Quick Answer

Usually, no: for a solo operator, a peo in california can introduce co-employment mechanics that conflict with direct client contracting. If you sell project-based services through your own entity, prioritize a setup where agreements, scope documents, invoices, and responsibility ownership stay consistent. A PEO can fit when you are actively building a W-2 team, but otherwise a narrower administrative arrangement is often easier to operate and defend.

The California PEO Trap: 3 Hidden Risks for the "Business-of-One"#

If you run a solo business in California, this guide starts with one practical filter: do you need an employment-style setup, or just clean direct contracting. In many cases, a broad PEO in California service is more than you need when your real objective is to contract with clients, invoice clearly, and get paid on time.

That distinction matters because paperwork tends to harden into your operating model. Once a provider, client, or internal team starts treating your work as if it belongs inside an employment framework, every later step usually follows that first choice: onboarding, approvals, insurance questions, invoice flow, tax handling, and offboarding. If that first choice was wrong, the friction shows up everywhere else.

A PEO is a third party that can take on payroll-tax functions under contract. Co-employment means the client and PEO share employer responsibilities, and neither is the employer for all purposes. An EOR is different: the provider is the legal employer while the client manages day-to-day work. AOR is often used as a contract label, so verify exactly what the provider is and is not doing.

For a business-of-one, that is where people get tripped up. A provider label can sound like a complete solution even when the underlying arrangement is narrow, partial, or just administrative. If the label sounds broader than the contract actually is, you can end up relying on a structure that does not do what you think it does.

The trap is usually not the label itself. It is the mismatch between the structure on paper and the way you actually work. In practice, that shows up in three places: your records, your deal process, and the compliance tasks that still stay with you.

Risk 1: Professional employer organization records drift from your California work model#

The first risk is documentation drift between your real business model and your paper trail. According to California AB 5 guidance, the ABC test applies to key classification questions and employee status is generally the default unless all three factors are met. If you operate as an independent business, adding a co-employment layer does not remove the need for consistent records. It makes consistency more important.

| Step | File item | What to confirm |

|---|---|---|

| 1 | Client agreement | Who is buying what |

| 2 | SOW | Scope, pricing, and deliverables match the agreement |

| 3 | Invoices | The pricing model mirrors the SOW |

| 4 | Proof that you control your tools and methods | The file shows how the work is actually performed |

| 5 | One-page responsibility map | Tax filings, reporting, workers' compensation, and payment flow are clear |

The key problem is not just whether each document is technically signed. It is whether all of the documents point to the same relationship. Your MSA may say your company is delivering a service. Your SOW may describe project-based work. Your invoice may look like vendor billing. But if a separate onboarding packet routes everything through a co-employment structure, reviewers will see two stories at once.

One story says, "this is a business buying services from another business." The other says, "this is being handled like employment admin." Even if both sets of documents exist for a reason, that tension invites questions.

A common failure point is label conflict. Your SOW describes a vendor service, but onboarding and payment are routed through a co-employment setup. That can create avoidable review cycles across legal, finance, and procurement because the documents no longer tell one clear story.

In practice, the review cycle often follows a predictable pattern. Procurement reads the SOW and treats you like a vendor. Finance sees payroll-style handling and asks why a vendor is not being paid as a vendor. Legal sees a provider layer and asks whether the underlying relationship is really direct, shared, or outsourced. Then someone asks you for a clarification call, a revised scope, a replacement invoice path, or a different onboarding route. None of that work improves the substance of the deal. It just tries to reconcile paper that should have matched from the beginning.

This is why you should think less about labels and more about traceability. If an outside reviewer opened your file cold, could they follow the relationship from start to finish without guessing? They should be able to see what you sell, who the client is, how the work is scoped, how you are paid, and which party handles which administrative tasks. If they need a long verbal explanation to connect the dots, your documentation is drifting.

A tight evidence pack helps: your MSA, SOW, scope and pricing, invoices, proof that you control your tools and methods, and a one-page responsibility map covering tax filings, reporting, workers' compensation, and payment flow. Also avoid outdated federal assumptions. The DOL NPRM announced on February 26, 2026 shows classification standards are still an active rulemaking area.

Build that pack in the same sequence a reviewer will use:

- Start with the client agreement that establishes who is buying what.

- Match the SOW to that agreement so the scope, pricing, and deliverables read like part of the same transaction.

