Quick Answer

Start with CRA’s gates before any deposit: confirm you are eligible to open, then verify FHSA room across every provider in one ledger. In Canada, room is shared, so extra accounts do not create extra contribution capacity, and excess amounts can trigger monthly tax while unresolved. Before you request funds, re-check that your purchase still fits qualifying-withdrawal conditions and that your residency status still supports it. If residency may shift, pause new contributions and reassess your account mix.

The FHSA for Global Professionals: A Strategic Guide to Canada's Most Powerful Savings Account#

For most people considering the first home savings account fhsa canada, the safest sequence is simple: confirm you can open the account, confirm your room, confirm withdrawal eligibility, then fund it. The most expensive mistakes usually happen when contributions come first and rule checks happen later, after residency, timing, or purchase plans have already changed.

| Order | Question | Check before funding |

|---|---|---|

| 1 | Can you open the account now? | Confirm you are a qualifying individual on the day you open the account |

| 2 | How much room do you actually have across all FHSAs? | Confirm current-year room, carryforward, and total contributions across all FHSAs |

| 3 | Is your intended use likely to qualify when the time comes? | Check residency, qualifying-home conditions, and the current CRA timing condition for purchase or build completion [verify current CRA threshold/date before submission] |

| 4 | Which account should hold which part of your home-buying cash? | Decide what belongs in the FHSA, RRSP with HBP, and TFSA |

That order matters more than provider choice, app design, or even investment selection. If you get the sequence wrong, the problem usually is not that the account itself failed you. It is that money went into a plan before the rules around opening, room, or withdrawal were checked against your actual situation.

For global professionals, that gap can widen quickly. Your work location can change. Tax residency can change. A purchase plan that looked realistic a few months ago can become uncertain by the time you are ready to move funds.

A clean FHSA process is not complicated, but it does need discipline. You want one decision chain that answers four questions in order:

- Can you open the account now?

- How much room do you actually have across all FHSAs?

- Is your intended use likely to qualify when the time comes?

- Which account should hold which part of your home-buying cash?

If you can answer those questions before the first contribution lands, you remove most of the avoidable risk. If you answer them after deposits are already spread across providers, or after your residency has changed, you are usually trying to repair a plan instead of running one.

