Stripe Capital's offer of "fast, easy funding" presents a critical problem for independent professionals: its convenience masks a deceptively high true cost and a dangerous loss of financial control. The core advice is to adopt a CFO's mindset, calculating the loan's effective Annual Percentage Rate (APR) to reveal its true cost and auditing the risks of automated repayments and platform dependency. This risk-first analysis empowers you to determine if the offer is a strategic asset for a specific growth opportunity or a high-cost liability that threatens your business's autonomy.

The CEO's Playbook for Stripe Capital: A Risk-First Framework for Your Business-of-One#

Fast, embedded financing can solve a timing problem, but it can also reduce control over your daily cash inflows. If you are evaluating Stripe Capital financing, use one decision standard: cash-flow resilience under stress, not convenience in the dashboard.

Use a clear framework before you decide#

Judge the offer through four lenses: cost, control, dependency, and fit-for-use.

- Cost: the total repayment structure, advance plus flat fee, not just how simple it looks at first glance.

- Control: repayments are withheld from your Stripe sales, so this directly affects operating cash coming in.

- Dependency: financing and payment collection can sit with the same provider, which can increase concentration risk.

- Fit-for-use: use this for a defined business need, not to cover an ongoing cash shortfall.

This program is also not one single product shape. Stripe says offers can be either a loan or a merchant cash advance, and the mechanics differ:

| Financing type | Repayment behavior in Stripe docs | Practical decision impact |

|---|---|---|

| Merchant cash advance | Payments vary with processing volume; no fixed payment schedule | Cash outflow flexes with sales, but still comes from Stripe receipts |

| Loan | Stripe describes minimum withholding checks, typically on a 30- or 60-day basis | You need to plan for shortfall pressure if sales are uneven |

What risk-first means in practice#

For a solo operator or small team, risk-first means protecting runway, avoiding repayment stress you might not be able to manually pace, and preserving your ability to change providers if needed. Start with three checks. First, confirm you actually have an offer, by email or in the Dashboard Capital tab. Next, identify whether it is a loan or MCA. Then remember that eligibility or notification is not final approval.

From there, work in order: product mechanics, true-cost math, risk audit, and alternatives.

Related: How to Open a Stripe Account for a Non-US Business.

What is Stripe Capital? (And Why It's Not a Traditional Loan)#

Stripe Capital is a financing program, not a single product. You may be offered either a term loan or a merchant cash advance, and you cannot request the type. That contract label is the first thing to verify because it changes how repayment risk shows up when sales slow.

Stripe describes an MCA as a purchase of future receivables, not a loan or credit transaction. In the same program, loans are business-purpose term loans issued by Celtic Bank with a maximum term and periodic payments. Even when both are repaid from Stripe sales, do not treat them as interchangeable; verify the contract mechanics against Stripe's Capital overview and the how Stripe Capital works documentation.

| Decision point | Term loan | Merchant cash advance |

|---|---|---|

| Product type | Business-purpose term loan issued by Celtic Bank | Purchase of future receivables, provided by YouLend or Stripe |

| Repayment mechanics | Fixed percentage withheld from Stripe sales, plus periodic minimum-payment checks | Fixed percentage withheld from Stripe sales, with payments varying by processing volume and no fixed payment schedule |

| Control over cash flow | Less control in slow periods if minimums are not met | More variable with sales volume because there is no fixed payment schedule |

| Early payoff behavior | Stripe states no late fees, early payment fees, or origination fees | Stripe states no late fees, early payment fees, or origination fees |

| If sales slow | If withholdings miss the minimum, Stripe can debit shortfalls from your linked bank account or account balance, typically checked every 30 or 60 days | Payments continue to vary with processing volume; no fixed periodic debit schedule is described |

Why the legal label changes your risk#

If your revenue is uneven, the practical risk changes with the contract type. With an MCA, payments move with processing volume, and Stripe says there is no fixed payment schedule or periodic debit. With a loan, Stripe also describes minimum-payment checks, typically every 30 or 60 days, and shortfalls can be debited from your linked bank account or Stripe balance.

Who you are actually dealing with#

Do not assume there is only one counterparty. Stripe is the interface, and its documentation says it is first-line support for servicing questions. But the financing party depends on the contract: loans are issued by Celtic Bank, while MCAs are provided by YouLend or Stripe. Check the named legal party in your agreement before accepting.

