Quick Answer

Yes, pro rata rights can help you hold your ownership level, but they are usually optional and only useful if the next check fits your cash plan. Confirm the right in signed deal documents, then use your current cap table to estimate participation size in the next equity round. If that amount strains reserves, declining can be the better decision even when you still like the company.

How pro rata rights fit your capital plan#

Pro rata rights are useful only if you can afford to use them when the next round arrives. They can protect upside by letting you maintain your ownership percentage, but for a freelancer, creator, or small team, that protection can come with a cash call at exactly the wrong moment.

At a basic level, this is a right, not an obligation. If you invested early and later rounds issue new shares, your percentage ownership can shrink unless you buy your proportional share of that new issuance. That is the core dilution problem. It is not just an abstract math change. Percentage-based voting power can fall with it.

The practical trap is easy to miss when your first check was small and manageable. A follow-on decision can show up when cash is already committed elsewhere. If you treat the right as automatic upside, you can end up funding a portfolio decision with money you need elsewhere. If you ignore it, you may give up more ownership than you expected.

A simple way to think about it is this: if you own 10% of a company, or 5% after a prior round, the right can let you buy enough in the next financing to stay at roughly that same percentage. You may also see these rights described as participation rights or preemptive rights. The label matters less than the economics. Later share issuance increases the denominator, and non-participation usually means dilution.

Before you get attached to preserving your stake, verify three basics:

- your current percentage ownership from the latest cap table or investor update

- whether the signed deal documents give you an optional right to participate in later rounds

- what writing the next check would do to your available cash, not just to the investment itself

That last point is where smaller investors can get squeezed. Protecting ownership can be sensible, but not if it pushes you into a concentration bet you cannot comfortably fund. A good decision here is rarely about maximizing paper ownership at all costs. It is about knowing when preserving your position is worth the capital commitment and when passing is smarter.

The rest of this guide keeps that practical view. You will get checkpoints for deciding whether to participate, a negotiation checklist for tightening vague language before it becomes a surprise, and a verification process for terms that can vary by deal. Done well, this is not just about avoiding dilution. It is about making a cleaner capital-allocation decision when follow-on funding shows up.

For related context, see A Guide to the UK's Enterprise Investment Scheme (EIS).

What pro rata rights are and are not#

Pro rata rights are a contractual option to participate in later financing rounds so you can maintain your ownership percentage as new shares are issued.

Treat the word option literally: this right is usually optional, not a requirement to keep investing. It is a strategic choice, not an automatic commitment and not an automatic allocation on whatever terms you want.

You may also see them called participation rights or preemptive rights. The mechanism is simple: new equity rounds usually increase total shares, and if you do not participate, your ownership percentage will likely fall, with percentage-based voting power potentially falling too.

What this right is not matters just as much. It is not the same as anti-dilution protection, and it does not guarantee full access in every future round. Before relying on it, confirm your latest ownership percentage and the exact signed language that defines your follow-on participation right.

How dilution changes your stake across rounds#

Dilution is denominator math: each equity financing round issues new shares, so your ownership percentage usually falls if you do not participate. If voting follows share ownership, your practical influence can fall too, but check the actual share class and rights before treating that as automatic.

Use the simple case as your baseline. If you own 10% after Seed and the company raises a Series A, a pro rata check can let you buy enough new shares to stay at 10%. If you pass, you still hold the same shares, but they represent a smaller slice of the company.

The tradeoff is liquidity versus concentration. Exercising the right means putting fresh capital into the same company, which can tighten cash available for other opportunities. That pressure compounds when multiple portfolio companies raise in the same window.

Make the call from your balance sheet, not from attachment to the position. Confirm your current stake on the latest cap table, then estimate how much new issuance the round adds and what check size participation requires. If that check strains your operating cash buffer, pass unless the position is central to your portfolio thesis.

For a broader look at governance mechanics, read How to Appoint a Board of Directors for Your Startup.