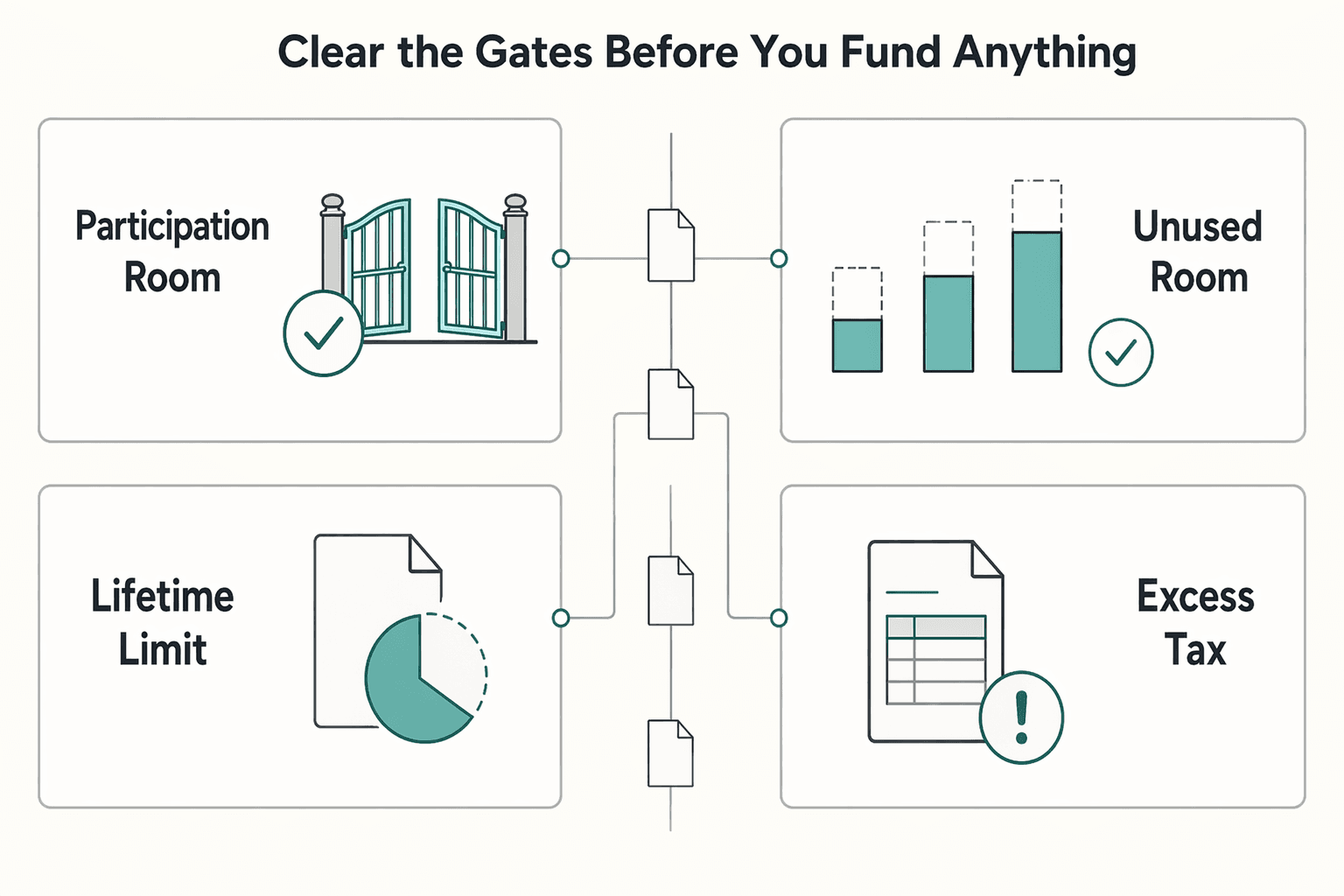

Clear the gates before you fund anything#

Start with CRA's opening gate. You must be a qualifying individual when you open the account, including being a resident of Canada and being 71 or younger on December 31 of that year. The first-time buyer test also applies to the preceding four calendar years.

| Rule | Amount | Article note |

|---|---|---|

| Participation room in the year you open your first FHSA | $8,000 | Shared across all FHSAs |

| Unused room carryforward | Up to $8,000 | Track use in one master contribution ledger |

| Lifetime limit | $40,000 | Opening accounts at multiple institutions does not increase capacity |

| Excess tax | 1% per month | Applies to the highest excess amount for each month an overcontribution remains |

Treat that opening gate as a live eligibility check, not as something you vaguely remember from a summary article or a conversation from months ago. Before the account is opened, pause and verify that your facts match the rule on the day you act. This matters even more if you have moved recently, expect to move soon, or have a purchase timeline that may cross a year boundary.

One simple way to handle this is to record the opening decision in a short note for yourself before any money moves. The note does not need to be elaborate. It just needs to say, in plain language, why you are eligible to open now and why you are opening now rather than later.

The point is not paperwork for its own sake. The point is to stop yourself from contributing first and checking later.

Next, get control of your room across all accounts. In the year you open your first FHSA, participation room is $8,000, unused room can carry forward by up to $8,000, and the lifetime limit is $40,000. That room is shared across every FHSA, so opening accounts at multiple institutions does not increase your capacity.

This is where many otherwise careful savers get loose. They look at one account screen, see that an account is active, and assume they still have space because no single provider is showing the full picture. But FHSA room is not tracked by your preferred dashboard. It is a combined limit across all your FHSAs.

If you are using more than one institution, your control system has to sit above the institutions, not inside any one of them. Keep one master contribution ledger. Track the date, amount, account, and whether each deposit uses current-year room or carryforward before every contribution.

In practice, this is the control point that matters most, because CRA can apply a 1% per month tax on the highest excess amount for each month an overcontribution remains.

That ledger should be the first place you look before you add money anywhere. Not the account homepage. Not the transfer screen. The ledger. If the total in the ledger does not clearly show what room remains, do not contribute yet.

Your FHSA ledger should let you answer four questions instantly:

- What has already been contributed this year across all FHSAs?

- How much of that amount used current-year room?

- How much used carryforward?

- What is the remaining amount you can safely contribute before the next deposit?

Keep the format simple enough that you will actually update it every time. Complexity is not your friend here. A neat spreadsheet, a plain tracker, or a running contribution log can all work if they are maintained. What matters is that every contribution is captured once, in the same place, and reconciled before the next deposit is made.

