Quick Answer

Yes. A remote seller can owe state sales tax even without a local office, so run a state-by-state check before assuming you are out of scope. Start with physical presence, then test the state threshold, then verify what counts in the base. New York references more than $500,000 and more than 100 sales over four quarters, while Texas uses a $500,000 twelve-month test with a fourth-month permit deadline after exceedance. If records are messy, escalate early and document the rule source you relied on.

After Wayfair, no-office is not enough: presence checks, state thresholds, and what to verify before registering#

Yes, you can trigger sales and use tax obligations in states where you have no office, warehouse, or local staff. It pays to verify early and keep clean records as you grow. One operational risk is letting your records drift out of sync. If that happens, you may not be able to show when nexus started, which sales counted, and when registration should have happened.

The rule changed on June 21, 2018, when the Wayfair decision removed the physical presence barrier for state collection responsibilities. States can impose collection duties based on economic presence even without a local footprint, so "no local office" is not a reliable reason to ignore state rules.

This guide gives you a practical monthly sequence:

- Check in-state presence first.

- Test threshold-based nexus under that state's rules.

- Confirm what the state counts before you register.

- Track state sales and dates so you are not rebuilding history later.

A quick New York vs. Texas contrast shows why this has to be state by state. New York says a business with no physical presence that meets its test must register as a vendor. Its published test references more than $500,000 and more than 100 sales over the immediately preceding four sales tax quarters. Texas uses a different structure. Remote sellers below $500,000 in Texas revenue in the preceding twelve calendar months are not required to obtain a permit or collect or remit use tax. Once that amount is exceeded, the permit deadline is the first day of the fourth month after the month of exceedance.

If your records are incomplete or the facts are ambiguous, escalate early instead of improvising. Weak preparation raises risk and can increase unexpected tax cost. This guide is practical operational help, not legal advice. State law and agency guidance control final obligations, and unclear cases should be reviewed with a qualified advisor.

Start With the Terms That Drive Your Filing Duties#

Start with these four terms. They determine whether a state stays on your watchlist or moves into registration and collection.

- Sales tax nexus: your business has enough connection with a state that it can require you to collect and remit sales tax.

- Economic nexus: that connection is created by crossing a state threshold, based on sales dollars, transaction count, or both.

- Physical presence: in-state footprint or activity that can create nexus, including property, workers, or goods stored in a warehouse or fulfillment center.

- Remote seller: a seller delivering into a state where it has no physical presence.

The main operating rule is simple. Sales tax duties can begin through either path: an in-state footprint or threshold activity. Treat them as separate checks so you do not miss the filing start date.

Why the baseline changed after Wayfair#

The baseline changed in 2018. The Wayfair ruling is commonly summarized as adding economic nexus, where sales or transaction thresholds can trigger collection duties even without local activity. That is why "we are fully remote" is not enough to close your nexus analysis.

What this means in practice#

Threshold-based nexus is state-specific, not nationwide. Some states use a sales dollar threshold, some use a transaction count threshold, and some use both. The Wolters Kluwer chart includes patterns like $100,000 in sales or 200 transactions, and notes that Connecticut and New York require both thresholds.

Use any threshold chart as a starting point, not your final answer. The chart referenced here was compiled as of October 7, 2025 and says it is general guidance, not legal advice. Your final check should always be current state rules and agency guidance.

Use a Three-Trigger Test Before You Register in Any State#

Run this sequence in order every time: physical presence first, economic nexus method second, counting rules third. If Trigger 1 is yes, move that state from watchlist to active sales and use tax review.

| Trigger | Check | Example |

|---|---|---|

| Physical presence | Review in-state footprint or activity before revenue thresholds | Sellers with physical presence are generally required to register regardless of sales volume |

| Threshold method | If there is no local footprint, test the state's current economic nexus method | Virginia: more than $100,000 annual gross retail sales or 200 or more transactions |

| Counting rules | Confirm what the state counts toward the threshold before acting | Washington: include facilitated sales and exempt sales; remote seller registration applies from Jan. 1, 2020 when combined gross receipts sourced or attributed to Washington are more than $100,000 |

Trigger 1 starts with physical presence#

Start here, not with revenue thresholds. Streamlined guidance indicates sellers with physical presence are generally required to register regardless of sales volume, so this check comes first.

