Quick Answer

Yes - r&d tax credits for startups can be worth claiming when you run them as a compliance workflow, not a year-end estimate. Start by testing eligibility under Section 41 at the business-component level, then build contemporaneous support that ties activities to costs and to Form 6765. If you plan to use the payroll tax path, confirm qualified small business status, election timing on the original return, and Form 8974 handling before final numbers are locked.

As a founder, you're building for the future while managing compliance risk in the present. The R&D tax credit is a common pressure point. It can be a meaningful source of non-dilutive cash, but it also comes with complex IRS rules and real documentation demands. Many startups hesitate to claim it because the rules feel unclear, the records are thin, or the audit risk is hard to judge. That often leaves you stuck on the same question: is the savings worth the risk?

This guide treats that question as an operating decision, not a marketing pitch. The goal is to turn the credit from a vague tax opportunity into a repeatable process you can evaluate, document, and file with confidence. It is not just for large companies or formal lab work. For eligible tech startups, especially those with less than $5 million in gross receipts, the credit can offset payroll taxes and improve cash flow before profitability. The key isn't optimism. It's disciplined qualification, solid records, and filing mechanics that actually hold up.

Phase 1: The "Qualify & Quantify" Framework#

Start with qualification, not spreadsheets. The material behind this section does not provide tax-authoritative eligibility rules; the only concrete reference is a 2019 public task-list page with Blogger references and SEO-oriented items, which is not a tax authority for eligibility decisions.

Use a verification grid before eligibility decisions#

If your team uses a four-part framework, treat it as a working checklist until you verify current legal definitions with primary authority or a CPA.

| Working checklist item | What you can safely conclude from this material |

|---|---|

| Eligibility standard | Unknown from current material; no tax-authoritative definition provided. |

| Technical vs business boundary | Unknown from current material; no supported boundary provided. |

| Uncertainty standard | Unknown from current material; no supported test standard provided. |

| Experimentation threshold | Unknown from current material; no supported threshold provided. |

Run this yes/no screen before tracking costs#

Before you build a claim, pressure-test these inputs. A timestamp is a useful process artifact, but it does not prove eligibility on its own.

- Do you have current, tax-authoritative support for the rule you are applying?

- Do you have internal context that matches dated checkpoints, not only retrospective summaries?

- Are you excluding public to-do pages, Blogger links, and SEO or link-building items from eligibility decisions?

- If you rely on task metadata, do you have dated checkpoints, for example an "Added" timestamp, and matching internal context?

Working triage for common startup activities#

Use this as an internal intake tool, not a filing position. It helps you separate items with verified support from items that still need facts or are likely excluded.

| Activity | Working label | Why |

|---|---|---|

| Any activity with verified tax-authoritative support | Likely qualifies | None shown in the material here. |

| Internal project work with dated records, but no verified legal standard yet | Needs facts | Documentation may exist, but eligibility rules are still unverified here. |

| SEO or link-building or content tasks from the public to-do list | Likely excluded | The material here flags these as a misclassification risk for R&D eligibility decisions. |

| Entries supported only by Blogger references | Likely excluded | The material here identifies these as non-authoritative for tax compliance decisions. |

Quantify in a safe order#

Once your qualification logic is grounded, quantify in this order. The material here does not establish rules for related-party costs, multi-entity structures, state conformity differences, or amended-return decisions, so escalate those to a CPA early.

| Step | Action | Condition |

|---|---|---|

| 1 | Confirm entity eligibility under current rules | Current thresholds still need verification before use |

| 2 | Confirm claim pathway | Confirm required forms or sequencing for your filing posture |

| 3 | Estimate cost buckets | Only after steps 1 and 2 are validated and your records are contemporaneous |

Related: A Guide to Section 1202 Qualified Small Business Stock (QSBS).

Phase 2: Build a "Compliance-by-Design" Documentation Engine#

If you want a file you can explain later, build it while the work is happening. A polished year-end memo can summarize a project, but on its own it may not provide a complete dated trail from work performed to cost records.