- Make sure your invoices mirror the pricing model in the SOW instead of introducing a different payment logic.

- Add the proof that you control your tools and methods so your file shows how the work is actually performed.

- Finish with the one-page responsibility map so there is no ambiguity about administrative ownership.

That one-page map does real work. It forces you to answer operational questions before someone else asks them. Who files what? Who reports what? Who is responsible for workers' compensation? Who receives payment first? Who remits money onward, if anyone? Where does the provider sit in the flow, and where does the client sit? If you cannot answer those points in a short written format, the arrangement is probably too vague.

It also helps to check for version drift. You can sign a clean set of documents at the start and then accumulate small changes through email, portal onboarding, or updated provider terms. Six months later, the signed contract says one thing, the current payment portal says another, and the people administering the relationship are following a third practice. That is how clean structures become messy ones. Periodically compare the live process to the signed paperwork and update whichever side is no longer accurate.

Another useful check is to ask whether each document supports your business model or quietly changes it. A vendor relationship can become harder to defend when later documents start importing employer-style assumptions by habit. The point is not to resist every admin request. The point is to make sure the admin layer does not rewrite the relationship by accident.

Risk 2: Your California PEO contract does not match how you deliver services#

The second risk is deal friction when the contracting model does not match the work model. Once the paperwork starts to drift, the next problem is usually commercial friction. If a client truly wants to employ you, an EOR can fit because the provider is the legal employer. If the client is buying services from your business, inserting a PEO layer can complicate what should be a clean vendor relationship.

This is where solo operators can lose time. The issue is not always that the deal fails outright. More often, the deal slows down because each party is trying to fit the work into a different category. You think you are selling services. The client team may think they are buying contractor support through a provider. The provider may think it is helping administer an employment-style arrangement. Those differences sound small at first, but they affect who can approve the deal, what intake forms are required, how the budget is coded, and how the relationship can end.

California adds a concrete reporting obligation here. According to EDD guidance, if a business pays an independent contractor $600 or more, or enters into a contract for $600 or more, contractor information may need to be reported to EDD within 20 calendar days. Late reporting can trigger a $24 penalty per failure without good cause, and intentional failure or false reporting can increase that to $490.

That reporting point shows why a vague deal structure gets expensive. If the parties are unclear about whether the relationship is direct contracting, co-employment, or something else, people may assume someone else is handling the reporting. The result is a classic gap: the task exists, everyone vaguely expects it to be covered, and nobody has clearly owned it.

Before you sign, ask for the full paper trail: the service agreement, the client-facing agreement, the invoice or payroll flow, and the termination terms. Then reduce the whole arrangement to one plain-English sentence: who pays whom, for what, under which legal relationship. If nobody can answer that cleanly, the structure is probably doing more harm than help.

That one-sentence test exposes hidden contradictions fast. A clean answer might say that the client contracts with your business for services and pays against invoices, while a provider only supports administration. A different clean answer might say that the provider is the legal employer and the client directs daily work. Both are understandable. Trouble starts with the half-mixed answer that tries to describe a vendor relationship, an employment-style payment route, and a shared responsibility model all at once.

When you review the paper trail, pay attention to sequence as much as content. Ask yourself:

- Which agreement comes first in the logic of the deal?

- Does the client agreement assume a direct services relationship?

- Does the payment flow match that assumption?

- Do the termination terms fit the same model, or do they read like a different arrangement entirely?

Termination language is especially revealing. If the work is supposed to be a vendor engagement, but offboarding rights and process read like employment administration, that is usually a sign that the structure was not designed around your actual work model. The same is true when payment mechanics pull you into a channel that makes ordinary invoicing look exceptional.

Another friction point is internal client escalation. A frontline manager may want your services and think the provider layer is a quick solution. But once procurement, legal, finance, and compliance see the documents, they evaluate the arrangement through their own criteria. If the documents do not line up, your internal champion may no longer be able to move the deal forward without a redesign. That redesign often takes longer than using the right structure from the start.

The best move is to force comparison early. If the client wants an employment-style setup, evaluate that path directly. If the client is buying services from your business, keep the service relationship direct unless there is a clear reason not to. If your pricing model is still being debated, align your paperwork first with project-based contracting mechanics. The more the structure mixes categories, the more likely you are to spend time explaining instead of operating.

