Quick Answer

Authors audit Hollywood accounting in book publishing deals by fixing the royalty base, limiting deductions to named and record-backed items, securing a usable audit clause, and checking each royalty statement against the contract. The article recommends a three-phase process: vet the publisher before negotiations, fortify the money terms in the agreement, and document every review cycle after signing.

Publishing contracts do not reward optimism. They reward clarity, control, and records you can verify. Yet when a book deal is on the table, many experienced professionals still give up that control by accepting vague accounting terms and contracts built to favor the publisher.

The fix is not paranoia. It is framing. Once you stop thinking like a hopeful author and start thinking like the manager of a business asset, the deal looks different. The manuscript is the product, but your intellectual property is the asset. Protecting it calls for the same discipline you would bring to any other high-stakes agreement.

This guide lays out a three-phase approach to protect your financial position. The goal is simple: move from hoping the accounting will be fair to setting up terms and review habits that let you test what you are paid.

Phase 1: Pre-Negotiation Due Diligence#

Before you discuss terms, decide what evidence would make you trust a publisher and what would make you walk away. That is a practical defense against unclear reporting. Do not negotiate from hope. Negotiate from a written objective and a clear no.

Vet the publisher with evidence, not reputation#

Reputation is not enough here. Start a one-page risk tracker before the first call. Log the publisher or imprint, the date checked, who answered, what payment artifact you saw, what rights answers you got in writing, and your current risk note.

A useful checkpoint is a real royalty statement or spreadsheet example. The point is to see how reporting actually works before you sign. If they cannot explain what the statement shows, or they dodge written questions about subsidiary rights, treat that as a live risk.

| Shortlist item | Transparency signals | Royalty reporting quality | Rights track record | Dispute responsiveness |

|---|---|---|---|---|

| Publisher A | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification |

| Publisher B | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification |

| Publisher C | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification | Current benchmark pending official verification |

That early file gives you something concrete to compare once the deal language shows up.

Frame your manuscript as an asset#

Do not wait for the publisher to define your value. Prepare a short negotiation brief for your agent or for yourself that states your objective, the rights you are prepared to license, and the questions you need answered in writing. Include your plan for subsidiary rights so your position stays consistent across conversations.

Set your non-negotiables before emotion enters#

This is the point where discipline matters most. Write down the outcomes you can accept and the terms that end talks. For any monetary cap or escalation trigger, insert "Current threshold pending official verification" and do not let anyone fill it from memory.

One practical rule matters more than the rest: be ready to walk away if the answers stay vague. Negotiation can burn hours and still produce zero dollars, so protect your time as carefully as your earnings.

You might also find this useful: The Best Platforms for Self-Publishing Your Book. Want a quick next step for book-finance admin? Try the free invoice generator.

Phase 2: Contractual Fortification#

Turn your Phase 1 decisions into exact contract language, because unclear royalty bases and open-ended deductions are where opaque accounting risk enters the deal.

Lock the royalty base before you argue percentages#

Set the royalty base first. A high percentage on a weak base can still pay less than a lower percentage on a clear base. In profit-participation systems, net profit is usually the hardest base to verify because it depends on internal cost allocations.

Ask for cover-price royalties where possible. If the draft uses net receipts, require a written definition that states what counts as receipts, which deductions are allowed, how returns and discounts are treated, and whether channel or sub-license sales are calculated differently. If terms are left as "standard practice" or internal policy, expect disputes later.

Use this table to pressure-test the draft before redlines:

| Royalty basis | What the base means in practice | What to verify before signing | Placeholder model |

|---|---|---|---|

| Cover price | Royalty tied to listed sale price, not internal cost allocations | Confirm which editions/channels use this basis and how returns affect payment timing | Cover price: Current sample price pending official verification |

| Net receipts | Royalty tied to money received after contract-defined deductions | Define each deduction, discount treatment, returns, channel-specific sales, and sub-license receipts | Deduction scenario: Current deduction scenario pending official verification |

| Net profit | Royalty tied to profit after costs that may be hard to test | Either define every cost/allocation rule and review right, or reject this base | Profit scenario: Current deduction scenario pending official verification |

Keep this rule: do not negotiate percentage until the base is fixed in writing.