For startups pursuing the credit, documentation is often where a file becomes hard to review. The material here does not provide a tax-authoritative substantiation standard, so treat this section as an internal operating approach, not a legal rule.

What makes records audit-usable vs. just descriptive#

The difference is practical: descriptive files tell the story, while stronger files let a reviewer trace that story back to dated records and related costs. These are working terms, not legal definitions. Here, "contemporaneous" means records are created close to the work. "Substantiation quality" means a record captures uncertainty, options considered, what happened next, and basic who/when context with cost linkage. "Traceability" means one project can be followed across supporting artifacts without obvious gaps.

Use a quick internal self-check: pick one project and trace one technical question from the summary to dated work evidence, then to a decision or test note, then to cost records. If the trail breaks, the file is descriptive rather than truly traceable.

Use one evidence map for each project#

Use one repeatable map for each project and one consistent project ID across records. The tool matters less than consistency. If a layer does not exist, note the gap instead of creating records retroactively.

| Evidence layer | What to capture | Internal verification check |

|---|---|---|

| Task record | Work item, owner, date, and the technical issue being addressed | Date and owner align with the project timeline |

| Work artifact | Output tied to the task, such as a code change, draft, script, design, or build artifact | References the same task or project ID |

| Test or decision evidence | Test result, failed attempt, comparison, or decision note | Sequence and date fit the work history |

| Cost support tag | Internal tag that links tracked costs to the project | Cost period overlaps the work period |

This discipline can reduce reconstruction work later.

Pick one internal allocation approach and document it#

Consistency is easier to operate than ad hoc changes. The material here does not establish an accepted tax method, so use this as an internal documentation aid and confirm the filing approach with a CPA before filing. If you mix approaches, document why by team and period.

| Record reality | What to document | Main risk |

|---|---|---|

| Reliable task-level records | Data source, covered period, and inclusion/exclusion rules | Mis-tagged work can distort totals |

| Clear project assignment windows | Assignment dates, staffing list, and assignment evidence | Non-project work gets swept in |

| Incomplete records, reconstructed effort | Estimator, records reviewed, and key assumptions | Highest review risk |

Keep a minimum viable project file per project#

Keep one compact packet for each project that points to the underlying artifacts. That keeps the review focused on traceability instead of narrative polish.

- Scope memo

- Uncertainty statement

- Alternatives tested

- Experiment or decision log

- Outcome summary

- Cost support

- Current filing rule or CPA position still needs verification

Escalate early when facts are ambiguous#

Do not push through ambiguity just to keep a filing timeline. Pause and get professional review when contractor treatment is unclear, related-party work is involved, multiple entities contributed to the same project, or logs do not cleanly link work to costs. That matches the stated limit of this material: it is informational, not legal advice, and readers should seek professional advice for their specific circumstances.

For related reading, see How Independent Experts Use France's CIR Tax Credit Without Overclaiming. If you want this process to run as an operational system instead of a year-end scramble, review Gruv's docs and map the controls to your team workflow.

Phase 3: The "Claim with Confidence" Strategy#

File only when your packet can substantiate the QREs on Form 6765 and your filing mechanics are workable. In practice, that matters more than stretching for a larger estimate.

Filing readiness triage#

Use this screen before return prep begins so you can decide whether to file, clean up gaps, or escalate.

| Status | What must be true | What to do now |

|---|---|---|

| Ready to file | Project packet by business component is complete, cost-allocation memo is written, and reconciliation notes tie totals to Form 6765. If using the payroll tax election, it is planned on the original return by the due date, including extensions, and Form 8974 ownership is assigned for employment-return attachment. | Proceed to draft filing set and final review. |

| Needs cleanup | Narratives exist, but continuity breaks, for example activity-to-person mapping is incomplete, cost periods do not align, or QRE totals do not reconcile cleanly to wages, supplies, and contract research. | Fix continuity and reconciliation before filing. |

| Escalate to advisor | Complex ownership or common control, amended claim posture (including pass-through amended claims), weak documentation continuity that requires reconstruction, or related-party/multi-jurisdiction facts with unclear treatment. | Pause and involve a CPA or tax attorney before numbers are finalized. |

