Quick Answer

U.S. founders abroad should handle GILTI in three steps: confirm they are a U.S. person with ownership in a foreign corporation that meets the CFC test, build a reconciled model from actual records and required forms, and then compare default treatment, a Section 962 election, or early structuring. Escalate early if distributions, multiple CFCs, tested losses, uncertain foreign tax treatment, or missed Form 5471 filings are involved.

From Anxiety to Agency: A Founder's 3-Step Playbook for Taming GILTI#

You need to make three decisions, in order. First, whether you are in scope. Second, which inputs create a current inclusion. Third, whether default treatment, a Section 962 election, or a structuring conversation is the right next move. If the global intangible low-taxed income, or GILTI, rules apply, your goal is a clear scope decision, a supportable exposure model, and a defined point where you escalate.

That order matters. Founders often jump straight to "what rate will I pay?" before they answer the threshold ownership and entity questions. That is how a manageable filing issue turns into a messy modeling exercise built on the wrong facts. Treat this like a decision tree. First determine whether the regime is even on the table, then build the numbers from records you can defend, then compare the treatment paths with enough detail to understand the tradeoffs.

Step 1#

Start with the eligibility screen before you do any tax math. The regime applies to a U.S. shareholder of a foreign corporation that is a CFC. Ask:

| Screen item | Who or what | Threshold or definition |

|---|---|---|

| U.S. person status | You | U.S. person for U.S. tax purposes |

| Foreign corporation status | Company you own | Organized outside the United States and treated as a corporation for U.S. tax purposes |

| CFC ownership test | U.S. shareholders | Own more than 50% of the foreign corporation; a U.S. shareholder holds at least 10% of voting power |

- Are you a U.S. person for U.S. tax purposes?

- Do you own shares in a foreign corporation that is organized outside the United States and treated as a corporation for U.S. tax purposes?

- Do U.S. shareholders own more than 50% of that foreign corporation, with a U.S. shareholder including a U.S. person that holds at least 10% of voting power?

If all three answers are yes, treat the company as in scope and move to input collection. If any answer is no, confirm classification before you model anything. If the CFC test is the sticking point, use: What is a 'Controlled Foreign Corporation' (CFC) for a US Shareholder?

The practical point is to slow down and verify each answer with documents, not memory. "I think I own around that amount" is not a reliable starting point if there were founder issuances, investor rounds, option activity, or reorganizations. Before you do anything else, pull the cap table, share certificates or equivalent ownership records, formation documents, and any amendments that changed voting rights or ownership percentages. If the legal entity was set up quickly and the records live across email threads, your first job is to get the ownership story into one clean file.

This is also where classification mistakes can derail the rest of the analysis. A founder may know the company is organized outside the United States and still assume that ends the question. It does not. For this screen, you are not asking only where the company was formed. You are asking whether it is a foreign corporation and treated as a corporation for U.S. tax purposes. If that treatment is unclear, stop there and resolve it before building a model. A polished spreadsheet based on the wrong entity classification is still wrong.

A useful operating rule is to answer the Step 1 questions in sequence rather than all at once:

- Confirm your own status as a U.S. person for U.S. tax purposes.

- Confirm the entity you own is a foreign corporation for this purpose.

- Confirm whether the CFC ownership test is met.

That sequencing keeps you from spending time on the CFC calculation when the earlier gating item is unresolved. It also makes the file easier to review if you later hand it to a professional. A short memo, or even a one-page note showing how you answered each question with the supporting records listed beneath it, can save real time downstream.

Common failure modes at this stage are simple but expensive: using an outdated cap table, ignoring voting rights, assuming local-law labels control U.S. tax treatment, or treating ownership as static when there were changes during the year. Even if the final answer is still yes, you want the basis for that yes to be visible and reviewable. If a future filing position depends on the company being in or out of scope, you do not want that conclusion resting on a vague assumption made in a rush.

If the answer is yes across the board, do not linger here. The goal of Step 1 is not to write a dissertation on ownership. It is to establish a supportable scope conclusion so you can move to the inputs that drive the current inclusion.

Step 2#

Once you are in scope, build the inputs before you debate rates. Under current section 951A, a U.S. shareholder of a CFC includes net CFC tested income in gross income.

| Record or form | Role in Step 2 |

|---|---|

| Ownership records | Pull from source documents |

| Trial balance | Pull the full year trial balance |

| Year-end financials | Pull year-end financial statements |

| Fixed-asset detail | Pull fixed-asset detail rather than relying on a summary line in the financials |

| Foreign tax records | Pull early, not at the end |

| Form 5471 Schedule I-1 | Confirm the CFC-side inputs |

| Form 8992 | Confirm the shareholder computation |

| Rough model workpaper | Show how the rough model was built |

Start from the company's profit base after U.S. tax adjustments, then work through tested income and tested loss amounts and the asset-based adjustment concept in the formula. Do not assume the inclusion equals local book profit. Pull from source documents: ownership records, trial balance, year-end financials, fixed-asset detail, and foreign tax records.