If contributions are made from more than one bank account, or if you are using more than one FHSA provider, the ledger becomes even more important. In that situation, your biggest risk is not misunderstanding the annual number. It is losing track of timing. A deposit initiated in one place while another recent deposit is still being processed somewhere else can create a mismatch between what you think has happened and what has actually posted.

Watch for a few common failure modes:

- You make one contribution, then forget it when funding a second FHSA at another provider.

- You remember the annual room number but not how much carryforward has already been used.

- You rely on memory because the amount feels small.

- You assume that extra accounts mean extra capacity.

- You treat initiated deposits and posted deposits as if they are the same thing without checking.

None of those errors feels dramatic when it happens. That is why they are expensive. The account still opens. The transfer still goes through. The problem only shows up after the contribution pattern has already crossed the line.

CRA's excess tax is based on the highest excess amount for each month an overcontribution remains. So the safer approach is to prevent the excess before it exists, instead of trying to clean it up afterward. A small bookkeeping error can matter more than expected if it sits unresolved. Reconcile first, contribute second.

Do not leave the withdrawal check until the end. A qualifying withdrawal can be tax-free if all conditions are met, and it does not require repayment. Before you request funds, run one pre-withdrawal check for residency, qualifying-home conditions, and the current CRA timing condition for purchase or build completion [verify current CRA threshold/date before submission].

The key phrase is before you request funds. Many people treat withdrawal eligibility as the final administrative step, something to handle once the property side is moving. That is backwards. Withdrawal eligibility should be part of the funding decision from the start.

The value of the FHSA depends on reaching a qualifying withdrawal path. If there is a serious chance that your path will not qualify, you need to know that while deciding where to place the money, not after the purchase process is already moving.

Your pre-withdrawal check should answer these questions in order:

- Are you currently a resident of Canada for the purpose that matters here?

- Do you have what you need to show the withdrawal still meets qualifying-home conditions when needed?

- Does your timing still fit the current CRA condition for purchase or build completion [verify current CRA threshold/date before submission]?

- If you are also planning to use HBP funds, have you kept a separate note showing that both rule sets are being handled?

That last point matters because people often collapse different home-purchase tools into one mental bucket. The cash may all be headed to the same property, but the rules do not merge just because the goal is the same. If you are combining programs, keep them separate in your records and in your thinking.

It also helps to decide what would count as a stop signal before you are under time pressure. If your residency may change before the withdrawal date, or if the purchase timeline slips far enough that you are no longer confident about the timing condition, do not treat that as a detail to resolve later. Pause and re-check the entire FHSA plan before making more contributions or relying on the account in your closing stack.

Once those gates are clear, the next decision is not where to open the account first. It is what role each account should play in your purchase plan.

That shift in thinking matters. Many people start by comparing products, but the more useful comparison is between jobs. Your FHSA, RRSP with HBP, and TFSA do different work in a first-home plan. If you assign each one a specific role based on certainty, flexibility, and repayment burden, account selection gets easier and mistakes get fewer.

Assign each account a specific job#

The strongest setup is to give each account a clear job instead of treating them as interchangeable. Use FHSA funds for high-confidence first-home money. If your purchase path is realistic, the FHSA gives you generally deductible contributions and a tax-free qualifying withdrawal. If your timeline or location may shift, choose accounts based on risk and flexibility, not on labels.

That sounds obvious, but it is where many plans get muddled. People often ask which account is "better" in the abstract, when the more useful question is what uncertainty the account needs to absorb. An FHSA is powerful when the purchase path is credible. A TFSA is useful when the plan may move. An RRSP with HBP can add capacity, but it brings a repayment obligation.

Once you think in terms of jobs rather than branding, the structure becomes clearer.

| Account | Best use | Main upside | Main risk | Wrong tool when |

|---|---|---|---|---|

| FHSA | Core first-home savings with a realistic qualifying withdrawal path | Contributions are generally deductible; qualifying withdrawals can be tax-free and do not require repayment | Overcontribution across institutions, or plans changing before withdrawal | Your residency or purchase path may change before you need the money |

| RRSP with HBP | Add purchase capacity when FHSA room is not enough | You can combine HBP and an FHSA qualifying withdrawal for the same qualifying home if each set of rules is met; HBP maximum is $60,000 | HBP withdrawals must be repaid within 15 years | You need flexibility more than additional purchase capacity |

| TFSA | Savings for uncertain purchase timing or location | Flexible access when plans are not firm; withdrawn amount is added back to room on January 1 of the next calendar year | No FHSA-style contribution deduction | You still have usable FHSA room and a credible Canadian purchase plan |

The table is the high-level view. The more useful step is to translate it into a working plan.