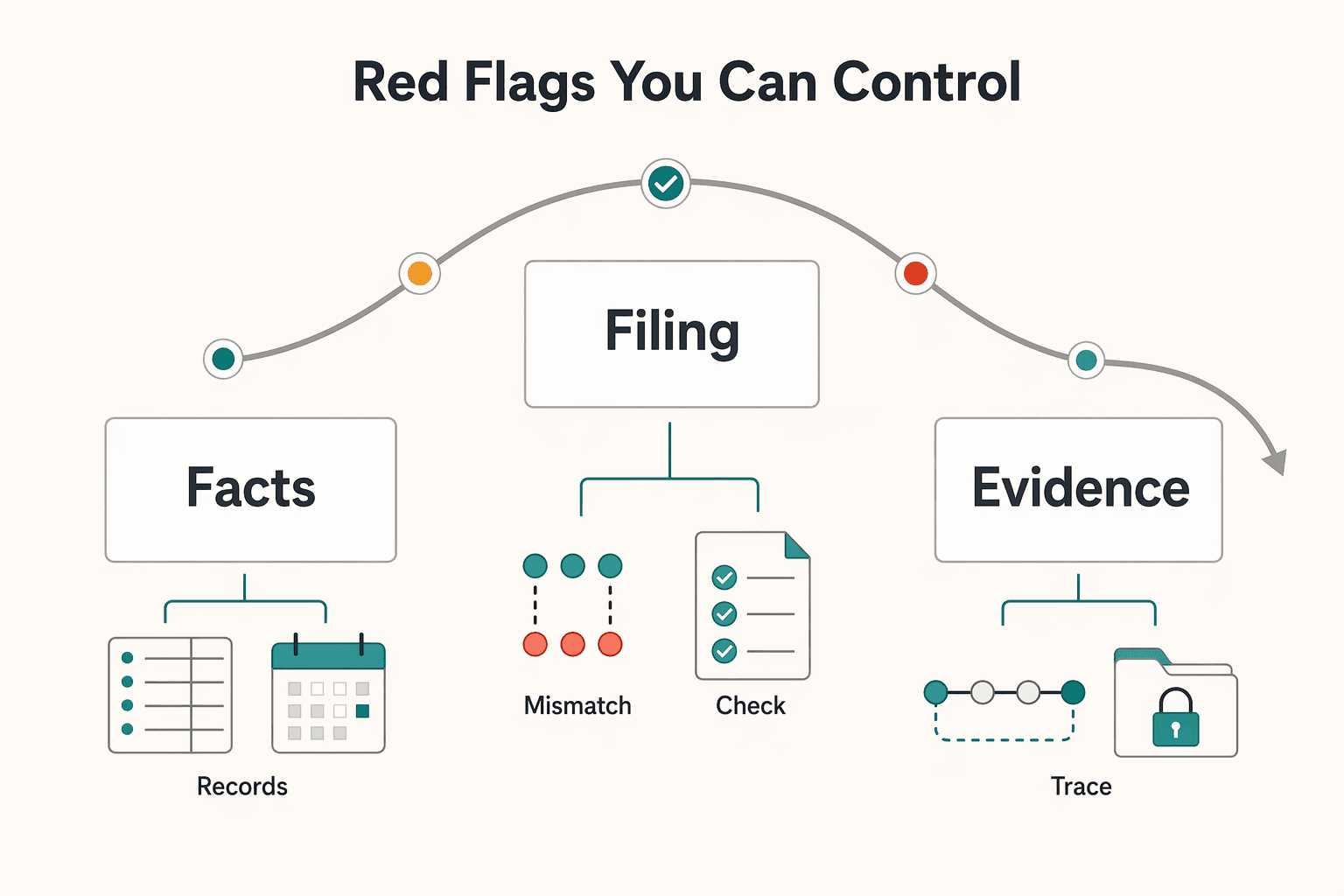

Red flags you can control#

You can't remove every tax risk, but you can eliminate the avoidable ones before filing. Focus on timing, reconciliation, and documentation continuity.

