Quick Answer

Freelancers file Schedule C defensibly by reporting sole-proprietor income and only ordinary, necessary business expenses, with every number traceable to records you control. Keep income support, separate business and personal spending, reconcile your books, document vehicle and home-office claims properly, and route owner-level items like retirement and self-employed health insurance to Schedule 1 when required.

The CEO's Playbook for Schedule C: A Strategic Guide for the Business-of-One#

Use Schedule C as the operating report for your solo business. It reports business income, expenses, and your net profit or loss. If you are a sole proprietor, this is usually the form that determines it. If you are a single-member LLC that has not elected corporate tax treatment, it is generally treated as a disregarded entity for income tax, and Schedule C is often used to report that business income and expenses.

That net figure affects income tax. When your total net self-employment earnings are $400 or more, it also drives Schedule SE for Social Security and Medicare tax.

Read Schedule C as a decision flow, not just a set of boxes. Part I covers income. Parts II, III, and V cover deductible costs, and Part IV captures required vehicle details when car and truck expenses are claimed. One boundary matters from the start: sporadic activity, hobbies, and not-for-profit activity do not qualify as a business for Schedule C treatment.

| Part | What you report | Why it matters | Common error to avoid | Records to keep |

|---|---|---|---|---|

| Part I | Gross receipts or sales, returns/allowances, and cost of goods sold from line 42 (if applicable) | Sets gross income before expenses | Reporting nonbusiness activity here, or failing to keep clear income records | Invoices, payment processor reports, bank deposits, client statements |

| Part II | Business expenses unrelated to qualified business use of the home | Directly reduces taxable profit | Mixing personal spending into business categories, or misplacing home-use costs | Receipts, canceled checks, account statements, bookkeeping reports |

| Part III | Cost of goods sold and inventory details, including closing inventory method | Applies when inventory-related costs are part of your business | Completing it without inventory-related costs, or skipping inventory valuation method fields | Inventory records, purchase records, supplier invoices, valuation method notes |

| Part IV | Vehicle-use details if you claim car and truck expenses | Supports a deduction the IRS asks you to substantiate | Claiming vehicle costs without mileage or use support, or not attaching extra vehicle details when required | Mileage log, trip-purpose notes, repair and fuel records, vehicle summary |

| Part V | Other ordinary and necessary expenses not deducted elsewhere | Captures valid costs not listed in earlier lines; total feeds to line 27b in current instructions | Using Part V as a catch-all for unclear items, or relying on outdated line mapping | Itemized expense list, receipts, vendor bills, category notes |

Use these scope checks before you file. Part I matters unless there was truly no profit or loss for the full year, in which case a Schedule C may not be necessary. Part III matters only when cost of goods sold or inventory applies. Part IV applies only if you claim car and truck expenses. If you used more than one vehicle, attach the additional statement the instructions require. Part V should stay specific, and anything that clearly belongs on another line should go there first.

Verification checkpoint: does your final net figure match the business story your records support? If total net self-employment earnings are $400 or more, use Schedule SE to compute self-employment tax. If you cannot trace each number to records, stop and fix that before filing.

Before you go deeper into systems and deductions, get three basics in place:

- Income records: invoices, platform reports, and bank deposit support

- Expense categories: a cleaned list separating business costs from personal spending

- Documentation habits: receipts, canceled checks, and notes that support each deduction

If you want help building routines around the admin side, you might also find this useful: The Freelancer Year-End Tax Prep Checklist.

Why Your Business Systems are Your Best Audit Defense#

The practical audit defense is simple: every Schedule C number should trace back to a record you control. Good systems will not prevent every IRS question, but they can make your return easier to support, explain, and correct.

