Quick Answer

Set compensation for a cross-border remote offer by pricing a defined base fee first, then putting payment currency, settlement rules, fees, incentives, and risk terms in writing. Build a fee band from role scope, market comparables, and delivery complexity, and treat benefits, compliance costs, and equity as separate deal terms so the headline number reflects what actually lands in your account.

If you work across borders, the offer in front of you is not just a salary discussion. It is a business deal. Review it that way.

This guide gives you a five-layer compensation stack you can use to price the work, protect cashflow, and keep avoidable risk out of the contract. The goal is simple: stop negotiating like a line item and start reviewing the deal like the person who has to run it.

Layer 1: Secure Your Foundation - Negotiating a Premium Base Fee#

Your base fee should be priced as a business fee for defined services, not as a location-adjusted salary. If you get this layer wrong, every upside term after it has to make up for an underpriced core deal.

This matters most when a company tries to fit you into its internal pay model. Some remote employers openly set pay by role, level, and location. You do not need to argue that model is wrong. You need to separate their employee compensation logic from the fee for your engagement.

How should you anchor when the scope is clear?#

When the company already knows the problem it needs solved, anchor on the outcome and the scope. The basic point is simple: your fee reflects the work, the responsibility, and the value of the result, not the cost of living where you happen to work.

Bring evidence that makes that position feel routine rather than confrontational. A solid evidence pack includes comparable role titles, a short scope summary, and market data tied to the occupation you actually perform. Public labor data helps here. The U.S. Bureau of Labor Statistics OEWS publishes annual wage estimates for approximately 830 occupations, and percentile wages let you show a range instead of one cherry-picked number.

If you get the usual location-based objection, do not escalate. Try this: "I understand your comp model uses location for employees. For this engagement, I'm pricing against the scope of work, the level of expertise required, and current market comparables for this function." Then ask a narrower question. Are they buying execution inside a pre-defined band, or are they buying independent delivery with your judgment included? That answer usually tells you whether to hold firm or walk.

Use this checkpoint before you make the case: verify that the comparator role really matches the work on skill, effort, and responsibility. If you use the wrong occupation code or compare against a narrower job, your band is easy to knock down. A common failure mode is leaning on one headline salary number with no documented assumptions.

How do you build a defensible fee band?#

Do not open with a single number. Build a low, mid, and high band first, then decide where to anchor based on the complexity of the work.

| Input | What to include |

|---|---|

| Role scope | What you own, what you advise on, and what you do not cover |

| Market comparables | More than one source, with at least one public benchmark such as OEWS percentiles |

| Delivery complexity | Cross-functional ownership, ambiguous requirements, or a need for independent decision-making |

Start with three inputs. Define the role scope in plain language: what you own, what you advise on, and what you do not cover. Collect market comparables from more than one source, with at least one public benchmark such as OEWS percentiles. Then adjust for delivery complexity, such as cross-functional ownership, ambiguous requirements, or a need for independent decision-making.

Percentiles are more useful than averages because they show the spread. For example, you can use the 50th, 75th, and 90th percentiles as a mid, strong, and premium reference point, or the 25th, 50th, and 75th if the scope is narrower. Write down why you chose that band. If the client pushes back later, you want a one-page memo that shows the occupation match, the scope assumptions, and what pushed the fee upward.

| Term | Weak base-fee term | Strong base-fee term |

|---|---|---|

| Pay basis | Salary-style amount with loose duties | Monthly professional service fee or retainer tied to defined scope |

| Currency denomination | "Local currency equivalent" at payer discretion | Invoice issued in [USD/EUR/other agreed currency], payable in that same currency where possible |

| Fee language | "Compensation" or "salary" | "Professional service fee" for services rendered under the agreement |

| Payment friction | Recipient absorbs wire fees, FX spread, and platform deductions | Client pays full invoiced amount; any transfer or provider fees are handled on payer side or grossed up |

That last row matters more than many people expect. The World Bank's remittance data still shows meaningful cross-border payment cost, with a global average of 6.49 percent. If the contract is silent, that friction can land on you depending on the payment rail and terms.

