Quick Answer

Yes, U.S. expats can use tax-loss harvesting if they file a U.S. return, but they should confirm tax residency first, calculate each sale in USD, avoid substantially identical replacements within 30 days before or after the sale, and update FBAR or Form 8938 tracking when proceeds affect foreign accounts.

Phase 1: The Global Portfolio Audit - Are You Harvesting in the Right Country?#

Before you sell anything, settle one question: which country may tax the sale, and which records will support the filing. If residency is clear, move on. If you see dual-residency signals or treaty uncertainty, stop and sort that out before you trade.

Define the terms before you act#

Tax residency determines which core tax rules apply to you. Dual residency means two countries each treat you as a resident under their own domestic rules. A treaty tie-breaker is the treaty mechanism used to assign one treaty residence when both treaty countries claim you.

Cost basis in reporting currency means your asset cost translated into the currency required on your return. For U.S. filing, amounts are reported in U.S. dollars, so your exchange-rate method should be documented and used consistently.

Make the go/no-go decision#

Use residency as the first gate:

| Residency situation | Action | Support |

|---|---|---|

| Residency is clear under domestic law and no second-country claim is apparent | Proceed to account inventory and basis cleanup | Use residency as the first gate |

| Dual-residency signals appear | Stop and review the actual residency article in the relevant bilateral treaty | Treaty residence is a threshold issue, and outcomes differ by treaty |

| Residency is unclear | Pause harvesting and get cross-border tax advice before any sale | A possible U.S. substantial presence outcome, 31 days in the current year and 183 days under the 3-year formula, is enough to trigger review |

Confirm what matters in each jurisdiction#

Once the residency question is settled, map the rules and records in each place that touches the trade. A trade can be economically correct and still create reporting problems if this map is wrong.

| Jurisdiction to check | What to confirm before harvesting |

|---|---|

| Home jurisdiction | Whether it still treats you as resident, how gains and losses are treated, and any current reporting trigger pending official or tax-advisor verification |

| Current jurisdiction | Whether local law treats you as resident, whether a treaty applies, and whether treaty residence could shift taxing rights |

| Brokerage jurisdiction | What reports the broker provides, whether basis is tracked, statement currency, and export access for confirms and year-end summaries |