That matters in practice. The National Taxpayer Advocate's 2025 report identified ten serious taxpayer problems in FY 2025, including delays and inadequate responses to taxpayer records requests. It also flagged severe compliance burdens for U.S. taxpayers living abroad. If records are hard to retrieve, your own documentation often becomes the file that carries the return.

| Area | Weak system | Stronger documentation system |

|---|---|---|

| Commingled funds | Business and personal activity run through the same accounts with no clear boundaries | Business activity is tracked separately where practical, with owner transfers labeled consistently |

| Uncategorized transactions | You defer categorization until year-end and rely on memory | You categorize transactions on a regular cadence and keep uncategorized items low |

| Missing documentation | Receipts and invoices are scattered across inboxes, chats, and apps | Key expenses have supporting receipts or invoices stored in one place, with a short business-purpose note when useful |

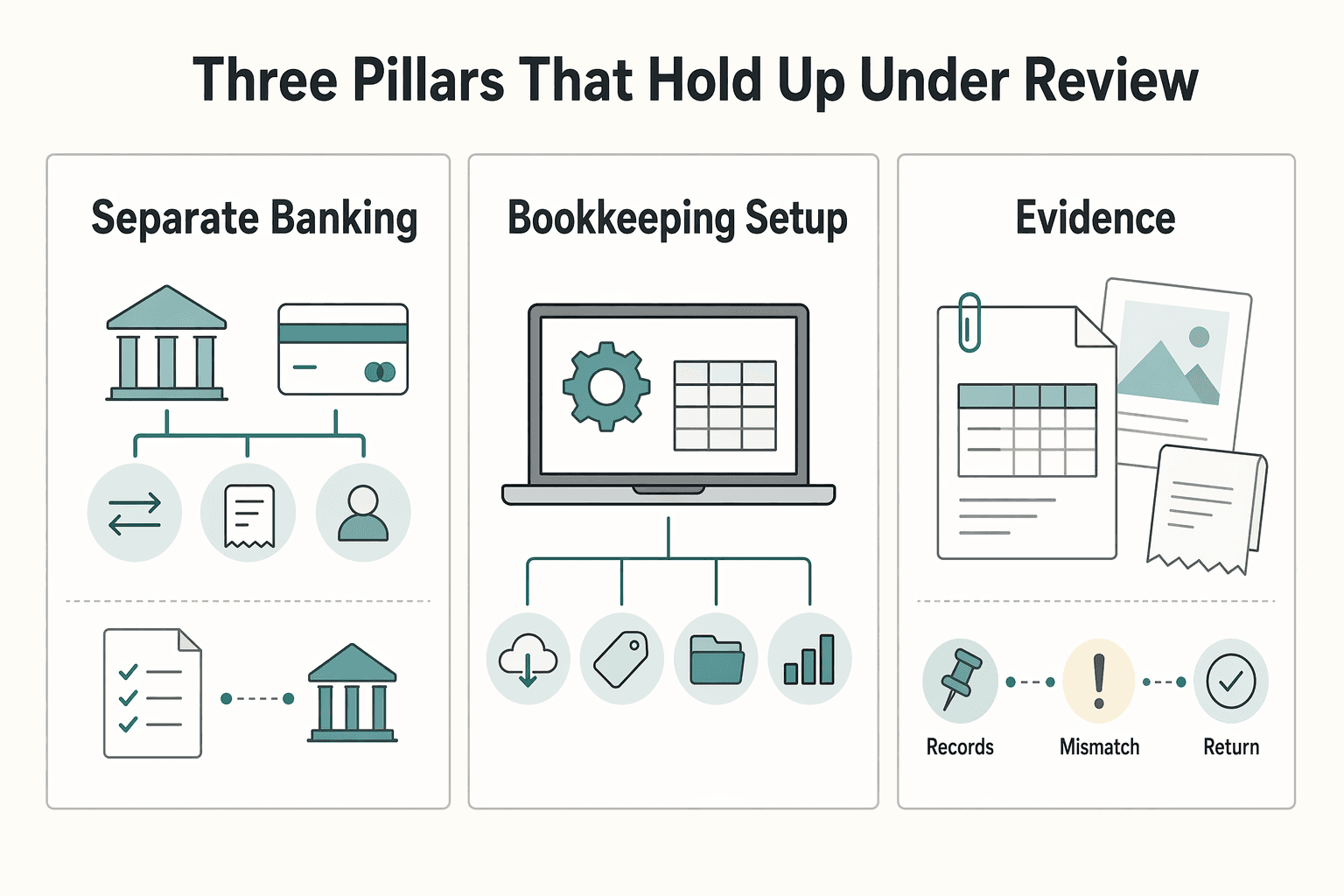

Three pillars that hold up under review#

1) Separate banking. Where practical, route client income and business spending through a dedicated account or card. Review transactions regularly and label transfers, reimbursements, and owner draws the same way each time. The result is a cleaner statement trail that ties to your books.

| Pillar | Core action | Outcome |

|---|---|---|

| Separate banking | Route client income and business spending through a dedicated account or card where practical, and label transfers, reimbursements, and owner draws the same way each time | A cleaner statement trail that ties to your books |

| Bookkeeping setup | Use a system you will maintain consistently, such as QuickBooks, Xero, Wave, Zoho Books, or a disciplined spreadsheet process; reconcile books to bank activity and clear uncategorized items on a regular schedule | Current books you can explain line by line |

| Receipt workflow | Capture receipts and invoices when the expense happens, store them in one place, and add a brief note when the business purpose is not obvious from the vendor name alone | Documentation that still makes sense months later |

2) Bookkeeping setup. Use any system you will actually maintain consistently, whether that is software like QuickBooks, Xero, Wave, or Zoho Books, or a disciplined spreadsheet process. Helpful features can include imports, consistent categorization rules, document storage, and exportable profit and loss reporting.

Reconcile your books to bank activity on a regular schedule and clear uncategorized items. By filing time, you want a current set of books you can explain line by line.

