Quick Answer

Yes. A section 351 transfer can defer gain when property is contributed to a corporation solely for stock and the transferor group meets Section 368(c) control immediately after closing. Verify ownership by stock class at the actual close sequence, isolate any service-related items excluded by Section 351(d), and model any boot under Section 351(b) before signing. If a binding prearranged step changes who controls the corporation, stop and get written tax advice.

Section 351 can defer tax when you incorporate, but only if the structure is clean#

A Section 351 transfer can defer gain when property is transferred to a corporation solely for stock and the transferor group is in control immediately after the exchange under 26 U.S.C. § 351(a). In practice, eligibility turns on structure, sequencing, and records, not just the label on the deal.

The control test is strict under Section 368(c): at least 80 percent of total combined voting power and at least 80 percent of shares of all other stock classes. This is a cap table test, not a general "founders still own most of the company" standard.

Timing matters just as much. Under 26 CFR 1.351-1(a)(1), "immediately after" does not always require perfectly simultaneous steps if party rights are defined in advance and execution is orderly. But a prearranged binding agreement that results in a taxable sale to a third party can break control for Section 351 purposes, as reflected in Rev. Rul. 2003-51 and its 40%/60% post-step ownership outcome.

Before signing or issuing stock, lock the transaction sequence in writing and verify:

- what property is being transferred

- what stock is issued solely in exchange

- who owns each class immediately after all planned steps

For globally mobile freelancers, keep the file defensible: signed transfer documents, stock issuance records, ownership support, and a dated timeline that matches the transaction steps. This guide walks through the eligibility gates, the control checks, the prearranged-deal red flags, and the minimum evidence set needed to support deferral. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