Give counsel a deduction checklist, not a general complaint#

Use a clause checklist your agent or counsel can mark up line by line:

| Checklist item | What to state |

|---|---|

| Named deductions only | If a deduction is not listed, it is not allowed. |

| Record-backed deductions | Each deduction needs underlying records you can inspect. |

| Cap logic | Where a category is allowed, set a written cap or formula using "Current cap pending official verification." |

| No vague catchalls | Strike broad buckets such as overhead, internal allocations, affiliate service fees, administration, or "other costs" unless narrowly defined. |

| Returns and discounts | State exactly how they affect the royalty base. |

| Channel and sub-license treatment | State how direct, retail, export, audio, foreign-rights, and other licensed sales are handled when relevant to your deal. |

This matters because opaque profit systems have been associated with inflated expenditures and inter-affiliate charges. Your contract should make those items testable, not discretionary.

Make the audit clause usable, not ceremonial#

Treat audit language as an execution plan, not a formality. Audit rights that are too narrow or too expensive often fail in practice.

| Clause point | What to include |

|---|---|

| Scope of records | Include statements, supporting records, and deduction calculations. |

| Affiliate/sub-license visibility | If revenue flows through related entities or outside licensees, include access needed to test those flows. |

| Response timeline | Insert a specific production deadline: Current response timeline pending official verification. |

| Dispute path | Define correction, repayment, and escalation steps for unresolved issues. |

| Cost shift trigger | Require the publisher to pay audit costs above Current threshold pending official verification. |

Ask for these points in the clause:

- Scope of records. Include statements, supporting records, and deduction calculations.

- Affiliate/sub-license visibility. If revenue flows through related entities or outside licensees, include access needed to test those flows.

- Response timeline. Insert a specific production deadline: Current response timeline pending official verification.

- Dispute path. Define correction, repayment, and escalation steps for unresolved issues.

- Cost shift trigger. Require the publisher to pay audit costs above Current threshold pending official verification.

Enforcement can work, but only if your clause makes verification realistic before a full dispute.

Related: How to Manage Bookkeeping for Your Freelance Business.

Phase 3: Post-Signature Verification#

Your contract only protects you if you run the same verification routine every statement cycle: intake, review, reconcile, action. Treat each cycle as operating work, not admin cleanup.

Intake and review#

Treat every royalty statement as a contract artifact. Archive the statement, remittance advice, and cover email in a period-labeled folder. If a statement or payment-change request arrives by email, verify the sender is using a real email address before acting. Scam controls reduce risk, but they do not eliminate it.

| Statement check | What to verify |

|---|---|

| Sales channels | Do listed channels match the editions and territories being exploited? |

| Returns and reserves | Are returns separate from reserves, and are reserve movements explained period to period? |

| Deductions | Does each charge map to a named deductible category in your agreement? |

| Rights income | If audio, foreign, book club, or other rights were licensed, is that income appearing when expected? |

| Payout timing | Were statement and payment issued when the agreement says they should be? |

| Math check | Recalculate a sample of line items instead of relying on the final total. |

Review each statement against the exact Phase 2 terms, especially net receipts, named deductions, reserves, rights reporting, and payout timing. Use one checklist every cycle:

- Sales channels: Do listed channels match the editions and territories being exploited?

- Returns and reserves: Are returns separate from reserves, and are reserve movements explained period to period?

- Deductions: Does each charge map to a named deductible category in your agreement?

- Rights income: If audio, foreign, book club, or other rights were licensed, is that income appearing when expected?

- Payout timing: Were statement and payment issued when the agreement says they should be?

- Math check: Recalculate a sample of line items instead of relying on the final total.

Reconcile and document#

A single statement is a snapshot; your leverage comes from trend records. Reconcile each cycle against prior periods and log unexplained changes, missing categories, or timing drift.

Keep a simple audit trail with four working files:

- Statement archive: every statement, payment stub, and attachment.

- Variance log: period-to-period changes and your notes.

- Correspondence log: dates, contacts, requests, and replies.

- Unresolved items register: open questions, requested support, and next follow-up date.

Weakly defined backend percentages are hard to interpret in isolation, so this running history is what makes the numbers usable.