Eligibility is pre-screened, not self-directed#

You are generally pre-screened based on Stripe account signals, then notified by email and in the Dashboard Capital tab if an offer is available. For US businesses, Stripe says at least 3 months of processing history may be required before an offer appears, and financing requests are still subject to final review before approval.

What to verify in the Dashboard before you accept#

Before speed or convenience starts to sway you, confirm the parts that determine repayment behavior:

- Contract type: confirm whether the agreement is a loan or MCA.

- Named counterparty: verify whether the issuer or funder is Celtic Bank, YouLend, or Stripe.

- Repayment trigger terms: confirm the withholding percentage taken from Stripe sales.

- Minimum-payment language: for loans, check the 30- or 60-day minimum check and shortfall terms.

- Account-debit permissions: confirm whether Stripe can debit your linked bank account, Stripe balance, or both.

- Approval and timing: acceptance still goes through final review, even if funding is typically next business day.

Fast access can be useful, but speed is not the decision standard. If the contract type, shortfall-debit terms, or counterparty are unclear, pause and resolve that before accepting.

Calculating the True Cost: Beyond the "Flat Fee"#

Once you know whether the offer is a loan or an MCA, switch from dashboard simplicity to annualized cost. For Stripe Capital financing, the flat fee is fixed, but your repayment speed can vary with sales volume.

Stripe documents total repayment as advance amount + fixed fee, with repayment taken as a fixed percentage of sales. Start with the nominal fee rate, then convert it into a yearly comparison rate so you can compare offers on the same basis.

The number that helps you compare#

APR is a yearly cost-of-credit measure. For a loan offer, that is the direct comparison lens. For an MCA, use the same annualized math as a comparison tool against alternatives rather than as a quoted APR. The CFPB's APR explainer is a good benchmark for keeping that distinction clear.

- Collect your inputs

- Advance amount:

A- Fixed fee:

F - Expected repayment duration (days):

D

Current estimate pending finance/source-record verification. Because repayments are sales-based,Dis an estimate, not a fixed installment term.

- Fixed fee:

- Compute nominal fee rate

Nominal fee rate = F / A

- Compute annualized comparison rate

Annualized comparison rate ≈ (F / A) × (365 / D)

- Test three repayment-speed cases

- Slower

- Base

- Faster

Scenario table (same fee, different timing)#

| Repayment scenario | Expected duration | Annualized comparison rate | What to watch |

|---|---|---|---|

| Slower repayment | D_slow days | (F / A) × (365 / D_slow) | Lower annualized rate, but longer balance exposure |

| Base case | D_base days | (F / A) × (365 / D_base) | Primary planning case |

| Faster repayment | D_fast days | (F / A) × (365 / D_fast) | Same fixed fee, higher annualized rate because payoff is quicker |

Where misreads happen#

The most common mistake is stopping at F / A. That nominal fee rate is not a yearly cost metric, so it is not enough for a side-by-side financing decision.

The second mistake is assuming early payoff works like an interest-based product. Stripe states there are no early payment fees, late fees, or origination fees, and describes the fee as fixed rather than compounding. So faster repayment changes timing, but not the fixed fee itself.

If your offer is a loan, keep the minimum-payment checks in view, typically on a 30- or 60-day basis. Depending on sales volume and your offer terms, withheld sales may not satisfy the minimum, and shortfalls can be debited from your linked bank account or Stripe balance. Stripe's servicing documentation is the reference point for those mechanics.

Before accepting, run one checkpoint. Compare your base-case and faster-case annualized rates against at least one alternative quote, such as a revolving working-capital line or another business financing option. Then compare both against your own cash-flow volatility.

Auditing the Risks to Your Autonomy and Cash Flow#

If the fee looks workable, audit the repayment mechanics next. The real question is simple: when sales are normal, slow, or absent, do you still control enough cash timing to run the business safely?

The three risks to check are straightforward. Platform dependency means eligibility and repayment collection are tied to payments you process through Stripe. Repayment-control loss means a fixed share of sales is deducted automatically, so you do not choose repayment timing. Lumpy-revenue mismatch means uneven sales can create liquidity stress, especially when a loan has minimum-payment checks.

Start with the offer type, not the brand#

The first branch in the risk audit is the contract itself. Stripe states that an offer can be either a loan or a merchant cash advance, and you cannot request a specific type.