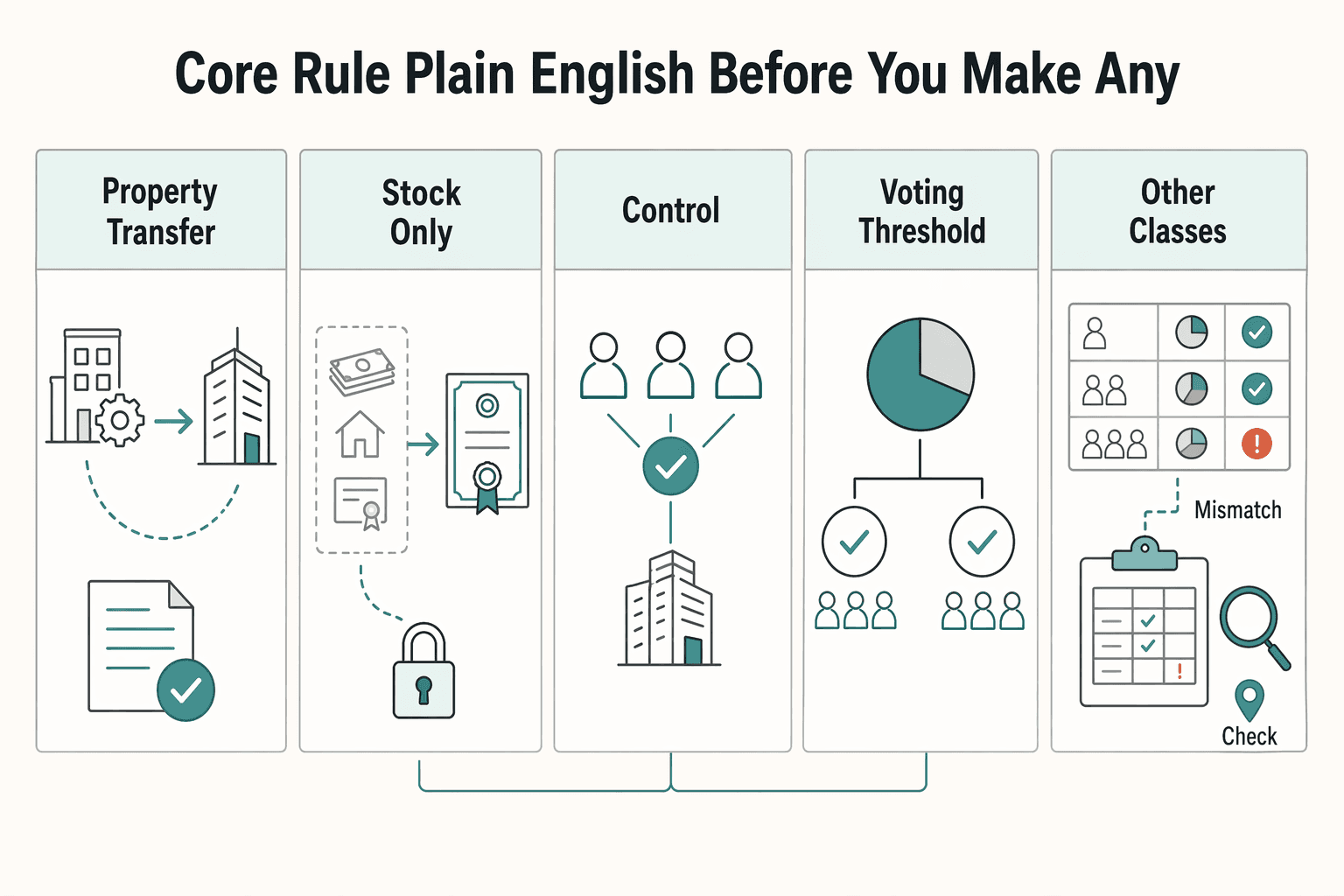

The core rule in plain English before you make any moves#

Treat Section 351(a) as a conditional nonrecognition rule, not a blanket "tax-free incorporation" label. It works only when property is transferred to a corporation solely for stock and the transferor group is in control immediately after the exchange.

| Element | Article point | Source |

|---|---|---|

| Property transfer | Property must be transferred to a corporation | Section 351(a) |

| Stock only | The exchange must be solely for stock | Section 351(a) |

| Control timing | The transferor group must be in control immediately after the exchange | Section 351(a) |

| Voting threshold | At least 80% of total combined voting power | Section 368(c) |

| Other classes threshold | At least 80% of shares of all other stock classes | Section 368(c) |

| Prearranged-step risk | A binding prearranged agreement with an outside party can affect the control analysis | 26 CFR 1.351-1(a)(1); Rev. Rul. 2003-51 |

That control test comes from Section 368(c), and it is specific: at least 80% of total combined voting power and at least 80% of shares of all other stock classes. Check the cap table class by class right after the exchange, because headline ownership can look fine while one nonvoting class misses the threshold.

"Immediately after" does not always mean literal simultaneity, but sequencing still controls the result. Steps that look acceptable in isolation can fail when read together, especially if a binding prearranged agreement with an outside party is already in place, as in the Rev. Rul. 2003-51 fact pattern that ended 40%/60%.

If your exchange includes consideration other than stock, do not assume this baseline Section 351(a) setup is still met. If investor or third-party terms are fixed in a binding prearranged agreement, treat the structure as higher risk from day one. Before closing, review the sequence against a dated, class-by-class ownership schedule for each planned step. For a related entity-choice comparison, see Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

The five eligibility gates to pass before filing incorporation documents#

Before you file, do a stop-or-go review of the documents. With Section 351, the conservative approach is simple: if a gate is not tied to authoritative text and final deal documents, pause.

IRS bulletin highlights are reader aids and "may not be relied upon as authoritative interpretations." FederalRegister.gov also states its pages are not an official legal edition and do not provide legal or judicial notice. So for Section 351(a), 351(b), 351(d), 368(c), and 351(e)(1), build your file from authoritative materials and the official printed PDF version, not summary pages alone.

| Gate | What to verify now | Evidence to keep | Stop sign |

|---|---|---|---|

| 1. Issue framing | The exact questions you need answered under Sections 351(a), 351(b), 351(d), 368(c), and 351(e)(1), based on your real transaction facts | Short issue list tied to current drafts and final signature set | You are relying on memory, old notes, or generic blog summaries |

| 2. Source authority | Each legal point is checked against authoritative text, not IRB highlights or prototype Federal Register text alone | Copy of authoritative text and the official printed PDF in the deal file | Your support file is only screenshots, summaries, or non-official excerpts |

| 3. Document consistency | The transfer, equity, and compensation documents describe the same transaction facts without internal conflict | Final draft packet: transfer docs, equity docs, compensation docs, board materials | Different documents characterize the same value in different ways |

| 4. Exception and risk log | Any potential exception or edge issue is explicitly flagged and resolved in writing before signature | Brief written memo listing open issues, decision owner, and resolution status | Team consensus is verbal only, with no written conclusion |

| 5. Final-close packet | The "right after closing" file is complete and matches what will actually be signed | Dated final packet: cap table, issuance docs, transfer schedule, timeline, approvals | Filing is moving ahead while core documents are still changing |

