Quick Answer

Use reps and warranties insurance when unknown-breach exposure is meaningful and you want cleaner proceeds at closing. Start broker outreach around the LOI, gather NBILs, and compare the policy draft against the purchase agreement and disclosure schedules before indemnity terms harden. If those documents do not align, expected protection can narrow and known issues should stay in explicit deal allocations.

R&W Insurance: Your Blueprint for a Clean Exit#

When you sign a purchase agreement, you make factual promises about the business. If one of those promises is wrong and the buyer suffers a loss, that can become a post-close claim. The same risk shows up across familiar rep areas like tax, employment, property, and title. This is standard M&A risk, not an edge case.

In most deals that use R&W insurance, the buyer is the insured party. Coverage usually turns on the buyer showing a breach of a representation or warranty in the acquisition agreement and a resulting financial loss. For covered matters, recovery may run to the insurer instead of relying first on seller proceeds.

In practice, three things have to line up: the rep package in the purchase agreement, the due diligence record, and the policy wording. Diligence findings can shape what gets disclosed or carved out in the deal terms. The indemnity terms then help determine what stays with the seller and what may shift to the policy.

If you are selling, review the policy draft against the exact reps and disclosure schedules, not just a summary. Also review change-of-control provisions so closing does not accidentally cancel existing coverage.

Do not assume the policy covers every issue tied to the business. Known diligence issues and other excluded matters may still need to be handled directly in the deal terms. Sellers can still retain liability for carved-out items such as purchase price adjustments and other exclusions. A clean exit comes from precise risk allocation, not broad assumptions about coverage.

There is also a practical post-close benefit for sellers. For covered losses, the buyer may pursue the policy rather than pursue you directly. That does not remove all friction, but it can shift part of the recovery path from seller-buyer collection to the insurer. Once that foundation is clear, the next question is how this compares with a traditional escrow structure. Related: A Guide to Selling Your Freelance Business or Agency.