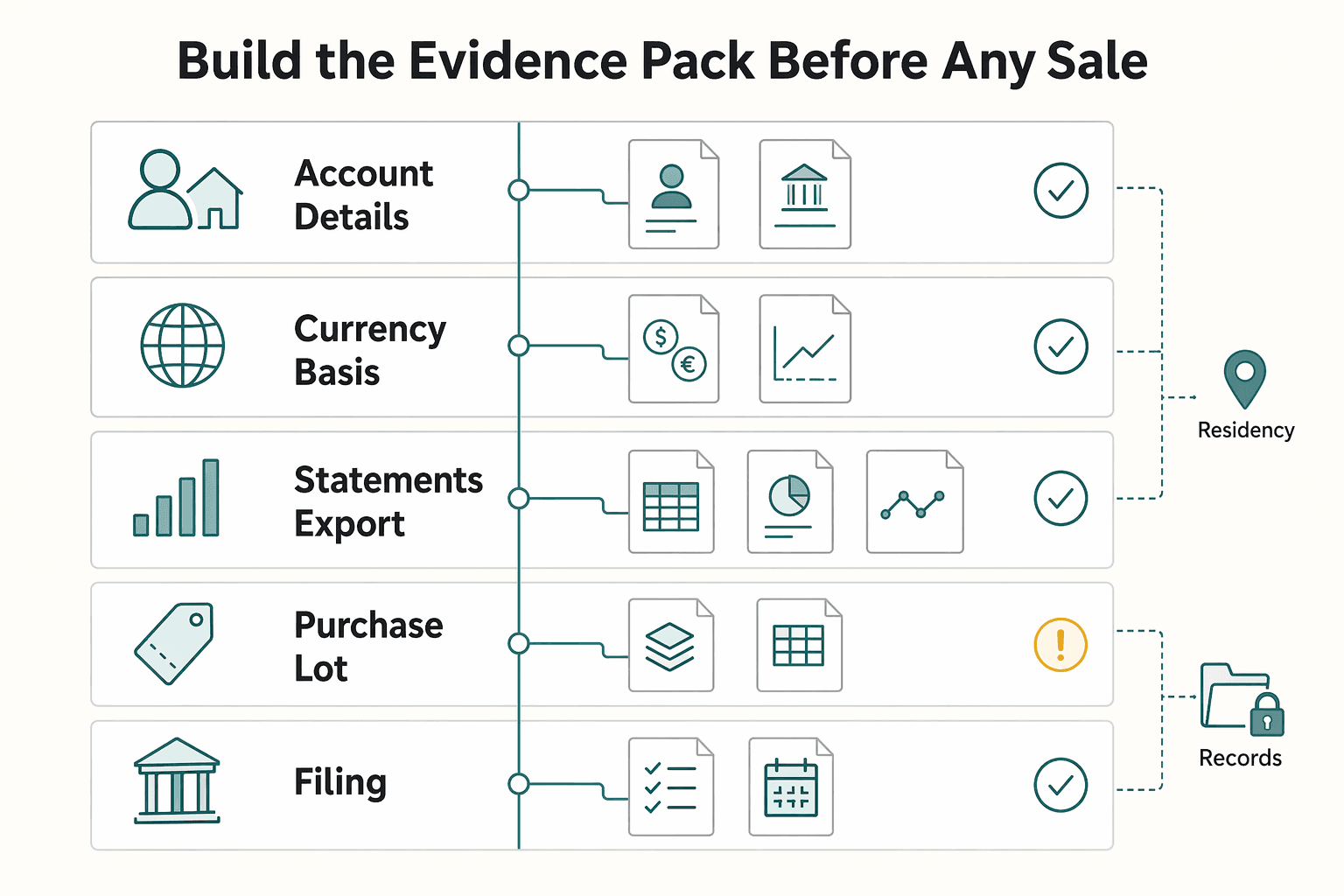

Build the evidence pack before any sale#

Build the file before execution, not after. For each account, save:

| Record | What to save |

|---|---|

| Account details | Account holder, institution, account type, country, and masked identifier, such as an account ending in 1234 |

| Currency and basis | Base currency, statement currency, and whether the broker reports basis |

| Statements and export | Year-end statement and latest transaction export |

| Purchase lot support | Original buy date, quantity, purchase price in original currency, USD translation, FX source, and proof of that rate |

| Filing path | Expected filing path, including Form 8949 when required to reconcile U.S.-reportable sales and any current non-U.S. reporting threshold pending official or tax-advisor verification |

| Foreign-account balance | Highest annual balance for foreign accounts, since foreign bank, brokerage, and mutual fund accounts count toward the $10,000 aggregate value FBAR trigger |

A few operating checks matter here:

- If basis is broker-reported, start with that basis on

Form 8949and record any correction as an explicit adjustment. - Use one consistent FX method across the file.

- For foreign accounts, track FBAR timing. It is due April 15, has an automatic extension to October 15, and required records should be kept for 5 years.

If residency indicators conflict, treaty language is ambiguous, or currency-basis treatment is unclear, talk to a qualified cross-border tax professional before you execute the sale.

Related: A Guide to Tax-Loss Harvesting with Crypto.

Phase 2: The CFO's Execution Model - A System for Seizing Opportunity#

Once residency, account scope, and basis are clean, treat each harvest trade as a three-step process: decide, execute, and document the result the same day.

Decide whether to harvest or hold#

Harvest only when the tax benefit is likely to outweigh the cost and compliance burden. Use this trigger framework before you place an order:

- Portfolio drift: Harvesting is stronger when you already want to reduce or reshape that exposure.

- Tax impact: Losses can offset capital gains. If losses still exceed gains, up to $3,000 ($1,500 if married filing separately) may offset ordinary income, and excess may carry forward.

- Transaction friction: Spreads, commissions, and rebalancing costs can reduce or erase the benefit.

- Compliance complexity: Pause if the trade raises unclear fund similarity, cross-border treatment, foreign tax credit complexity, or currency-characterization uncertainty.

If the benefit looks small and the complexity looks high, hold and reassess.

Run two calculations, not one#

This is where many otherwise solid trades go wrong. For most U.S. taxpayers, your functional currency is USD, and U.S. return amounts must be reported in U.S. dollars. Treat local-currency broker profit and loss as an input, not the final tax result. Run two separate analyses:

| Mistake | Article guidance |

|---|---|

| Using broker local-currency profit and loss as the tax result | Treat local-currency broker profit and loss as an input, not the final tax result |

| Applying one average annual FX rate where transaction-date rates are required | Convert buy and sell amounts using exchange rates prevailing on the relevant transaction dates |

| Combining security return and currency movement into one number | Run separate analyses for security gain/loss in USD and any Section 988 currency characterization check |

| Ignoring holding period classification | Keep one year or less separate from more than one year |

| Assuming foreign-currency treatment is always capital or always ordinary without a Section 988 check | First confirm that the transaction actually creates a separate nonfunctional-currency item |

- Security gain/loss in USD: Convert buy and sell amounts using exchange rates prevailing on the relevant transaction dates, then compute gain or loss by lot.