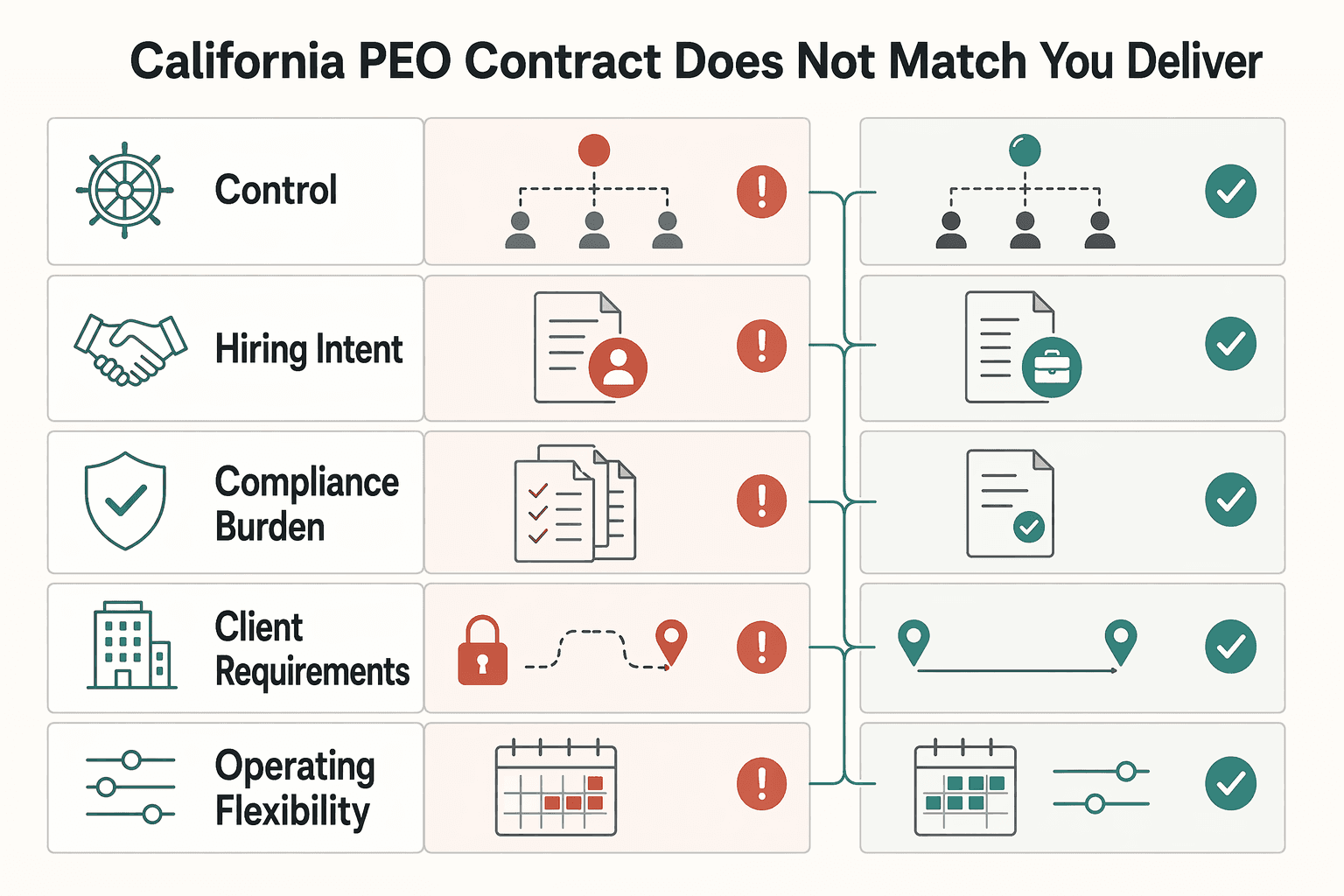

| Decision criterion | Choose a PEO when... | Choose a provider-labeled AOR service when... |

|---|---|---|

| Control of work | You accept shared-employer structure and contract-level admin controls | Contract keeps you as the service provider and limits the provider to admin support |

| Hiring intent | You plan to build or manage employees | You are not building a W-2 team and mainly need contracting/payment admin |

| Compliance burden | You want bundled HR/payroll support and can manage residual obligations | You only want specific admin help and can verify exact task ownership |

| Client requirements | Client or business model requires an employment-style setup | Client will still contract with your business directly and accepts the provider layer |

| Operating flexibility | You can trade flexibility for structure | You need a narrow layer that does not reshape the underlying relationship |

Use that comparison as a screening tool, not as a branding exercise. The question is not which label sounds simpler. The question is which structure leaves the fewest unresolved assumptions once the deal becomes real: onboarding, reporting, invoicing, approval, and exit.