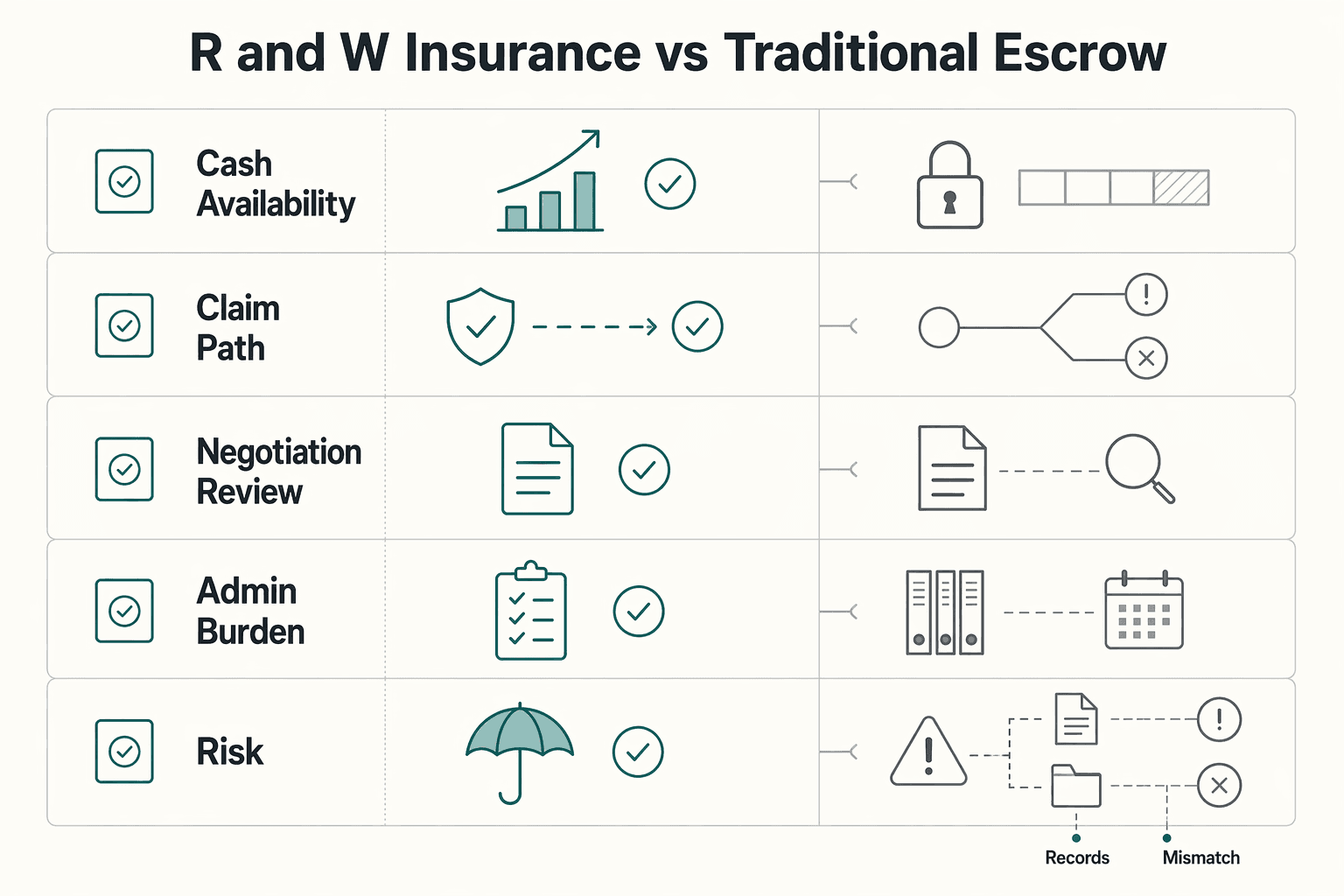

The Strategic Trade-Off: R&W Insurance vs. Traditional Escrow#

Your core choice is simple: keep more proceeds available at closing, or leave part of your payout tied to post-close representation and warranty claims.

That choice is set by the purchase agreement and the policy terms, because coverage generally follows the representations and warranties written into the deal.

| Decision point | Traditional escrow | Reps and warranties insurance |

|---|---|---|

| Cash availability at close | Part of seller proceeds is held at closing to cover indemnifiable losses tied to reps and warranties. | Seller holdback may be reduced depending on deal and policy structure, which can leave more proceeds available at closing. |

| Claim path | Claims are handled through purchase-agreement indemnity and escrow mechanics. | For covered matters, recovery may route through the policy under its terms instead of relying first on seller-held proceeds. |

| Negotiation and review focus | Escrow and indemnity terms are negotiated in the deal documents. | Insurance can reduce or eliminate escrow in some deals, but underwriting scrutiny and policy wording add their own review cycle. |

| Admin burden after close | Seller proceeds can remain contingent while escrow-related claims are resolved. | Post-close work can shift toward policy notice and claims handling; claims activity can still be significant. |

| Who bears breach risk | Seller proceeds are the practical backstop inside the indemnity structure. | Covered breach risk can shift to the insurer under policy terms. |

The real trade-off is not escrow versus insurance in the abstract. Escrow ties up proceeds. Insurance can reduce that holdback in some structures, but it also adds underwriting, extra review, and policy-language risk.

Before you get comfortable with either structure, review the purchase agreement and policy draft together. If those documents are not aligned, the risk transfer on paper may be narrower than it looks in the term sheet.

Claims activity and underwriting scrutiny can also add execution pressure. In practice, that often shows up in underwriting questions and policy-term decisions.

When each option fits#

Use traditional escrow when both sides prefer seller proceeds as the primary backstop for indemnifiable losses. Use insurance when you want less reliance on seller proceeds for covered issues and potentially more cash available at closing.

If you are deciding between them, start with one question: should post-close breach risk sit on your sale proceeds or on a transaction-risk policy? The answer usually clarifies the rest of the structure.

The Decision Framework: When is R&W Insurance Non-Negotiable?#

Treat R&W insurance as a strong fit when two conditions are both true: unknown-breach exposure is meaningful, and clean seller proceeds at closing are a priority. If only one condition is true, treat it as case-by-case. If neither is true, a seller-backed structure is often enough.