3) Receipt workflow. Capture receipts and invoices when the expense happens and store them in one place. Add a brief note when the business purpose is not obvious from the vendor name alone. Months later, that is what turns a pile of transactions into documentation that still makes sense.

If you have unresolved prior-year gaps, a large uncategorized backlog, or complex changes in how you track income, expenses, or inventory, consider bringing in a tax professional before filing. Once the records are clean, the next question is classification: what belongs on Schedule C, what belongs somewhere else, and what should not be claimed at all.

For a related issue, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

The Strategic Deduction Matrix: Moving Beyond "Office Supplies"#

Clean books are only half the job. A well-documented expense can still create problems if it goes on the wrong form, includes a personal portion, or lacks records that support what you reported.

Use this three-tier check before you file: decide whether a cost belongs on Schedule C as a current operating cost, on Schedule 1 as an owner-level deduction, or nowhere on the return. Keep the IRS anchor constant: deductible business expenses must be both ordinary, meaning common and accepted in your field, and necessary, meaning helpful and appropriate for your business.

| Tier | Purpose of spend | Where it is typically reported | Audit-sensitive documentation | Common misclassification risk |

|---|---|---|---|---|

| Operational costs | Keep the business running now | Schedule C current operating costs | Records that support what was reported, including the amount paid and business purpose | Claiming mixed-use items at 100%, such as deducting more than the business-use share of vehicle-related interest |

| Growth investments | Support current delivery or revenue activity | Often Schedule C when directly tied to operating the business and meeting ordinary-and-necessary standards | Records that support the expense and its direct tie to current business operations | Treating loosely related or personal-improvement spending as a business cost |

| Wealth and wellness items | Owner-level protection or long-term savings | Often Schedule 1, not Schedule C, when allowed | Insurance premium records, policy details, retirement contribution records, and required calculation forms | Booking owner retirement contributions or self-employed health insurance as standard Schedule C expenses |

Tier 1 and Tier 2 boundaries#

Start with a practical rule: if you cannot clearly explain the business purpose, do not claim it yet. Schedule C is for current operating costs, including technology and software that are ordinary, necessary, and directly related to running your business.