For loans, Stripe documents a maximum term and periodic payment obligations. It also says shortfalls can be debited from your linked bank account or Stripe balance when withholdings do not meet the minimum, typically checked on a 30- or 60-day basis. For MCA structures, its guidance describes a receivables purchase, not a loan, and says there should be no bank debits in an MCA program.

Where your control can tighten#

Repayment is withheld from Stripe-processed sales, so financing and payment operations become more tightly coupled. If Stripe is your main inflow rail, that coupling matters more.

Stripe also describes repayment as a fixed percentage of sales until the balance is paid. In stronger periods, paydown speeds up. In slower periods, it eases. The tradeoff is that cash is withheld before you decide other priorities for that period.

If revenue is uneven, test the downside explicitly. Stripe’s servicing example shows the mechanism. If 7% withholding over 60 days was expected to satisfy a 2,000 USD minimum but only 1,500 USD was withheld, the remaining 500 USD can be debited from your bank account or Stripe balance.

Your risk-audit checklist#

| Trigger event | What happens to inflows | What happens to repayments | What fallback options remain |

|---|---|---|---|

| Normal Stripe sales period | Net cash is reduced by withholding | Fixed percentage is withheld automatically until balance is paid | Additional or manual paydown is available; no prepayment penalty is stated |

| Slow Stripe sales period | Gross inflow and withheld amount both may decline | Loan minimum checks may still apply on a 30- or 60-day basis | Use reserves if needed; confirm whether your offer is loan or MCA |

| Very low or zero Stripe sales in the check window | Little or no repayment from withholding | For loans, shortfall can be debited from linked bank account or Stripe balance | Bank buffer and/or manual paydown |

| You route more sales outside Stripe after funding | Less Stripe-linked inflow available for collection | Withholding slows; loan minimum risk can increase | Proceed only with a clear repayment plan if Stripe-linked volume drops |

| Sales accelerate faster than expected | Higher inflow but faster effective paydown | Balance may clear sooner; fee and payment rate remain the terms set in your offer | Confirm you can operate with reduced day-to-day cash discretion |

Quick decision scenario#

Map your real cycle before accepting: the financing type (loan or MCA), the repayment rate from your offer, and the minimum check cadence (30/60-day or as stated in the offer for loans). Then pressure-test one low-collection window. If withholdings undershoot, can your linked bank account absorb a modeled shortfall without disrupting core obligations? If that answer depends on optimistic timing, treat the liquidity risk as high.

Pass or fail#

Pass only if the repayment mechanics fit your cash pattern: financing type is verified, shortfall behavior is clear, and you can absorb a weak collection window while automatic withholding runs.

Treat the offer as high risk if revenue is uneven, buffers are thin, or you need manual control over payment timing. If you cannot clearly explain what happens in a zero-sales period, pause and resolve that before accepting.

Stripe Capital vs. A Business Line of Credit: A Strategic Comparison#

If control and payment-rail flexibility are top priorities, compare how tightly repayment is tied to Stripe-processed sales. If speed matters most and most of your inflow already runs through Stripe, an offer here can still fit, but only when the repayment mechanics match your cash-flow pattern and margins.

Start by defining the products clearly. A Stripe Capital offer can be either a loan or a merchant cash advance, and Stripe says you cannot choose the type. A business line of credit is a revolving credit account: you draw, repay, and draw again, with interest generally charged only on the amount you use.

Decision matrix#

| Decision factor | Stripe Capital offer (loan or MCA) | Revolving business line of credit |

|---|---|---|

| Eligibility access | Stripe says eligibility is based on account factors such as payment volume and history, updates daily, and, for US businesses, may require at least 3 months of processing history to receive an offer. You also cannot request a specific financing type. | Access depends on lender underwriting and product terms. For SBA-backed options, revolving lines are permitted only under SBA Express, Export Express, or CAPLines. |

| Funding speed | Stripe says funds are typically deposited into your Stripe account by the next business day after review. | Timing varies by lender and review process. |

| Pricing structure | Stripe documents total payback as advance amount plus a flat fee. | Interest typically starts when you draw and applies to the borrowed portion; agreement terms determine rates and fees. |

| Repayment mechanics | Stripe says repayments are withheld from Stripe sales. For MCA offers, payments vary with processing volume and there is no fixed payment schedule. For loan offers, Stripe describes maximum terms, periodic payments, and possible shortfall debits when minimums are not met, typically checked on a 30- or 60-day basis. | Repayment follows the lender agreement. The line is generally reusable after repayment, which helps when needs recur. |

| Operational control | Financing and collections are tightly coupled to Stripe-processed sales. | Repayment mechanics are set by the lender agreement. |

Document-level checks matter more than product labels. For a Stripe offer, confirm financing type, total payback, and whether loan minimum checks apply on a 30- or 60-day cycle. For a line of credit, confirm interest method, draw rules, repayment timing, and reuse terms. Stripe’s line-of-credit explainer notes draw periods are typically up to 24 months, but your lender agreement controls.