For remote sellers, being small or having only limited sales there does not usually change that first decision. If your facts suggest in-state activity, treat the state as active and confirm timing on the state revenue page.

Use one gating question before reviewing sales totals: "Do we have presence facts here?" If the answer is unclear, do not assume it is no.

Trigger 2 is the state's current threshold method#

If you truly have no local footprint, test economic nexus under that state's current method. States do not use one universal logic. Many use sales OR transactions, while some use sales AND transactions.

That difference can change the result. Virginia, for example, applies threshold-based nexus at more than $100,000 annual gross retail sales or 200 or more transactions. South Dakota's Wayfair-era rule used more than $100,000 or 200 transactions. Use these as examples only, not as templates for other states.

Trigger 3 is what the state actually counts#

Before you act, confirm what counts toward the threshold. States may use gross sales, gross revenue, retail sales, or taxable sales, and many do not exclude non-taxable sales from threshold testing.

Also verify marketplace treatment. Washington shows why this matters: its guidance says to include facilitated sales and exempt sales in threshold calculations, and notes remote seller registration applies from Jan. 1, 2020 when combined gross receipts sourced or attributed to Washington are more than $100,000.

For this step, use two sources together: the official state revenue page and Streamlined's Remote Seller State Guidance. Save what you relied on, when you checked it, and the matching sales report.

If your data is messy, decide early#

If your totals are incomplete, marketplace splits are unclear, or sales are rising, register early instead of betting on ambiguity. Streamlined states you may choose to register when you know you will be making sales into a state, which can be a lower-risk move when records lag reality. Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