- Currency characterization check: Separately assess whether a nonfunctional-currency item may fall under Section 988, which can require separate computation and ordinary treatment.

Do not assume every foreign-currency-denominated sale creates a separate ordinary FX result. First confirm that the transaction actually creates a separate nonfunctional-currency item.

Replace exposure without inviting a wash sale#

The replacement trade is where judgment matters most. If you sell at a loss and acquire a substantially identical security within 30 days before or after the sale, the loss may be disallowed. This is often described as a 61-day matching window. This can also apply through an IRA or Roth IRA acquisition.

Use replacements you can defend in plain language. These are judgment calls, not bright-line safe harbors:

| Exposure objective | Possible replacement logic | Red-flag similarity signals | Window note for your trade ticket |

|---|---|---|---|

| Broad U.S. equity exposure | Move to a different provider and a different broad-market index methodology | Same issuer, same benchmark, or share-class wrapper only | Current wash-sale window pending IRS or tax-advisor verification |

| Developed ex-U.S. equity exposure | Keep region exposure, but change index family or inclusion rules | Near-clone mandate, same benchmark family, minor fee or share differences only | Current wash-sale window pending IRS or tax-advisor verification |

| Core bond exposure | Keep duration goal, but change index methodology or bond universe | Substantively same index exposure, same issuer family, wrapper-only change | Current wash-sale window pending IRS or tax-advisor verification |

If you cannot explain why the replacement is not substantially identical, pause before you execute.

Post the trade into filing prep the same day#

Do the paperwork while the details are still easy to verify:

- Build support for Form 8949 first, then complete the related Schedule D lines.

- Keep short-term and long-term results clearly separated in your worksheet before final netting.

- If net capital loss remains, apply the annual deduction limit, $3,000, or $1,500 if married filing separately, and track any remainder as a capital loss carryover for next year.

Talk to a tax professional before executing if any of these apply: unclear "substantially identical" risk, mixed-jurisdiction taxation, uncertain foreign tax credit impact, or unclear Section 988 characterization.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Phase 3: The Compliance & Reinvestment System - Bulletproof Your Records#

After each harvest trade, move straight into compliance work: capture proof, update reporting exposure, keep the wash-sale block active, and tie everything into filing workpapers.

1) Close the trade file the same day#

Same-day file closure is a practical default. Save the documents that prove the lot, proceeds, and replacement trade while details are fresh. That usually means buy and sell confirmations, the broker activity statement, and the basis support you used for return reporting. Keep records that support return items through the applicable limitations period, generally 3 years from filing.

Use a log that is audit-ready, not just stored away:

| Required field | What you record | Source document / file link | Review status |

|---|---|---|---|

| Lot sold | Security, ticker, acquisition date, quantity, cost (original currency and USD) | Purchase confirmation + basis worksheet | Unchecked / Verified |

| Sale details | Sale date and proceeds exactly as reported by broker | Sell confirmation + 1099-B line link | Unchecked / Verified |

| Replacement purchase | Replacement security, trade date, why it is not substantially identical, note: "30-day wash-sale window around sale date (before/after)" | Buy confirmation + trade memo | Open / Cleared |

| Proceeds destination | Account where cash landed, account identifier, foreign vs U.S., updated year-high balance note | Cash ledger + reporting tracker | Needs review / Complete |

| Return mapping | Short-term/long-term bucket, Form 8949 category, any 1099-B box 1g entry, carryforward impact | Draft tax workpaper | Pending / Filed |

When you prepare Form 8949, report proceeds exactly as shown on broker statements or forms so your return ties to reported amounts.

2) Recheck foreign-account reporting when cash settles#

If proceeds land in a foreign account, update your tracker that day and recalculate the year-high aggregate across all foreign financial accounts. FBAR is triggered if that aggregate exceeds $10,000 at any point in the year, and that test does not depend on whether the account generated taxable income.

Track Form 8938 separately. It does not replace FBAR, and FBAR does not replace it. Keep a standing tracker line that says the current Form 8938 reporting threshold must be verified against IRS instructions or tax-advisor records before use. If an account is jointly owned, each owner reports the full account value on FBAR. Keep the filing path explicit. FBAR is due April 15, has an automatic extension to October 15, and is filed separately from the income-tax return.

3) Keep the wash-sale block active until cleared#

Do not rely on memory here. Mark the sold position as blocked for the 30-day wash-sale window around the sale date (before or after). Keep that block visible in your trade notes, calendar, and transaction log.