What currency mechanics should you set before you sign?#

Once the fee is right, lock down how it will actually be paid. A stable invoice currency helps, but it does not remove exchange risk by itself. It only works if the contract states who converts, which rate source applies, and when the conversion is fixed.

Your contract and invoice should match on four points: invoice currency, settlement currency, conversion source, and fee responsibility. If same-currency settlement is not possible, add a checkpoint such as: payment converted using your bank or payment provider rate on the invoice date or payment date, with no deductions from the invoiced amount. Then verify three things before signing: the payer can send the invoice currency, your local tax or VAT treatment, and your own reporting currency rules.

Those details are not admin trivia. In the UK, you can invoice in any currency, but VAT accounting still requires sterling conversion, and HMRC gives 2 standard ways to do that. For U.S. tax reporting, amounts must be expressed in U.S. dollars, and the IRS says to use the exchange rate when the item is received, paid, or accrued. If you skip these checkpoints, a premium fee can shrink in practice through conversion losses, reporting errors, or fee deductions. If you want a quick next step, try the free invoice generator.

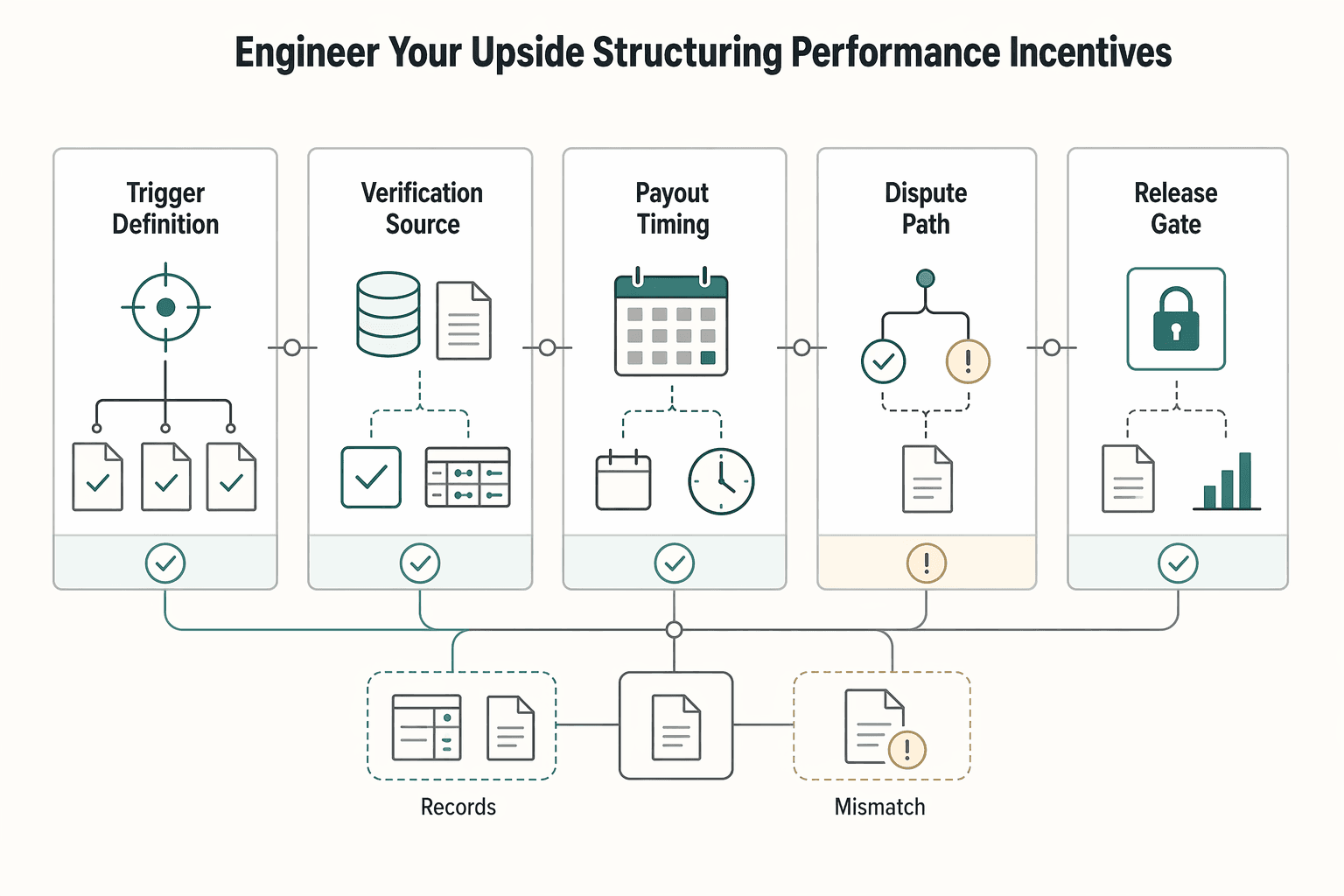

Layer 2: Engineer Your Upside - Structuring Performance Incentives#

After you lock your base fee, treat variable pay as real only when you can measure it, verify it, and invoice it. If payout depends on discretion, budget timing, or a manager's opinion, treat that upside as uncertain and keep your core fee priced accordingly.

Use the same precision you used for base-fee benchmarking: define outcome triggers in writing, then choose your short-term cash vs long-term equity mix deliberately. That mix can work, but only when trigger and payout mechanics are explicit in the contract.

| Contract point | Discretionary bonus | Outcome-based incentive |

|---|---|---|

| Trigger definition | Broad language like "based on performance" | Specific metric or milestone written into the agreement |

| Verification source | Manager opinion or internal review | Named data source, report, or sign-off record |

| Payout timing | Undefined or "subject to company timing" | Fixed payout timing tied to a verified confirmation record |

| Dispute path | Often unclear | Defined review path using the agreed record set |

