Quick Answer

Start by running your special needs trust as an operating routine, not a one-time filing. Trace funding ownership to pick the correct structure, then review each payout by payee type and shelter exposure before money goes out. Keep distribution logs with invoices and brief rationale notes, and hold a scheduled yearly review of titling, benefit outcomes, and team responsibilities. That process reduces avoidable SSI problems and keeps you ready for agency follow-up.

Phase 1: Designing the Trust Architecture#

Start with one decision: whose assets will fund the trust. That choice sets the rest of the architecture because it drives eligibility treatment, drafting requirements, and whether payback language may apply.

Pick the trust type by tracing asset ownership#

Use pre-transfer ownership as your split point.

| Situation | Likely trust path | When this applies | Key eligibility point | Common mistake to avoid |

|---|---|---|---|---|

| The beneficiary owns the assets before funding | First-party trust | Assets are already titled to the beneficiary | SSA exception criteria include disability and being under age 65, but the trust still requires resource analysis | Assuming "under 65" means SSI will automatically disregard the trust |

| Someone other than the beneficiary (or spouse) funds the trust | Third-party trust | Family or other third parties fund the trust directly | SSA treats this as third-party funding, but distributions can still affect SSI depending on payment method | Letting assets pass to the beneficiary first and trying to fix eligibility later |

| Ownership is mixed or unclear | Pause and trace funds before drafting | Records, title history, or transfers are unclear | Funding source is the first architecture split, and trust analysis is state-law dependent | Commingling beneficiary and non-beneficiary assets without a clean paper trail |

For first-party planning, keep the age condition explicit. SSA's special-needs-trust exception is for a disabled individual under age 65. California DHCS states that a (d)(4)(A) SNT can be established only for a disabled individual under 65. Even then, SSA says the trust must still be evaluated under broader resource rules.

In California, DHCS also states that the trust must include notice and payback provisions to the State at death or earlier termination. Treat that as a state-specific drafting issue, not a universal rule for every trust type in every jurisdiction.

Build spending rules around payment method#

Once the structure is set, payment method becomes the main operating risk. The practical rule is to support the beneficiary without creating avoidable countable income or SSI-sensitive ISM outcomes.

Since September 30, 2024, SSA no longer includes food in SSI ISM calculations, so shelter is the main ISM-sensitive category here. Cash paid directly from the trust to the beneficiary is still unearned income. SSA also indicates that certain third-party non-cash items, other than food or shelter, are not income.

Trustee payment checklist#

Before money leaves the account, the trustee should work from the same short checklist every time:

- Pay vendors or service providers directly where possible.

- Treat direct cash to the beneficiary as a flagged decision that requires benefit-impact review first.

- Treat shelter-related payments as review-required, not routine.

- Keep the invoice, proof of payment, and a short trustee note on the benefit check performed before payment.

- Maintain a distribution log with payee, amount, date, purpose, and pre-payment eligibility review.

Stress-test cross-border facts before funding#

If the grantor, trustee, beneficiary, or assets span countries, pause before signing or funding. Do not classify the arrangement based only on mailing address or residence. U.S. trust status uses the court and control tests.

| Checkpoint | Form or test | Key point |

|---|---|---|

| Grantor location | Form 3520 | Foreign-trust transactions can trigger Form 3520, filed separately for each foreign trust |

| Asset location | FBAR (FinCEN Form 114) | Foreign accounts can trigger FBAR if aggregate value exceeds $10,000 at any point in the calendar year |

| Beneficiary or trustee location | Court and control tests | Residence alone does not determine trust status |

| Reporting responsibility | Form 3520-A | A foreign trust with at least one U.S. owner has an annual Form 3520-A return |

| Timing | Form 3520 due date | Generally due the 15th day of the 4th month after tax year end, or the 15th day of the 6th month for taxpayers living and working outside the United States |

Use this checkpoint list before signing or funding:

- Grantor location: foreign-trust transactions can trigger Form 3520, filed separately for each foreign trust.