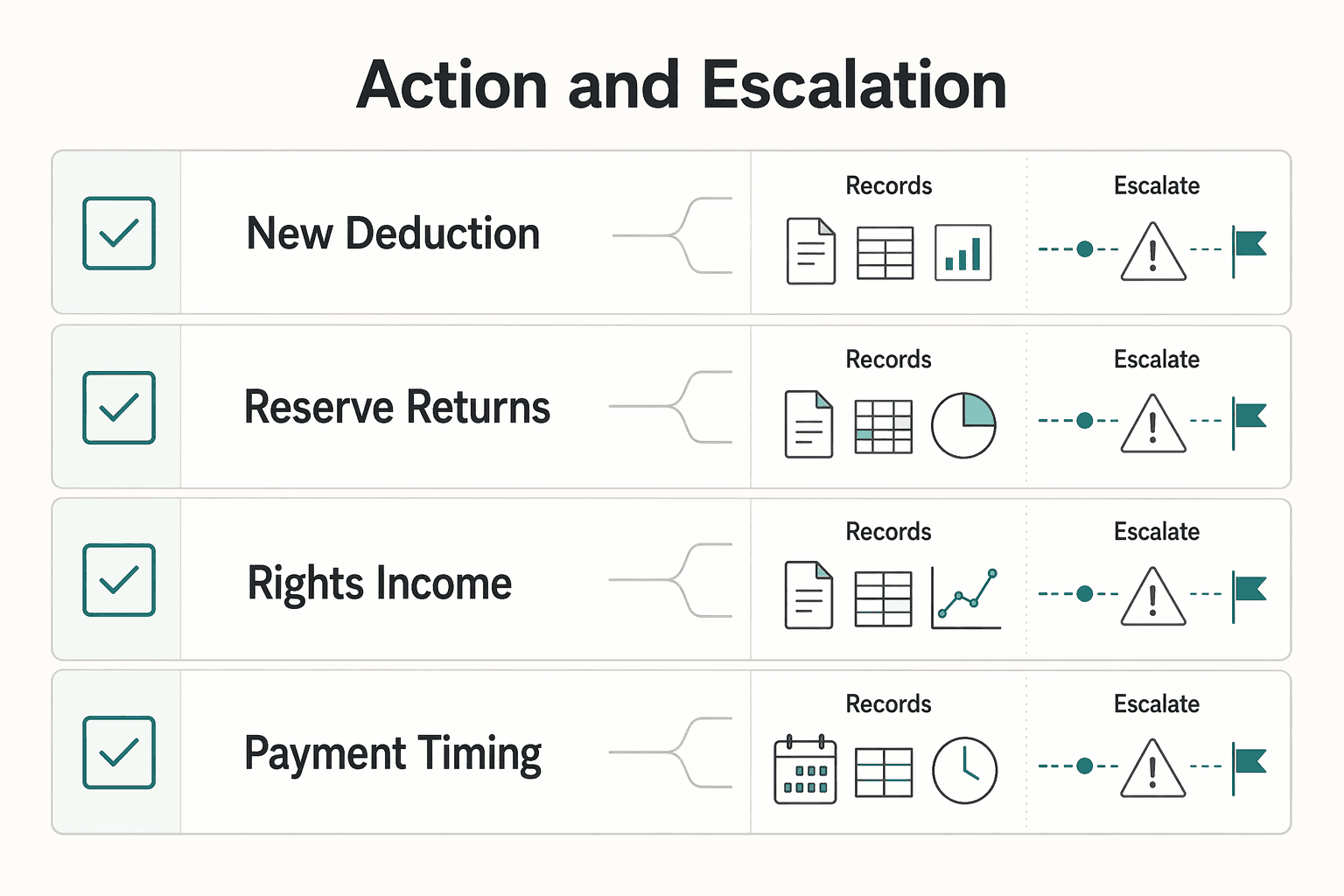

Action and escalation#

Escalate in stages so your record stays clear and credible.

- Formal query: Send a written query that cites statement period, line item, and contract clause.

- Cure window: Use the contract cure window; if none is stated, set an internal deadline such as Current threshold pending official verification.

- Professional review: If support remains incomplete, escalate to your agent, lawyer, or royalty accountant.

- Audit invocation: If unexplained variance, delay, or missing support crosses Current threshold pending official verification, invoke the audit clause.

| Anomaly | Likely cause | Evidence to request | First response |

|---|---|---|---|

| New deduction label appears | Charge outside named categories or relabeled internal cost | Deduction calculation and supporting records | Formal query tied to deduction clause |

| Reserve for returns stays high or rises unexpectedly | Timing issue, opaque reserve policy, or over-withholding | Reserve rollforward by period | Ask for reserve calculation and release logic |

| Rights income missing | Reporting lag, sublicense delay, or omitted income | License summary, receipt dates, and statement support | Query rights accounting and expected reporting period |

| Payment timing slips | Admin delay or disputed internal processing | Statement issue date, payment date, remittance detail | Cite timing clause and request correction |

If a statement cannot be tested, it cannot be trusted.