Which path fits your situation?#

If your revenue is predictable and seasonal, and the use case is short and specific, a Stripe offer can be workable when payback aligns with expected Stripe sales.

If revenue is project-based or uneven, a revolving line can be a better fit because you draw when needed and the line is reusable after repayment.

If preserving processor flexibility is a priority, compare how each option handles repayment before deciding.

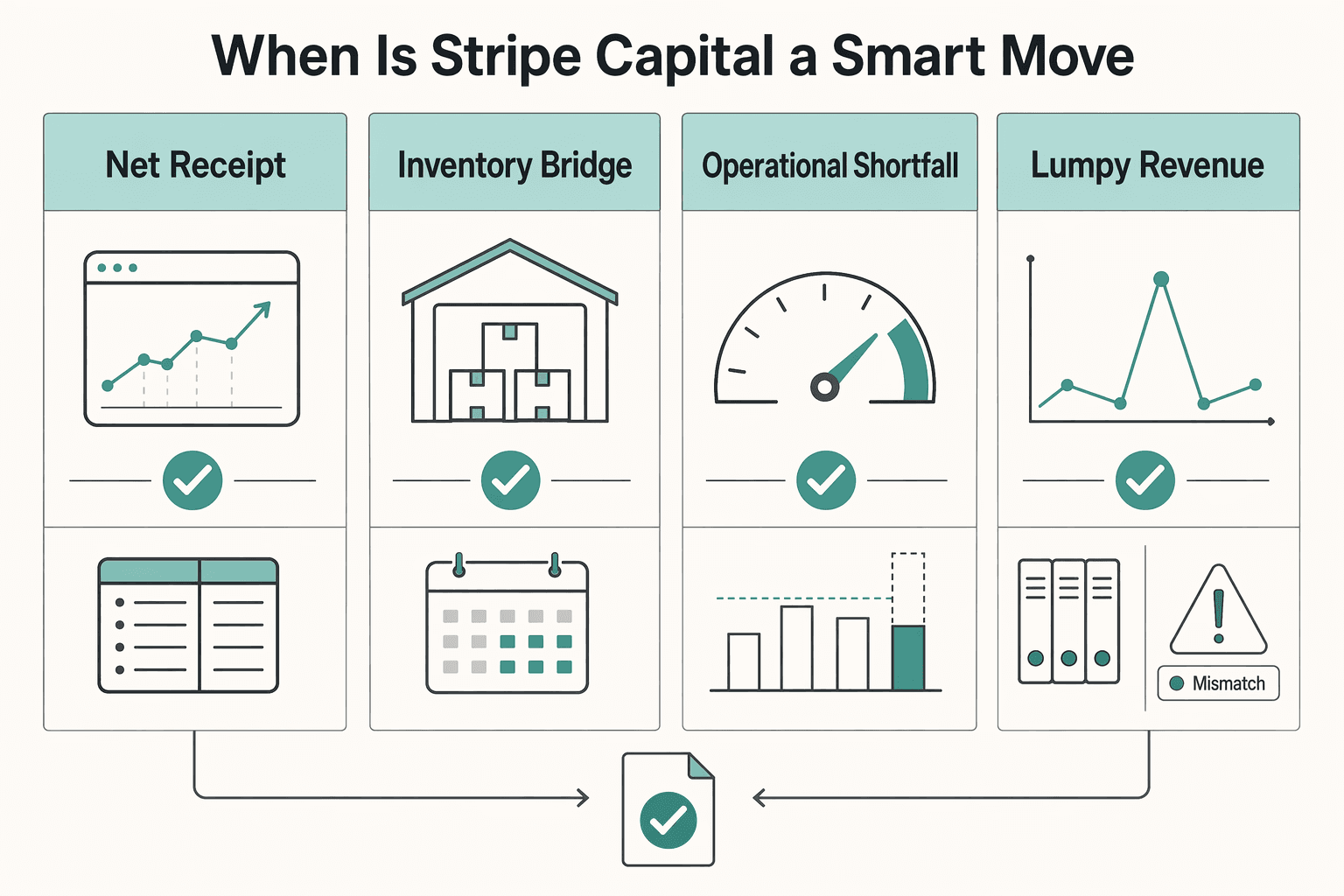

The Strategic Use-Case Matrix: When is Stripe Capital a Smart Move?#

Use Stripe Capital only when repayment clearly matches the revenue event you are funding. It can be a smart move when revenue is near-term, expected to process through Stripe, and strong enough to absorb the flat fee plus automatic withholding.

| Use case | Why Stripe Capital can fit | Primary risk signal | Better alternative if risk appears |

|---|---|---|---|

| Strategic growth, only if you can verify a steady processing record, a predictable revenue path, a short payback window, and a margin cushion. Current payback window pending source-record verification; current margin cushion pending finance-record verification. | It can fit when spending is tied to a specific revenue unlock, for example, a launch, fulfillment ramp, or time-sensitive capacity increase, and those sales are expected to land in Stripe soon after funding. | Revenue depends on a long or uncertain sales cycle, or meaningful sales will settle off Stripe. If the offer is a loan, weak sales can still trigger minimum-payment pressure. | Business line of credit if you want draw timing and repayment mechanics that are not tied to one processor |

| Inventory bridge, only if demand is seasonal or already visible, sell-through is short, and gross margins can absorb the fee | This can be a strong fit: costs rise first, then sales can repay through Stripe withholding as inventory converts. | Sell-through slows, discounting compresses margin, or too much volume shifts off Stripe, so repayment no longer matches the inventory cycle. | Business line of credit, especially for multi-channel sales and tighter repayment control |

| Operational shortfall, such as rent, payroll, or recurring software bills | Can be a poor fit when the funding covers a gap instead of creating near-term revenue. | You are repeatedly using short-term funding to support a longer-term deficit. | Line of credit only for a true timing gap; otherwise reduce burn, reprice, or tighten collections |