Where pro rata terms live in your deal documents#

Treat the right as a contract check, not a memory check: confirm it in signed documents before you decide on a follow-on investment. The term sheet helps you spot scope and intent, but the enforceable language is in the final deal papers.

| Item | Role | What to check |

|---|---|---|

| Term sheet | Helps spot scope and intent | Look for language on a proportional participation right |

| Final signed agreements | Control the right in practice | Confirm the enforceable language before deciding on a follow-on investment |

| Stock purchase agreement | May contain the relevant clause | Verify the exact clause text and related sections on capitalization or pre-emption |

| Investors' rights agreement | May contain the right depending on the deal | Check whether it includes the follow-on participation right |

| Stockholders' agreement | May contain the right depending on the deal | Check whether it includes the follow-on participation right |

| Side letter | May contain investor-specific rights | Check for any investor-specific rights |

Start with a fast document pass:

- term sheet language for a proportional participation right, sometimes called participation rights or preemptive rights

- final signed agreements that control the right in practice

Depending on the deal, that language may appear in a stock purchase agreement, investors' rights agreement, stockholders' agreement, side letter, or a mix of these. If you are working from a stock purchase agreement, verify the exact clause text and related sections on capitalization or pre-emption. In one SEC-filed agreement dated September 5, 2023, a section is titled 1.2 Pre-emption Waiver and Consent, which is the kind of contract signal you want to see.

Map related rights separately#

Map pro rata rights separately from board seat, information rights, and broader shareholder rights. These rights can sit in different documents and can be subject to different conditions, so do not assume one right confirms the others.

Check SAFE impact before the priced round#

If SAFEs are outstanding, confirm how the next priced round treatment is reflected in the cap table you are using and which signed agreement governs rights after conversion. Do not rely on an old cap table snapshot when you estimate your next-round allocation.

If you need a refresher on the instrument itself, What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising? is the right background read.

Keep a one-page evidence pack#

Keep a one-page pack so you can verify your position quickly before any notice window:

- signed term sheet and final agreements

- latest capitalization table

- any side letter with investor-specific rights

- notice mechanics and response deadlines

- one contact for allocation questions

If you cannot point to the signed clause, current cap table, and deadline in under two minutes, pause before relying on the right.

Decide when to exercise and when to pass#

Decide this as a portfolio tradeoff, not an automatic yes. If writing the check would materially reduce your flexibility, passing can be the stronger move even when you like the company.

| Decision | Ownership impact | Required cash | Expected voting power | Portfolio concentration |

|---|---|---|---|---|

| Exercise | May help you hold closer to your current stake | Cash goes out now | May help preserve influence tied to ownership | Increases exposure to one company |

| Pass | You accept dilution in the round | Preserves cash for other uses | Influence may decline with a smaller relative stake | Keeps more room across your portfolio |

| Red flag and pause | Do not decide until terms are clear | Keep cash uncommitted | Voting implications are unclear until documents are clear | Avoids adding risk you cannot evaluate |

If performance looks strong but your allocation is only partial, focus first on the rights that matter most to your actual control and visibility, such as information rights or a board seat, before chasing raw percentage.

If the required check is large relative to your available capital, passing protects flexibility for other venture capital financing opportunities and for your own cash buffer.

Pause before wiring funds when share issuance terms are unclear or liquidation preference changes are ambiguous. If you cannot clearly explain what you are buying and what rights remain after the round, you are not ready to decide.

Build a capital plan before follow-on funding windows open#

Build your capital plan before any follow-on notice arrives, so the right stays a deliberate choice instead of a pressure decision. The goal is simple: protect ownership only when it fits your overall capital plan.

Keep one live allocation table that shows likely subsequent financing rounds, your estimated pro rata check, your maximum check size, and your minimum cash reserve.

| Holding | Current percentage ownership | Likely subsequent financing round | Estimated check to maintain ownership | Your max check size | Yes/no threshold |

|---|---|---|---|---|---|

| Company 1 | [fill in] | [fill in] | [fill in] | [fill in] | [fill in] |

| Company 2 | [fill in] | [fill in] | [fill in] | [fill in] | [fill in] |

| Company 3 | [fill in] | [fill in] | [fill in] | [fill in] | [fill in] |

Sequence the decision in order#

- Update your capitalization table and confirm your current percentage ownership.

