Quick Answer

To avoid survivorship bias in business advice, treat every success story as a partial sample and verify whether it transfers to your setup. Check the hidden structure behind the result, map the failure cases the story leaves out, and confirm any legal, tax, contract, or filing claims against current official or expert-reviewed sources before acting.

The Invisible Bullet Holes in Every Success Story#

The most dangerous part of a success story is rarely the tactic you can see. It is the operating condition you cannot see. That is survivorship bias in business advice at work. You draw conclusions from the businesses that made it back, while missing the ones that failed first.

The visible part of a founder or freelancer story is easy to admire: the niche, the pricing shift, the move abroad, the fast client growth. What usually decides whether that advice survives contact with reality is less visible: the assumptions, constraints, and documentation checks the story leaves out.

| Success stories usually show | Success stories usually hide | What you should verify first |

|---|---|---|

| "I copied this playbook and grew fast" | Missing failure cases | Which conditions were present in the winners, and which failed cases were excluded |

| "I moved and kept working" | Jurisdiction and documentation assumptions | Which rules may apply to your situation and what records you need |

| "I scaled fast as a solo operator" | Operational prerequisites | Which controls, processes, and dependencies made that growth possible |

| "I followed this regulation update" | Source quality and legal status | Whether the cited rule is official, current, and the right one for your case |

A practical checkpoint is to verify legal claims at the document level, not just from a post or thread. FederalRegister.gov says users doing legal research should verify against an official edition, and its pages link to the official PDF on govinfo.gov. The eCFR is authoritative for reference, but it is still marked unofficial.

The failure mode is simple. You act on a summary rather than the governing text, then build your business on a rule that was incomplete, outdated, or not official enough to rely on.

That is the diagnosis. Next, turn it into a method by deconstructing the hidden infrastructure behind the survivor's story. You might also find this useful: A freelancer's guide to thinking.

Step 1: Deconstruct the Survivor's "Invisible Infrastructure"#

Before you copy a tactic, run a quick PER check on the person giving it: passport/visa context, legal entity setup, and tax-residency position. In practice, outcomes often depend more on this structure than on the visible tactic.

Treat this as a transfer test, not a biography exercise. Ask: what had to be true for this to work for them, and is that true for me?

| Hidden layer | What to ask about the advisor | Why it changes the advice | What to verify about yourself first |

|---|---|---|---|

| Passport or visa context | What status lets them live or work where they operate? | Work options and admin burden can change what is realistic. | What status you hold now, what permissions you have, and any current rule you still need to confirm. |

| Legal entity setup | Are they operating personally or through a company? Who signs contracts and invoices? | Liability, admin load, and client expectations can differ by setup. | Your current structure, documents you can produce, and constraints already affecting your client work. |

| Tax residency position | Do they clearly state where they are treated as resident for tax purposes? | The same tactic can carry different consequences under a different residency position. | Where residency questions may apply to you, what records you keep, and any current rule you still need to confirm. |

When advice points to a source, verify the source itself before you trust the summary. For example, the Frontiers in Psychology article is identifiable by publication date (2021 Dec 15), article ID (12:644145), and DOI (10.3389/fpsyg.2021.644145). Those checkpoints help you confirm that you are evaluating a real, traceable document.

Also keep provenance separate from endorsement. The NLM page states that inclusion in an NLM database does not imply endorsement, so treat listing as access, not validation. Then test fit: the 2025 FTSG report notes that trend impact timing varies by industry, which means applicability can shift across markets.

Finally, surface the invisible team behind polished advice. Signals like "my accountant handled it," "our lawyer reviewed this," or "my coach helped me decide" point to hidden support. Contextual guidance matters here: many people may not need a coach; the key is support mismatch, not a universal rule to hire or avoid help.

Once you can see hidden advantages, move to Step 2: map the failure patterns the success story leaves out. Related: Digital Nomad Health Insurance: A Comparison of Top Providers.

Step 2: Map the "Failure Archipelago" to Find the Real Risks#

Before any cross-border move, build a failure-pattern map first, because success stories usually hide the failed cases you also need to learn from.

| Output | What to capture |

|---|---|

| Top 3 risks to monitor | By likelihood and downside |

| Earliest warning signal | For each risk |

| Record that proves control | For each risk |

| One item still marked | Current rule still needs confirmation |

You are not collecting inspiration here. You are building a planning checkpoint so major decisions rest on visible risks, not winner-only narratives.

