both dates side by side before choosing the start date |

In dual-test years, do not pick one path and ignore the other. Track both candidate dates, then apply the earlier-of rule.

If a first-year election under IRC Section 7701(b)(4) may apply, treat it as an escalation item for professional review before filing. Or use a focused explainer like The 'First Year Election' for US Tax Residency: A Deep Dive.

If you are unsure about filing or reporting implications of the start date, escalate instead of making a best guess. Related: A Guide to Tax Residency in the Czech Republic for Nomads.

Build an audit-ready residency evidence pack#

You want a file that lets another person reproduce your residency result without guessing. A year-by-year folder is one practical way to do that.

What to include (minimum)#

| File item | What it supports |

|---|---|

| Travel log for the current year and, when relevant, the prior two look-back years | Lets you reconcile the year-by-year presence history |

| Days-of-presence worksheet for the United States | Shows the count used for the residency position |

| Visa or status records | Support counted and excluded days |

| Exact rule sources relied on, including IRS pages and Publication 519 | Shows the authorities used |

| Short assumptions log | Captures the assumptions used |

| Final reviewer note with open issues, resolutions, and escalation points | Summarizes the conclusion and remaining review items |

| First-year choice statement attached to Form 1040, if relevant | Supports a first-year choice filing position |

Put raw records before conclusions. First checkpoint: reconcile worksheet totals to the travel log before you use the result in a filing position.

Preserve the rule trail, not just the result#

Save the exact authorities you used, or at least the exact pages and the date you relied on them, so the file stays defensible if pages change later. Keep the legal anchor explicit: IRS residency rules for tax purposes are under Internal Revenue Code Section 7701(b). For day-count exclusions, keep the Substantial Presence Test materials and Publication 519 together with your records.

If this file depends on a residency starting-date decision from the prior step, keep a short note showing which test path controlled and why the start date follows from that path.

Log assumptions while facts are fresh#

Short, specific assumptions are more useful than broad notes. Record the issue, source, conclusion used, and supporting evidence. This matters most near thresholds. IRS examples show that a weighted three-year total of 180 days still does not meet substantial presence.

Second checkpoint: if you are testing first-year choice, confirm exempt-individual days were not included in that qualification count. Also note clearly that "exempt individual" does not mean exempt from U.S. tax.

End with a reviewer note#

Close with a one-page reviewer note that states your conclusion, controlling rule, key evidence, and any uncertainty. If a small day-count change could flip the outcome, or a key exclusion is uncertain, mark it for review before filing instead of leaving a silent assumption.

Before filing season, run your travel records through the Tax Residency Tracker so your day-count method and evidence pack stay consistent year to year.

Apply decision checkpoints to common freelancer situations#

These checkpoints matter most when your travel pattern is messy. Use them before you make more travel or year-end decisions. The goal is to document the residency path you can prove, then plan from that result.

| Situation | Checkpoint | Action |

|---|---|---|

| Green card plus heavy travel | Treat the Green Card Test and the Substantial Presence Test as separate residency topics | Keep separate analyses in the same annual file and document any residency starting date issue explicitly |

| Days packed around year boundaries | Lock the residency-status analysis before booking more travel | Use one dated worksheet, reconcile it to your records, and resolve conflicting records |

| Closer connection is not a casual fallback | Treat closer connection as a separate documented position | Build the primary residency file first and do not treat this toolkit as plug-and-play guidance |

| Choose the version you can prove | Use the interpretation you can substantiate | Pause and escalate before filing if the conclusion depends on undocumented dates, unclear status facts, or an exception you have not documented separately |

Green card plus heavy travel#

If you have a green card and heavy travel, review both paths before making year-end decisions. IRS Publication 4152 treats the Green Card Test and the Substantial Presence Test as separate residency topics, so do not assume one replaces the other.

Keep them as separate analyses in the same annual file. Then, if the result raises a start-date issue, document that next step explicitly because Residency Starting Date is its own topic in Publication 4152.

Days packed around year boundaries#

If your U.S. days cluster around year-end, lock your residency-status analysis before booking more travel. Use one dated worksheet, reconcile it to your records, and avoid planning from estimates.

This is not just a numbers checkpoint. It is a documentation checkpoint. Publication 4152 includes a Fact-Gathering Process, so resolve conflicting records before those conflicts turn into filing assumptions.

Closer connection is not a casual fallback#

If you plan to rely on a closer-connection position, treat it as a separate documented position, not an assumed backup. In this toolkit, closer-connection material is marked out of scope, including student-specific closer-connection content, so do not treat it as plug-and-play guidance here.

Build your primary residency file first, then document any separate exception position with the facts and authority you can support. If helpful, start with The 'Closer Connection' Exception: How to Avoid US Tax Residency Even if You Spend Time in the US and test it against your records.