One common failure mode is blending documents and hoping the labels sort themselves out later. Keep a clean, dated record, and require written resolution for any open gate before filing. That is a more defensible approach if the transfer is reviewed later.

You might also find this useful: The Pros and Cons of a C-Corp for a Freelance Business. Before you sign anything, keep your incorporation timeline and residency facts aligned in one place with the Tax Residency Tracker.

Control math that determines whether Section 351 treatment survives#

Control is tested at one stated moment: immediately after the exchange. Under 26 CFR 1.351-1, Section 351(a) is a general nonrecognition rule for a transfer by one or more persons of property, solely in exchange for stock, if the corporation is controlled by the transferor immediately after the exchange.

In practice, build your control analysis from the final, signed ownership snapshot at that checkpoint, not draft models or what the parties meant to do.

| Scenario | What to verify at the immediate-after checkpoint | Documentation signal |

|---|---|---|

| Single founder, one class | Final cap table, stock issuance records, transfer documents, and approvals all show the same founder transfer and stock receipt | Stronger support when all signed documents tell one consistent story; unresolved conflicts indicate the file needs reconciliation |

| Single founder, multiple classes | The final file clearly shows which classes were issued and who holds each class immediately after the exchange | Stronger support when class issuance and ownership are documented consistently across the signed set; mismatches indicate unresolved facts |

| Founder plus another transferor in the same closing | The final packet identifies each actual property transferor and the stock each received in the same exchange | Stronger support when the transferor group and post-exchange snapshot match across signed records; mismatches indicate unresolved facts |

| Planned sequence changes before close | If issuance order or deal steps change, rebuild the immediate-after snapshot using the updated signed sequence | Stronger support when analysis is refreshed to the final signed sequence; stale pre-change ownership math can leave the record uncertain |

The checkpoint that matters most#

Anchor your process to the phrase "immediately after the exchange." You should be able to open one closing folder and get the same answer from the cap table, issuance records, transfer schedule, and approvals. If those documents do not reconcile, treat control as unproven on the current record until they do.

Single founder is simpler, not automatic#

A single-transferor structure is easier to document, but it is not self-proving. If your records include multiple classes or staged issuances, confirm the immediate-after snapshot from signed documents, not assumptions. For Section 351, a clean file is worth more than a confident narrative.

Multiple transferors increase documentation risk#

The rule expressly allows "one or more persons" transferring property, so a founder and another transferor can be part of the same exchange. The hard part is factual clarity: who actually transferred property, and what stock each transferor received immediately after. If your documents answer that differently, pause and reconcile before filing. For related tax-planning context, see A Guide to the Augusta Rule (Section 280A) for Renting Your Home to Your Business.

What counts as property and what does not under the statute#

This is where many founder deals get messy: the property-for-stock leg only works if stock is issued for property, and Section 351(d) excludes specific items from that property leg. The practical risk is mixing a valid property transfer with compensation-style terms in the same issuance.

The statutory line#

The statutory line is simple. If stock is issued for any item below, that stock is not treated as issued for property under Section 351(d):

| Item issued stock for | Treatment under Section 351(d) | Practical effect |

|---|---|---|

| Services | Excluded | Stock paid for labor does not count as stock issued for property |

| Indebtedness of the transferee corporation not evidenced by a security | Excluded | That issuance does not belong in the property-for-stock leg |

| Certain accrued interest on transferee indebtedness | Excluded | Interest-related issuance can also fall outside the property leg |

The operating rule is straightforward: if any part of a founder "contribution" is really payment for work, separate it from the property-for-stock exchange. Keep service compensation documents separate from the stock issuance documents you rely on for Section 351 treatment.