| Approval dependency | Usually needs extra internal approval | Limited to confirming the agreed trigger occurred |

How should you draft KPIs like contract terms?#

Draft each KPI or OKR like an invoice condition so it survives procurement, finance review, and team changes. Use this framework:

| KPI element | What to specify |

|---|---|

| Metric owner | Who maintains the number |

| Baseline | Starting figure and date |

| Measurement window | Exact period |

| Data source | Named source of truth |

| Acceptance criteria | What counts as success, including exclusions, overrides, or minimum quality threshold |

- Metric owner: who maintains the number, for example [client RevOps lead] or [product analytics owner]

- Baseline: starting figure and date, such as [metric value on DD/MM/YYYY]

- Measurement window: exact period, such as [30/60/90 days] or [quarter ending DD/MM/YYYY]

- Data source: named source of truth, such as [CRM dashboard], [finance report], or [signed acceptance memo]

- Acceptance criteria: what counts as success, including exclusions, overrides, or minimum quality threshold

Before signing, confirm you can access or receive the data needed to prove the trigger. If you cannot verify the number, you cannot reliably collect the incentive.

When does equity make sense?#

For an independent contractor, equity is a risk and time-horizon decision, not a cash substitute. Review four clause checkpoints before you treat it as meaningful value: vesting trigger type (time-based or milestone-based), acceleration conditions, treatment on termination, and exit-event handling.

If any of those points is missing, get it in writing before you sign. The tradeoff is straightforward: equity may increase long-term upside, but it also increases exposure to delayed value and termination risk.

How do you turn completion bonuses into payment controls?#

A completion incentive is strongest when it is tied to acceptance workflow, not motivation language. Define what is reviewed, who signs off, when sign-off is considered complete, and which event releases the final invoice.

Lock three points in the contract: acceptance workflow, invoice release condition, and default sign-off mechanics if the client goes silent after delivery. Without those controls, the completion incentive is often the easiest line item to delay.

If you want a deeper dive, read What to Do If You've Been Misclassified as an Independent Contractor.