- Estimate what participation would be required to stay near that ownership in the next round.

- Set a hard maximum check size.

- Pre-commit a clear yes/no rule tied to that max and your reserve.

The failure mode to avoid is treating the right as free upside. Used poorly, it can restrict flexibility, and over-allocation can create pressure in future raises.

Run one quarterly reconciliation#

Once per quarter, reconcile your current percentage ownership, remaining dry powder, and upcoming rights windows. If more than one likely round would force overlapping capital calls, tighten your limits or pass earlier.

Related reading: How to Create a Financial Forecast for a Funding Round.

Negotiate pro rata terms without boxing yourself in#

Lead with process clarity, not maximum breadth. If you are unlikely to fund every follow-on round, negotiate for terms you can actually use instead of the broadest entitlement language.

The practical outcome usually depends on exact drafting in the investors' rights agreement, stockholders' agreement, side letter agreement, or related financing documents.

Make the allocation process explicit#

If a round is oversubscribed, do not assume a default priority order. Ask the agreement to state, in plain language:

- who is eligible for participation rights (preemptive rights)

- how allocation works when demand is higher than available room

- whether any holders have priority over others

Even for a small holder, clarity matters more than broad wording. A proportional concept on paper is straightforward; conflict usually appears when multiple investors try to participate at once and the documents leave discretion open.

Ask for precision where rights often narrow#

Get explicit language on notice mechanics, transferability, and any conditions linked to information rights. Confirm what triggers notice, how notice is delivered, and whether eligibility depends on keeping other rights in good standing.

Also compare the term sheet and final financing documents line by line on these points. Misalignment here is where a broad headline right often becomes narrower in practice.

Do not negotiate for breadth you cannot fund#

Surface the tradeoff early: broad grants can add cap table pressure and reduce room for new investors in later rounds. If you write smaller checks, prioritize certainty of process over aggressive language you may not be able to exercise.

Handle country and program differences safely#

Do not assume pro rata terms work the same way across countries or program structures. Enforceability can change based on governing law, the full financing document set, and the vehicle you invest through.

These rights are often spread across multiple deal documents, including a stockholders' agreement, investors' rights agreement, side letter, or similar financing agreement. The stock purchase agreement separately sets the purchase-and-sale terms for the share transaction. Deal paper is often highly specific, so treat each clause as context-dependent, not portable.

What to verify before you rely on the right#

Before you plan around future participation, confirm local treatment of pre-emption rights and anti-dilution protection with qualified counsel in the relevant jurisdiction.

Use this minimum checklist across all signed documents:

- Governing law: Which law controls, and is it consistent across the deal set?

- Notice mechanics: How notice must be delivered, when it is deemed received, and which document controls if terms conflict.

- Transfer restrictions: Whether the right stays with the holder or can move with shares or an affiliate vehicle.

- Dispute resolution: Whether disputes go to court, arbitration, or a specific forum.

If the investors' rights agreement and side letter do not align on these points, treat that as unresolved until counsel confirms the controlling interpretation in writing.

Use cautious language in planning#

In operating notes and investor updates, describe participation as subject to signed financing documents and applicable local law, not automatic or standard.

Most failures here are operational: assumptions about notice, transferability, or forum terms break your follow-on plan when a round moves quickly. If you are investing across borders or through a program vehicle, pause and verify before you treat future allocation as available.

Related: A Freelancer's Guide to Angel Investing and Venture Capital.