For a step-by-step walkthrough, see A Guide to 'Accrual' vs. 'Cash Basis' Accounting for a Small Agency.

Conclusion: You Are the Ultimate Guardian#

The practical answer to opaque publishing accounting is not suspicion for its own sake. It is control. If you vet the deal before signing, tighten the money language in the contract, and review every statement against that language, you can improve payment protection, cash flow visibility, and your ability to defend your rights over time.

Phase 1 builds your due diligence file. Phase 2 locks the terms that decide how money is calculated. Phase 3 tests what actually gets reported and paid. That mirrors a useful audit habit: even the IRS Entertainment Audit Technique Guide begins with "Planning the Audit," including "Information to Obtain" and "Recordkeeping," then calls out "Royalties and License Fees" and "Advances" as review areas. Use that as a prompt for discipline, not as legal authority. The guide itself says it is not an official pronouncement of law, and it warns that technical accuracy may change after its 3/20/2023 revision date.

What to do now:

- Build one deal file with the draft contract, signed agreement, rights grant, royalty clause, net receipts definition if used, advance terms, statements, remittances, and key emails.

- Decide your negotiation priorities before the next call. For example, prioritize royalty basis first, deduction limits second, and audit and record access third.

- Set a statement review routine. Compare each report to the signed clause, check that the categories stay consistent, and keep notes so you can spot drift instead of relying on memory.

- Be strict about freshness. If a source is marked as more than 23 years old, treat it as background, not current operating guidance.

If you want the exact execution steps, go back to the phase sections and the FAQ. That is where this loop becomes a repeatable process to protect your author earnings.

If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

Frequently Asked Questions

What are “net profits” in a book publishing contract?

The article does not treat net profits as a universal legal definition. It says the term must be defined in the contract itself, and notes that profit-based systems are usually the hardest to verify because they depend on internal cost allocations.

How do you protect yourself from hollywood accounting in book publishing?

Use the contract as your checkpoint list and keep strong records from day one. Save statements, remittances, and correspondence, compare each period against the agreement, and watch for missing rights income, timing changes, or new deduction labels without a clear contract basis. If the contract includes an underpayment trigger, verify the exact number in the signed deal before relying on it.

What are the most important clauses in your publishing contract?

The article does not claim one mandatory clause set for every publisher. It prioritizes the clauses that control money flow and verification, including how advances are paid, when an advance is earned out, how royalties or license fees are reported, how deductions are handled, and what records are available for review. Any percentage or trigger should be confirmed in the signed agreement.

How are royalties calculated?

Royalties are calculated according to the contract, not a single universal formula. A practical check is to trace the payment flow line by line from advance installments to reported royalties or license fees, and confirm whether accrued royalties have covered the advance before expecting additional royalty cash. If you cannot follow the move from prior balance to current balance, ask for clarification before treating the figure as final.

Is a book advance deducted from royalties?

A book advance is an upfront prepayment of future royalties, so you usually do not receive additional royalty cash until the advance has earned out. The article notes that payment timing varies by publisher and contract, and that advances may be split into 2 or 3 installments. It also says to confirm whether the money reaching you is gross or net of representation costs.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- egrove.olemiss.edu/cgi/viewcontent.cgitrusted

- govinfo.gov/content/pkg/GOVPUB-Y1_2-ac427e66cdd2ff1a0945...trusted

- huskiecommons.lib.niu.edu/cgi/viewcontent.cgitrusted

- irs.gov/pub/irs-pdf/p5774.pdftrusted

- law.ucla.edu/sites/default/files/PDFs/Ziffren/Backend%20-...trusted

- lawlib1.lawnet.fordham.edu/contractscasebook.org/casebook-builds/Edited...trusted

- nsuworks.nova.edu/cgi/viewcontent.cgitrusted

- authorsalliance.org/wp-content/uploads/2018/10/20181003_AuthorsA...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Freelance Bookkeeping for Faster, Safer Client Payments

Control over cash starts with records you trust. When entries are current, categorized, and easy to trace, you spot risk earlier and make calmer decisions about follow-up, spending, and month close.

Book Advances and Royalties for Authors Who Need Steady Cashflow

Treat your **book advance** as business capital before you spend any of it. The first risks show up immediately: **publishing contract** terms, tax exposure, and cashflow control.