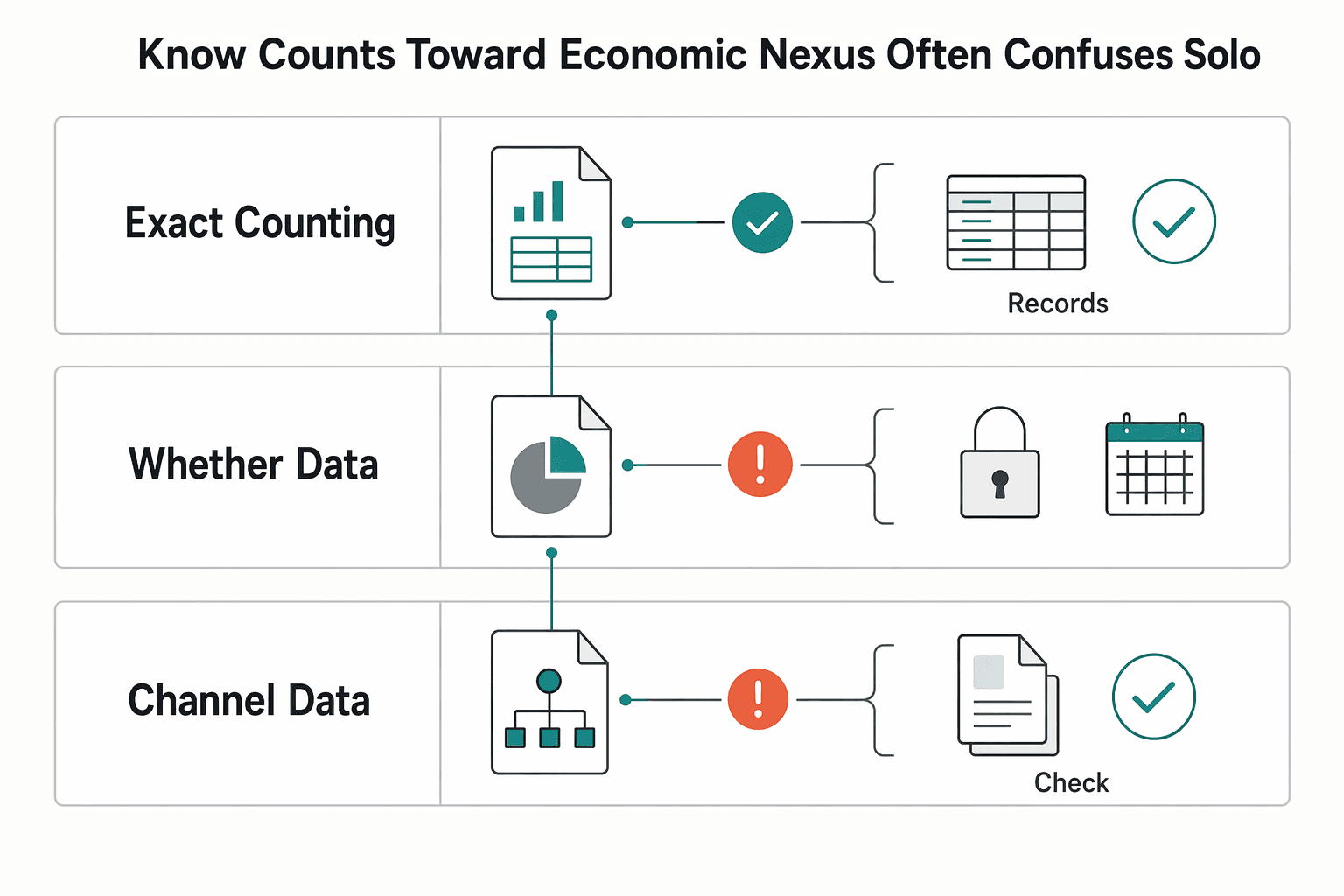

Know What Counts Toward Economic Nexus and What Often Confuses Solo Operators#

Do not use this section by itself to decide what counts. One source is inaccessible, and another is an SEC Form S-1/A page rather than sales tax nexus guidance.

Treat this as a verification stop, not a decision point. Before you register, wait, or make a nexus decision for any state, confirm the exact counting rule from current state tax guidance and match it to the way your records are actually structured.

| What to verify | What to pull from your records | What to save as proof |

|---|---|---|

| Exact counting rule text used for your decision | State-sourced totals for the same review period | Dated copy of the state page you relied on |

| Whether your data matches the rule's required counting basis | Raw exports behind your rollup, not just summary totals | Short note showing how each total was calculated |

| How channel data is handled in your review | Separate direct and platform-originated sales data by destination | Saved channel exports and your reconciliation notes |

If you only track invoiced revenue rather than state-sourced totals by channel, you may not have decision-ready nexus data yet. Rebuild the totals first, then apply rule text you can reproduce.

Physical Presence Can Override Threshold Comfort#

Threshold math can give false comfort when an in-state footprint is in play — treat it as a review trigger, not an automatic registration rule. Physical location has long been treated as a tax-jurisdiction touchstone; verify current state guidance before you act.

If your work includes in-state activity, do not rely on thresholds alone. Review local activity first, then test thresholds only if that review does not already change your posture.

One-off activity vs ongoing footprint#

Do not auto-classify a one-off in-state activity or an ongoing in-state footprint from this evidence alone. Use this operating rule:

| Scenario | Practical move |

|---|---|

| One-off in-state activity | Do a state-specific nexus check before assuming threshold comfort still applies. |

| Ongoing or repeated in-state activity | Escalate sooner and document your state-specific review before relying on threshold-only logic. |

If activity is planned this quarter, decide timing before it starts#

If in-state activity is planned this quarter, review registration timing before it starts, not after delivery or month-end close. Use this pre-activity checkpoint:

| What to verify | What to pull | What to save |

|---|---|---|

| Whether planned in-state activity changes nexus posture | Contract/SOW, calendar/travel details, service location | Dated copy of the state guidance you used |

| First in-state activity date | Confirmations, work logs, expense records | Short memo with your timing decision and rationale |

| Whether threshold analysis still applies after presence review | State-sourced totals for the same period | Reconciliation showing presence review happened first |

A practical risk is delay and later reconstruction. Early documentation is much easier than rebuilding dates, facts, and decisions later.

North Carolina Example You Can Copy for State-by-State Checks#

Use North Carolina as a repeatable pattern: start with NCDOR guidance, then verify the definitions referenced in N.C. Gen. Stat. § 105-164.3 before relying on any summary chart.