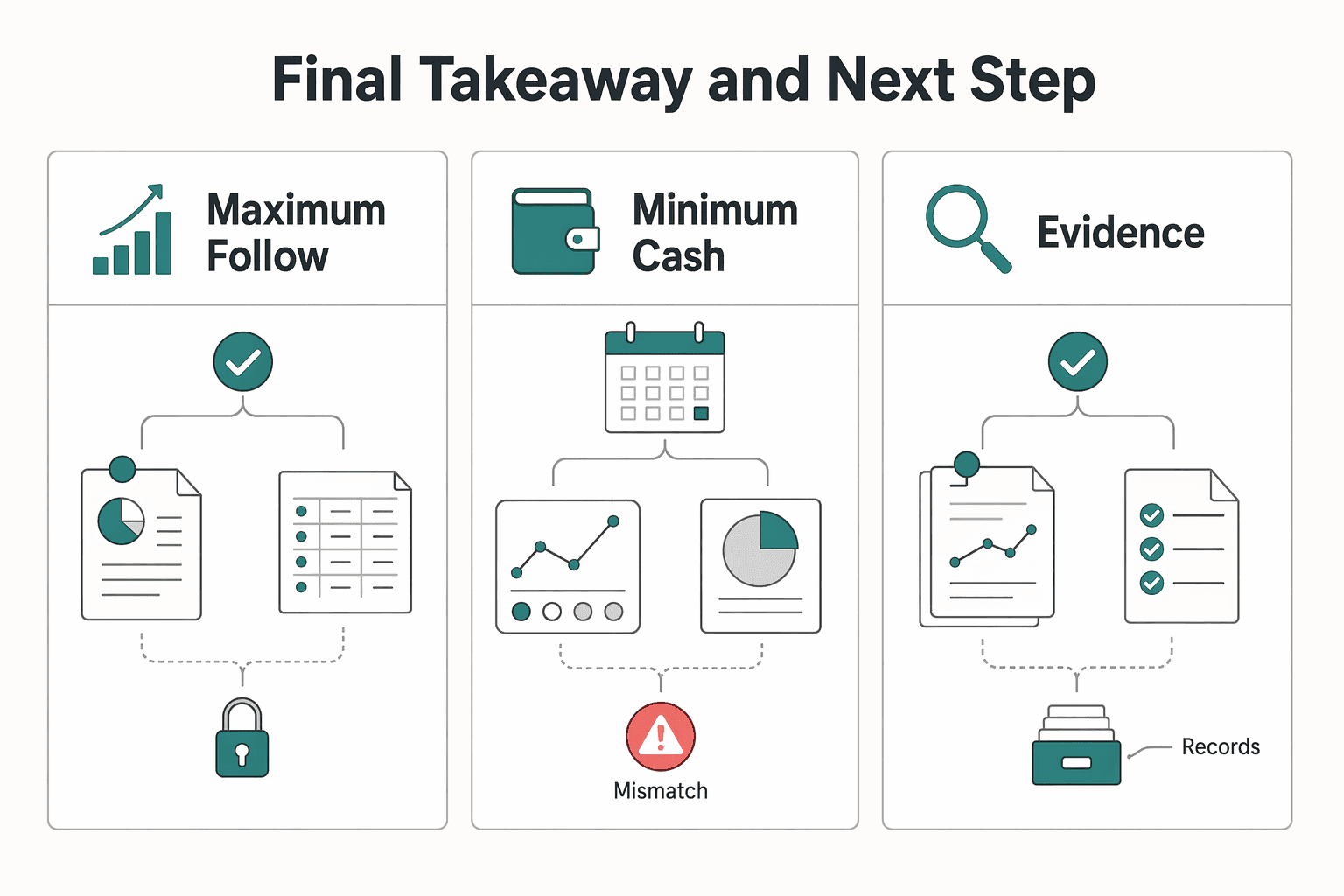

Final takeaway and next step#

Treat the right as a capital-allocation decision, not an automatic yes. Protecting your ownership only helps when each follow-on check still fits your cash plan across multiple rounds.

Used well, these rights can reward long-term conviction. Used poorly, they can restrict your flexibility and add cap table pressure by leaving less room for new investors in later rounds.

