Quick Answer

Constructive receipt means freelance income is taxable when you can access it without a meaningful restriction, not only when it reaches your bank account. For cash-method taxpayers, funds shown as available, a delivered check, or money credited for immediate withdrawal usually count in the current tax year. Unpaid invoices, real holds, reserves, disputes, or contract-based approval gates can point the other way.

For many professionals, "constructive receipt" feels like a tax trap. That mindset gives up too much control. In practice, this rule is about timing: when income becomes taxable because you can access it, not just when cash lands in your bank account.

This guide treats constructive receipt as a rule you can plan around. Once you understand how access, restrictions, and contract terms fit together, you can make better decisions about when income is recognized and how to support that position.

What is Constructive Receipt? A No-Nonsense Primer#

For cash-method taxpayers, the constructive receipt doctrine means income is taxable when it is available to you without a meaningful barrier, not only when cash hits your bank. Treasury Regulation § 1.451-2 says income is treated as received when it is credited to you, set apart for you, or otherwise available for immediate draw. The exception is when your control is subject to a substantial limitation or restriction.

The practical distinction is access versus possession. If a client payment is credited to your account on December 29 and shows as available for withdrawal, waiting until January 3 to transfer it usually does not change the tax year. Delaying your move is not the same as lacking access.

That is the right lens for year-end. This rule usually picks up delays by choice, not delays caused by a real barrier. Holding a check or postponing withdrawal can still trigger constructive receipt. If no funds were credited, set apart, or otherwise available, or access was meaningfully restricted, constructive receipt may not apply. IRS Publication 538 is explicit that you cannot hold checks or postpone taking possession to push income into a later year.

The two questions to ask on every payment#

- Was the money made available?

Was it credited to your account, set apart for you, or otherwise available for immediate draw?

- Was there a substantial restriction?

Was access meaningfully blocked, or was the delay only your own choice?

This test is more reliable than labels like "paid," "pending," or "invoiced." For cash-method filers, the 2025 Schedule C instructions require reporting income actually or constructively received during the year. They frame constructive receipt around amounts credited or made available without restriction.

As a year-end checkpoint, review each open or recent payment as of December 31 and document its exact status on that date. "Available for withdrawal" and "not yet released" are different states. Keep records that support your conclusion: contract terms, payment notices, account timestamps or screenshots, and dated client approval records.