Start with the FHSA role. The FHSA should usually hold the portion of your down payment money that you are willing to tie to a realistic Canadian first-home path. "Realistic" does not mean guaranteed. Very few purchase plans are guaranteed. It means the path still makes sense when you check the actual conditions that matter: residency, timing, and the likelihood that the home purchase will still be the intended use when you need the cash.

In practice, FHSA money is best treated as purpose-specific money. You are not just saving in a tax-advantaged account and hoping the rules work out later. You are assigning part of your savings to a defined use case that depends on a qualifying withdrawal path remaining available.

That is why the account is so strong when your purchase plan is credible. It is also why it gets riskier when your location or timeline may shift.

For cross-border readers, this distinction matters even more. If your career could move you between countries, or if your purchase city is not settled, separate "home money I am confident will stay on a Canadian qualifying path" from "money I may need to keep flexible because my plans are still moving." Those are not the same pool, and they should not sit in the same account by default.

Use the RRSP with HBP for a different job: adding purchase capacity when FHSA room is not enough. This is not simply a backup version of the FHSA. It solves a different problem. The FHSA is attractive because a qualifying withdrawal can be tax-free and does not require repayment. The HBP can help when you need more room than the FHSA gives you, but the tradeoff is that HBP withdrawals must be repaid within 15 years.

That repayment feature changes the character of the money. The cash may help you close on the property, but it also creates a future obligation that the FHSA does not. So the practical question is not just whether you can use the HBP. It is whether you want that obligation attached to your post-purchase budget.

A simple way to think about the account order is this:

- Use the FHSA for the first layer of home money when you have a realistic qualifying withdrawal path.

- Add the HBP only if that first layer is not enough and you are comfortable carrying the repayment obligation afterward.

- Use the TFSA for the portion of your savings that needs to stay flexible because your purchase timing, location, or residency is still uncertain.

That ordering keeps your most favorable non-repayable qualifying path in front, adds HBP capacity only when needed, and reserves the TFSA as your uncertainty buffer.

The TFSA's job is often undervalued in home-buying plans because it looks less dramatic on paper. It does not offer the same FHSA-style contribution deduction. But for uncertain purchase timing or location, that flexibility is exactly the point. If your plans are not firm, the TFSA can be the account that stops you from forcing uncertain money into a structure that depends on a later qualifying event.

That is especially useful when:

- You know you want to buy, but not when.

- You expect to buy in Canada, but the city is not settled.

- You might buy in Canada, but a move to another country is still possible.

- You are building a down payment while your work, immigration, or residency path is still changing.

In those cases, the TFSA is not a consolation prize. It is the correct parking place for uncertainty. It lets you avoid using the FHSA for money that may no longer fit the FHSA's intended path by the time you need it.

For cross-border readers, make those roles explicit. Use the FHSA first for money you can keep tied to a qualifying purchase path. Use the RRSP with HBP when you need more capacity and are willing to take on the repayment obligation. Keep the TFSA for uncertainty in your buy date, city, or country.

If you do not make that role split explicit, you can end up with the wrong problem in the wrong account. The issue is not always that the FHSA was a bad account. Sometimes the mistake is that you put uncertain money into the FHSA and flexible money needs into the RRSP, then discovered later that your purchase path changed. The account structure only works when each account is holding the kind of money it is suited to hold.

Before the next contribution, divide your future purchase funds into three buckets:

- Committed first-home money: money you are comfortable tying to a realistic qualifying withdrawal path.

- Capacity money: money that may need the HBP if FHSA room is not enough.

- Flexibility money: money you may need to move, access, or redirect if plans shift.

You do not need new products to do this. You need clarity. Once those buckets are defined, account assignment becomes much easier.

Also keep contribution types separate in your records. RRSP-to-FHSA transfers are not deductible, even though regular FHSA contributions are generally deductible. A clean split between new FHSA contributions and transferred RRSP amounts will save you confusion later.

This detail feels small until you are trying to reconstruct your contributions later. If your records simply show money arriving in the FHSA without clearly distinguishing regular FHSA contributions from RRSP-to-FHSA transfers, you create avoidable confusion around what was deductible and what was not.

The easiest fix is to keep separate lines in your ledger or records for each type of funding. The objective is not elaborate administration. It is to make sure that if you review the account months later, you can still tell what happened without guesswork. You want to know what went in, where it went, when it happened, and which category it belongs to.