A remote sale is an item ordered by mail, phone, internet, app, or similar method when the order is received outside North Carolina and the item is delivered to or made accessible in North Carolina. This framework also covers services sourced to North Carolina. A remote seller is a seller without physical presence in North Carolina and without another legal requirement to register, but with sales sourced to the state.

If you already have an in-state footprint or another legal collection requirement, treat that as a separate trigger. NCDOR states that a retailer with physical presence in the state or another legal requirement to collect tax must collect tax on remote sales.

Use the statute section as your checkpoint#

For this state, treat N.C. Gen. Stat. § 105-164.3 as your definition checkpoint, not optional background. NCDOR ties its remote sale guidance directly to that section.

Also document what you relied on. The North Carolina General Statutes page says its website text is not official and includes changes through SL 2025-97, so save the NCDOR page and your review date in your workpapers.

Keep marketplace and direct sales in one North Carolina view#

For threshold testing, combine channels in one total. NCDOR says collection is required when gross sales sourced to North Carolina are in excess of $100,000 in the previous or current calendar year, including marketplace activity.

| Sales channel | Count in NC threshold test? | Practical check |

|---|---|---|

| Direct sales | Yes | Include gross sales sourced to North Carolina |

| Sales as a marketplace seller | Yes | Include, then review NCDOR's marketplace page for marketplace-specific guidance |

| Marketplace-facilitated sales | Yes | Include even when a platform is involved |

If you only track direct invoices, you can undercount your North Carolina exposure.

If tax was not collected, do not end the review there#

If sales tax was not collected, keep going. NCDOR directs purchasers to review consumer use tax obligations when a seller does not collect North Carolina sales and use tax.

Then check whether those sales should have been included in your North Carolina threshold count and whether your North Carolina collection posture needs to change. Keep a dated record of the transaction facts and the NCDOR guidance you used so any correction decision is traceable.

For related context, see A Guide to Provincial Sales Tax (PST) for Canadian Freelancers.

Marketplace Sales Change the Math Faster Than Most Freelancers Expect#

Marketplace collection may reduce what you collect directly, but it does not mean your state exposure is fully handled. Separate the roles first. A Marketplace facilitator may collect on marketplace sales, while you as the Marketplace seller still need a clear view of threshold exposure and any remaining sales and use tax responsibilities.

| Role or entity | Treatment | Operational note |

|---|---|---|

| Marketplace facilitator | In California, is generally responsible for collecting, reporting, and paying tax on retail sales made through its marketplace for California delivery | Beginning October 1, 2019 |

| Marketplace seller | Still needs a clear view of threshold exposure and any remaining sales and use tax responsibilities | Keep separate channel logs but maintain one state-level nexus view |

| Delivery network company | Not a marketplace facilitator unless it elects to be one | Confirm status before treating those sales as fully handled |

California shows this clearly. Under the Marketplace Facilitator Act, a marketplace facilitator is generally responsible for collecting, reporting, and paying tax on retail sales made through its marketplace for California delivery beginning October 1, 2019. California also states these rules affect registration, collection, and payment responsibilities, and points to Revenue and Taxation Code sections 6041-6041.6 for core definitions. Use that as your verification checkpoint when a platform summary sounds broader than the statute.

A common place teams slip is channel accounting, not theory. When direct and marketplace channels are tracked separately but never reconciled, state totals can drift and your nexus view can become unreliable.

If you sell both ways, keep separate channel logs but maintain one state-level nexus view. Reconcile monthly by state with:

- direct sales by destination state

- marketplace sales by destination state

- a note on whether the marketplace collected tax for those orders

Keep the monthly marketplace settlement report and your state-sourced sales export together so your counting method is traceable.

One more check: not every platform-adjacent service is automatically a marketplace facilitator. In California, a delivery network company is not a marketplace facilitator unless it elects to be one, so confirm status before treating those sales as fully handled.

For a related walkthrough, see A Deep Dive into the US-Mexico Tax Treaty for Remote Workers.

Remote Team Members Can Create Nexus Even When Sales Stay Low#

A remote team member can raise nexus risk before you hit a state threshold, so check in-state presence first and sales thresholds second.