Do not let market chatter make the decision for you. The market is broad, with nearly 40 underwriting participants in the current market context, and placement can move quickly in some deals once submission and diligence are underway. Even so, terms and coverage scope still vary deal by deal. Use live broker feedback, not stale benchmarks. Older shorthand can help directionally, but not as a rule. For example, "~10% escrow" is a historical reference point, not a universal outcome.

Classify the deal#

| Classification | Strongest signals | What to do next |

|---|---|---|

| Strong fit | Buyer is pressing for broad indemnity protection or a meaningful escrow; unknown-breach exposure is material; sellers need prompt access to proceeds at closing | Start broker outreach early and request NBILs before indemnity terms harden. Review policy and purchase agreement language in parallel. |

| Case-by-case | Buyer wants protection but is flexible on structure; diligence is solid and documented; some holdback may be workable | Run an escrow-versus-policy comparison using the buyer's actual indemnity asks. Compare claim path, process load, and proceeds timing side by side. |

| Likely unnecessary | Buyer is comfortable relying mainly on seller-backed remedies; unknown-breach concern is limited; diligence is clean and easy to evidence; no strong need to free proceeds at closing | Keep a seller-backed structure unless negotiation pressure changes. Confirm the purchase agreement matches that lower-risk posture. |

Use this as a practical next step. Strong fit means start broker market checks early and prepare for NBIL and underwriting-call work. Case-by-case means run a real side-by-side structure comparison. Likely unnecessary means keep seller-backed terms and watch for buyer-demand drift.

The check that matters before you spend time on quotes#

Before you treat insurance as a live option, verify diligence quality and document alignment. Underwriters review buyer third-party diligence reports, broader diligence materials, and seller-provided data-room content. If those records are thin or inconsistent, underwriting can get harder and policy outcomes may drift from expectations.

Use this checkpoint before you chase indications: compare the purchase-agreement reps, disclosure schedules, and diligence reports to confirm they tell the same story. If that alignment is weak, fix it first. A useful checklist reference is A M&A Consultant's Guide to Due Diligence Checklists.

A common failure mode#

A common miss is assuming the policy will fix gaps in deal drafting or diligence. Because policy terms vary materially by deal, known or already identified issues should be allocated explicitly in the transaction terms rather than assumed to be covered.

Once you decide how much post-close risk to transfer versus retain, map how proceeds and contingent payments will actually move so controls are clear before signing. Use Gruv Docs as a practical workflow reference.

From Defensive Cost to Offensive Weapon: Using R&W in Your Negotiation#

Your position improves only when your deal file is disciplined. What helps is a documented process with clear checkpoints, traceable requirements, and staged sequencing, not broad assurances.

When a complex issue is live, lead with process. In complex negotiations, staged sequencing usually works better than trying to settle every issue at once. Keep each discussion tied to one concern, with the supporting draft language and records ready before you make the ask.

Negotiate in stages#

Start with the immediate concern, then connect it to verifiable materials. Get the scope right first, then test whether the current draft set is actually ready, then move forward as the documents evolve.

| Buyer concern | Better framing | Seller verification check before presenting |

|---|---|---|

| Scope ambiguity | "Let's confirm scope first, then carry that agreement into the draft set." | Confirm scope decisions are captured in the active draft set. |

| Proposal readiness | "We want this evaluated against the current record, not assumptions." | Check required proposal items are present and consistent. |

| Requirement alignment | "We will show how each key requirement is addressed so both sides can review the same trail." | Maintain a current requirements traceability matrix for key items. |

| Implementation coordination | "Complex work should move in stages, with explicit overlap decisions and recurring progress reviews." | Verify phase sequencing, overlap choices, and progress-meeting cadence are documented. |

People will look past promises and look at the record. If you cannot show one consistent package, uncertainty rises fast, especially when coordination spans multiple contracts.

What to say vs. what not to say#

- Say: "We are not asking for less discipline. We are proposing a documented structure, and we can walk through the scope decisions, traceability items, and implementation checkpoints."