That same logic applies if you use more than one provider. Extra accounts can be useful if you need different pricing, access, or investment choice, but they increase the importance of central recordkeeping. If the role split between accounts is clear, multiple providers can work. If the role split is vague and the records are fragmented, multiple providers usually make mistakes easier, not harder.

Think about provider choice after you assign the job, not before. If an account's role is "high-confidence first-home money," then the provider should support that role with the access and setup you need. If an account's role is "flexibility while plans remain uncertain," then convenience and simplicity may matter more. The main mistake is choosing the provider first and only later deciding what the money is supposed to do.

A clean account plan should also survive a change in your circumstances. That is the real stress test. If your timeline slips, does the TFSA still cover the uncertain portion? If FHSA room is not enough, does the HBP remain a conscious capacity choice rather than an automatic fallback? If your residency may change, does the FHSA still hold only the money you are comfortable keeping on a qualifying path?

That account plan only works if your residency status stays aligned with your withdrawal plan. If that may change, treat it as a hard stop, not a minor footnote.

Treat residency changes as a stop signal#

If your residency changes, pause immediately. CRA states you cannot make a qualifying withdrawal while you are a non-resident of Canada. If you may become a non-resident before purchase, do not assume the FHSA balance will still be available as tax-free down payment cash.

| Check | What to confirm before requesting funds |

|---|---|

| Contribution ledger | One contribution ledger across all FHSAs, current before any withdrawal request |

| Residency information | Your current residency information, with current status matching the status you are relying on |

| Qualifying-home records | The records you may need to support qualifying-home conditions |

| HBP note | A note showing whether HBP funds are also being used |

| Tax treatment | Re-check tax treatment before requesting funds; if a withdrawal is taxable, it must be included in income, and for non-residents, withholding can be 25% unless reduced by treaty |

| CRA timing condition | The current CRA timing condition for purchase or build completion [verify current CRA threshold/date before submission] |

For many global professionals, this is the section that matters most. Residency changes are not a side note in an FHSA plan. They are a switch that can change the entire value of the strategy. If the account was funded on the assumption of a tax-free qualifying withdrawal and that assumption no longer holds at withdrawal time, the problem is not minor.

It changes how much cash you actually have available. It also changes how you should have allocated money across accounts in the first place.

That is why "pause immediately" is the right instinct. Not "keep going and sort it out later." Not "it will probably be fine." Pause. When residency becomes uncertain, stop treating the FHSA as automatic down payment cash until the withdrawal path is checked again.

Use any potential residency change as a three-step review:

- Pause new contributions until you are clear on the account's role.

If you are no longer confident that the money will be withdrawn on a qualifying path while you are a resident of Canada, ask whether new FHSA contributions still fit the plan.

- Re-check the withdrawal assumption before your property timeline gets too far ahead of your account review.

Do not let the home search, offer process, or build timeline outrun your eligibility review.

- Re-check tax treatment before requesting funds.

The cash planning decision should follow the current treatment, not the treatment you expected when you first contributed.

This pause is about discipline, not pessimism. A lot can change between opening the FHSA and withdrawing from it. If your work location, tax residency, or purchase location may shift, review the account against your current facts, not the facts that were true when the strategy first looked clean.

Re-check the tax treatment before you request anything. If a withdrawal is taxable, CRA says it must be included in income, and for non-residents, withholding can be 25% unless reduced by treaty. Until you confirm the treatment, budget conservatively.

That budgeting point matters. If you are planning a purchase and still assuming full FHSA availability on qualifying terms while your residency is unclear, you may be building a financing plan on cash you cannot count on in the way you expected.

In practice, avoid using the FHSA balance as "committed closing cash" if your residency status at withdrawal time is still in doubt. Until the treatment is confirmed, the safer approach is to model the purchase without assuming that the most favorable withdrawal result is available. If the favorable result is later confirmed, that helps. But it should not be the unsupported assumption holding the purchase budget together.

Before any withdrawal request, keep a complete file: one contribution ledger across all FHSAs, your current residency information, the records you may need to support qualifying-home conditions, and a note showing whether HBP funds are also being used. This is the practical way to avoid last-minute failure caused by outdated assumptions.