How to keep the exchange clean#

Use a share-by-share test before you sign: was this stock issued for transferred property, or for something else? If the answer is mixed, split the transaction into separate legs.

As a practical checkpoint tied to the "immediately after" sequencing concept in 26 CFR 1.351-1, keep contemporaneous transfer records so the sequence is clear. No specific format is mandated here, but clear records make it easier to reconcile transfer documents, stock issuances, and the cap table to one closing sequence.

Also watch for Section 351(b) exposure: if money or other property is received in addition to stock, gain recognition can apply. A clean file should show one clear property-for-stock leg, with service terms and any non-stock consideration documented separately.

When boot creates taxable gain even if the transfer still qualifies#

Section 351 is not all or nothing. Even when the exchange still qualifies, boot can make part of it taxable. Under Section 351(b), boot is money or other property received in the exchange in addition to stock.

| Topic | Article point | Reference |

|---|---|---|

| Stock portion | The stock portion can remain in nonrecognition treatment if the transfer otherwise fits Section 351 and control requirements are met | Section 351 |

| Cash received | Money received in addition to stock is boot and can create recognized gain | Section 351(b) |

| Other property received | Other property received in addition to stock is boot and can create recognized gain | Section 351(b) |

| Liabilities assumed | In higher-risk debt transfers under Sec. 357(b), the full assumed debt can be treated as money received, or boot | Sec. 357(b) |

| Debt-as-boot limit | In debt-as-boot cases, recognized gain is the lesser of boot received (relieved debt) or realized gain | Sec. 357(b) |

If the transfer otherwise fits Section 351 and the control requirements are still met immediately after, the stock portion can remain in nonrecognition treatment. Gain can still be recognized up to the fair market value of the boot received.

Before closing, trace every part of the consideration, not just the equity percentages:

- stock issued

- cash paid to a transferor

- non-stock property returned to a transferor

- liabilities assumed by the corporation

Liability assumptions need extra care. In higher-risk Sec. 357(b) fact patterns, such as debt transfers made to avoid tax or without a bona fide business purpose, the full assumed debt can be treated as money received, or boot. In those debt-as-boot cases, recognized gain is the lesser of boot received (relieved debt) or realized gain.

Use this as a decision checkpoint: if boot is unavoidable, model basis, fair market value, and likely recognized gain before you sign, then decide whether the timing and structure still make sense. For related context, see A Guide to Transfer Pricing for Small International Businesses.

Prearranged and multi-step deals where founders lose protection#

Once the consideration is mapped, pressure-test the sequence. The exchange becomes higher risk when a later stock move or ownership shift is already locked in before closing. If a binding third-party agreement is part of the sequence, analyze control on the integrated transaction, not on one clean-looking step.

Under 26 CFR 1.351-1(a)(1), exchanges do not have to be simultaneous. Non-simultaneous steps can still be treated as one exchange when party rights are pre-defined and execution proceeds in an orderly, expedited way. That flexibility helps legitimate closings, but it also means prearranged steps can be read together for control.

Why "immediately after" can cut both ways#

Control is tested immediately after the exchange under Section 368(c): at least 80 percent of voting power and at least 80 percent of other stock classes. Rev. Rul. 2003-51 is a practical warning that a brief moment of control may not automatically protect you when the same deal already commits a follow-on stock movement with a third party.

The ruling addresses a prearranged binding agreement context and notes court treatment where control was not satisfied in certain binding-agreement fact patterns involving loss of control to a third party. The real risk is not timing on paper alone. It is whether the precommitted sequence shows that the transferors may not retain the required control as the actual end result.

Order of operations matters more than labels#

Rev. Rul. 2003-51 lays out an ordered sequence: a first transfer, then a second transfer where W contributes Z stock to Y for Y stock, and simultaneously X contributes $30x to Y. After the second and third transfers, ownership in Y is 40 percent for W and 60 percent for X.

The practical takeaway is simple: sequence controls the analysis. A first issuance can look compliant on its own, while the coordinated set can produce a different control result.