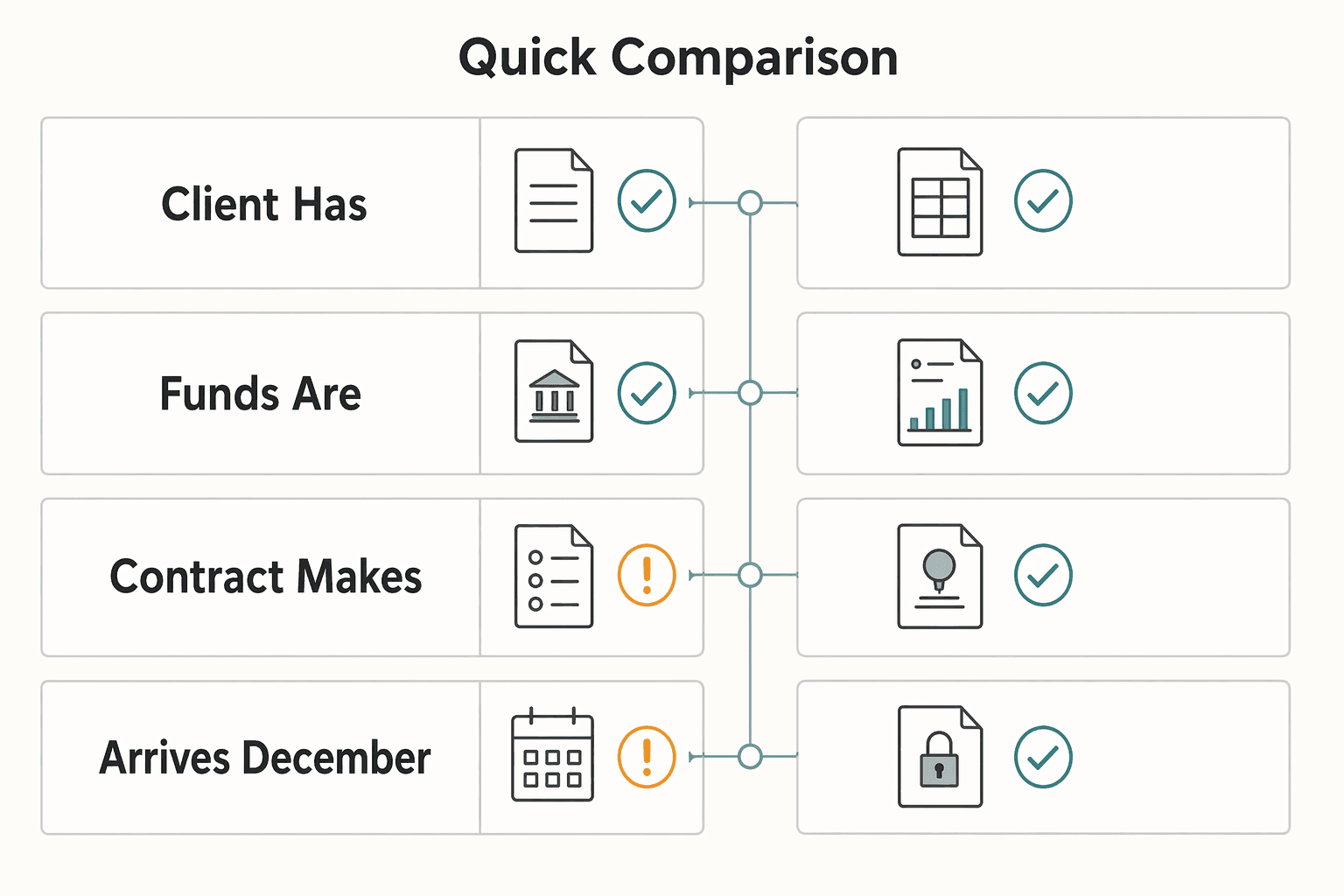

Quick comparison#

| Situation | Likely result | Why it points that way | What to verify |

|---|---|---|---|

| Client has not paid, and no funds were credited or set apart for you | Usually not constructive receipt | No amount appears available for immediate draw | Invoice status, payment notices, client correspondence |

| Funds are shown as available for withdrawal on December 31 | Usually is constructive receipt | Amount appears available without restriction | Account status screenshot, ledger timestamp, payout terms |

| Contract makes final payment available only after written acceptance, and acceptance has not happened by December 31 | May be not yet constructive receipt | A real preexisting gate may be a substantial restriction if access is blocked until signoff | Signed contract, acceptance clause, dated approval trail |

| Check arrives in December, but you deposit in January | Usually is constructive receipt | Delaying deposit does not remove availability | Delivery date, check copy, relevant mail record |

If money was already available and you simply did not withdraw, transfer, or deposit it, that usually does not defer recognition. If timing is tied to approval or another business milestone, that gate should exist before funds become available and be documented clearly, which is what the next section covers.

For a step-by-step walkthrough, see The 'At-Will' Employment Doctrine in the US Explained.

The Contractual Firewall: Defining Your Income Timing Before Day One#

If you want timing to follow a real approval or release step, put that step in the contract before work starts and before funds become available. Under Treasury Regulation § 1.451-2, the key test is whether income was credited, set apart, or otherwise available for you to draw. The exception is when your control is subject to a substantial limitation or restriction.

Your contract is not a guarantee, but it can be a key record for the real question: did you already have an unconditional right to the money? If your terms effectively allow immediate collection at delivery, you may have little separation between finishing the work and having access to funds.

What a substantial restriction looks like in contract terms#

A substantial restriction is a real business gate that delays unconditional access to payment. It should state what must happen before payment becomes available, such as written acceptance, completion of a defined milestone, or another objective release condition set in advance.

Use this pre-signing check: Does this clause delay unconditional access to funds? If no, rewrite it or assume timing control is weak. If yes, keep it and make sure your invoicing and collection process actually follows it.

A useful nuance from § 1.451-2 is that a bookkeeping credit is not automatically receipt when the amount is not available until a future date. That is why release conditions matter more than labels like "earned," "billed," or "posted."