The file matters because most FHSA problems near withdrawal time are not caused by one dramatic rule misunderstanding. They are usually caused by a collection of smaller failures:

- the contribution record is split across providers,

- the residency position was never re-checked,

- the qualifying-withdrawal information is not organized,

- the HBP plan exists in someone's head but not in a clear note,

- or the account owner is relying on old assumptions because the transaction timeline is moving fast.

A complete file reduces that risk. It gives you one place to review whether the account still matches the purchase plan before money is requested.

The most practical way to maintain that file is to keep it live rather than rebuilding it at the end. Update it when a contribution is made. Update it when your residency situation changes. Update it when the property process moves from a general plan to concrete purchase or build details. Update it again if HBP use is added. The file should reflect your current position, not a reconstruction project.

A strong pre-withdrawal review usually includes:

- Confirm that your contribution ledger is current across every FHSA.

- Confirm that your current residency status matches the status you are relying on.

- Confirm that you have the information needed to support qualifying-home conditions for the withdrawal.

- Confirm whether HBP funds are part of the same purchase plan and note that clearly.

- Confirm the current CRA timing condition for purchase or build completion [verify current CRA threshold/date before submission].

If one of those items is incomplete, the right move is usually to stop and resolve it before you request anything. Speed is rarely your friend when eligibility is in question.

This is also why you should not treat a residency change as a minor administrative update to think about later. If the residency fact changes first and the withdrawal plan is updated second, you can carry an outdated assumption deep into the purchase process. By the time you discover the issue, you may already have mentally committed the FHSA balance to the transaction.

The stop-signal mindset helps prevent that. It tells you that any meaningful change in residency is not just a note to file away. It is a trigger to revisit the account mix itself:

- Is the FHSA still the right home for this money?

- Should additional savings stay in the TFSA while plans are uncertain?

- If more purchase capacity is still needed later, does the HBP remain appropriate?

- Does the timing of the intended purchase still line up with the current rules you are relying on?

If you ask those questions early, the FHSA remains a tool. If you ask them late, the FHSA can become a constraint.

Can I open more than one FHSA to get more room?#

No. CRA says participation room applies across all your FHSAs, so extra accounts do not create extra room. Open more than one account only if you need different providers for pricing, access, or investment choice, and track all contributions in one ledger.

That "no" is simple, but the operational consequences are worth spelling out. Multiple FHSAs can make sense, but only for execution reasons. They do not change the room calculation. So before you open a second FHSA, ask a narrower question: what problem is the second account solving that the first account cannot solve for you?

If the answer is clear, an extra account can be reasonable. If the answer is vague, extra accounts usually create more bookkeeping risk than benefit.

A second FHSA can be justified if you want a different provider for one of the reasons already mentioned:

- pricing,

- access,

- or investment choice.

Those are legitimate reasons. But they are provider reasons, not room reasons. That distinction matters because it keeps you from treating account count as a planning tool when it is really just a platform choice.

If you do use more than one FHSA, keep the setup intentionally boring. The more moving parts you add, the more central your ledger becomes. Every contribution should be recorded in one place before the next one is made, regardless of which provider received it. The ledger should be the control system. The providers are just containers.

For multiple providers, use a simple workflow:

- Decide which provider will receive the next contribution.

- Check your master ledger first, not the provider dashboard.

- Confirm how much room remains across all FHSAs.

- Make the contribution.

- Update the ledger once the amount is committed and again if needed when it is fully posted.

That may feel repetitive, but repetition is exactly what reduces overcontribution risk. When multiple accounts are involved, routine is your safety feature.

There is also a simplicity argument here that many people ignore. If you do not have a strong reason to split across providers, one FHSA is often easier to control than several. The question is not whether you can manage multiple accounts. It is whether the extra complexity is doing useful work for you. If it is not, simplicity has value.

Another helpful rule is to never assume a provider view reflects your total FHSA position. Even if one institution gives you a polished experience, it still does not know what you have contributed elsewhere. That is your job to track. The more confident you feel in a provider interface, the more important it is to remember that the room limit sits across all accounts.

So yes, you can open more than one FHSA. But do it only with a purpose, and understand the tradeoff. Multiple providers can improve your access, pricing, or investment choice. They can also make it easier to lose sight of total contributions if your recordkeeping is weak. Extra accounts help only when your control process is stronger than the added complexity.

Should I use the FHSA or the HBP first?#

Use the FHSA first when you have a realistic path to a qualifying withdrawal, because qualifying FHSA withdrawals do not require repayment. Use the HBP when FHSA room is not enough and you can manage the 15-year repayment schedule. You can combine both for the same qualifying home if each program's conditions are met.