- Asset location: foreign accounts can trigger FBAR (FinCEN Form 114) if aggregate value exceeds $10,000 at any point in the calendar year.

- Beneficiary or trustee location: residence alone does not determine trust status.

- Reporting responsibility: a foreign trust with at least one U.S. owner has an annual Form 3520-A return.

- Timing: Form 3520 is generally due the 15th day of the 4th month after tax year end, or the 15th day of the 6th month for taxpayers living and working outside the United States.

When these facts are present, consider review by U.S. tax counsel and local counsel before funding. Trust interpretation is state-law dependent and may require legal counsel.

Recheck funding and distributions annually#

A signed trust is the start of operations, not the finish line. Run an annual review of asset titling, prior-year distributions, benefit outcomes, and filing triggers.

Recheck the assumptions that tend to drift over time: spending needs, inflation, investment performance, care setup, and trustee capacity. Keep a year-end file with statements, distribution logs, benefit notices, and any relevant Form 3520, 3520-A, or FBAR filings. Add a placeholder to verify current program and tax thresholds for the applicable state and tax year before relying on prior numbers. You might also find this useful: A Guide to Superannuation for Australian Freelancers.

According to SSA, changes that affect SSI should be reported as they happen, not reconstructed months later. Before each annual review, confirm current reporting steps on SSA's reporting changes page and refresh any delegated-support paperwork with How to Set Up a Power of Attorney for Financial Matters if the support team changed.

- Log the current 2026 review date, reporting contact, and benefit-notice checklist in the trust file.

- Match recent vendor payments to receipts before the meeting starts.

- Flag any housing or living-arrangement change that could alter future SSI treatment.

Phase 2: Assembling Your High-Performance Trust Team#

Once the design is set, the main risk shifts from drafting to execution. In this phase, the goal is to assign clear owners for drafting, administration, oversight, and advice so distribution decisions, benefits issues, and appeals do not stall.

2025 SNT administration materials highlight the same pressure points. They include public-benefits complexity, uncertainty in administration, Medicaid appeals strategy, drafting language, trust protectors and co-trustees, conflicts of interest, and oversight of delegated fiduciary duties. Use that as your hiring risk map.

Interview counsel like an operator#

Hire counsel for administration readiness, not just drafting quality. You need someone who can explain how the trust will run after signing. That includes how benefit-sensitive decisions are reviewed and how issues get escalated when something goes wrong.

| Area | Questions |

|---|---|

| Special-needs trust experience | Ask for recent SNT matters and what happened after funding, especially where administration became complicated |

| Benefits coordination approach | Ask how distribution decisions are reviewed when public-benefits impact is possible, and how appeal-related issues are handled |

| Complex-case handling | Ask how they handle unusual fact patterns and when they bring in outside specialists |

| Trustee guidance | Ask what operating guidance trustees receive and how successor trustees are prepared |

| Rule-change updates | Ask how rule changes are tracked and how clients are updated when changes affect administration |

Use this interview framework:

- Special-needs trust experience: Ask for recent SNT matters and what happened after funding, especially where administration became complicated.

- Benefits coordination approach: Ask how distribution decisions are reviewed when public-benefits impact is possible, and how appeal-related issues are handled.

- Complex-case handling: Ask how they handle unusual fact patterns and when they bring in outside specialists.

- Trustee guidance: Ask what operating guidance trustees receive and how successor trustees are prepared.

- Rule-change updates: Ask how rule changes are tracked and how clients are updated when changes affect administration.

A practical check is to ask for a redacted sample of trustee operating materials, such as a distribution review checklist or annual review agenda. If they cannot show process materials, expect more execution burden on your side.