Payment due is not payment available#

The clause that controls access matters more than the clause that says payment is owed. Use the comparison below to see how small wording changes can shift the facts.

| Common clause pattern | Better drafting direction | Why it changes the facts | Legal review note |

|---|---|---|---|

| "Final payment due upon delivery." | "Final invoice may be issued only after Client's written acceptance of final deliverables, and payment becomes due after that acceptance." | Delivery-only language can make payment collectible sooner. Written acceptance creates a defined gate first. | Get jurisdiction-specific wording verified. |

| "Consultant will invoice 50% at project completion." | "Phase 2 invoice may be submitted only after Client approves Phase 1 deliverables in writing." | Ties the next invoice to a documented milestone instead of completion alone. | Get jurisdiction-specific wording verified. |

| "Fee will be credited at month end." | "Any internal credit or statement entry does not create a present right to withdraw funds before the stated release condition is met." | A book entry without current access is not the same as funds being available for immediate draw. | Get jurisdiction-specific wording verified. |

Before you sign, confirm who can release funds, what event triggers release, and whether your billing or payment process could make funds withdrawable earlier than the contract intends.

Build a release chain you can prove#

For larger projects, consider documenting a sequence from scope through payout rather than relying on one clause alone:

| Step | What it covers | Examples |

|---|---|---|

| Scope gate | Define what completion means for that stage | SOW, milestone schedule, or deliverables list |

| Approval trigger | State the client action that unlocks the next step | Written approval by email or portal signoff |

| Invoice trigger | Specify when invoicing is allowed | Ideally after the approval trigger |

| Payout trigger | State when payment is due after invoicing and any hold or release condition | Any hold or release condition that still applies |

| Required documentation | Keep records that show timing and access | Signed contract, SOW, dated approvals, invoice timestamps, payment notices, and year-end evidence of whether funds were withdrawable on December 31 |

Deferred compensation needs early sequencing#

If you want to defer a large payment into a later year through a nonqualified deferred compensation arrangement, set it up before services are performed. Do not improvise at year-end. Under 26 CFR § 1.409A-2, a deferral election must be made and become irrevocable under the timing rules. The regulation includes examples where elections lock as of December 31 for compensation tied to services in the following year.

| Approach | Risk level | Why |

|---|---|---|

| Define ordinary project fees with clear approval or release gates before work begins, then follow them exactly | Safer | Aligns timing with documented access conditions from the start. |

| Finish the work, then ask the client to hold payment until January | Higher risk | Looks like a late timing change after access is already available. Escalate to a tax professional. |

If a § 409A arrangement fails, deferred amounts can become currently includible. There can also be an additional 20 percent tax and interest at the underpayment rate plus 1 percentage point. Treat meaningful deferral planning as something to review with a professional, not a last-minute contract tweak. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

Your Year-End Checklist: Navigating Invoices, Platforms, and Payments#

Year-end is a facts check, not a guess. Start with this rule: if funds were available for you to draw without a meaningful restriction, treat that as a strong current-year income signal. If access was genuinely restricted, save proof of that restriction.

For cash-method timing, constructive receipt turns on access. If money was credited or otherwise available to you without restriction, the risk points to the current year. If your control was subject to a substantial limitation or restriction, timing may differ, but you need records showing that limitation actually existed.

Verify platform balances first#

Start with any place funds can sit before they hit your bank: Stripe, PayPal, Upwork, and any other platform you use. Check status as of December 31.

| Platform or status | Year-end read | What to save |

|---|---|---|

| Available | Current-year warning sign if you could have withdrawn | Dated screenshot with amount, status label, and timestamp |

| Pending | Potential restriction evidence | Supporting status details |

| Hold | Potential restriction evidence | Platform notice explaining why funds were restricted |

| Reserve | Potential restriction evidence | Supporting status details |

| Upwork hourly | Timing can differ; hourly earnings become available ten days later (the following Wednesday) | Verify each payment line by contract type and payout flow |

| Upwork fixed-price | Timing can differ; funds are released five days after milestone approval under the standard security period | Verify each payment line by contract type and payout flow |

- Treat

availableas a current-year warning sign if you could have withdrawn. - Treat

pending,hold, orreserveas potential restriction evidence, then capture the supporting status details. - Save dated screenshots with amount, status label, and timestamp.

- Save platform notices that explain why funds were restricted.