That order keeps the review practical. Historical nexus analysis described physical presence as the typical connection point, and current remote-work guidance warns that even one remote employee in another state can create tax obligations there. If someone works from State B, start by assessing whether that work location creates in-state concerns. Then evaluate your threshold exposure.

Use payroll and registration signals as an early warning, not just sales dashboards. Remote-work guidance says withholding generally follows the state where the employee works, and that employers may need state registration and withholding setup there. If you already opened payroll withholding in a state, treat that as a strong prompt to review broader state tax exposure immediately.

The common failure mode is delay: low sales can look like safety while a person is already working in-state. That can lead to back taxes and fines tied to missed withholding.

Keep a small evidence file for each out-of-state team member:

- role and worker status

- work state and start date

- payroll withholding status for that state

- the state guidance page or official handbook used for your decision

Caveat

State treatment varies. Do not assume one remote employee has the same result everywhere, and do not assume no impact because sales stay low. Keep role and location records, then confirm with current state agency guidance or an official state tax handbook before closing the issue. Arizona's 2025 Tax Handbook is one example of the type of state material worth checking for current tax descriptions and statutory updates.

Build a Monthly Evidence Pack Before You Ever Get a Notice#

The lowest-stress way to manage nexus is to review it during month-end close and keep one evidence pack. It should show your state-by-state numbers, the rule you applied, and your decision: no nexus, watchlist, or register now. This is an internal control, not a legal label, but it keeps decisions consistent and easier to defend before a notice arrives.

If physical presence exists in a state, treat that as immediate registration risk regardless of sales amount. For remote seller analysis, use SST remote-seller guidance pages, including Remote Seller State Guidance, as your starting map for thresholds, compliance dates, and state links. Then verify requirements directly with each state and document what you applied.

Your monthly checklist#

Use one state tracker on the same cadence as bookkeeping close.

| Monthly item | Owner | Internal due date | What to capture |

|---|---|---|---|

| State-sourced sales totals | Finance owner or founder | 3 business days after month-end close | Gross sales by state and your sourcing method |

| Transaction counts | Finance owner or ops | 3 business days after month-end close | Separate transaction counts by state |

| Channel split | Founder or revenue ops | 4 business days after month-end close | Direct sales, marketplace sales, marketplace-facilitated sales by state |

| Sales and use tax status | Founder or tax owner | 5 business days after month-end close | Not registered / registered / collecting, filing frequency, pending decisions |

Match your tracker to each state's threshold logic. States vary on OR vs AND tests, sales base such as gross sales, gross revenues, retail sales, or taxable sales, and whether non-taxable sales count toward threshold testing.

What goes in the evidence file#

For each state, keep:

- A screenshot or export from

Remote Seller State Guidance - The relevant state agency page

- A short applied-rule note with your numbers and period tested. Example note format: "Michigan reviewed for previous calendar year; threshold is over

$100,000gross sales or200transactions; current totals are below both."

Also store the page capture date. If state guidance changes, you can still show what rule you relied on at the time.

Use three internal decision checkpoints#

These are operational labels for your process, not official state classifications:

No nexus: No physical presence and no threshold met under that state's current rule.Watchlist: Threshold not met, but you are close or the sales mix could change the result.Register now: Physical presence exists, or threshold is met under the state's test and timing.

Use explicit state criteria in each note:

- North Carolina: more than

$100,000sourced sales in the previous or current calendar year, including marketplace seller and marketplace-facilitated sales. - Michigan: over

$100,000gross sales or200transactions in the previous calendar year. - Texas:

$500,000in the preceding twelve calendar months, with collection starting no later than the first day of the fourth month after exceedance.

Make the file audit-ready before you need it#

Keep four artifacts current:

- Assumption log, including sales base used, marketplace treatment, and rule interpretation

- Registration dates

- Collection start dates

- Correction notes for missed periods

Retention and filing discipline matter. Virginia sets filing frequency based on liability and returns are due on the 20th of the following month. Records should be kept for at least three years from return due date. Texas requires marketplace sales records for at least four years. Maryland places the burden on the seller to prove sales and use tax was collected and paid correctly.

After registration, keep filing each reporting period even when no tax is due. If you find a missed period, record what was missed, what you corrected, and when collection began. That is much safer than reconstructing the timeline later.