During the blocked window, do not buy the sold security, and do not buy any replacement you cannot clearly defend as not substantially identical. Treat broker reporting as a checkpoint, not a control. Box 1g on Form 1099-B may show a disallowed wash-sale loss for covered securities, but you still need your own review.

4) Reconcile carryforwards on a recurring schedule#

Carryforward errors compound if you wait until filing season. At quarter-end and again during return prep, net short-term and long-term results and update your carryforward schedule. Complete Form 8949 before Schedule D where required so the transaction detail feeds the return in the right order.

If net capital loss remains after gains are offset, the current annual ordinary-income offset is up to $3,000, or $1,500 if married filing separately. Carry the excess forward. Before filing, verify the applicable deduction limit against current IRS instructions or tax-advisor records.

Talk to a tax professional before filing if any of these apply:

- You cannot classify whether the proceeds account is foreign-reportable.

- FBAR and Form 8938 treatment appears inconsistent.

- Your carryforward does not tie to last year's filed Schedule D and Form 8949 support.

You might also find this useful: A Freelancer's Guide to Donating to Charity (and the Tax Benefits).

Before you lock your trade log and cash-movement records, run a quick exposure check with the FBAR calculator.

Conclusion: You Are the CFO of Your Freedom#

Treat this as an operating rule, not a slogan. Use tax-loss harvesting only when it improves your tax position, reduces avoidable execution errors, and supports disciplined decisions in volatile markets.

In plain language, tax-loss harvesting is selling an investment at a loss so that loss is realized for tax purposes. The wash sale rule is the timing guardrail that can disallow that loss if you repurchase the same security too soon, including within 30 days. A replacement asset is a similar but materially different holding that keeps you invested without an immediate same-security buyback. Keep clear trade notes showing what you sold, what you bought, when you executed, and which accounts were involved.

Your wash-sale review has to cover purchases across accounts tied to the same tax ID, not just the account you happen to be viewing. The common failure mode is simple: you buy back too soon, or in the wrong linked account, and the harvested loss no longer works as planned. Treat tax treatment as jurisdiction-sensitive as well. Do not assume an example from one country carries over cleanly to another.

Use this checklist each cycle before you trade:

- Confirm you are working under the rules tied to your filing position and jurisdiction.

- Verify the replacement asset is similar enough to keep exposure but materially different from what you sold.

- Update records immediately after execution, including dates, symbols, accounts, and replacement rationale.

- Flag jurisdiction-sensitive or account-scope questions early, and escalate before trading when treatment is unclear.

When you execute with that level of discipline, the strategy can produce realized losses that may offset gains and reduce taxable income, with fewer avoidable errors. If residency is unclear, reporting overlaps across jurisdictions, or the characterization of the sale is uncertain, pause and involve a qualified tax professional before trading.

For a step-by-step walkthrough, see A Guide to R&D Tax Credits for Tech Startups.

If you want a safer default before your next harvesting cycle, validate your country assumptions with the tax residency tracker.

Frequently Asked Questions

Can you use tax-loss harvesting if you live abroad?

Yes, in many cases, if you file a U.S. return, harvested losses can still be used. Losses can offset gains, and if losses exceed gains, the deductible amount is currently $3,000 or $1,500 if married filing separately, with excess carried forward. Pause if dual residency or treaty position is unclear.

How does this work when your brokerage activity involves multiple currencies?

Treat the broker's local-currency summary as an input, not the final tax result. If your functional currency is USD, translate tax items into dollars using the relevant transaction-date rates and separately check whether any FX component may be ordinary under Section 988. Pause for professional review if your records cannot clearly support the split.

Does the wash sale rule still matter if you switch into an international ETF or a foreign-listed fund?

Yes. A wash sale can disallow the loss if you acquire substantially identical stock or securities within 30 days before or after the sale. Because substantially identical has no universal bright-line ETF test, use a defensible facts-based review before rebuying.

What should a replacement ETF look like if you want to keep market exposure?

Use a placeholder approach that keeps broad exposure for about 30 days without using a near-clone replacement. A stronger replacement changes the provider, index, or methodology while keeping a similar portfolio role. Document why it is not substantially identical before you trade.

Does this strategy affect FBAR or Form 8938?

Potentially. Trading can change balances and reporting facts, and FBAR is triggered if the aggregate of foreign financial accounts exceeds $10,000 at any point in the year. Form 8938 does not replace FBAR, so verify current filing thresholds and instructions before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Crypto Tax-Loss Harvesting for Globally Mobile Freelancers

Crypto tax loss harvesting can lower capital gains exposure, but only when you turn a paper loss into a real disposal and can support the numbers afterward. A market drop by itself does not create a usable tax loss.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.