- Do not say: "Just trust the proposal" or "the details can be worked out later."

- Say: "If a point is not supported in the current draft set, we will treat it as open and document it before asking you to rely on it."

- Do not say: anything definitive about coverage, exclusions, or outcomes that is not reflected in current drafts.

Coordination is the real checkpoint#

The main operational risk here is coordination drift. If scope documents, traceability artifacts, and implementation materials move on different timelines, mismatch risk climbs fast.

Run a joint cross-team review before the buyer meeting, not after. Use a simple traceability sheet for key requirements: scope reference, proposal reference, supporting record, and implementation owner. If any link is missing, treat that as a stop sign.

For practical prep, use A M&A Consultant's Guide to Due Diligence Checklists.

Pre-meeting checklist#

- Use one date-stamped draft set for the meeting.

- Confirm scope decisions are reflected in that draft set.

- Spot-check the highest-risk requirements for wording and support consistency.

- Confirm speaking lanes and owners in advance.

- Remove buyer-facing statements that go beyond current draft support.

- If a required artifact is missing, pause and fix it first.

Handled this way, process discipline is not just defensive. It becomes a useful negotiation tool, but only when your documentation can withstand scrutiny and cross-contract coordination demands.

The Playbook: Navigating the R&W Insurance Process#

Treat R&W insurance as two linked tracks: underwriting and claims. Build the underwriting record with a later claim in mind. Recovery generally turns on two primary thresholds - breach and loss - and both are common dispute points.

| Phase | Primary participants | Key inputs | Key decisions | Common failure points |

|---|---|---|---|---|

| Underwriting setup | Insurer and policyholder teams | Underwriting submissions and transaction record | Whether underwriting questions are sufficiently addressed | Gaps in the record that can later complicate breach or loss analysis |

| Breach analysis (claim stage) | Insurer and policyholder teams | Policy language and evidence of the alleged breach | Whether a breach is established | Hyper-technical breach positions that diverge from the policyholder view |

| Loss analysis (claim stage) | Insurer and policyholder teams | Loss methodology and supporting calculations | How loss is measured | Disputes over quantification, including use of a multiple |

Phase 1 underwriting setup#

This phase sets the foundation for later claims handling. Your objective is to build a clear underwriting record that can also support future breach and loss analysis. Process ownership varies by deal, but insurer and policyholder teams should keep responsibilities explicit. Good output here is a documented record of key underwriting questions, answers, and unresolved issues. Flag factual or documentation gaps early so they do not turn into claim-stage disputes later.

Phase 2 breach analysis#

If a claim arises, breach is one of the two main gates to recovery. Your objective is to tie the alleged breach to the policy language and the underlying facts. At this stage, insurer and policyholder teams will present and test competing breach positions. A strong file gives you a focused breach analysis backed by a consistent factual record. Expect technical disagreement on whether the breach standard is met, and build the record with that in mind.

Phase 3 loss analysis#

Loss is the other main gate to recovery, and it is often a source of dispute. Your objective is to quantify loss in a way that is clearly linked to the alleged breach. Insurer and policyholder teams will evaluate methodology, assumptions, and calculations. The right output is a loss analysis with transparent assumptions and support. Address valuation and methodology disagreements directly, including any dispute about use of a multiple. Recovery generally depends on establishing both breach and loss, so disagreement on either point can block resolution.

For a deeper prep checklist before underwriting, see A M&A Consultant's Guide to Due Diligence Checklists.

The Bottom Line: Cost vs. Certainty#

The decision is straightforward: pay a defined cost to transfer unknown-breach risk to an insurer, or keep more of that risk with the seller through escrow and indemnity. A buy-side policy can create a cleaner recovery path for covered unknown issues, while traditional indemnity keeps recovery tied more directly to seller obligations.