| Lumpy revenue while you wait for a client invoice or project payout | Can be a weak fit when repayment timing depends on delayed receivables. Repayment still comes from Stripe sales, not from the invoice unless that payment arrives there soon. | Inflows arrive in bursts, low-volume periods are common, or clients pay outside Stripe. Loan minimum checks can add pressure before a receivable clears. | Invoice financing for a specific receivable, or a line of credit for broader flexibility |

Before you treat any "smart" case as approved, verify the actual offer terms. Stripe says you cannot choose financing type, so confirm loan vs. MCA, the withholding rate, total payback, and whether loan minimums are checked on a 30- or 60-day cycle.

Use a simple go or no-go evidence check. Identify what revenue this funding is meant to create, when that revenue should arrive, whether it will process through Stripe, and how much margin buffer you still have if timing slips. The common failure mode is a mismatch between automatic repayment and delayed, off-platform, or thinner-than-expected revenue.

- Go if funding is tied to identifiable revenue creation, Stripe volume is steady, and payback stays inside your margin cushion.

- Caution if the opportunity is plausible but timing, channel mix, or financing type is unclear. Verify loan vs. MCA, withholding, total payback, and any minimum-payment language first.

- Avoid if you are covering recurring overhead, waiting on a large receivable, or prioritizing maximum cash-flow control. In those cases, a business line of credit is usually cleaner.

For a step-by-step walkthrough, see A Guide to Stripe Radar for Fraud Protection. Before you accept any offer, run the numbers against your current setup with the payment fee comparison tool.

Conclusion: A Tool, Not a Crutch#

Use Stripe Capital for speed only when it passes a risk-first check. Funds may arrive by the next business day, but convenience is not a decision rule. For any stripe capital financing offer, run the same three checks: verify true cost, test cash-flow resilience, and confirm the control tradeoff.

Start with cost. Stripe describes total repayment as your advance plus a flat fee. For comparison, translate total cost into an annualized metric, and use APR when comparing loan options. That remains true even though Stripe says there are no late fees, early payment fees, or origination fees. A fixed fee can still be expensive on an annualized basis if repayment happens quickly.