When to Register Early and When to Escalate to a Tax Pro#

Register early when your numbers are clearly trending toward a state threshold, and escalate when presence or sourcing facts are unclear. The highest-risk situations are mixed marketplace and direct sales, unclear in-state activity, and cross-border structures.

Register early when threshold timing is tight#

Early registration is practical when your monthly trend suggests a likely threshold hit and the state's timing rules leave little room to react. This matters even more when you sell both directly and through marketplaces.

| State | Threshold or trigger | Detail |

|---|---|---|

| Virginia | More than $100,000 annual gross retail sales or 200 or more transactions | Threshold testing combines direct and marketplace-facilitated sales |

| California | Remote sellers, including foreign sellers outside the United States, must register when they exceed $500,000 | Measured in the preceding or current calendar year |

| New York | No-physical-presence business: more than $500,000 and more than 100 sales over the immediately preceding four sales tax quarters | Timing can be immediate; certificate application may need to be filed at least 20 days before operations begin |

In Virginia, threshold testing combines direct and marketplace-facilitated sales, so channel mix can change the result quickly. In California, remote sellers, including foreign sellers outside the United States, must register when they exceed $500,000 in the preceding or current calendar year. In New York, timing can be immediate for a no-physical-presence business that meets nexus requirements, and when registration is required, certificate application may need to be filed at least 20 days before operations begin.

Before you register, confirm the state rule text you relied on, including how the threshold is counted and whether marketplace-facilitated sales are included. Also avoid blanket Streamlined registration as a default when nexus is uncertain, because it can create collection and remittance obligations even where you do not have nexus.

Escalate when presence or rule interpretation is unclear#

Escalate immediately when in-state activity facts are unclear. Washington treats physical presence as requiring only more than the slightest presence, and having an employee working in the state is one explicit signal.

Escalate when sources conflict, too. State rules differ, so if your tracker, summary source, and state page do not align on counting rules, timing, or registration duty, resolve it at the state-source level or with a tax pro.

Use a hard trigger list#

Talk to a tax pro now if any of these are true:

- You are near a threshold and your state mix includes both direct and marketplace-facilitated sales.

- Official state guidance conflicts with your summary source on counting rules, timing, or registration duty.

- In-state activity signals are present or unclear, including employee location in-state.

- You are a foreign seller or non-US owner selling into multiple states and are unsure how state sales and use tax rules apply.

- You are relying on foreign ownership alone as a reason not to register.

Use this default: early registration is a judgment call, but unresolved ambiguity is an escalation event.

Mistakes That Trigger Expensive Cleanup Later#

Expensive cleanup usually starts with stale assumptions, not one dramatic error. The highest-cost pattern is simple: your facts change, but your tax position and documentation do not. A few mistakes drive most of that cleanup:

- Treating your current tax position as permanent after your activities change.

- Counting sales with logic that does not match the state rule you are testing.

- Assuming Marketplace facilitator coverage removed all of your obligations.

- Relying on secondary summaries instead of current agency language.

- Waiting for a notice before building your monthly documentation file.

A common miss is keeping a threshold-only view after facts shift. Remote hiring, inbound sales, and enterprise contracts can create obligations quickly, so treat those as immediate recheck triggers rather than "review later" items.

Another frequent miss is counting logic. If your internal tracker is built for invoicing or taxability, but the state rule counts sales differently, you can miss the point where obligations begin. Thresholds are often crossed without a clear internal signal, so your monthly tracker needs to match the state's counting method.

Marketplace coverage is not the same as full coverage#

Marketplace rules can reduce your workload, but they are not a blanket exemption. In California, beginning October 1, 2019, a marketplace facilitator is generally responsible for collecting, reporting, and paying tax on retail sales made through its marketplace.

That still does not answer your full exposure if you also sell directly. Keep a combined state view plus channel-level logs so you can separate what the platform handles from what your direct channel may still require.

California is also a reminder to verify definitions in primary text. CDTFA ties marketplace terms to Revenue and Taxation Code sections 6041 through 6041.6 and directs businesses to review registration, collection, and payment responsibilities in current agency guidance.