The key phrase is use the FHSA first. That does not mean the HBP has no role. It means the FHSA is usually the cleaner first layer when your qualifying withdrawal path is realistic, because it gives you generally deductible contributions and a qualifying withdrawal that does not need to be repaid. That is a very different burden from using the HBP.

So the right comparison is not just "which account gets me more cash for the purchase?" Ask a second question too. "What obligation will still be with me after the purchase closes?" The HBP may increase purchase capacity, but it does not disappear from your financial life once the down payment is made. The repayment schedule remains part of the picture.

A practical sequence is:

- First, determine how much of your first-home money still belongs in the FHSA because the qualifying path is realistic.

- Next, check whether that FHSA layer is enough for your expected purchase needs.

- If it is not enough, decide whether adding HBP capacity is worth the later repayment obligation.

- Keep TFSA savings available for the part of the plan that still needs flexibility.

That sequencing helps you avoid using the HBP out of habit when what you really need is either more time, more clarity, or more flexible savings. The HBP is useful when the problem is capacity. It is less attractive when the real problem is uncertainty.

Another way to think about it is this. The FHSA is usually your first choice for money you want to convert into a qualifying down payment without a repayment trail. The HBP is the tool you reach for when that first choice does not provide enough room and you are prepared to carry the repayment structure afterward.

This matters emotionally as much as mathematically. Before a purchase, extra capacity feels helpful. After a purchase, repayment obligations can feel heavier than they looked on paper. That does not mean the HBP is wrong. It means you should choose it for a clear reason rather than sliding into it because the purchase budget expanded.

If you plan to combine both for the same qualifying home, keep the administration separate from the beginning. The property may be the same, but the programs are not. Separate notes and clean records make it easier to avoid mixing assumptions. At minimum, your file should make clear:

- what funds are expected from the FHSA,

- what funds are expected through the HBP,

- and that you are tracking each set of conditions on its own terms.

That is especially important if your timeline is moving quickly. Under time pressure, people tend to compress all home-buying funds into one mental category: "down payment money." But FHSA money and HBP money do not become one rule set just because the purchase is the same. Treating them separately is one of the easiest ways to reduce last-minute confusion.

There is also a discipline point here for global professionals. If your residency or purchase path may change, the FHSA-first recommendation still depends on having a realistic path to a qualifying withdrawal. If that path becomes less credible, "FHSA first" may stop being the right operational answer for new savings. At that point, flexibility can matter more than maximizing the account that looked strongest under a more stable plan.

So when choosing between the FHSA and the HBP, do not ask only which one is more powerful in theory. Ask these questions in order:

- Is my FHSA qualifying withdrawal path still realistic?

- If yes, how much first-home money should still be concentrated there?

- Is that amount enough for my likely purchase?

- If not, am I comfortable adding HBP capacity and the 15-year repayment schedule?

- What portion of my savings still needs TFSA-style flexibility because plans remain uncertain?

That sequence keeps the decision grounded in your actual path rather than in abstract account rankings. For many buyers, the result will still be the same: use the FHSA first, add HBP only as needed, and keep the TFSA for uncertainty. But the logic matters, because it stops you from overcommitting to one tool when the real issue is not capacity but flexibility.

What if I might leave Canada before buying?

Treat that as a decision gate, not a minor risk. If you are a non-resident at withdrawal time, you cannot make a qualifying FHSA withdrawal while non-resident. Pause any near-term purchase plan that assumes FHSA qualifying treatment and re-check your account mix before you contribute more.

The most important word here is might. You do not need to have a confirmed departure date for this to matter. If leaving Canada before buying is a real possibility, that possibility belongs in your FHSA decision now, not later. The account is most powerful when the intended use stays aligned with the qualifying withdrawal path. If that path could break because your residency may change first, treat the uncertainty as material.

Start by separating two different questions:

- Do I still want to buy a qualifying home in Canada?

- Am I likely to be a resident of Canada when I need to make the FHSA withdrawal?

Those questions are related, but they are not identical. You may still want the same home purchase and still lose confidence in the qualifying withdrawal path because your residency could change before the money comes out. That is exactly why this should be treated as a decision gate.

A sensible response is to pause future FHSA contributions until you can answer what job the account is still meant to do. If the purchase plan remains credible and the residency risk feels remote, you may still decide the FHSA is appropriate. But that should be a conscious decision, not a habit carried forward from an earlier situation.