Choose the trustee by failure mode, not title#

The trustee role is where administration either holds together or starts to slip. Compare options by decision quality, documentation discipline, continuity planning, and conflict controls, not familiarity alone.

| Trustee option | Failure modes to pressure-test |

|---|---|

| Family member | Can they follow written processes for recurring and exception requests, and is there a clear backup during illness, burnout, or incapacity? |

| Professional fiduciary | Can they manage benefits-sensitive administration with strong records, and how are successor coverage and conflict checks handled? |

| Corporate trustee | Can they support your case within their service model, and how are account transitions and escalation contacts handled? |

Set authority lines before money moves#

Do not leave authority boundaries to custom or assumption. Write them plainly in the trust documents and related appointments.

Role boundaries are document-specific and should be confirmed before administration begins. Make sure the team has clear, written authority for funding decisions, distributions, protector actions, and advisory input.

Keep one rule explicit: delegated fiduciary duties still require oversight. If each professional assumes someone else is checking benefits impact, conflicts, or appeal readiness, critical controls fail.

Onboard the team with one operating checklist#

Before the first meaningful administration decision, run one formal handoff so everyone works from the same operating file. This is where you turn a signed document into an operating plan.

- Document handoff: Signed trust and amendments, benefit records, care summary, contact map, and prior distribution records. Include placeholders to verify current legal, program, and tax requirements before relying on prior practice.

- Communication protocol: Primary family contact, urgent decision owner, routine update channel, and who receives notices and statements.

- Distribution review workflow: Intake owner, benefits-impact reviewer, required backup, approval notes, and storage location for records.

- Escalation path: First contact for denied benefits, suspected mismanagement, or conflicts, plus when separate counsel is required.

If the team cannot explain this process clearly, the roles are still too ambiguous. Related: A Guide to Estate Planning for Digital Nomads.

Phase 3: Activating the Trust: A Playbook for Flawless Governance#

Once roles are assigned, the work becomes operational. A special needs trust performs best when the trustee handles distributions, reporting, and document upkeep as a repeatable routine rather than case-by-case improvisation.

Most breakdowns are small and preventable. A payment goes out before SSI impact is checked, the Letter of Intent is outdated, or the current trust documents are hard to produce during review. Those can lead to benefit reductions or avoidable delays.

Build a Letter of Intent someone can actually use#

Make the Letter of Intent practical enough that a successor can use it under pressure. It is not legally binding, and it should be updated at least once a year. Treat it as a living operating guide, not a one-time memo.

| Section | Include |

|---|---|

| Beneficiary profile | Daily supports, routines, health context, key providers, and what a stable week looks like |

| Decision principles | How to weigh quality of life, independence, dignity, and risk when trustee discretion applies |

| Care preferences | Preferred caregivers, activities, therapies, housing priorities, and known stressors |

| Communication norms | Who gets routine updates, and who is alerted for urgent issues, denied services, or benefits notices |

| Update ownership | One named owner for revisions, version dates, and distribution of the current copy to trustees and successors |

Use this five-part template:

- Beneficiary profile: daily supports, routines, health context, key providers, and what a stable week looks like.

- Decision principles: how to weigh quality of life, independence, dignity, and risk when trustee discretion applies.

- Care preferences: preferred caregivers, activities, therapies, housing priorities, and known stressors.

- Communication norms: who gets routine updates, and who is alerted for urgent issues, denied services, or benefits notices.

- Update ownership: one named owner for revisions, version dates, and distribution of the current copy to trustees and successors.

Put the version date on page one and retain prior versions so a successor can identify the current document immediately.

Give the trustee a payment screen before money leaves the account#

Use an SSI-focused distribution screen before every disbursement. This is where routine discipline prevents avoidable benefit problems.