Before the next notice arrives, get your document pack ready and keep it current: the signed agreement that grants the right, your latest cap table, and the notice language with any deadlines. Your core check is simple: confirm your current fully diluted ownership, the check size required to maintain it, and the response deadline in the signed documents.

Set your thresholds before you are under time pressure, and use the same sheet every time:

- Maximum follow-on check you will write into one company

- Minimum cash reserve you will not breach

- Clear pass triggers when notice terms or allocation details are not clear in signed documents

Next step: run one quarterly review to reconcile ownership, available investment cash, and likely exercise windows, then apply the same checklist to each new follow-on decision. If documents for the next priced round are still unclear, review What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising? before you commit.

Frequently Asked Questions

What are pro rata rights in one sentence?

They are a contractual right that lets an existing investor buy a proportional share of stock in future financing rounds so they can maintain their ownership percentage. In practice, that right is usually written into an investors’ rights agreement, stockholders’ agreement, side letter agreement, or similar financing document.

How do pro rata rights prevent dilution in a new equity financing round?

Dilution happens when a company issues new shares and your ownership percentage drops because the total share count goes up. If you own 5% after a Series A, the right may let you buy up to 5% of the stock offered in the next round so your stake stays roughly in line. To estimate what that means, review your cap table and round documents for the proportional amount you are allowed to buy.

Are pro rata rights mandatory to exercise?

No. They are generally an option, not an obligation, so you can decline if the check size no longer fits your capital plan. Treat participation as a potential follow-on investment, not an automatic requirement.

Who usually receives pro rata rights in startup investing?

They are commonly requested by early-stage investors, but they are not automatic for every investor. Whether you actually have them depends on the signed financing documents, not casual deal language. If you are unsure, check the final agreement set instead of relying on the term sheet summary.

What is the difference between pro rata rights and anti-dilution protection?

They are related because both deal with dilution, but they are not the same thing. One is a participation right in a new round. The other is a separate protective concept defined by the financing terms. If those terms are used loosely in deal emails, treat that as a cue to verify the signed language.

Why would an investor decline pro rata even in a promising company?

Because keeping ownership percentage is not free. Exercising requires new capital, and you may decide the follow-on check does not fit your capital plan at that time. Passing can be rational even when you still like the company.

Why do startups agree to grant pro rata rights at all?

Usually because they want to attract investors and secure the capital those investors can provide. Offering the right can make a round more attractive to some early investors, and the scope is set in the financing documents.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- congress.gov/crs-product/R47447trusted

- ecfr.gov/current/title-12/chapter-III/subchapter-B/pa...trusted

- federalreserve.gov/publications/files/bhc-4000-201902.pdftrusted

- hhs.gov/sites/default/files/hhs-grants-policy-statem...trusted

- irs.gov/pub/irs-irbs/irb24-30.pdftrusted

- michigan.gov/-/media/Project/Websites/dtmb/Procurement/Co...trusted

- oge.gov/web/oge.nsf/0/11AF3BE8C3A7F42A85258A6200572A...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

A Freelancer's Guide to Angel Investing and Venture Capital

**Build a decision system that protects your operating cash first, then treat angel investing as an optional use of true surplus.** If you are considering angel investing as part of broader wealth building, you need controls that keep "startup investing" from quietly raiding rent, taxes, or payroll. Knowledge feels productive, but constraints keep you solvent. As the CEO of a business-of-one, your job is to protect the operating cash that keeps the machine running.

What is a SAFE (Simple Agreement for Future Equity) in Startup Fundraising?

A SAFE, short for Simple Agreement for Future Equity, is a contract where an investor gives you money now in exchange for a future ownership interest if a trigger event happens, often a later equity financing or an acquisition of the company. It usually fits an early raise when you need speed, simpler documents, and the ability to close investors one by one. It is a weaker fit when investors want negotiated control rights now, or when you need exact dilution certainty before taking money.