Mixed-use costs need stricter treatment. For mixed-use vehicle-related interest, only the business-use portion is deductible on Schedule C, and your allocation needs records that support what you reported.

Growth spending follows the same standard. Software and technology tools can qualify when they are ordinary, necessary, and directly related to operating your business. Costs without a clear connection to current business activity should be treated cautiously.

Tier 3 is usually not a Schedule C line#

Retirement and self-employed health insurance can be deductible, but that does not make them Schedule C expenses. For self-employed owners, retirement plan deductions are taken on Schedule 1, not Schedule C. If they were deducted on Schedule C, correction requires an amended return.

| Item | Typical treatment | Key note |

|---|---|---|

| Retirement plan deductions | Schedule 1, not Schedule C | If they were deducted on Schedule C, correction requires an amended return |

| Self-employed health insurance | Use Form 7206 to determine the deduction and report it on Schedule 1, line 17 | Policy may be in either the business or individual name, and eligibility can be rule-dependent |

| General wellness or gym spending | Do not treat as automatically deductible | Keep separate from the Form 7206 path unless current verified rules clearly support treatment |

Self-employed health insurance also follows an above-the-line path. Use Form 7206 to determine the deduction and report it on Schedule 1, line 17. Policy titling by itself does not settle treatment, because the policy may be in either the business or individual name. Eligibility can be rule-dependent, so verify current instructions before filing.

Do not treat general wellness or gym spending as automatically deductible just because you are self-employed. Keep those separate from the specific Form 7206 path unless current verified rules clearly support treatment, and run each gray-area item through this check before filing:

- Business purpose test: Can you show the cost is ordinary and necessary for the business, not mainly personal?

- Documentation test: Do your records support what you reported, including what was paid and the business purpose?

- Escalation point: If classification is unclear between Schedule C, Schedule 1, or non-deductible personal spending, pause and confirm with a tax professional before filing.

For a step-by-step walkthrough, see Top 10 Tax Deductions for Freelancers. Before you lock in vehicle write-offs, sanity-check your records and method with the mileage deduction calculator.

The Global Professional's Schedule C: Navigating International Complexity#

Once money, travel, or vendors cross borders, consistency matters even more. Keep Schedule C tight: report sole-proprietor business income or loss on your individual return, and keep records you can reconcile.

Convert foreign income with one consistent workflow#

For foreign-currency income, the excerpts here do not specify one required conversion source or method. In practice, the standard is consistency plus traceable records.

- Pick one rate source you can document and retrieve later.

- Apply it the same way for similar transactions across the year.

- Keep a record of the rate you used, whether per transaction or by documented batch.

- Tie each converted USD amount to the invoice, payment record, and bookkeeping entry.

- If your source or method changes midyear, record the reason and effective date.

What is clear on cross-border costs, and what needs escalation#

Use this quick filter before you post expenses to Schedule C.

| Item type | What the excerpts here support | Common risk | Documentation to keep |

|---|---|---|---|

| Travel and meals | Travel and deductible meals are separate Schedule C Part II entries | Blending personal portions into business totals | Itinerary, receipts, payment trail, and business-purpose notes |

| Business use of home | Report on line 30 only; do not report elsewhere on Schedule C. Form 8829 is required unless using the simplified method | Duplicating home-office amounts in other expense lines | Home-office calculation records and Form 8829 support, if used |

| Payments to vendors or contractors, including cross-border | Schedule C includes a checkpoint asking whether payments required Form 1099 filing | Missing the 1099 checkpoint or weak payment documentation | Contract or invoice, payment record, and vendor details |

| Other cross-border charges such as bank fees, platform fees, relocation costs, or mixed-use items | No special cross-border deduction category is defined in these excerpts | Treating "international" as automatically deductible | Keep records, separate personal portions, and escalate unclear items |

Keep a review-ready travel file#

The excerpts here identify travel and deductible meals as expense lines, but they do not prescribe a travel-log format. If you claim international business travel, keep a file that makes the business purpose and allocations easy to follow.