| Red flag | Prevention control | Required supporting artifact |

|---|---|---|

| QRE totals on Form 6765 are not explainable | Reconcile totals to method and source records before filing | Cost-allocation memo + reconciliation notes |

| Payroll tax election timing is unclear | Decide payroll-credit path before filing; election is not available on an amended return | Filing calendar + Form 6765 election workflow note |

| Payroll credit is claimed but employment-return workflow is undefined | Assign Form 8974 owner and attachment workflow up front | Form 8974 prep checklist + employment-return attachment note |

| Amended refund claim lacks required detail | Build packet around business components, activities, personnel mapping, and QRE categories | Amended-claim narrative set + QRE category schedule |

| Common control facts were not surfaced early | Resolve controlled-group or common-control status before final computation | Ownership chart + controlled-group attachment draft |

| Documentation continuity is weak | Trace one project end-to-end and document any gap explicitly | Evidence map + dated artifacts + gap memo |

Standardized claim packet template#

A standard packet keeps the process reviewable year after year. Use one structure every time, and add a payroll-tax sheet if you elect that path.

| Packet item | What to include | When used |

|---|---|---|

| Project narratives | By business component, including research activities and who performed them | Use one structure every time |

| Eligibility summary | Technical uncertainty and experimentation logic by component, not just novelty claims | Use one structure every time |

| Cost-allocation memo | Method, covered period, QRE categories, assumptions, and exclusions | Use one structure every time |

| Reconciliation notes | How packet totals map to Form 6765 totals; include unresolved-state notes where current rules must be confirmed | Use one structure every time |

| Payroll-tax sheet: election timing | Confirm election is made on the original return due date, including extensions | If you elect the payroll tax path |

| Payroll-tax sheet: Form 8974 workflow | Confirm Form 8974 owner and employment-return attachment workflow | If you elect the payroll tax path |

| Payroll-tax sheet: timing expectation | Credit applies beginning in the first calendar quarter after the income tax return is filed | If you elect the payroll tax path |

| Payroll-tax sheet: limits and ordering | Reflect current-year limits and ordering in instructions, including the $500,000 annual election cap for eligible years, up to $250,000 per quarter against employer Social Security tax, and then Medicare for any remaining credit | If you elect the payroll tax path |

In the reconciliation notes, label unresolved current-rule checks plainly so reviewers know which filing assumptions still need verification.

If you elect the payroll tax path, make sure the sheet covers election timing, Form 8974 ownership, expected timing, and current-year limits and ordering.

When to involve a CPA or tax attorney#

Use this checkpoint before you lock numbers. If all four checks are clean, proceed with your standardized packet and final filing review.

| Check | Trigger | Escalate when |

|---|---|---|

| Controlled group or common control | Item B on Form 6765 is potentially "yes" | Before computation or allocation is finalized |

| Amended refund claim | Includes pass-through flow-through complexity | Before filing the amended claim packet |

| Related-party or multi-jurisdiction facts | Facts materially affect claim structure and treatment is still unclear | Before final QRE totals are locked |

| Traceability | Records cannot be traced from uncertainty to activities to costs without major gaps | Before filing |

If any answer is yes or still unclear, escalate before filing rather than trying to sort it out during return prep.

Plan the cash conservatively#

Treat the credit as potential non-dilutive capital, not guaranteed cash on a fixed date. Protect runway first, then pick one contained use, for example hiring, contractor capacity, or reinvestment, once filing readiness is complete and totals are reconciled.