Platform labels are strong evidence, not the whole answer, so confirm the underlying facts and your contract terms. For Upwork specifically, verify each payment line by contract type and payout flow. Timing can differ, including hourly earnings becoming available ten days later (the following Wednesday), and fixed-price funds released five days after milestone approval under the standard security period. Do not assume all balances follow one timeline.

Triage open invoices and payments#

Sort each item into one bucket and act right away.

| Status at year end | What to verify now | Working read | Action |

|---|---|---|---|

| Unpaid | No funds sent, credited, or set apart for you | Usually not currently available | Keep invoice, due date, and follow-up records showing nonpayment |

| Disputed or held | Funds exist but access is blocked by dispute, hold, reserve, or approval gate | May not be currently available if restriction is real | Keep dispute or hold notices, contract clause, and timeline proof |

| In transit | Payment initiated, but settlement or access status unclear | Facts-dependent | Confirm whether funds were actually withdrawable by December 31 |

| Received | Funds were in your control, or a valid check reached you by year-end | Strong current-year inclusion signal | Record receipt date, method, and supporting payment record |

Do not collapse "invoice sent" into "income received." Also do not assume delaying a transfer or check deposit changes timing if funds were already available or a valid check was received by year-end.

Confirm transit status, not promises#

"In processing" is not enough. Ask for status you can classify:

- Was it credited?

- Was it withdrawable?

- Was it pending, held, or unsettled?

For Stripe-type flows, pending means incoming but not yet settled into available balance. For PayPal hold flows, access can be restricted until release conditions are met, including the noted seven-day release timing after order completion confirmation. Use those details to place each payment on the right side of year-end access. Use this short template framework when you need confirmation:

- Subject line: Year-end payment status confirmation for the invoice

- Contract reference: Cite the relevant MSA, SOW clause, or milestone term and ask the client to confirm the current status under that term.

- Expected payment window: State the expected date or event-based release shown in your records.

- Confirmation request: Ask whether funds were sent, credited, withdrawable, pending, or on hold as of December 31.

Build a year-end evidence file#

If a payment is ambiguous or high value, build a dedicated file for it. You want documents that prove both timing and access.

| Evidence type | What it can show | Examples |

|---|---|---|

| Contract or SOW clause | What controls approval, invoicing, payout, holdback, or release | Contract or SOW clause controlling approval, invoicing, payout, holdback, or release |

| Client messages | Approvals, disputes, delays, or release timing | Client messages showing approvals, disputes, delays, or release timing |

| Platform status evidence | Whether funds were shown as available, pending, reserve, or hold | Visible dates and timestamps |

| Payment records | Remittance, receipt, posting, or invoice timing | Remittance notices, check receipt dates, bank posting records, and invoice timestamps |

| Conflicting status records | Why the treatment decision is evidence-based when records do not align | Records showing funds appear available while also under reserve or hold, or a payer claims payment was sent without proof of availability |

- Contract or SOW clause controlling approval, invoicing, payout, holdback, or release

- Client messages showing approvals, disputes, delays, or release timing

- Platform status evidence like

available,pending,reserve, orhold, with visible dates and timestamps - Payment records such as remittance notices, check receipt dates, bank posting records, and invoice timestamps

Keep records for at least the general 3-year IRS assessment period. If year-end access is unclear, keep conflicting status records together so your treatment decision is evidence-based. For example, funds may appear available while also under reserve or hold, or a payer may claim payment was sent without proof of availability. Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. Before you close the year, standardize your payment-language templates and approval triggers with the Freelance Contract Generator.

From Liability to Asset: Using Constructive Receipt for Strategic Deferral#

Treat this section as a review framework, not as established deferral guidance. It does not establish doctrine-specific criteria for when these planning goals work.

| Planning goal | Higher-income year | Deferred recognition year | When deferral helps | When it does not | What documentation is required |

|---|---|---|---|---|---|

| Tax-rate management | Criteria not established here | Criteria not established here | Not established here | Not established here | Documentation requirements not established here |

| Retirement funding timing | Criteria not established here | Criteria not established here | Not established here | Not established here | Documentation requirements not established here |

| Lending profile stability | Criteria not established here | Criteria not established here | Not established here | Not established here | Documentation requirements not established here |

Use this default sequence before you treat deferral as usable:

- Treat this section as unresolved unless you have qualified tax guidance for the specific arrangement.