SSA says direct cash paid to the beneficiary reduces SSI. Shelter payments can also reduce SSI, but only up to SSA's applicable limit. Payments made directly to a vendor for items other than food and shelter do not reduce SSI under SSA trust spotlight guidance. Since September 30, 2024, food is no longer included in ISM calculations, but Medicaid treatment can still vary by state.

| Usually lower SSI risk | Gray area, review first | Higher SSI risk |

|---|---|---|

| Medical care, therapies, adaptive equipment, education, technology, recreation, and personal services paid directly to vendors | Food payments after 09/30/2024 (not counted as SSI ISM, but still worth confirming broader program impact), bundled invoices that may include shelter, and reimbursement requests without clear receipts or purpose | Cash paid directly to the beneficiary |

| Clearly non-shelter, non-food items with complete documentation | Requests tied to trust amendments, benefit-status changes, or unclear payee details | Shelter costs paid to another party for the beneficiary |

| Vendor-paid quality-of-life expenses supported by invoices | Mixed-purpose charges where the non-shelter portion cannot be separated cleanly | Payments released before confirming whether they are direct cash or shelter-related |

Use this pre-disbursement check flow:

- Confirm payee: beneficiary, vendor, or third party.

- Classify whether the request includes shelter.

- Verify current benefit status and governing trust documents.

- Save the invoice, rationale, and approval note before funds are sent.

This record matters because SSA evaluates trust distribution income implications in post-eligibility review and requires trust document review for trust resource determinations.

Define the reporting packet, not just the cadence#

A reporting schedule helps only if every cycle produces the same core packet. Set the cadence from your trust document, state law, and advisor guidance, then require the same governance file each time:

- Account activity: balances, inflows, outflows, and exceptions.

- Distribution rationale log: what was paid, to whom, and why.

- Unresolved issues: open benefits, administration, or documentation items.

- Pending compliance items: who owns each item and due timing.

Keep compliance checks explicit. SSI recipients or representative payees must report changes that can affect benefits, including changes in income and resources. For federal tax compliance, Form 1041 is due by the 15th day of the fourth month after the trust tax year closes. For a calendar-year trust, that is April 15.

Make the annual review produce decisions#

An annual review should end with decisions, not just discussion. Capture these three outputs in writing:

- What changed in the beneficiary's needs.

- What policy or process changes are now required.

- Who is accountable for each follow-through item before the next review.

Track each action with an owner, deadline, and closure evidence. If benefits status changed, the trust was amended, or distribution patterns shifted, trigger document review immediately instead of waiting for the next cycle.

If you want a deeper dive, read A Guide to Setting Up a Trust for Asset Protection.

If your trust governance includes cross-border income or relocation risk, track jurisdiction changes in one place with the Tax Residency Tracker.

From Anxiety to Agency: Taking Command of Your Family's Legacy#

After signing, your job is straightforward: keep the structure sound, keep decision-makers accountable, and keep the review routine active so benefit issues are caught early.

Phase 1 put you in control of structure. You should be clear on whose assets are in the trust. You should also know whether an SSA exception is being used. For the special-needs-trust exception, conditions such as disability, being under age 65, and the correct establishing party apply. Even when a trust appears to meet an exception, SSA says it still must be evaluated under other countable-resource rules, so treat funding changes as review triggers.

Phase 2 put you in control of decision-makers. You need clear ownership for distribution approvals, recordkeeping, and agency responses. Documentation is critical: money paid directly to the SSI recipient reduces SSI, and shelter payments can reduce SSI up to a limit. If someone on your team is also a representative payee, SSA can require expense records and an accounting.

Phase 3 put you in control of governance routines. Keep a repeatable process for benefit-impact checks, document updates, and fast response to SSA requests. SSA redeterminations for most SSI recipients occur once every 1 to 6 years, and appointment letters or forms generally require a response within 30 days. Report listed SSI changes, including living situation, resources, or marital status, no later than the tenth day of the following month.

