Quick Answer

Portugal's simplified regime in 2026 should be managed as a verified process, not a one-time setup. Confirm current rules before registration and first billing, keep contracts, invoices, payment proof, and treatment notes in one evidence trail, and review quarterly whether the structure still fits your actual clients, costs, and VAT exposure. Escalate unclear points before they reach live invoices.

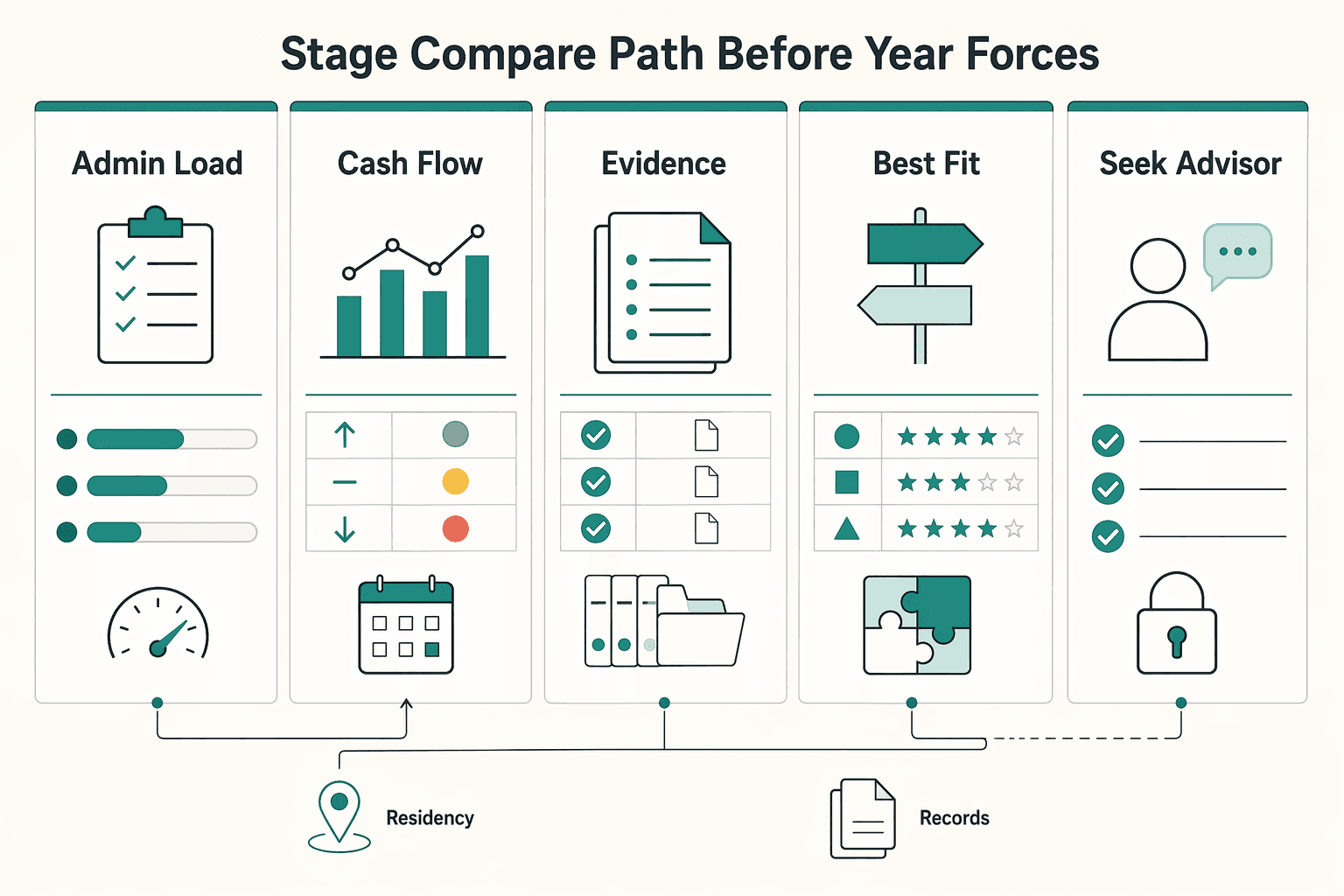

A CEO's Playbook for Portugal's Simplified Regime: Your 3-Stage Framework for Profit & Peace of Mind#

Use Portugal's simplified regime as an operating discipline, not a one-time setup. Verify live 2026 rules, document each judgment call, and escalate before uncertainty reaches your invoices.

Start with a hard filter on sources. Policy studies, yearbooks, and older blog posts may help you understand the market, but they are not authority for rates, thresholds, or eligibility. If a number drives a decision, verify the current value from Portuguese authority guidance or written advisor input before using it.

This framework is about process. It does not assert Portugal-specific rates, thresholds, or filing rules from non-authoritative material.

That sounds strict, but it is what keeps a manageable regime from becoming an expensive guessing exercise. Most problems here do not start with bad intent. They start with a copied assumption, an untested invoice template, or a casual sentence like "I think this still works the same way." Your standard should be higher than that. If you cannot point to what you verified, when you verified it, and where you stored it, the issue is not closed.