- Write a one-sentence business purpose for the trip.

- Keep an itinerary that connects travel dates to business activity.

- Save supporting business records such as client emails, meeting notes, contracts, and event registrations.

- Maintain a dated activity log while traveling.

- Split out personal days, family costs, and upgrades before totals hit Schedule C.

Know where Schedule C stops#

Schedule C reports sole-proprietor profit or loss. If it shows a profit, it carries to Schedule 1 line 3 and Schedule SE line 2. If it shows a loss, continue through line 32 as directed on the form. Partnerships generally file Form 1065, not Schedule C.

The excerpts here do not address separate foreign account reporting or international information-return rules. If structure, account reporting, or cross-border classification gets mixed or unclear, that is the point to bring in a professional. For related background, see How to Choose the Right Business Structure for Your Freelance Business.

The CEO's Pre-Flight Check: Audit-Proofing Your Filing#

Before you submit, review the return like a skeptical reviewer. Your income, deductions, and business story should all line up with how you actually operated. The goal is not smaller-looking numbers. It is a return you can explain without backtracking.

This matters even more if you work across borders. The National Taxpayer Advocate identified 10 major taxpayer problems in FY 2025, including records-access delays, and separately identified severe compliance burdens for taxpayers living abroad. Do not assume you can pull missing support together at the last minute.

Run the consistency check first#

- Reconcile income end to end. Tie gross receipts to bookkeeping, 1099 summaries, invoices, and platform exports. If you converted foreign income to USD, confirm the same conversion workflow shows up in your final totals.

- Check expense reasonableness against your real business model. Compare major categories such as travel, meals, contract labor, software, vehicle, and home office to your service model, client mix, and delivery pattern.

- Write a plain-language rationale for outliers. For each unusually large category, add a short note explaining what it covered, which work it supported, and why it was business-related in your context.

Check documentation-sensitive categories before filing#

| Potential review point | What you should have ready | How to explain it consistently |

|---|---|---|

| Round-number entries | Invoices, receipts, bank or card records, and reports showing exact totals | "This total is from reconciled booked transactions, not estimates." |

| Vehicle or home-office claims | Mileage log, trip-purpose notes, parking and toll support, and home-office calculation records, including Form 8829 support if used | "This reflects documented business use tied to actual trips or a defined business workspace." |

| Recurring losses | Year-by-year profit and loss statements, contract or invoice history, pipeline evidence, and notes on unusual periods | "The loss reflects documented business conditions or business investment, not personal spending." |

Do not treat these items as automatic audit triggers. If a current-year cap, substantiation limit, or trigger point applies, verify it in current IRS instructions before filing.

Build your audit-defense file before you submit#

Before you submit, build one clearly labeled folder for the tax year and include:

| File item | When noted |

|---|---|

| Final profit and loss statement | Before you submit |

| 1099 summary with income reconciliation | Before you submit |

| Invoice register and payment-platform exports | Before you submit |

| Bank and card statements supporting booked expenses | Before you submit |

| Receipts for large, unusual, or mixed-use items | Before you submit |

| Mileage log and trip-purpose notes | If relevant |

| Travel file with itinerary, business-purpose note, and activity log | If relevant |

| Home-office support and Form 8829 file | If relevant |

| Return narrative memo that explains items a reviewer could question | Before you submit |

Final reviewer check: if your accountant, reviewer, or future you cannot trace each number without guessing, fix the file before filing. If you are also reviewing owner-level deductions, we covered a related issue in detail in A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

Conclusion: From Compliance to Command#

Use Schedule C as a defensibility check, not a memory exercise. You are reporting income or loss from your sole-proprietor business, so the return should be traceable, explainable, and supported by records.