In a traditional indemnity structure, the seller indemnifies the buyer if reps or warranties are untrue and losses result. With buy-side insurance, the buyer can seek recovery from the insurer directly. Escrow may be reduced or removed in some deals, but not all.

| Cost or exposure element | How it works in practice | What certainty you gain | Document alignment checkpoint |

|---|---|---|---|

| Premium | Transaction cost allocated by the deal terms | Prices part of unknown-breach exposure up front | Confirm who pays and verify the policy draft matches the latest purchase agreement |

| Retention (if applicable) | A policy may include a first-loss layer before full insurer recovery | Clarifies what risk remains with the insured before coverage responds | Check how retention interacts with escrow and indemnity terms in the acquisition agreement |

| Escrow or holdback | Proceeds held back under traditional indemnity mechanics | Gives the buyer a funded recovery source | Confirm escrow terms are consistent with the insurance structure and the acquisition agreement |

| Excluded matters and fraud exposure | Some items stay outside coverage, and sellers may still have liability | Makes clear where insurance stops and seller exposure continues | Compare exclusions with the acquisition agreement |

Before signing, run one final checklist on the live drafts: premium payer, retention treatment, escrow interaction, excluded-matter allocation, and whether the policy wording still tracks the latest acquisition agreement. Misalignment between policy terms and the agreement can leave avoidable gaps.

Avoid outdated rules of thumb on pricing or retention. Use live quotes and current draft language. Where benchmarks are still unresolved, keep the pricing and retention discussion open until broker quotes and policy drafts are confirmed.

For transaction prep before placement, see A M&A Consultant's Guide to Due Diligence Checklists.

What R&W Insurance Doesn't Cover: Understanding the Exclusions#

Do not treat R&W insurance as blanket post-close protection. Its main job is often to address breach risk the buyer did not know about. Known or specifically carved-out issues still need to be allocated in the deal terms unless the policy wording says otherwise.

Scope is not uniform across products. Some market guidance frames R&W as protection for unknown risk. At least one buyer-side small-deal product for deals under $20 million is described as covering some known breaches tied to seller knowledge. The practical takeaway is simple: do not assume a point is excluded, and do not assume it is covered. Confirm it in the current draft.

| Issue type | Policy wording check | Purchase agreement allocation | Disclosure schedule treatment | Pricing or escrow consequence |

|---|---|---|---|---|

| Diligence-found red flag | Confirm whether the draft excludes it, narrows it, or leaves a coverage path | If excluded, allocate through special indemnity, pricing, or holdback | Keep schedule language aligned with the diligence record | Meaningful carve-outs can push risk back into escrow or economics |

| Seller-disclosed matter | Check whether disclosure limits coverage under this policy form | Decide explicitly who keeps this risk if the policy will not respond | Avoid vague disclosure language that blurs what was disclosed | Broader disclosure can reduce coverage certainty |

| Underwriter-added specific exclusion | Track each added carve-out in the latest policy markup | Mirror that allocation in indemnity mechanics before signing | Tie the carve-out to the same fact pattern in schedules and deal records | If material, re-test escrow reduction assumptions |

A short exclusions workflow#

- Identify likely carve-outs early from diligence findings and draft disclosures.

- Test those items during underwriting, especially if you are evaluating a buyer-side form that may address some known-breach scenarios.

- Before signing, reconcile the final policy draft against the purchase agreement, disclosure schedules, and escrow or indemnity structure.

Pre-close control list#

- Match insurer submissions to the actual diligence record, including any third-party review of prior diligence work.

- Recheck the latest acquisition agreement against the latest policy markup.

- Confirm every identified issue has one clear home: covered, excluded, indemnified, priced, or escrow-backed.

- Catch possible mismatches early: an issue fully discussed in diligence but described loosely in underwriting, which can later create disputes over whether it was truly unknown.

If you want a broader sale-prep checklist before placement, see A Guide to Selling Your Freelance Business or Agency.