Risk 3: Compliance tasks in a California PEO setup do not fully transfer#

The third risk is overestimating how much compliance responsibility is actually transferred. Do not assume that outsourcing payroll transfers the hard parts of compliance. A PEO does not automatically eliminate client-employer federal tax responsibility. The contract decides which tax tasks are handled by whom. You need explicit task allocation, not assumptions.

| Checkpoint | What to verify | Source or proof |

|---|---|---|

| Tax functions | Which tax tasks are handled by whom | Exact contract clause, workflow, or document |

| Workers' compensation coverage | What policy is being relied on and whether it is active | Policy details; WCIRB coverage inquiry tool |

| Claimed CPEO status | Whether the provider appears on the IRS public CPEO list | IRS public CPEO list |

| Payroll-tax agency need | Whether a Section 3504 agent appointment is a more precise tool than full co-employment | Form 2678 |

This can be expensive because it often feels settled when it is not. A provider may be handling a meaningful slice of administration, and that can create the impression that compliance as a whole has been moved over. But administrative involvement is not the same thing as full responsibility. If the contract allocates only certain functions, the rest still needs an owner, and that owner may still be you or your client depending on the structure.

The practical question is simple: can you point to the exact clause, workflow, or document that assigns each task? If not, the task is still at risk of being missed. For a business-of-one, that matters because there may be no internal HR or legal team catching loose ends later.

California workers' compensation is the clearest checkpoint. According to state guidance, some employers buying bundled PEO services still lacked valid workers' compensation coverage. Operating without required coverage can be a criminal offense. Penalties can reach $100,000, and enforcement can stop operations until valid proof is shown. If coverage is said to be included, verify the policy details and check records through the WCIRB coverage inquiry tool.

That workers' compensation example shows the right mindset: verify the operational fact, not just the sales language. "Included" is not enough by itself. "Covered" is not enough by itself. You need to know what policy is being relied on, whether it is active, and whether the records line up with what you were told. If proof is needed, you want to have that proof before there is a dispute, not after.

A practical way to handle this is to turn the broad idea of compliance into a short task list and assign an owner to each line. Your one-page responsibility map from Risk 1 can do that work if you keep it concrete. List the task, list the party responsible, and list what document proves it. For example, if a provider is handling a tax function, note the contract section or form that supports that. If workers' compensation is said to be included, note the policy details and verification source. If reporting remains with another party, say so directly. The point is to reduce room for assumption.

Two final checks keep this grounded. First, confirm any claimed CPEO status against the IRS public CPEO list, which is updated by the 15th day of the first month of each calendar quarter. Second, if your need is limited to payroll-tax agency, evaluate whether a Section 3504 agent appointment using Form 2678 may be a more precise tool than full co-employment.

Both checks matter because they push you toward fit instead of bundle. If a provider claims a particular status, verify it rather than relying on marketing shorthand. If your actual need is narrower than full co-employment, ask whether a narrower tool matches the problem better. A business-of-one can get into trouble by buying a large structure to solve a small administrative need, then assuming the larger structure automatically solves every adjacent issue too.

It also helps to test the arrangement against a few failure modes before you sign. If a payment is delayed, who fixes it? If a reporting question comes in, who answers it? If a client asks for proof of coverage, who produces it? If the relationship ends, who handles the final administrative steps? You do not need a long memo for each scenario. You just need enough clarity to know that the same question will not bounce among you, the client, and the provider with no clear owner.

That is the practical standard throughout this decision. Do not ask whether the arrangement sounds complete. Ask whether the responsibilities can be traced clearly enough to be carried out without confusion.

The decision is usually simpler than it first appears. If you expect to hire employees, a PEO may be a reasonable trade. If a client wants to employ you directly, evaluate an EOR path. If you sell expert services across clients through your own entity, keep the structure as direct as possible and add only the admin layer you can explain clearly on one page. For a second opinion before signing, compare your options with Gruv's PEO selection guide.