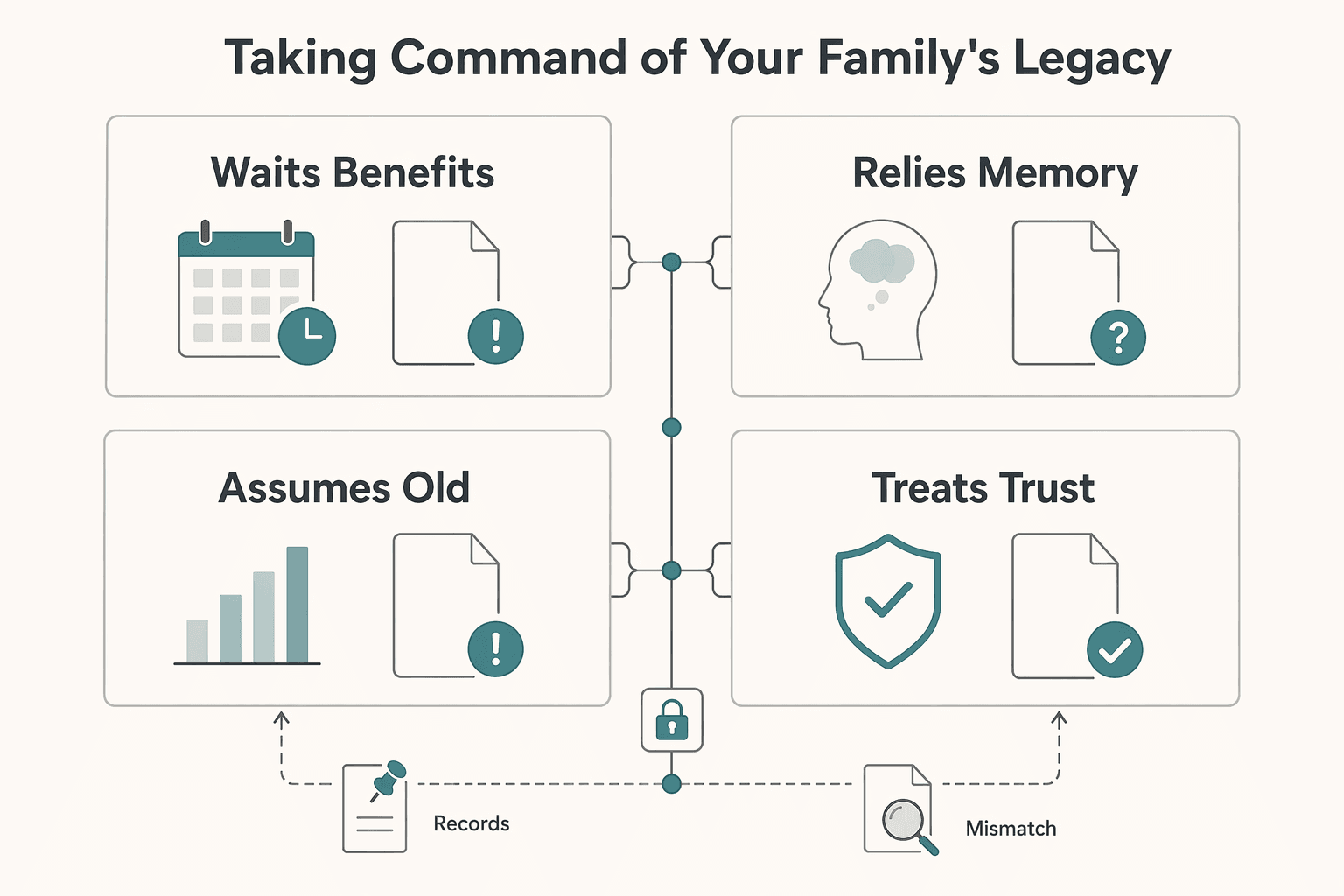

| Anxiety-driven approach | Agency-driven approach |

|---|---|

| Waits for a benefits problem before reviewing distributions | Reviews higher-risk payments before funds are released |

| Relies on memory and informal updates | Keeps receipts, payment logs, and brief benefit-impact notes |

| Assumes old rules still apply | Re-checks current SSA rules, including the ISM food update effective September 30, 2024 |

| Treats the trust as a one-time setup | Runs it as an ongoing care and benefits-protection process |

What you do now:

- Set a recurring review cadence, and trigger an extra review after funding, housing, or living-situation changes.