The ruling also states that, viewed separately, each listed step qualified. That is exactly why these deals create founder risk. Isolated steps can look fine while the integrated facts change the Section 351 control conclusion.

| Checkpoint | Clean sequence | Risk sequence |

|---|---|---|

| Preclosing commitment | No prearranged binding commitment to immediate third-party stock movement as part of the exchange | Prearranged binding agreement commits a follow-on stock movement with a third party |

| Step order | Property transfer and stock receipt occur without a precommitted immediate follow-on change | Property transfer occurs, but immediate next stock movement is already precommitted |

| Simultaneous step | No simultaneous third-party contribution tied to the same step set | Third-party cash or property moves in simultaneously with the coordinated transfer steps |

| Control read | "Immediately after" control can remain with transferors under the full sequence | Integrated facts can show transferor control below the 80 percent thresholds |

What to verify before signing#

Rebuild the transaction in exact order: who transfers property first, who receives stock, and what happens immediately after each step. Then test control on the full coordinated sequence, not one interim snapshot.

If third-party funding or simultaneous transfers are pre-negotiated, pause and get written tax counsel before signing. Not every multi-step deal fails, but Rev. Rul. 2003-51 and 26 CFR 1.351-1 show that prearranged facts can change the control analysis in ways founders often miss.

Choosing your entity path before you rely on Section 351#

Start with the structure, not the tax label. If you are not transferring property to a corporation in exchange for stock, Section 351 is not the right framework to organize around. The Section 368(c) control test matters only once the corporate stock-exchange structure actually exists.

| Entity path | Is Section 351 the relevant starting point? | First check | Execution risk if you force a Section 351 path |

|---|---|---|---|

| Sole proprietorship | Usually no | Whether you need a corporation now | Unnecessary transfer and stock documentation before it is needed |

| LLC | Usually no | Whether you are staying LLC or planning a later corporate contribution | Treating LLC formation like a corporate stock exchange |

| C corporation | Yes, if property is transferred for stock | "Immediately after" control under Section 368(c) | Failing control because ownership is not preserved across voting and nonvoting classes |

Start with the end state, not the tax label#

Before you build around a corporate nonrecognition rule, confirm the transaction is actually a transfer of property to a corporation for stock. This is not "simpler is always better." It is "use Section 351 only when the transaction is actually a corporation-for-stock property transfer."

Why choosing a C corporation changes execution risk#

With a C corporation, structure and timing become decisive. Control is tested immediately after the exchange, and Section 368(c) requires at least 80% of voting power and at least 80% of all other stock classes.

That means your transfer documents, stock issuance records, and cap table must align on the same closing sequence. Do a class-by-class snapshot right after the exchange. One headline ownership percentage is not enough.

Practical solo-founder call#

If you do need the corporate route, separate property from services when you structure founder consideration, because services are not treated as property for Section 351. Also treat qualification as a binary execution issue: if the requirements are met, nonrecognition is mandatory. If they are not, the transfer can be taxable. Related reading: A Deep Dive into South Africa's Section 10(1)(o)(ii) Exemption for Foreign Employment Income.

The document pack that keeps your position defensible on review#

Your position is only as strong as the file behind it. Build around one principle: the transaction should be provable from primary records, not reconstructed later from memory or summary text.

Keep one coherent transaction record#

Treat your documents as one timeline with a clear before-state, transfer event, and after-state. Keep signed, final versions together, and make sure dates, parties, and descriptions stay consistent across the set.

A practical checkpoint is to pick one date and one transaction step, then confirm every related record tells the same story. Review issues can come from mismatched versions, late backfills, or timelines rebuilt after the fact.

Use primary authority, not summary blurbs#

Do not treat IRS bulletin highlight synopses as legal authority. The bulletin itself says those reader aids "may not be relied upon as authoritative interpretations." Use that as a filter. Rely on executed documents and authoritative tax materials, and treat summaries as navigation only.

Exclude materials that are not fit for tax support#

If a source is not tax authority, do not use it to support a tax position. For example, a U.S. Code page labeled Title 35 is patent law, and a draft database with sharing restrictions is not authoritative support.

Keep cross-border and operational records aligned#

If your facts span countries, keep transaction timing, parties, and descriptions aligned to the same chronology so your narrative stays internally consistent on review.