For filings, confirm the CFC-side inputs on Form 5471 Schedule I-1 and the shareholder computation on Form 8992 and its schedules, which IRS materials still label for GILTI. If those do not reconcile, the number is not ready for a real decision. As a practical checkpoint, if your rough model shows positive tested income and no planning changes, expect a current U.S. inclusion and move to Step 3.

This is the part founders tend to underestimate because the words "tested income" sound like a single line item. In practice, Step 2 is a build-and-reconcile exercise. You are assembling the number from records created for different purposes, then checking that the tax filing mechanics tell the same story. The right question is not "what did the company make?" but "what amount survives the U.S. tax adjustments and reconciles across the forms and support?"

A practical workflow looks like this:

- Pull the full year trial balance and year-end financial statements.

- Tie those records to the ownership period and the entity you screened in Step 1.

- Pull fixed-asset detail rather than relying on a summary line in the financials.

- Pull foreign tax records early, not at the end.

- Map the CFC-side amounts to Form 5471 Schedule I-1.

- Map the shareholder-level computation to Form 8992.

- Check that your workpapers, forms, and rough model all point to the same underlying inputs.

That sequence matters because it reduces the chance that you start with a conclusion and then force the forms to match it. If you wait until the end to pull fixed-asset detail or foreign tax records, you often discover that your rough model was rough in the wrong places.

The working rule to keep in mind is simple: local accounting profit is not the answer. It may be a starting point, but it is not a substitute for U.S. tax inputs. A founder looking only at local financial statements can easily conclude that the problem is small, large, or nonexistent and still be wrong, because the tested income computation and the related form mechanics were never built from the actual records.

Your support file should be organized like an evidence pack, not a folder of unrelated PDFs. At minimum, keep these items together:

- ownership records

- trial balance

- year-end financials

- fixed-asset detail

- foreign tax records

- draft or filed Form 5471 Schedule I-1

- draft or filed Form 8992

- any workpaper showing how the rough model was built

If a number cannot be traced back to one of those items, flag it. Do not smooth over missing support with an estimate and then forget that you estimated it. A model can still be useful if one line is provisional, but only if you label the uncertainty clearly enough that it drives the next action.

Another useful discipline is to separate "model complete" from "model decision-ready." A model is complete when every key input has been pulled and placed somewhere. It is decision-ready when the inputs reconcile across the documents that matter. Those are not the same thing. Many founder-built models get to complete but not decision-ready because the Form 5471 Schedule I-1 numbers do not line up with the shareholder computation on Form 8992. When that happens, do not argue over the rate implications yet. Fix the reconciliation first.

The other operational point is timing. Step 2 is easier when you gather the records while the year-end information is fresh and before distribution planning hardens. If you already know there are planned distributions, multiple CFCs, tested losses, or foreign tax uncertainty, treat those as escalation signals while you are building the inputs, not after. The reason is practical. Those facts affect whether your rough model is enough to support a decision or only enough to tell you that you need help.

As a founder, the checkpoint you want is modest but clear. If your rough model shows positive tested income, your records support that result, and no planning changes are being implemented, move to Step 3 on the assumption that there will be a current U.S. inclusion. That does not tell you the best treatment path. It tells you the issue is real enough that it will not disappear on its own.