Next, verify the financing type in your agreement. Stripe says offers might be a loan or a merchant cash advance, and you cannot request a specific type. That changes repayment risk. For an MCA, payments vary with processing volume and there is no fixed payment schedule or periodic debit. For loans, shortfalls can be debited from your linked bank account or account balance, with minimum-payment checks typically on a 30- or 60-day basis.

Use this final filter to decide:

- Proceed if the funds are for a specific short-term use, most of your revenue runs through Stripe, your margins can absorb the fixed sales deduction, and the agreement terms fit your cash-flow pattern.

- Pause if your revenue is lumpy, you need tighter repayment control, or any policy point still needs official/provider verification.

- Decline if the advance is covering a recurring operating gap, or if it would make you too dependent on one processor for both revenue and funding.

One last check: financing requests are still subject to final review before approval, so do not plan around the money until approval is confirmed. Financing should strengthen your payment system and long-term independence, not patch a recurring operating weakness.

If you want a more resilient get-paid workflow with fewer operational surprises, review Merchant of Record for freelancers.

Frequently Asked Questions

What is the real cost of Stripe Capital?

The real cost is its effective Annual Percentage Rate (APR), not the simple flat fee. Because the fee is fixed, repaying faster due to strong sales significantly increases your effective APR. There is also an inflexibility cost: unlike a traditional loan, you cannot save money by paying it off early.

What are the biggest risks of using Stripe Capital?

The primary risks are the loss of control and autonomy. Specifically: Platform Dependency (tying financing to your payment processor creates a single point of failure), Loss of Cash Flow Control (the automated daily repayment model removes your ability to strategically manage daily cash flow), and The 'Lumpy Revenue' Trap (the minimum payment requirement is a significant danger for consultants and freelancers with irregular income).

Is Stripe Capital a good idea for freelancers or consultants?

Generally, no. It is a high-risk tool for service-based professionals. The business model of a consultant—based on large, infrequent project payments—is fundamentally mismatched with Stripe Capital's model of daily repayments and periodic minimum payment obligations.

How does Stripe Capital compare to a business line of credit?

Stripe Capital prioritizes speed and convenience, while a business line of credit prioritizes flexibility, control, and cost-efficiency. A line of credit is platform-agnostic, allows you to draw and repay funds as needed, and typically has a lower effective APR. For professionals managing uneven cash flow, a line of credit is almost always the more prudent choice.

Does taking a Stripe Capital loan affect my personal credit score?

No. Eligibility is determined by your business's sales volume and history on the Stripe platform, not your personal credit history.

What happens if my sales drop to zero while I have a Stripe Capital loan?

Your obligation continues. Stripe Capital loans have a minimum payment requirement that must be met over a set period (e.g., every 60 days). If withholdings from your sales do not meet this minimum, Stripe will automatically debit the remaining balance from your connected bank account.

Can I repay my Stripe Capital loan early to save on fees?

No. While you can repay the total amount owed at any time without an early repayment penalty, doing so does not save you any money. The flat fee is fixed, regardless of how quickly you pay it back.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-lo...trusted

- consumerfinance.gov/compliance/compliance-resources/small-busine...trusted

- docs.stripe.com/capital/how-stripe-capital-workstrusted

- docs.stripe.com/capital/overviewtrusted

- ecfr.gov/current/title-12/chapter-X/part-1026/subpart...trusted

- ecfr.gov/current/title-13/chapter-I/part-120/subpart-...trusted

- fdic.gov/consumer-resource-center/loanstrusted

- federalreserve.gov/boarddocs/rptcongress/fc_study.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

How to Open a Stripe Account for a Non-US Business

**Treat your Stripe setup as a system for cashflow, not a quick signup, so your first payouts are more predictable.** If you run a small business, this is one of those setup decisions where "close enough" gets expensive later. If you are a nonresident operator, the pain usually shows up in a few places: payout delays, avoidable verification loops, and uncertainty about which path actually fits your business. If you guess early, you usually create rework later, especially when invoices are already waiting.

What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising?

A SAFE, short for Simple Agreement for Future Equity, is a contract where an investor gives you money now in exchange for a future ownership interest if a trigger event happens, often a later equity financing or an acquisition of the company. It usually fits an early raise when you need speed, simpler documents, and the ability to close investors one by one. It is a weaker fit when investors want negotiated control rights now, or when you need exact dilution certainty before taking money.