Layer 3: Build Your Risk Shield - Critical Contract Clauses#

After you set fee and upside, lock down the clauses that protect what actually lands in your account and who carries which risks. In cross-border work, keep these points in the signed contract itself, not in side emails.

| Clause area | Weak clause | Enforceable clause to confirm before signing |

|---|---|---|

| Currency adjustment | "Payment will be made in local equivalent." | States invoice currency, exchange-rate source, valuation date, who calculates adjustment, and an adjustment threshold verified from official contract or payroll records before use. |

| Payment terms | "Paid upon processing" or "standard company terms." | Defines invoice trigger, due date verified from the signed agreement before use, accepted payment rail, and the record that starts the clock. |

| Fee allocation | Silent on bank/platform/intermediary charges. | Assigns responsibility for wire, platform, and correspondent/intermediary fees so short settlement is handled by rule, not negotiation. |

| Liability coverage | "Contractor will maintain insurance if needed." | Defines policy scope, covered activities, exclusions, certificate timing, and how coverage aligns with confidentiality/data-handling duties. |

How should each clause do one job?#

Use each clause as a mini-template:

- What it does: names one operational rule.

- What risk it prevents: shows the downside if the rule is missing.

- What to confirm: lists the exact drafting elements you check before signing.

For currency and settlement, the clause should preserve value, not just describe a payment method. Your risk is invoicing one amount and receiving less because of conversion timing, deductions, or process changes. Confirm invoice currency, settlement mechanics, payment rail, and whether the client can switch rails without your approval.

For payment terms, confirm when you can invoice, when payment is due, and what evidence proves the due-date clock started. If you cannot tell whether "received" means sent by the client or settled into your account, the term is still too weak.

Who handles compliance responsibility?#

Treat compliance as a workflow with clear boundaries, not a vague promise. Country rules vary across payroll, benefits, taxes, contracts, and terminations, and missteps are often expensive and slow to fix. Confirm who provides classification records, residency/tax documentation, withholding details, and who pays for cross-border advisory support if a filing issue appears.

If these responsibilities matter, they should appear as labeled clauses or a schedule in the final agreement. If the answer is "finance will handle later," treat that as unresolved risk.

How should liability match your real work?#

If you touch client systems or confidential information, your contract should include clear data security and privacy obligations. That helps reduce compliance risk and lowers the chance that weak safeguards become a cyber exposure. Confirm permitted data access, required controls, breach-notice process, and whether insurance scope actually covers your activities.

Before signing, run this section-only checklist:

- invoice currency is explicit

- settlement mechanics are explicit

- transfer-fee responsibility (including intermediary fees) is explicit

- dispute path for short payment or clause disagreement is explicit

- insurance scope definitions match the work

For a step-by-step walkthrough, see How to Set Up Workers' Compensation Insurance for a Remote Team.

Layer 4: Fund Your Infrastructure - Redefining 'Benefits'#

Treat benefits as an operating budget you control, not a vague perk bundle. If a cost is required for continuity, compliance, or secure delivery, you should either build it into your base fee or define it as reimbursable in the contract.

Start by naming your operating categories, then assign a funding rule to each one. Global teams operate in changing legal, tax, economic, and geopolitical conditions, so your structure should be built for volatility, not best-case stability. Your documentation standard is simple: each category is either included in fee, reimbursable with proof, or client-provided.

| Category to define | Business outcome protected | Proof required for reimbursement | If the client declines a stipend line |

|---|---|---|---|

| Health and personal coverage | Continuity when your work capacity is disrupted | Contract should define acceptable proof in advance | Increase base fee to absorb the cost |

| Workspace, internet, and connectivity | Reliable delivery and meeting readiness | Contract should define which document starts review | Fold recurring costs into your monthly fee |

| Equipment, software, and security | Delivery quality, speed, and safer client-data handling | Contract should define preapproval and receipt/invoice rules | Request client-provided tools or a larger setup fee |

| Compliance and payroll administration | Lower cross-border admin friction and fewer process errors | Named vendor invoice or client-provided service record | Ask the client to provide a centralized global compliance/payroll platform |

| Long-term savings support | Personal financial resilience over multi-year work | Separate written contribution rule | Convert to cash compensation and document it clearly |

Avoid broad "allowance" wording that leaves reimbursement discretionary. If a line is real, define its trigger, proof, and decision owner in writing.

Before signing, confirm this implementation checklist:

- stipend structure by category (included, reimbursable, or client-provided)

- payout cadence

- currency and conversion handling

- documentation expectations per reimbursable line

- review cadence for documented term updates

Keep long-term savings support as a separate, jurisdiction-dependent line. Verify the available vehicle or option from official plan, contract, or payroll records before use, or document the cash alternative explicitly. Related: How to Manage and Pay a Global Team of Contractors Compliantly.