You might also find this useful: The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Conclusion: Transform Compliance from a Liability into Your Competitive Edge#

The main takeaway is simple: R&D tax credits for startups are a managed compliance process, not guaranteed cash. The benefit can be meaningful, but only when your Section 41 position, records, and filing steps hold up under review.

| Decision criteria | Higher-risk pattern | Stronger filing posture |

|---|---|---|

| Qualification test | Treating broad engineering work as qualifying without testing technical uncertainty and experimentation by business component | Documenting, component by component, what uncertainty existed and how alternatives were tested |

| Evidence quality | Reconstructing support late and relying on estimates | Keeping contemporaneous records that tie activities to qualified research expenses, then reconciling to Form 6765 |

| Filing mechanics | Deferring component mapping and payroll-election timing until return prep | Confirming deadlines and payroll-election fit before filing |

| Complexity triggers | Handling pass-through or common-control issues informally | Escalating early when controlled-group/common-control or refund-claim detail is involved |

What to do next:

- Confirm your eligibility logic first: verify that the work meets the technical standard under Section 41 and Treas. Reg. 1.41-4.

- Validate documentation readiness: make sure you have business-component narratives, activity records, and a clear tie from costs to Form 6765.

- Set an internal pre-filing review cadence so issues are caught while facts are still easy to verify.

If you plan to use the payroll tax election, treat timing and QSB status as hard gates. Test both the under-$5,000,000 gross-receipts condition and the 5-taxable-year lookback condition. Make the election on the originally filed return by the due date, including extensions, and file Form 8974 with the employment tax return. Do not assume a missed election can be fixed on an amended return.

Bring in a qualified CPA or tax attorney before filing when entity structure is complex, qualifying activities are unclear, or your documentation trail is weak. The strategic value is disciplined planning. Stronger compliance makes any credit you claim easier to forecast, support, and use responsibly.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

If you're ready to align tax-credit documentation with day-to-day money operations, talk to Gruv to validate fit, controls, and coverage for your setup.

Frequently Asked Questions

Do r&d tax credits for startups cover software work?

Yes, but only when the work satisfies all Section 41 tests at the business-component level, including a qualified purpose and a process of experimentation. Shipping code alone does not establish eligibility, and work after commercial production or simple reproduction of an existing component can be excluded. Practical move: create a one-page component narrative that captures the uncertainty, alternatives tested, and evidence that testing occurred.

What records matter most if the IRS asks questions later?

The key is continuity from activities to costs to what you report on Form 6765. For refund claims, IRS guidance requires business-component activity detail plus totals for qualified wages, supplies, and contract research expenses. Contemporaneous records mapped to a business component are usually easier to defend than generic summaries written after the fact, and contractor or cloud amounts need their own support instead of broad rollups. Keep a reconciliation memo that ties your packet to Form 6765 and clearly flags any items that still need verification.

Can we use the payroll tax offset instead of waiting for income tax benefit?

It depends on whether you meet the qualified small business definition and file correctly. The statute includes a gross-receipts ceiling of $5,000,000 and a no-gross-receipts-before-the-5-taxable-year-lookback condition. The election must be on an originally filed return by the due date, including extensions, and it cannot be newly made on an amended return. Practical move: confirm QSB status first, verify the current annual election cap, and assign a single Form 8974 owner; IRS currently reflects a $500,000 cap for eligible years beginning after December 31, 2022.

Do state credits follow the federal claim?

Not reliably, so treat state treatment as jurisdiction-specific until verified. California conforms to the federal ASC method as of January 1, 2025, with state modifications, while New Jersey limits defined credit terms to research conducted in-state. Practical move: validate each state program before filing, especially when payroll, contractor activity, or research execution crosses borders.

When should I talk to a CPA or tax attorney?

Escalate before filing when allocations are judgment-heavy, your structure involves multiple entities or possible controlled-group or common-control issues, you are preparing an amended claim, or your documentation trail has gaps. Also verify current Form 6765 instructions because Section G is optional for tax years beginning before 2026 and required for tax years beginning after 2025. Default move: pause filing and hand over your ownership chart, allocation memo, and evidence map for review before finalizing numbers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Section 1202 QSBS for Founders Who Need a Defensible Exit

You are managing two risks at once: building the company and protecting your personal tax outcome. With QSBS, that means running an evidence and review process from day one, not doing a one-time check and hoping it holds until exit.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.