That last test is worth taking seriously. If you can explain the structure, the payment flow, the reporting ownership, and the coverage checks on one page without contradictions, the arrangement is probably matched to the work. If you cannot, the problem is not that you need more labels. The problem is that the structure has become more complicated than the business model it is supposed to support.

California PEO decision guide: FAQ for solo operators#

If you need a fast answer-first recap, use these questions to pressure-test fit before you sign anything.

Do I need a California PEO if I have zero employees right now?#

Usually no. If your business model is direct client services and you are not running payroll for staff, start with a simpler admin stack and clean contracts. You can always move to a broader setup later when you actually build a team, and keep a lighter ops flow like freelancer-friendly Merchant of Record workflows in the meantime.

Can a client require me to use its preferred provider to approve a contract?#

A client can set procurement rules, but you should still ask whether the chosen flow changes your legal relationship on paper. If the provider flow starts making your vendor engagement look like employment handling, you may need to renegotiate terms or pick a different path. If classification language is already drifting, review misclassification warning signs before final approval.

- Who is the legal contracting party?

- Who controls day-to-day methods and tools?

- Who issues payment and in what format?

- Who owns reporting and tax tasks under the written contract?

- Who can terminate the relationship and under what process?

What should I verify before relying on workers' compensation coverage in California?#

Verify policy details, active status dates, and named coverage parties in writing, then confirm against public lookup records where available. This is a pre-sign checkpoint, not a post-incident cleanup step.

When is Form 2678 enough instead of full co-employment?#

If your need is narrow payroll-tax agency support, a Section 3504 route can be a better operational fit than a broad co-employment bundle. Validate this with your advisor and contract language before implementation.

What is a practical pre-sign checklist for a California PEO decision?#

Use this guide checklist before signing, then escalate unresolved conflicts to Gruv's compliance support team:

- Confirm whether the client relationship is vendor services, employment, or co-employment.

- Tie your client agreement, SOW, and invoice flow to one consistent story.

- Assign ownership for EDD reporting, tax workflows, and coverage verification.

- Verify any claimed CPEO status on the IRS public list.

- Confirm workers' compensation records before you begin work.

- Document who owns offboarding and final payment actions.

- Escalate legal or tax ambiguity before onboarding starts.

If you want a deeper dive, read What to Do If You've Been Misclassified as an Independent Contractor. If your decision is to stay independent but reduce admin friction, review freelancer-friendly Merchant of Record workflows. If you want to pressure-test your California setup before you commit, talk to Gruv about fit and coverage.

Frequently Asked Questions

Do I need a California PEO if I have zero employees right now?

Usually no. If you are delivering direct client services and are not running payroll for staff, start with a simpler contracting and admin setup and only expand when your hiring model changes.

Can a client require me to use its preferred provider to approve a contract?

Clients can set procurement rules, but you should still verify that the required flow does not rewrite your legal relationship in ways that conflict with your vendor model.

What should I verify before relying on workers' compensation coverage in California?

Verify policy details, active dates, and covered parties in writing, then confirm through the relevant coverage records before work starts.

When is Form 2678 enough instead of full co-employment?

When the operational need is limited to payroll-tax agency support, a Section 3504 Form 2678 route may be a better fit than a full co-employment bundle, subject to advisor review and contract terms.

What is a practical pre-sign checklist for a California PEO decision?

Confirm relationship model, align contract and invoice flow, assign reporting and tax owners, verify claimed provider status, and validate workers' compensation proof before onboarding.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- dir.ca.gov/peo.htmltrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemakingtrusted

- edd.ca.gov/en/Payroll_Taxes/Independent_Contractor_Repo...trusted

- edd.ca.gov/en/Payroll_Taxes/ab-5trusted

- ftb.ca.gov/file/business/industries/worker-classificati...trusted

- irs.gov/government-entities/third-party-payer-arrang...trusted

- irs.gov/tax-professionals/certified-professional-emp...trusted

- adp.com/resources/articles-and-insights/articles/e/e...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

The Best PEO Services for Small Businesses

Many **best peo services** pages are just comparison lists. They help you spot names, but they usually do not answer which provider fits your hiring model, your risk tolerance, or how much HR admin your team can realistically absorb.