Choose the version you can prove#

When facts are ambiguous, choose the interpretation you can substantiate, not the one that only lowers exposure. Publication 4152 includes both fact gathering and Consequences of Failure to File, which is a practical signal to prioritize a defensible position.

If your conclusion depends on undocumented dates, unclear status facts, or an exception you have not documented separately, pause and escalate before filing.

Know exactly when to bring in a tax professional#

Bring in a tax professional before filing when the result depends on exclusions, timing rules, or elections you cannot verify cleanly from IRS materials. If one assumption changes your filing position, treat that as a review trigger, not a judgment call.

Escalate early when any of these apply:

- your day count depends on disputed non-countable days, including exempt-individual days, regular commuting days, or under-24-hour transit days

- your status across the Green Card Test and the Substantial Presence Test is unclear

- your residency starting date is unclear

- first-year choice might apply, because eligibility and timing are strict:

- you do not meet the green card test or substantial presence test in the current year * you did not meet those tests in the prior year * you meet substantial presence in the following year * you have at least 31 consecutive days in the current year * you meet the 75% presence requirement after that period, with only up to 5 absence days treated as presence * you must attach a statement to Form 1040 to make the choice

- your situation depends on residency-rule details you cannot confirm from the IRS summaries you used

When you do escalate, send a focused brief, not a pile of screenshots:

- your status path so far

- your day-count table by year

- each claimed exclusion and supporting records

- your exact open questions

Attach the core documents you used to compute the position so the advisor can validate your assumptions quickly.