If you use Gruv, preserve invoice trails and ledger exports where available as supporting operational records. They can reinforce timing and activity context, but they do not replace your legal and transaction documents.

Cross-border compliance checks that sit next to Section 351#

A clean Section 351 file does not handle foreign-asset reporting for you. Treat incorporation and annual reporting as separate workstreams, then make sure both rely on the same ownership facts.

| Check | Article point | Applies to |

|---|---|---|

| Ownership facts | Lock the corporation name, issuance dates, and who owned what after closing before preparing reporting forms | Incorporation record and annual reporting |

| Form 8938 timing | Keep the applicable calendar year or tax year, the annual return it is attached to, and the transaction timing aligned; Form 8938 is filed by that return's due date, including extensions | Form 8938 |

| Record match | Signed stock and transfer records, your foreign account and asset list, and the facts used in Form 8938 and any FinCEN filing should match | Form 8938 / FinCEN filing |

| Separate filing rule | Filing Form 8938 does not remove a separate FBAR filing requirement when FBAR is otherwise required | Form 8938 / FBAR |

| Threshold variation | The IRS notes a general $50,000 trigger for some taxpayers, higher thresholds for joint filers and taxpayers residing abroad, and for certain specified domestic entities $50,000 at year-end or $75,000 at any time during the tax year | Form 8938 |

| No-return rule | If no income tax return is required for the year, Form 8938 is not required even if assets exceed the threshold | Form 8938 |

| FBAR timing check | Verify current timing when the filing year includes disruption because FinCEN can post event-specific extension notices for affected groups | FBAR |

Finalize the ownership record first#

Lock the legal facts before you prepare reporting forms: corporation name, issuance dates, and who owned what after closing. Then reconcile annual reporting to that same timeline, including whether foreign accounts or specified foreign financial assets were held personally, transferred, or newly controlled.

For Form 8938, keep three checkpoints aligned: the applicable calendar year or tax year on the form, the annual return it is attached to, and the transaction timing in your signed records. Form 8938 is attached to the annual return and filed by that return's due date, including extensions.

Use this practical check before filing:

- signed stock and transfer records

- your foreign account and asset list

- the facts used in Form 8938 and any FinCEN filing

If those do not match, fix the record first.

Form 8938 is separate from FBAR#

Form 8938 and FBAR are not interchangeable. Filing Form 8938 does not remove a separate FBAR filing requirement when FBAR is otherwise required.

For Form 8938, start with whether you are a specified person, then apply the correct threshold category. Thresholds are not uniform. The IRS notes a general $50,000 trigger for some taxpayers, higher thresholds for joint filers and taxpayers residing abroad, and for certain specified domestic entities $50,000 at year-end or $75,000 at any time during the tax year.

One narrow but important rule: if no income tax return is required for the year, Form 8938 is not required even if assets exceed the threshold.

Variation is normal, so verify before filing#

Reporting triggers differ across programs. Confirm the requirements that apply to your filing profile before filing rather than assuming your Section 351 analysis answers every compliance question.

Also avoid assuming one FBAR timing rule in every situation. FinCEN can post event-specific extension notices for affected groups, so verify current timing when your filing year includes disruption.

If you are a freelancer, do one final personal-return check. Confirm your return attachments still fit your current filing profile, including whether Form 8938 applies and whether a separate FBAR filing is required. Need the full breakdown? Read A Guide to Section 1202 Qualified Small Business Stock (QSBS).

Red flags that mean you should stop and escalate#

If any of these red flags are present, pause and get written tax review before you rely on a Section 351 position.

Control is not obvious on the actual cap table#

You should proceed only if you can prove Section 368(c) control immediately after the exchange: at least 80 percent voting power and at least 80 percent of shares of all other stock classes. If your analysis depends on assumptions, or your cap table omits a class, escalate. Use signed records to verify ownership by class.

Mixed consideration is an escalation point#

This article does not establish the detailed treatment of mixed consideration under Section 351(b) or Section 351(d). If the same closing package mixes stock with cash, other non-stock items, or possible compensation elements, stop and escalate for written tax review. Map each transfer item to what was received in return.