- Keep records complete, dated, and internally consistent.

- Send doctrine-specific treatment questions to a qualified tax advisor.

- Escalate before relying on a deferral position when the criteria are not clearly established.

Because this planning section does not establish doctrine-specific deferral rules, treat it as a prompt for tax-advisor review rather than a standalone tax position. You might also find this useful: A Guide to 'Accrual' vs. 'Cash Basis' Accounting for a Small Agency.

You Are in Control#

Once you know the yes-or-no test, use it consistently: set timing terms before work starts, verify access at year-end, and document unclear facts before you file.

Set the rule before work starts#

Treat every engagement as pass or fail on timing clarity:

- Pass: Payment terms clearly state when funds become available and what condition must be met first.

- Fail: Timing is vague, can be changed informally, or depends on ad hoc messages.

Your strongest setup is a real restriction in place before income is available. Under 26 C.F.R. § 1.451-2, income is not constructively received when substantial limitations or restrictions apply. A future availability date or required written approval is most defensible when it is documented before funds are credited or otherwise within immediate control.

Verify the facts before year-end#

For cash-basis taxpayers, the core question is whether income was credited to you and under your immediate control. Review each open payment before year-end and make a clean call.

- Pass: Funds were not available to you because of a substantial limitation or restriction.

- Fail: Funds were credited, delivered by check, or otherwise available, and the only barrier was your choice not to withdraw, deposit, or cash.

If a check was received, not cashing it is usually not the deciding factor. If funds are in escrow and only time blocks access, that can still point to current-year income.

Document ambiguity and align your filing position#

When timing is unclear, build the file before you file the return:

- Keep: signed contract, approval and payment records, invoice trail, year-end account screenshots, delivery or check-receipt records if relevant, and any written escrow agreement or amendment.

- Practical default: If facts are ambiguous, document your reasoning and consider treating the amount as current-year income unless a substantial restriction is clearly documented.

- Escalate: Talk to a tax pro when the issue involves cross-border facts, platform-held funds, escrow structures, or deferred-comp-style timing.

You do not need perfect timing control. You need clear terms, a year-end check, and records that support your reporting position. That leads to fewer surprises, cleaner records, and a more defensible return. We covered this in detail in The Best Receipt Scanner Apps for Freelancers. To keep this doctrine manageable alongside your broader compliance workflow, use the Tax Residency Tracker.

Frequently Asked Questions

What is the difference between actual receipt and constructive receipt?

Actual receipt means the money is already in your hands or account. Constructive receipt means the money was available to you without a substantial limitation or restriction, even if you did not move it yet. The key question is whether you could access the funds by year-end without a meaningful barrier.

How do you reduce constructive receipt risk through your contract?

Set payment timing before work starts, not after funds are already available. Use clear approval, milestone, or release conditions that create a real access barrier, and make sure your invoicing and payout process follows them. Keep the signed terms with your year-end records.

Is an unpaid invoice at December 31 automatically taxable to you?

No. An unpaid invoice by itself is not automatically taxable. If payment was not made and no funds were credited, set apart, or available to you by year-end, that usually points away from constructive receipt.

If money sits on a platform and you do not withdraw it, is it received?

Maybe. If the platform balance was available for withdrawal without a substantial limitation or restriction, that usually points to constructive receipt even if you left it there. If the balance was pending, on hold, in reserve, or otherwise not withdrawable, that can point the other way.

What if a client mails you a check in late December but you deposit it in January?

The deposit date is usually not the main test. If the check was delivered, or delivery was attempted, by December 31, that generally points to current-year constructive receipt. If it could not possibly reach you until January, it points to next-year receipt.

When are the facts too messy to handle on your own?

Escalate when your records conflict or the timing facts are unclear, such as changed payment terms, disputed approval, unclear platform holds, or uncertain check delivery. Reconcile the contract, payment-status records, invoices, receipts, deposit slips, and any canceled checks. If they do not line up, do not make a DIY call.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- govinfo.gov/content/pkg/GOVPUB-T22-705c151bf782598e2e76c...trusted

- irs.gov/publications/p538trusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

- kb.osu.edu/server/api/core/bitstreams/552eb136-685f-5e1...trusted

- law.cornell.edu/wex/constructive_receipt_of_incometrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Accrual vs Cash Basis Accounting for Small Agencies

---