Conclusion: Securing Your Legacy with Confidence#

A clean exit does not come from the policy alone. It comes from keeping the policy wording, purchase agreement reps, and disclosure schedules aligned as one package. When that alignment holds, the upside is practical: escrow pressure may be reduced, indemnity negotiations are less likely to stall the deal, and covered breach risk has a defined insurance path.

| Decision lens | Traditional escrow path | Insured path |

|---|---|---|

| Capital access | Part of your proceeds may remain in escrow as holdbacks. | Escrow pressure may be reduced, depending on final deal terms. |

| Claims handling path | Recovery is handled through purchase-agreement indemnity mechanics. | Covered losses are handled through the policy, based on final wording. |

| Post-close planning flexibility | Proceeds planning can be constrained by holdbacks. | Planning can be more flexible if the policy clearly picks up the relevant risk. |

Use one final document-control check before signing: compare the reps-and-warranties articles in the purchase agreement against the policy draft and disclosure schedules. In one SEC merger agreement dated August 20, 2024, those sections are explicitly separated as Article IV and Article V. Treat that structure as a checkpoint. If agreement language, schedule language, and policy wording drift apart, coverage certainty may drop.

One highlighted failure mode shows up after closing, when inaccurate disclosures are alleged or an unknown claim appears months later. If your documents are inconsistent, the dispute shifts to what was represented, what was disclosed, and where the risk was supposed to sit.

The practical takeaway is simple: do not evaluate a clean-exit promise at headline level alone. Confirm it only after counsel, broker, and the deal team reconcile the latest agreement draft, disclosure package, and policy wording line by line. If you want to tighten transaction prep first, read A Guide to Selling Your Freelance Business or Agency. Then use A M&A Consultant's Guide to Due Diligence Checklists.

As you finalize your exit plan, pressure-test the money-movement and compliance handoffs with your legal and finance stakeholders. Then talk with Gruv to confirm fit for your operating model.

Frequently Asked Questions

When does reps and warranties insurance actually reduce escrow pressure?

It can reduce escrow pressure only when the final policy, retention structure, purchase agreement, and disclosure package all line up. Do not assume insurance automatically replaces escrow. Confirm what risk still sits with the seller, what remains excluded, and what the buyer still wants funded at closing.

What should I verify before I rely on a buyer-side policy?

Verify who pays the premium, how retention works, how exclusions are worded, and whether the underwriting draft still matches the latest acquisition agreement. Then pressure-test the handoff across broker, counsel, and finance so the policy wording and deal mechanics are describing the same risk allocation.

Does reps and warranties insurance cover known issues?

Not by default. Some market products may address narrow scenarios tied to seller knowledge, but the practical rule is to confirm the live policy wording instead of relying on a rule of thumb. If an issue was identified in diligence, decide explicitly whether it is covered, excluded, indemnified separately, or priced into the deal.

When should I keep risk in pricing, escrow, or a special indemnity instead?

Use that route when the issue is known, specifically carved out, or too material to leave ambiguous. If the policy draft, disclosure schedules, and purchase agreement do not tell one coherent story, keep the risk allocation explicit in the deal terms instead of assuming the policy will solve it later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/sites/default/files/page_file_uploads/Part-5...trusted

- connect.ncdot.gov/business/Turnpike/ProcurementsLibrary/C540%2...trusted

- dgs.ca.gov/-/media/Divisions/PD/PTCS/PAU/FISCAL-Financi...trusted

- dmv.dc.gov/sites/default/files/dc/sites/disb/publicatio...trusted

- dot.ca.gov/-/media/dot-media/programs/design/documents/...trusted

- federalregister.gov/documents/2023/04/05/2023-05767/cybersecurit...trusted

- hcpf.colorado.gov/sites/hcpf/files/Hewlett%20Packard%20MMIS%20...trusted

- hcpf.colorado.gov/sites/hcpf/files/Colorado%20Access%20Amendme...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

A Guide to Selling Your Freelance Business or Agency

**When you sell your freelance business, buyers are paying for a reliable asset they can verify, transfer, and run, not for your personal hustle.** A common mistake is mixing advice about winning clients with advice about closing an acquisition. Those are different jobs. This guide is a sellability-to-close playbook designed to reduce surprises before buyer conversations begin.

A M&A Consultant's Guide to Due Diligence Checklists

Most mergers and acquisitions fail, not in the negotiation room, but in the months after closing. The deal buckles under operational confusion, cultural friction, and liabilities that were not understood early enough. A common cause is bad due diligence, treated as a defensive box-checking exercise instead of a decision tool. That is the strategic mistake.