Build your risk map by category#

Start with these four buckets and label any live rule you have not confirmed yet as unresolved.

| Risk area | Trigger to investigate | What can go wrong | What to log now |

|---|---|---|---|

| Immigration | You plan to work, stay, or re-enter under a status you have not verified | Work disruption, travel disruption, client delivery disruption | Jurisdiction, status used, activity performed, and the current rule you still need to confirm |

| Tax reporting | You earn, hold accounts, or move money across borders without checking reporting duties | Missed filings, corrective filings, avoidable cleanup work | Country tie, account/payment flow, filing obligation, and the current rule you still need to confirm |

| Indirect tax invoicing | You bill clients in another country without confirming invoice treatment | Rejected invoices, delayed payment, reissued paperwork | Client location, service type, invoice template used, and the current rule you still need to confirm |

| Permanent-establishment exposure | Your work pattern could raise taxable business-presence questions | Client concern, contract friction, extra tax analysis | Country worked from, authority to contract, duration/pattern, and the current rule you still need to confirm |

If one tactic touches multiple buckets, give it extra attention.

Research failure cases like an operator#

Use public threads and communities to find patterns, not to prove rules. Then verify with sources you can inspect and a predefined quality checklist before you trust a case.

| Evidence condition | Article guidance | Decision use |

|---|---|---|

| Public threads and communities | Find patterns, not prove rules | Verify before you trust a case |

| Jurisdiction, timing, business setup | Context you can audit | A case is more useful when it includes these details |

| Trigger event, consequence, prevention action | Context you can audit | A case is more useful when it includes these details |

| Those details are missing | Log it as weak evidence | Do not use it to drive a major decision |

A case is more useful when it includes context you can audit:

- Jurisdiction

- Timing

- Business setup

- Trigger event

- Consequence

- Prevention action

If those details are missing, log it as weak evidence and do not use it to drive a major decision.

| Naive success query | Risk-focused query | Decision you can make |

|---|---|---|

| "How do people freelance from anywhere?" | "What status or rule did people misunderstand before working from another country?" | Whether to get legal review before travel or delivery |

| "How do I invoice international clients?" | "Which invoice mistakes caused payment delays or rework in my target market?" | Whether to update your invoice template before sending |

| "Can I stay abroad while running my business?" | "What facts triggered residency or reporting questions in similar cases?" | Whether to add day-count tracking and a filing check |

| "How do I keep a client happy overseas?" | "What work pattern made a client worry about local tax presence?" | Whether to adjust contract terms, authority, or location pattern |

Log each case in three fields only: trigger, consequence, prevention control.

Before Step 3, finish this one-page output:

- Top 3 risks to monitor by likelihood and downside

- Earliest warning signal for each risk

- Record that proves control for each risk

- One unresolved current rule to confirm

For a step-by-step walkthrough, see A guide to 'Antifragile' thinking for building a resilient freelance business.

Step 3: Build Your Resilient Operating System#

Your system should turn survivorship-bias stories into verifiable decisions from your own records, not borrowed narratives.

Use three linked control areas so you can spot problems early, choose a response, and keep personal movement and business operations connected.

| Control area | Risk if ignored | What to monitor weekly | Escalate to advisor when |

|---|---|---|---|

| Movement and residency tracking | You cannot show where you were, miss a trigger, or find issues after travel or client work already happened | Entry/exit dates, planned travel, days by jurisdiction, work performed while present, and any current-rule question still unresolved | New country, longer stay, repeated presence pattern, or uncertainty about whether activity changes your status |

| Invoicing compliance controls | Delayed payment, rejected invoices, rework, and client friction | Client location, service type, invoice date/status, template version used, required business details collected, and any current-rule question still unresolved | New client jurisdiction, request for specific invoice language, or any invoice dispute/return |

| Cash-plus-tax planning controls | Cash gaps, missed obligations, reactive cleanup, low visibility on available cash | Income received, tax set-aside, major expenses, account movements, expected filings, proof of submissions, and any current-rule question still unresolved | Large or unusual payment, new account/payment flow, sharp income change, or uncertainty about what to reserve or file |

Keep one source-of-truth tracker across all three areas. It can be simple, but each record needs dates, status, and enough context to answer: what changed, when, and what does it affect?

Pair it with an evidence log. Save invoices, payment confirmations, contracts, travel records, submitted filings, advisor guidance, and any official material you relied on. For each high-risk item from Step 2, you should have a dated record and at least one supporting document.