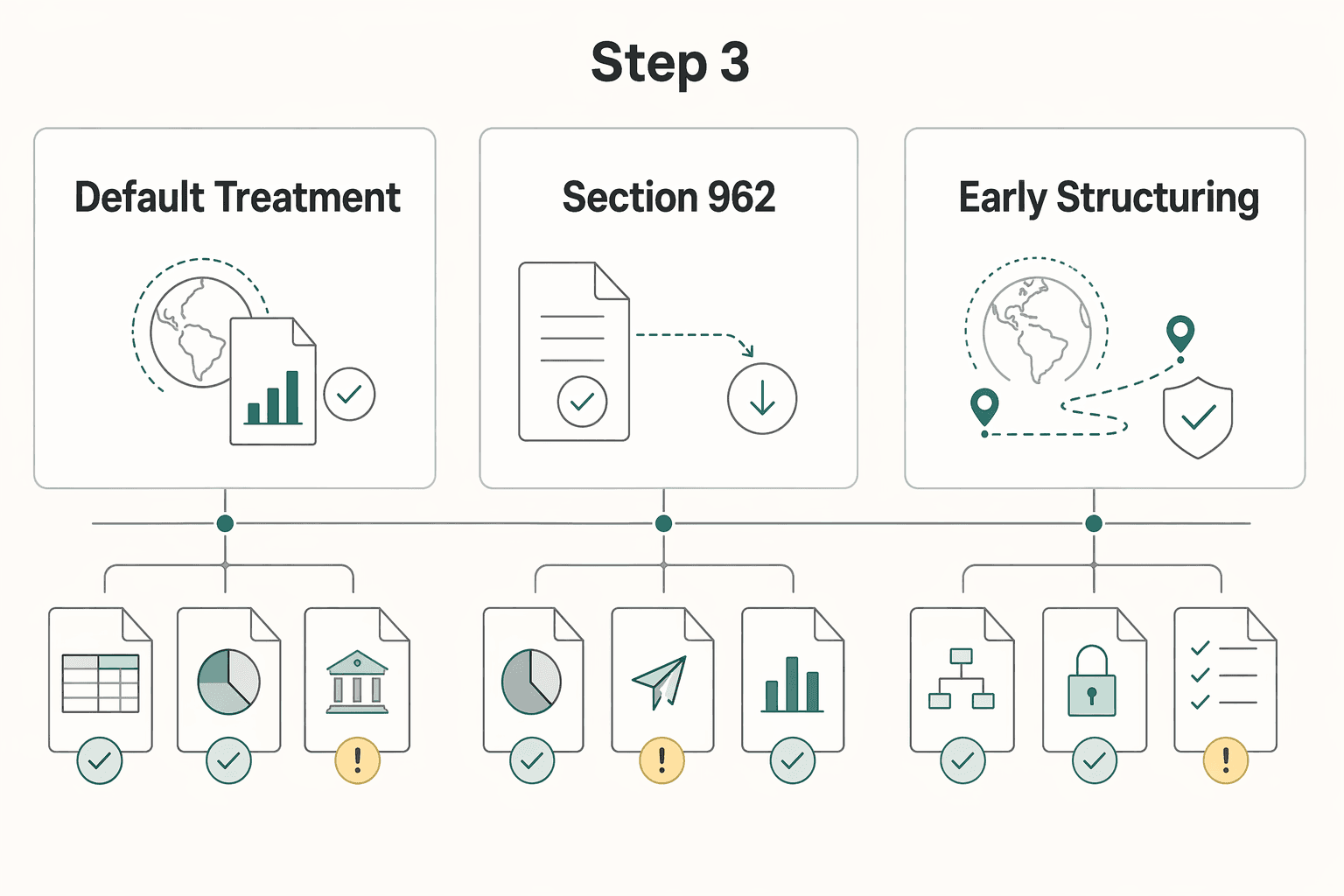

Step 3#

The real decision here is treatment design, not "pay vs avoid." Compare default treatment, a Section 962 election, and early structuring against credit usability, distribution consequences, and filing burden.

For 2026 planning, verify section 250 assumptions carefully. IRS Form 8993 instructions state the percentages change after January 1, 2026, with deductions reduced to 33.34% and 40% thereafter.

| Path | Eligibility | Current U.S. tax treatment | Credit usability | Distribution consequences | Compliance burden |

|---|---|---|---|---|---|

| Default treatment | Individual U.S. shareholder with a current inclusion | Inclusion under section 951A on the individual path | Do not assume corporate-style section 960 foreign tax credit treatment | No Section 962-specific distribution rule, but earnings tracking still matters | Baseline CFC filings |

| Section 962 path | Individual U.S. shareholder making a valid election | Taxed as if amounts were received by a domestic corporation under section 962 | Corporate-style foreign tax credit treatment may apply; Form 1118 is required if claiming that treatment | Later distributions can be included again in gross income to the extent distributed E&P exceeds tax paid | Higher, with election support plus Form 8993 and often Form 1118 |

| Early structuring path | Usually before formation or before facts harden | May change entity status, CFC status, or inclusion outcome based on facts | Depends on structure, local law, and shareholder profile | Depends on structure and earnings history | Front-loaded and advisor-heavy |

Use Section 962 as a serious modeling path, not as an automatic default. Escalate early when the facts include planned distributions, multiple CFCs, tested losses, or uncertain foreign tax treatment.