Secondary summaries go stale faster than your risk does#

Use summaries to triage, not to finalize decisions. Effective rules change over time; for example, beginning January 1, 2022, some California marketplace facilitators were required to obtain additional accounts for applicable fees on certain retail sales.

The low-friction control is a monthly documentation habit. Keep:

- the state rule or agency page you relied on

- an export showing your sales totals and channel split

- a short note stating your conclusion:

no nexus,watchlist, orregister now

Waiting for a notice before creating that file can increase remediation cost and weaken your ability to defend timing and assumptions.

Take the Low-Stress Route and Decide in This Order#

Use this as a practical process, not a legal shortcut: document your current exposure, check registration timing and compliance facts, then decide whether to register now or escalate.

- Gather the month's activity notes in one place.

- Review any registration-date questions or gaps early.

- Record what you reviewed, which sources you used, and your month-end conclusion.

- Take action:

register nowor escalate when facts are unclear.

The practical win is simple: clear monthly records protect your decisions and make future filings faster. Keep a dated note of what you reviewed, what source you relied on, and your conclusion for that month.

That discipline matters because ecommerce sales tax enforcement is described as increasingly aggressive and coordinated, using tools like pre-audit surveys, shared data, multi-state collaboration, audit task forces, and questions about registration timing. If the burden is on you to prove compliance, a clean monthly file is evidence, not admin overhead. Review your current exposure this month in that order, and escalate quickly anywhere the facts are unclear.

Related reading: The Best Software for Calculating and Remitting Sales Tax. If your facts conflict across states or your setup is cross-border, get a practical review and talk with Gruv.

Frequently Asked Questions

What is sales tax nexus for a remote business?

Sales tax nexus is when your connection to a state is enough to trigger sales and use tax duties like registration, collection, and remittance. That connection can come from in-state presence or from threshold rules. Do not treat “no office” as the only test.

Do I owe sales tax in a state where I have no office?

Possibly, yes. After the 2018 Wayfair shift, many states apply economic nexus even without physical presence. A common pattern is $100,000 in sales or 200 transactions, but rules vary by state, and California is often cited with a $500,000 threshold.

Does physical presence override economic nexus thresholds?

In practice, in-state presence is the first trigger to check. If you have local facts such as an office, inventory, employees, or trade show activity, you may need to register regardless of sales amount. Contractor or agent treatment varies by state, so if those facts are unclear, treat it as a review-now issue.

Do marketplace-facilitated sales count toward nexus thresholds?

It depends on the state. Keep marketplace and direct-channel logs separate, then review them together on a recurring state-by-state cadence. Use state revenue department guidance for the final call, and treat Streamlined Sales Tax’s Remote Seller State Guidance as a starting point.

What should I track every month to stay compliant?

Track state-sourced sales totals, transaction counts, channel mix, each state’s threshold method, and your current registration and collection status. Keep a simple monthly evidence file with the state page you used, your state-level export, and your conclusion: no nexus, watchlist, or register now. Nexus review is recurring, and many businesses need quarterly or monthly checks.

When should I talk to a tax professional instead of deciding myself?

Escalate when state rules conflict, your in-state activity facts are unclear, or your setup is cross-border and multi-state. Get help when contractors or agents are involved because treatment varies by state. If you are near a threshold and still unsure how a state counts sales, get advice before timing slips and late-registration penalties build; for US-entity cross-border setups, How a German Freelancer Can Handle US Sales Tax with a US LLC is a useful next read.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- advocacy.sba.gov/wp-content/uploads/2013/11/An-Analysis-of-In...trusted

- azjlbc.gov/revenues/25taxbk.pdftrusted

- cdtfa.ca.gov/industry/MPFAct.htmtrusted

- comptroller.texas.gov/taxes/sales/remote-sellers.phptrusted

- congress.gov/committee-report/117th-congress/house-report/17trusted

- dor.wa.gov/taxes-rates/retail-sales-tax/marketplace-fai...trusted

- irs.gov/pub/irs-prior/p5316--2023.pdftrusted

- maine.gov/revenue/taxes/sales-use-service-provider-tax...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How a German Freelancer Can Navigate US Sales Tax with a US LLC

Use this as your default: a U.S. LLC can change how you operate and document the business, but it does not turn German and U.S. tax questions into one answer.