Run a recurring review cadence with event triggers: do your regular weekly check, then review again when you add a client, change location, receive an unusual payment, or approach a filing event. The FAQ covers the setup questions most people ask first: what to track first, how much detail is enough, and when to get expert help.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

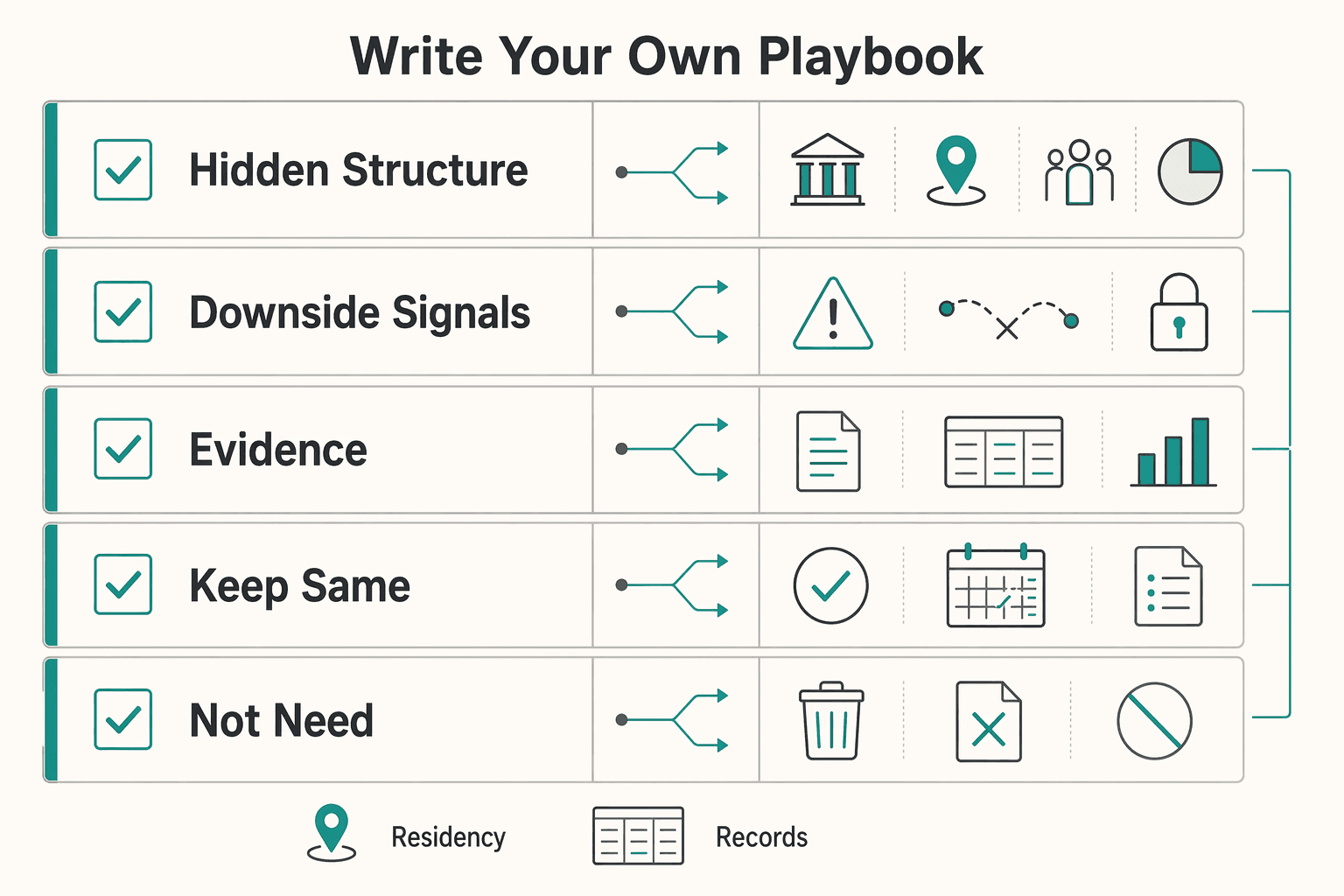

Write Your Own Playbook#

Use this as your rule: do not copy business advice until you verify whether it transfers to your setup. There is no universal template, so run three checks before you act.

| Check | Focus | Article note |

|---|---|---|

| Hidden structure first | Entity setup, current residency position, advisor support, client mix | Advice can break when you invoice across borders, sign different contract terms, or need stronger records |

| Downside signals, not just success signals | Amended filings, rejected applications, contract disputes, later "I had to fix this" updates | Short-term upside is not enough |

| Evidence path | A dated official source, a current professional review, or your own documented evidence pack | Confirm what source or review supports it in your context |

- Check the hidden structure first.