Layer 5: Vet the Offer - Spotting Red Flags in the Contract#

Once money terms look good, this section is your final risk filter: do not sign until each critical risk is written in plain, enforceable contract language.

How do you verify the engagement model and the actual payor?#

Use one rule for either model: if the paperwork does not clearly match who contracts with you, who pays you, and who handles disputes, treat the offer as a bad fit until it is fixed.

Ask for a written responsibility map that names:

- contracting entity

- invoicing or payroll entity

- issuer of formal pay or tax records

- escalation contact for payment or contract disputes

Bad-fit triggers before signing:

- recruiting messages and contract entity names do not match

- the model changes late, but contract documents are not reissued

- the company will not provide supporting compliance records when it says structure is compliance-driven

If they cite a compliance record, ask to see the record itself. For example, a PCRB Data Card is an issued document from the Pennsylvania Compensation Rating Bureau and can show risk name, location, PCRB file number, authorized classifications, and sometimes experience modification.

What should complete currency language include?#

Your contract should fully state payment mechanics before execution. If key terms are implied, you carry the risk.

| Risky wording | Acceptable wording | Why it matters |

|---|---|---|

| "Payment will be made in local currency at the prevailing exchange rate." | Contract names payment currency and states complete conversion handling in final text. | "Prevailing" is not auditable later. |

| Transfer, bank, or FX fees are not mentioned. | Contract explicitly states how transfer and conversion fees are handled. | Silence creates post-payment disputes. |

| Unverified adjustment threshold left in draft text. | All placeholders are removed and replaced with signed final language. | Draft notes are not protection. |

Use a direct redline request: "Please replace vague conversion language with complete payment mechanics and remove all placeholders before execution."

How do you ring-fence your IP and narrow exclusivity?#

Assume broad IP language will expand unless you limit scope in writing. Phrases like "perpetual, irrevocable, royalty-free, fully-paid, nonexclusive, worldwide license," combined with rights to "sublicense or otherwise authorize" third parties, and terms that continue "perpetually without any right of termination or revocation" can reach far beyond one project if you do not carve boundaries.

| Boundary | Limit in the contract |

|---|---|

| Background IP | You retain background IP (templates, methods, pre-existing tools) |

| Client ownership | Limited to defined deliverables in the statement of work |

| License to your background IP | Limited to what is necessary to use those deliverables |

| Exclusivity | Limited to defined direct competitors, defined scope, and defined term |

Redline for explicit scope boundaries:

- you retain background IP (templates, methods, pre-existing tools)

- client ownership is limited to defined deliverables in the statement of work

- any license to your background IP is limited to what is necessary to use those deliverables

- exclusivity is limited to defined direct competitors, defined scope, and defined term

For framing, the sample SEC language shows how a competitor restriction can be narrowed to direct competitors during a defined support period, which is tighter than a blanket "no other clients" restriction.

Before signing, run this final checklist:

- engagement model rationale and named payor are documented

- payment currency mechanics are complete and ready to use

- background IP carve-outs are explicit

- exclusivity limits are narrow and time-bound

- escalation path is named for contract or payment disputes

We covered this in detail in How to Handle Payroll Taxes for a Remote US Team.

Conclusion: You're Not a Line Item, You're the CEO#

If an offer only works at the headline level, it is not ready. Your job is to turn a number into an operating deal: money you can plan around, scope you can defend, and terms you can verify before you sign.

Use the five layers as a final check on every offer:

- secure a base fee that matches the role and responsibility

- tie any upside to defined outcomes, not broad promises

- reduce downside with clear written terms around how the deal actually works

- fund the tools, coverage, and admin costs you absorb

- vet the document pack for gaps, placeholders, and policy language nobody can explain

Those five layers collapse into three practical commitments you can carry into any contract review. Protect downside first. A weak payment path or vague obligations can hurt you faster than a disappointing bonus. Fund operations second. If you pay delivery costs out of your own pocket without pricing them in, the margin can disappear even when the rate looks strong. Price for delivered outcomes third. Variable pay can be useful, but only when the trigger, calculation method, and decision-maker are clear in writing.