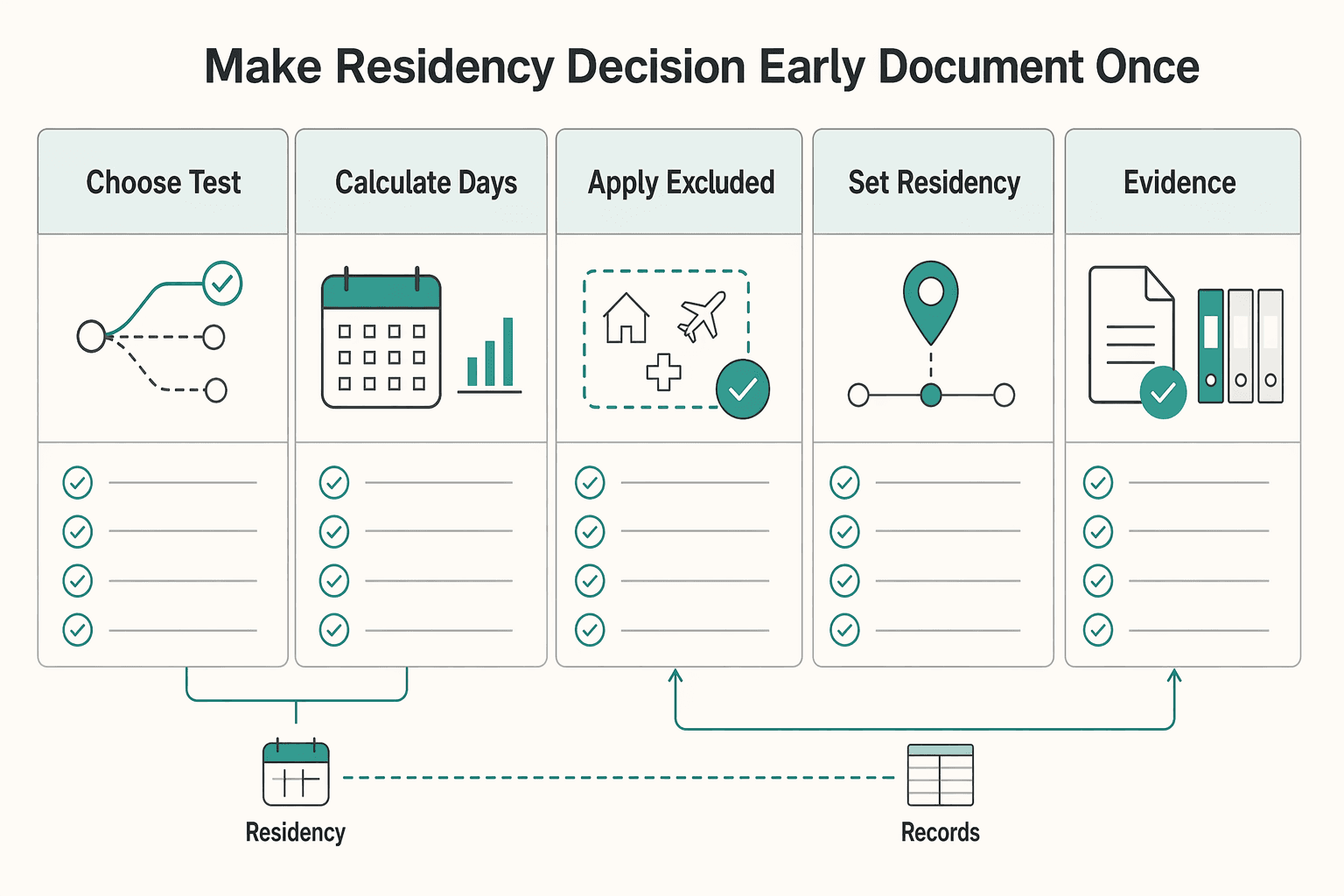

Make your residency decision early and document it once#

Make your U.S. tax residency call early each year, then document it in one place. The sequence is consistent: choose the right test path, run the day count correctly, apply exclusions, set the residency start date, and save the support.

- Choose the test path first.

- Calculate days under the right rule.

- Apply excluded-day rules carefully.

- Set the residency starting date.

- Archive the evidence you relied on.

Order matters. You can do clean math and still get the wrong result if you start on the wrong path.

If the Green Card Test applies, treat it as its own residency path. If you were a lawful permanent resident at any time in the calendar year, start with that analysis and verify your status document (Permanent Resident Card, Form I-551). If the Green Card Test is met and the Substantial Presence Test is not, residency starts on your first U.S. day as a lawful permanent resident.

If the Green Card path does not control, run the Substantial Presence Test the same way every year. You need at least 31 days in the current year and at least 183 days under the three-year weighted formula of 1, 1/3, and 1/6. Example: 120 days in each of 2023, 2024, and 2025 equals 180 weighted days, so that does not meet substantial presence.

Before finalizing, review excluded days. The IRS is explicit that not every physical day counts for substantial presence, and Publication 519 is the check when category treatment is unclear. Also, "exempt individual" here does not mean exempt from U.S. tax; it means certain days may be excluded from the count.

Do not guess on the residency starting date. IRS examples show you can cross the substantial presence threshold midyear while the residency starting date is earlier in that same calendar year. If timing changes your filing position, treat it as a review point.

Keep one defensible file: your day-count worksheet, reconciled travel records, status-path support, and a short note on exclusions or judgment calls. When facts are mixed, default to the position you can prove most clearly and escalate early.

For a step-by-step walkthrough, see Tax Residency in Croatia: A Guide for Nomads on the Adriatic.

If your residency outcome depends on mixed tests or disputed exclusions, talk with Gruv to pressure-test your workflow before you file.

Frequently Asked Questions

What is the look-back rule for U.S. tax residency?

Here, “look-back rule” refers to the Substantial Presence Test. It is a weighted three-year day-count method, not a separate formal IRS test name. You should also check the Green Card Test, because that is a separate path to U.S. tax residency.

Is U.S. tax residency really just the 183-day rule?

No. For the Substantial Presence Test, you must have at least 31 days in the current year and at least 183 days over the three-year weighted calculation. That is why a simple “under 183 days this year” conclusion can be wrong. See 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

How do I calculate the Substantial Presence Test step by step?

Add all U.S. presence days in the current year, then add 1/3 of days from the first prior year and 1/6 of days from the second prior year. If that weighted total is 183 or more, and you also have at least 31 current-year days, you meet the test. Then apply any exclusions you can support with your records.

Which days do not count as days of presence in the United States?

Some days are excluded, including regular commuting days from Canada or Mexico and U.S. transit days of less than 24 hours between two non-U.S. locations. Other exclusions may apply for exempt-individual or medical-condition grounds. If you claim excluded days on exempt-individual or medical-condition grounds, include Form 8843 with your return.

If I have a green card and also meet substantial presence, which rule controls my start date?

If you meet both tests in the same year, your residency starting date is the earlier applicable date. That timing can affect whether you are treated as dual-status in an arrival or departure year. If the date changes your filing position, treat it as a review point rather than a guess.

What documents should I keep to support my residency position?

Keep records that substantiate the position on your return, such as your day-count worksheet, the travel records you relied on, and copies of forms tied to your claim. Well-organized records make return prep and exam response easier.

Which parts of residency timing rules are still unclear enough that I should ask a professional?

Ask for help when the result depends on disputed excluded days, unclear residency starting dates, or arrival and departure timing that may create dual-status treatment. Escalate if you plan to claim the closer connection exception (including timely Form 8840 filing) or raise treaty-residency questions, because those outcomes can differ from Internal Revenue Code residency results.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

The 'Closer Connection' Exception: How to Avoid US Tax Residency Even if You Spend Time in the US

If your U.S. travel is increasing, the real risk is not your intent. It is drifting into the wrong filing posture because you waited too long to make a clear decision. Use this section as a practical framework to decide early, document your position, and avoid a last-minute scramble.