If someone says, "I work from anywhere with one simple setup," verify the structure behind that result: entity setup, current residency position, advisor support, and client mix. Advice from a domestic solo operator can break when you invoice across borders, sign different contract terms, or need stronger records.

- Check downside signals, not just success signals.

Use a structural risk view: vulnerabilities can compound over time, so short-term upside is not enough. Look for amended filings, rejected applications, contract disputes, or later "I had to fix this" updates before you treat advice as reliable.

- Check your evidence path.

Before you adopt a structural change, confirm what source or review supports it in your context: a dated official source, a current professional review, or your own documented evidence pack.

| Advice you hear | What you verify in your context | Your next step |

|---|---|---|

| "Keep the same company and invoice setup everywhere" | Residency position, where work is performed, filing consequences, and any threshold that still needs confirmation | Map countries, dates, and client flows before copying |

| "You do not need professional help yet" | Whether the speaker had advisor support, and your own filing/contract exposure | Get a limited-scope review for structural decisions |

| "One contract template works for every client" | Client jurisdiction, privacy terms, invoicing requirements, tax wording | Pilot by client segment, then revise |

Apply this checklist each time:

- Screen advice: separate tactical tips from structural decisions.

- Validate assumptions: confirm with an official source or current professional review.

- Log risk: capture missing facts and required documents.

- Set a review cadence: re-check rules so "worked once" does not become stale policy.

We covered a related pattern in How Confirmation Bias Hurts Your Freelance Business.

Frequently Asked Questions

How do you practically avoid survivorship bias in business advice?

Treat each success story as a partial sample, not a template. Ask what failure subgroup is missing, what structural factors helped the visible winner, and whether the advice affects legal, filing, contract, or tax decisions. If it touches structure, pause and verify before you act.

Is all advice from successful people bad?

No. Tactical advice can often be tested cheaply and kept reversible. Structural advice needs source checks first because luck, timing, connections, and background can materially affect outcomes.

What is an example for an independent professional?

An independent professional might hear, "I work while traveling and keep the same company and invoice setup everywhere." That result may depend on legal and business setup, client locations, or current local rules. Map their situation against yours line by line before you copy the behavior.

What questions should I ask before copying a strategy?

Ask what jurisdiction the advice depended on, what legal or business structure the person used, and when the advice was true. Ask what hidden support they had, what failure cases are missing, and what records you would need to prove your position if you followed it. If you cannot answer most of those, you do not yet have enough to safely copy the strategy.

When do I need to verify with official sources or an expert?

Verify when advice affects filings, legal status, fees, thresholds, or formal notices. If you are using U.S. federal regulatory material, check the official PDF on govinfo.gov or the official edition of the Federal Register before relying on it. Do not act on screenshots, summary posts, or old date stamps without confirming what changed.

Why is this especially risky for global professionals?

Because structural mistakes can cross borders faster than revenue does. A wrong structural assumption can create multiple downstream problems, and winner-only stories rarely show them. A single visible success should count as inspiration, not proof.

How current does advice need to be?

Advice needs to be current enough that you can tie it to a live rule or a dated official source. Policy and fee information can change at an institution's discretion, so "worked for me last year" is not a strong basis for a structural decision today. If the advice depends on a threshold, form, plan, or filing date, keep it marked for verification until you confirm it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- compton.edu/academics/docs/2024-2025_Compton-College-Cat...trusted

- ecfr.gov/current/title-42/chapter-IV/subchapter-B/par...trusted

- emmanuel.edu/sites/default/files/2024-10/24-25_academic-c...trusted

- federalregister.gov/documents/2024/05/09/2024-09237/nondiscrimin...trusted

- federalregister.gov/documents/2016/11/04/2016-25240/medicare-pro...trusted

- hhs.nd.gov/ndcc-get-involvedtrusted

- hsph.harvard.edu/author/suminasuwaltrusted

- journals.law.harvard.edu/ilj/wp-content/uploads/sites/84/HLI204_crop-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

Thinking, Fast and Slow for Freelancers Who Want Better Clients

Treat thought leadership as risk control for your business, not just a visibility tactic. The real shift is from fast, reactive client chasing to slower, deliberate asset building. You publish to reduce risk before the next dry month, pricing call, or bad-fit project shows up.