Prearranged steps can override your intended sequence#

Same-day steps are not automatically disqualifying, but a binding agreement can change the analysis. Under 26 CFR 1.351-1(a)(1), "immediately after" does not require literal simultaneity, and Rev. Rul. 2003-51 shows why sequencing still matters: steps that look valid on their own can be integrated, with ownership ending 40 percent / 60 percent after coordinated transfers.

If third-party commitments or follow-on stock movements were set by a pre-exchange binding agreement, treat the deal as a potential prearranged transaction and escalate.

Do not self-approve exceptions#

If you are relying on an exception, including Section 351(e)(1), do not proceed based on memory or summary-level guidance. This section does not establish the criteria for that exception. Require written professional review that states the exception considered, the facts tested, and whether it applies.

The bottom line for freelancers incorporating this year#

For freelancers, the practical win is clarity before speed. If you are planning to rely on Section 351, do not assume the tax treatment is settled from general guidance alone.

Before closing, keep one clean file that shows who is transferring what, what each party receives, and the exact order of steps, with records that do not contradict each other.

What to do next#

- Write down your ownership, transfer, and consideration terms before signing.

- Build a pre-close file before signing, not after.

- Check that your cap table, agreements, payment records, and timeline all tell the same story.

- If any part of the transaction is described differently across documents, pause and reconcile it before closing.

The guardrail to take seriously#

If the outcome depends on assumptions you cannot support in your signed records, treat that as a stop signal. Get tax and legal review before you file.

Related reading: How to Conduct a 'Functional Analysis' for Transfer Pricing. If you want compliant, traceable money movement once your structure is set, review the Merchant of Record for Freelancers.

Frequently Asked Questions

What is a Section 351 transfer in one sentence?

A section 351 transfer is a property-for-stock exchange where no gain or loss is recognized if the transferor group is in control immediately after the exchange under Section 351(a). Whether that treatment holds depends on what was transferred, what was received, and who actually controls the corporation right after the exchange.

What is the control requirement under Section 351, and when is it tested?

Control is tested under Section 368(c) immediately after the exchange. The transferor group must meet both thresholds: at least 80 percent of total combined voting power and at least 80 percent of the total number of shares of all other stock classes. Check this class by class, because a cap table can look fine at a headline level and still fail in a specific class.

Can I still use Section 351 if I receive stock plus cash or other property?

Sometimes, but not as full nonrecognition. Under Section 351(b), if you receive stock plus money or other property, gain can be recognized up to the cash plus the fair market value of the other property received, and no loss is recognized. Treat mixed consideration as a tax-impact item, not a minor drafting detail.

Do services, debt, or accrued interest count as property for a Section 351 exchange?

Not in every case. Under Section 351(d), stock issued for services, certain indebtedness of the transferee, and certain accrued interest is not treated as issued for property. If your deal mixes property with those items, separate and document them clearly before relying on Section 351 treatment.

Are multi-step transactions valid if documents were prearranged before closing?

They can be, but prearranged steps are a common failure point. Even though "immediately after" does not always require literal simultaneity, a binding agreement can cause the Section 351 control requirement to fail. Review the full deal package to confirm control is not effectively handed off as part of one coordinated transaction.

What is the fastest checklist to decide whether I should proceed or call a tax pro?

Use this quick screen: you are transferring qualifying property, not Section 351(d)-excluded items, you are receiving stock with any non-stock consideration identified, the transferor group meets both 80 percent control tests immediately after the exchange, and no binding prearranged step changes post-exchange control. If any point is unclear, assumption-driven, or disputed in your documents, pause and get written tax advice before closing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- federalregister.gov/documents/2000/11/15/00-28950/stock-transfer...trusted

- federalregister.gov/documents/2020/03/31/2020-04799/facilitating...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/pub/irs-drop/rr-03-51.pdftrusted

- irs.gov/pub/irs-pdf/i8938.pdftrusted

- answerconnect.cch.com/document/arp10021b2acc7c5610009becd8d385ad16...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The Pros and Cons of a C-Corp for a Freelance Business

Entity choice is not just paperwork. It changes how the business is taxed, how ownership can be structured, and how much compliance work you take on. Use this article to make a practical call: keep your current setup, consider an LLC or S-corp path, or move to a C-corp only if the tradeoffs fit where you are headed.