That last point matters more than most people think. Compensation plans can be adjusted in complicated ways, and incentive design can distort behavior instead of rewarding the right result. Your checkpoint is simple: if the other side cannot show how the metric is measured, who can change it, and what document controls the payout, discount that upside and negotiate the fixed terms harder. Negotiation is expected behavior, especially at larger companies, and it rarely creates hard feelings.

In your next client conversation, walk through the offer once out loud, then do a second pass on the contract with a pen or comments turned on. Mark every item as fixed cash, conditional upside, operating cost, or unresolved risk. If anything important stays in that last bucket, you are not ready to sign.

Frequently Asked Questions

How do you push back on location-based pay without turning it into a debate?

Acknowledge the company's model, then anchor on scope, expected outcomes, and the value of replacing that capability. Ask for the actual band, the inputs behind it, and whether they are pricing your location, the role, or the market for the skill. If they cannot show the basis, treat the method as unclear rather than settled.

What should you treat as non-negotiable first?

Start with cashflow risk: payment currency mechanics, payment terms, fee allocation, and IP boundaries. Ask for the invoice trigger, due date, approval step, and any internal threshold or approval standard to be written into the contract rather than left to policy or email. Keep unresolved payment mechanics explicit if they cannot verify them.

How do you ask for a better package without sounding rigid?

Acknowledge budget limits, then anchor on total deal value instead of only base cash. Ask which part of the package can move, such as cash, equity, sign-on support, or expense coverage. That keeps the conversation commercial and opens more than one path to a better outcome.

How should you treat equity in a global offer?

Treat equity as one part of the total package, not as a replacement for clear cash terms. Ask for the grant documents, vesting schedules and timelines, and a written explanation of local compliance and tax implications. If they cannot explain how the grant works in your jurisdiction, discount its value until you verify it.

How do you calculate your all-in number before you counter?

Start with the amount you need the contract to produce, then add every cost you will personally absorb. Include taxes and filing support, insurance and benefits, long-term savings contributions, software, hardware, workspace, connectivity, legal and accounting time, banking and transfer costs, a contingency buffer, and target profit. Do not rely on the headline rate alone.

How do you compare offers that pay in different currencies or deduct different amounts?

Do not compare gross to gross. Check the payout currency, where conversion happens, the exchange-rate source, send and receive fees, intermediary fees, withholding or local deductions, and the amount expected to land in your account. Ask for a sample payout statement or a written settlement example before you compare offers.

What do you ask for next when the company says “that’s just our policy”?

Acknowledge the policy, then ask for the written document that controls the outcome. Request the clause, exhibit, grant document, or payroll note that defines the payment path, fee handling, and escalation contact. If they cannot produce it, treat the point as unresolved rather than settled.

How do you think about EOR versus direct contractor?

Do not assume one model is automatically better. Ask who hires you, who pays you, what documents you receive, and which compliance tasks stay with you versus the company. If that responsibility map is not clear in writing, pause before you sign.

When should you slow down or walk away?

Slow down when the recruiter's explanation and the contract pack do not match, when placeholders remain in the draft, or when equity is mentioned without grant paperwork. Walk away if they refuse to name the payor, the governing documents, or the escalation path for payment problems. Those gaps are evidence that the deal is not ready.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bls.gov/oestrusted

- dol.gov/agencies/oasam/centers-offices/civil-rights-...trusted

- eur-lex.europa.eu/EN/legal-content/summary/equal-pay-for-equal...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- opm.gov/policy-data-oversight/pay-leave/pay-administ...trusted

- remittanceprices.worldbank.orgtrusted

- snaphunt.com/resources/onboarding-and-employing-talent/gu...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay International Contractors With Fewer Delays and Disputes

Paying international contractors reliably starts with compliance setup before the first invoice. Missed registration or filing steps turn routine payouts into delays and penalties.

Tax on Foreign Inheritance for U.S. Persons

Start by separating three decisions before you touch any forms: whether a foreign transfer is treated as a gift or bequest that is excluded from gross income, whether `Form 3520` reporting may apply, and when the facts are uncertain enough to require a qualified tax professional. The goal is documented judgment, not guesswork.