- Keep the signed trust, amendments, and distribution records together in one accessible file.

- Confirm who reports SSI changes, who maintains records, and who responds to agency requests.

- Check SSI impact before direct cash or shelter-related payments, then re-check when SSA guidance changes.

For a step-by-step walkthrough, see How to Set Up a Power of Attorney for Financial Matters.

When you are ready to align trust funding with cross-border money movement, contact Gruv to confirm coverage and compliance controls for your market.

Frequently Asked Questions

What is the practical difference between a first-party and third-party special needs trust?

In the New Jersey Medicaid framework cited here, the SNT under 42 U.S.C. 1396p(d)(4)(A) is a trust that contains the disabled individual’s own assets. If the funds belong to the beneficiary, NJ Medicaid review and reimbursement rules can apply. If the funds come from someone else, this FAQ alone does not resolve all outcomes, so confirm the structure with counsel.

What to do next: Map each planned funding asset to its true owner before drafting or funding.

Does Medicaid payback apply?

For the NJ Medicaid trust described above, yes: at the beneficiary’s death, New Jersey Medicaid must be reimbursed up to total benefits paid. If trust funding comes from personal injury proceeds, related Medicaid payments must be reimbursed before the trust is established.

What to do next: Confirm payback exposure and clear any injury-related Medicaid claims before funding.

What can the trust pay for?

Use a simple sole-benefit test. Generally allowed: the beneficiary’s special needs, plus appropriate and reasonable trust fees when they align with New Jersey law and your trust terms. Review before paying any expense you cannot clearly document as for the beneficiary’s sole benefit.

What to do next: Keep the invoice, payee details, and a short sole-benefit note for each payment.

Who can establish the trust, and when must it be funded?

Under the NJ FAQ, a parent, grandparent, legal guardian, or a court can establish the trust. Deposits must occur before the individual reaches age 65. If the person is already Medicaid-eligible, newly acquired assets funding the trust must be reported as a resource change.

What to do next: Confirm the authorized setup party and screen planned deposits against the age-65 timing rule.

Who can serve as trustee or co-trustee?

This New Jersey Medicaid FAQ does not define trustee eligibility, co-trustee rules, or trust protector authority. Treat this as a legal-structure decision, not an assumption. A practical checkpoint is whether the proposed fiduciary can carry out the trust terms and keep records needed for sole-benefit administration and agency review.

What to do next: Get written counsel guidance on who may serve, who signs, and who maintains records.

What does Medicaid review when the trust is submitted?

The eligibility determination agency receives the trust and its completed Schedule A listing funding assets. Required trust language is also tied to N.J.A.C. 10:71-4.11(g)1. Submit complete materials so the agency can review the trust and funding assets together.

What to do next: Keep the signed trust, completed Schedule A, and funding records together before submission or any resource-change report.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

When a Trust for Asset Protection Makes Sense for Your Business

Use a trust only after your core liability setup is solid. A trust for asset protection is an escalation layer, not a substitute for entity separation, insurance, or clean operations.

Estate Planning for Digital Nomads: Legal Intent and Cashflow Continuity

Treat estate planning for digital nomads as a two-part continuity system: legal intent plus operational execution, so your business keeps moving when you cannot. The common trap is thinking, "I have a will, so I'm covered." If you run a business-of-one, cashflow, logins, and process often live in your head until you deliberately externalize them.

A Guide to Superannuation for Australian Freelancers

**Treat superannuation for freelancers australia as a repeatable operating decision, not a guess you make under invoice pressure.** As the CEO of a business-of-one, your job is to turn fuzzy compliance questions into a simple system you can run on demand. Freelance income moves, contract terms shift, and one wrong super call can squeeze cashflow or create a compliance problem you only notice later.