The practical mistake here is turning Step 3 into a slogan. Founders hear that a Section 962 election can improve the result in some cases and start treating it as the standard answer. Others hear that restructuring might solve the problem and jump into entity conversations before they have a stable Step 2 model. Both reactions skip the actual decision framework.

You are not just comparing current tax. You are also comparing whether foreign tax credit treatment is usable on the facts you actually have, what later distributions may do, and how much filing and support burden you are taking on. That is why Step 2 has to come first. A treatment comparison built on unreconciled inputs is just a more sophisticated guess.

For the default treatment path, the main discipline is not to import corporate assumptions into an individual result. If you are an individual U.S. shareholder with a current inclusion, model that path on its own terms and resist the temptation to assume corporate-style foreign tax credit treatment automatically travels with it. The attraction of this path is that it starts from the baseline CFC filing framework. The tradeoff is that simplicity on the current-year filing side does not mean the economic result is always the same as other paths.

For the Section 962 path, take the election seriously enough to model both the current-year effect and the later distribution consequences. Founders often stop at the first comparison point, which is the current inclusion. But the file cannot stop there. If later distributions can be included again in gross income to the extent distributed E&P exceeds tax paid, then planned distributions are not a side note. They are part of the decision. If you expect distributions, that fact belongs in the model before you decide that the Section 962 path is attractive.

The compliance burden matters too. A path that looks cleaner in a rough spreadsheet can become much heavier once election support, Form 8993, and often Form 1118 are in view. That does not make the path wrong. It means the compliance cost is part of the decision, especially if your records are not already organized well enough to support those filings.

For the early structuring path, the key question is timing. This is usually a before-the-facts-harden conversation, not a cleanup exercise after a year has already run with ownership, entity status, and earnings history in place. That is why "early" matters more than "structuring" in the label. If you are still at formation or before the ownership and operating pattern are locked in, it may be worth discussing whether the current structure is creating a result you did not intend. If the facts are already baked and filings are due, the right move may be to stabilize the current-year treatment first and discuss future changes separately.

A grounded way to use Step 3 is to write down the comparison criteria before you compare the paths:

- current inclusion under the actual Step 2 model

- likely foreign tax credit treatment based on the path being modeled

- whether distributions are planned

- whether multiple CFCs or tested losses complicate the picture

- whether your records are strong enough to support the added filings

That list does not answer the question for you, but it prevents the most common bad habit: choosing the path with the most appealing single feature and ignoring the rest of the file.

And for 2026 planning, do not reuse an old model without rechecking the section 250 assumptions. If your spreadsheet still reflects pre-2026 thinking because it was copied forward from an earlier year, verify it against the Form 8993 instructions before relying on it. This is exactly the kind of stale assumption that makes a model look polished while quietly pushing you toward the wrong treatment choice.

Frequently Asked Questions

What do founders most often get wrong?

Founders most often test business size instead of ownership structure. They also model from local accounting profit without validating U.S. tax inputs and sometimes reuse pre-2026 section 250 assumptions without rechecking Form 8993 instructions. The safest sequence is ownership and classification first, reconciled inputs second, treatment comparison third.

Which forms and records should you confirm with a professional?

At minimum, confirm your Form 5471 filing category and schedules, including Schedule I-1. Then confirm whether Form 8992, Form 8993, and Form 1118 apply to your facts. Keep a clean support file with ownership records, financials, asset detail, foreign tax records, and a distribution ledger so a reviewer can trace the file from ownership to forms to planned distributions.

When should you escalate to a cross-border tax advisor?

Escalate when you have multiple entities, multiple owners or share classes, tested losses, planned distributions, or unclear foreign tax treatment. Escalate immediately for missed Form 5471 filings because an initial $10,000 penalty per form per year may be assessed, with continuation penalties up to $50,000. As a practical rule, escalate once the issue is no longer a single-company, single-path modeling exercise.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

What Is a Controlled Foreign Corporation (CFC) for a U.S. Shareholder?

**If your foreign company might raise a CFC question for U.S. tax purposes, do not guess.** Get to a documented yes or no with a qualified advisor. In practice, that means confirming three things in order: how the entity is being treated for the U.S. tax review, how ownership and control are being analyzed, and what compliance or filing steps, if any, apply this year. Keep those frameworks separate, too. NYSE "[controlled company](https://www.sec.gov/Archives/edgar/data/1977102/000119312523254724/d507917d424b4.htm)" language in SEC materials is not the same as U.S. tax CFC analysis, and mixing them creates false confidence fast.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.