Walk through the account mix again:

- If the money is still meant for a realistic Canadian first-home path and you expect to remain aligned with the withdrawal rules, the FHSA may still be the right home for that portion.

- If your buy date, city, or country is genuinely uncertain, the TFSA may be the better place for additional savings while you wait for clarity.

- If you still expect to need more purchase capacity later, the HBP remains a separate question, not a substitute for unresolved FHSA eligibility.

This is less about predicting the future perfectly and more about avoiding false certainty. If you might leave Canada before buying, the risk is not just that your plans could change. The risk is that you keep funding the FHSA as though nothing has changed, then discover at withdrawal time that the favorable path you were counting on is no longer available.

That is why "re-check your account mix before you contribute more" matters so much. New contributions should follow your current probability map, not your old one. If the chance of leaving Canada has increased, the flexible share of your savings may need to increase too.

Before each additional FHSA contribution while your plans are unsettled, ask yourself one short question: If my move happens before I buy, will I still be comfortable with this money having been placed in the FHSA? If the answer is no, or even "not really," that is usually a sign to pause and redirect the uncertain portion to the TFSA until the path is clearer.

Also avoid building a near-term purchase budget that quietly assumes qualifying FHSA treatment if your residency could change first. That kind of budget can look stable right up until the point it is tested. Conservative planning is better here. Let confirmed eligibility improve the outcome later, rather than letting hoped-for eligibility hold the plan together now.

Most importantly, do not downgrade this to a footnote. For a globally mobile buyer, possible departure before purchase is not a minor risk around the edges of the FHSA strategy. It is one of the main facts that determines how much of the strategy should sit in the FHSA at all. If that fact changes, the account mix should change with it.

If you want a deeper dive, read Ho Chi Minh City, Vietnam: The Ultimate Digital Nomad Guide (2025).

If your location or timeline could shift before withdrawal, run a quick scenario check with the Tax Residency Tracker before you commit funds.

If steadier collections would make your savings plan easier to execute, review Merchant of Record for freelancers as a practical next step.

Related Playbooks and Official References#

- Use this implementation guide before changing your operating model.

- Cross-check your pipeline assumptions with this sales workflow.

- Anchor financial decisions in this cash-planning framework.

- Stress-test price positioning using this pricing guide.

- Protect execution quality with this contingency checklist.

Validate strategic assumptions against industry analysis, classic disruption research, and operator-level benchmarks.

Treat your FHSA plan like a quarterly operating plan: review contribution pace every 90 days, update your target purchase date each quarter, and recalculate affordability when rates move by 50 basis points or more.

Documentation Checklist Before You Contribute#

- Confirm your contribution room and carry-forward before each deposit cycle.

- Record the account provider, contribution date, and settlement amount in one tracker.

- Keep account statements and withdrawal records in the same year-by-year archive.

How to Handle Residency Changes Without Breaking Your Plan#

If your tax residency changes, stop and reassess your contribution and withdrawal strategy before continuing. Run a documented review with your tax adviser so account actions still align with local reporting and treaty treatment.

A 12-Month Review Cadence for FHSA Execution#

- Quarterly: review contribution pace and housing timeline.

- Semi-annual: rebalance risk level to match purchase window.

- Annual: validate reporting, slips, and withdrawal eligibility assumptions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Ho Chi Minh City Digital Nomad Guide for a 30-Day Move (2026)

Ho Chi Minh City is a strong base if your priority is keeping work momentum while relocating. You get density, plenty of places to work from, and a social scene that can help you settle quickly. It is a weaker fit if your best days depend on calm streets, easy walking, and long stretches of quiet. In practice, Saigon tends to reward people who want convenience and activity more than retreat pace.

How to Write a Newsletter That Your Subscribers Actually Read

If your newsletter only goes out when you feel sharp, you do not have a writing problem. You have an operating problem. A reliable way to improve is to stop treating each issue like a fresh performance and start running the same five-part routine every time: plan, draft, quality check, publish, review.

Liability Insurance for Freelance IT Consultants: Do You Need It?

**Treat your insurance decision like risk management, not online shopping.** As an independent IT consultant, you can face a negligence allegation, a client financial-loss claim, and legal defense costs even when you delivered in good faith. One bad dispute can drain time, focus, and cash before anyone proves fault. If you run solo, you are the CEO of a business-of-one, and risk decisions are part of the job.