Keep the system simple and consistent: separate business activity from personal spending, capture records as transactions happen, and categorize deductions the same way all year. Before filing, confirm your activity still meets the business standard, and keep business-use-of-home expenses isolated to line 30. Use this readiness check before you file:

- Confirm records: Reconcile return numbers to statements, invoices, and receipts.

- Confirm categorization: Verify categories match your books, confirm home-office entries are only on line 30, and answer the Schedule C Form(s) 1099 payment question for the form year shown.

- Confirm support file: Keep one support set with receipts, invoices, payment records, contracts, and business-purpose notes.

- File or escalate: If line 31 shows profit, confirm flow to Schedule 1, line 3 and Schedule SE, line 2. If line 31 shows loss, go to line 32 and verify next-step handling before you file.

Bring in a professional when the facts are not clean. That includes complex facts, including cross-border situations, recurring losses or uncertainty after line 32 is triggered, or deductions you cannot clearly support. If you are not clearly filing as a sole proprietor, or the business qualification itself is unclear, get help before filing. That is how you stay in control: defensible filing and lower compliance stress.

This pairs well with our guide on Canada GST/HST for Freelancers Who Want Fewer Filing Surprises.

If your work and travel pattern changes during the year, keep a running evidence trail with the tax residency tracker.

Frequently Asked Questions

What is the difference between a Form 1099 and Schedule C?

Schedule C reports income or loss from a sole proprietorship business or profession. It also asks whether payments in the form year required Form(s) 1099 and whether those forms were or will be filed. Schedule C line 31 profit flows to Schedule 1, line 3, and Schedule SE, line 2.

What are the biggest audit red flags on a Schedule C?

This article does not give one official IRS list of biggest Schedule C red flags. The practical standard is traceability and line-level accuracy, including correct routing for home-office amounts on line 30, profit on line 31, and loss handling on line 32. Reconcile totals to records before filing, and get professional help if you cannot clearly support a number.

Do I need a separate business bank account to file Schedule C?

No. These excerpts do not say a sole proprietor must have a separate business bank account to file Schedule C. But separate banking where practical creates a cleaner statement trail and makes it easier to tie totals to books and records.

How do I deduct health insurance premiums?

Self-employed health insurance is discussed here as an above-the-line deduction, not a standard Schedule C expense. Use Form 7206 to determine the deduction and report it on Schedule 1, line 17. If placement is still unclear, verify the current instructions before filing and talk to a tax professional.

How do I report income from a foreign client?

Report sole-proprietor business income from a foreign client on Schedule C. If you were paid in foreign currency, use one documented and consistent conversion workflow and keep records that tie the USD amount to the invoice and payment record. Get professional help if the treatment is unclear.

Do I always have to file Schedule C if I freelanced during the year?

No. If your sole proprietorship had no profit or loss for the full year, filing Schedule C is not necessary. But if your net self-employment earnings from all businesses are $400 or more, use Schedule SE. Check both conditions before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Choose the Right Business Structure for Your Freelance Business

Most freelancers end up in a business structure by default rather than by design, but that accidental choice shapes taxes, personal liability, and payment operations in ways that compound over time. This guide walks independent professionals through four entity types — Sole Proprietorship, Single-Member LLC, S-Corp election, and Corporation — covering the tax treatment, liability exposure, and operational overhead of each. Rather than prescribing a single best answer, it provides a trigger-based framework: start with the structure that fits today, then upgrade when specific signals — indemnification clauses, enterprise KYB requirements, a first hire, or material net profit — make the switch worthwhile. The result is a deliberate, revisable foundation that keeps records clean, reduces onboarding friction, and avoids the expensive mismatches that come from letting structure lag behind business growth.

The Freelancer's Year-End Tax Prep Checklist (US Expat Edition)

Your year-end target is filing readiness. By December 31, you want a complete file for your U.S. federal return, not a last-minute chase for documents. For a globally mobile freelancer, the hard part is usually proving what happened, choosing the likely FEIE or FTC lane, and spotting the facts that need professional review.