The simplest way to stay calm is to separate setup, ongoing evidence, and structure review. Each stage has a clear output. Stage 1 gives you a registration path and a first-invoice position you can explain. Stage 2 gives you a record trail that survives time, client changes, and memory gaps. Stage 3 gives you a deliberate comparison before the year pushes you into a rushed decision.

Stage 1. Get set up only when your facts are real#

Do not register on autopilot. Set up only when you can explain your registration path and first-invoice treatment in plain language.

| File | Owner | Review cadence | Keep |

|---|---|---|---|

| Registration file | You | Once before registration, again before first invoice | current guidance screenshots or PDFs; activity classification notes; written advisor input; planned billing start date |

| First-invoice file | You | Before each new client type | signed contract or SOW; invoice template; client location note; short treatment rationale |

| VAT readiness file | You or bookkeeper | Monthly | turnover tracker; domestic vs foreign revenue split; trigger note: "Confirm the current turnover threshold with the tax authority or advisor." |

At this stage, verify the registration path, invoice treatment, and baseline records before first billing. Keep watching your actual business start date, client mix, and any VAT or cross-border point that is still unclear. Escalate if you cannot justify the treatment of your first invoice or if you are relying on unverified 2024-2025 figures to make 2026 decisions.

The key word here is actual. Use actual start timing, actual clients, and actual services, not the version of the business you imagined a few months ago. A setup that made sense when you expected one domestic client may need a fresh look if your first work is for a foreign client. A setup that seemed simple when you planned one kind of service may deserve review if the work now includes a different delivery pattern, subcontractor involvement, or a billing structure you did not expect. The regime may be simplified, but your fact pattern still has to be true.

Use this test: if someone asked you why your first invoice is being treated that way, could you answer in a few lines without improvising? If not, pause before sending it. The first invoice often sets habits. If the template, treatment note, and support file are weak at the start, the same weakness usually repeats across later invoices.

Before registration, write down the basics you are relying on. Keep it short, but make it real:

- what you will do

- who you expect to bill first

- where those clients are located

- when you expect to start billing

- what still needs verification before the first invoice goes out

That short summary does two things. First, it shows whether your setup path matches reality. Second, it exposes gaps early, while you still have time to ask questions without unwinding live billing. If you need a practical intake template, use Freelance Client Onboarding Checklist.

Use the three files in the table above to keep the setup clean:

- Registration file

- First-invoice file

- VAT readiness file

Those files work best when each one answers one question. The registration file answers, "Why did I register this way?" The first-invoice file answers, "Why did I bill this client this way?" The VAT readiness file answers, "What should I be watching before a threshold or treatment issue becomes urgent?" If you let those purposes blur together, you end up with a messy folder full of documents but no decision trail.

A few practical failure modes are common at this stage:

- registering before you have confirmed which activity description or classification notes you are relying on

- using an invoice template built for a prior client without checking whether the new client is materially different

- treating cross-border work as if it were domestic because the service feels similar

- assuming a bookkeeper or advisor has confirmed something when the answer was never actually written down

- planning around stale figures because they were repeated in several secondary sources

None of those problems are dramatic on day one. They become painful later because they force you to reconstruct intent from memory. That is why written notes matter. A short note like "Client is foreign; treatment reviewed before invoice" is better than silence. A short note linked to a contract is better still.

Also be careful with timing. "I registered around then" or "I started working before I billed" may feel harmless when you are busy, but fuzzy timing creates fuzzy treatment. However, once dates are anchored, many later VAT and reporting decisions become easier to defend. Anchor your file to the real business start date and the real billing start date. If there was a delay between the two, note it. If the first invoice went out later than planned, note that too. The point is not bureaucracy for its own sake. It is being able to show a clean sequence later.

Once your setup is grounded in verified facts, the next job is to make sure the record trail stays just as clear.

Stage 2. Run light admin, but heavy evidence#

Light admin is fine, but light evidence is not. Keep one evidence pack that ties contracts, invoices, payments, and treatment notes together so you can still defend your decisions months later. Monitor classification consistency, invoice-to-bank matching, and any change in how you earn or spend. Escalate when revenue grows quickly, material costs show up, subcontractor use begins, or invoice and payment mismatches keep recurring.

| File | Owner | Review cadence | Keep |

|---|---|---|---|

| Income support | You | Monthly close | issued invoices; payment confirmations; contracts; treatment notes for non-obvious cases |

| Expense support | You | Monthly close | invoice or receipt; proof of payment; business-purpose note; mixed-use allocation note when relevant |

| Quarterly position note | You, with accountant review if needed | Quarterly | year-to-date turnover; domestic vs foreign split; VAT status; one-line check: "Does my current structure still match reality?" |

The easiest way to lose control is to let documents live in separate places with no link between them. The contract is in email, the invoice is in billing software, the payment is in the bank feed, and the reason for a judgment call is nowhere. That can feel manageable while volume is low. It stops feeling manageable the moment you need to explain one transaction from start to finish. Your evidence pack should let you follow a simple chain:

- what the client asked for

- what you agreed to deliver

- what you invoiced

- what was paid

- why you treated it the way you did

If that chain breaks at any point, fix it while the details are fresh. Do not wait until quarter-end to remember why a payment amount differed from an invoice or why one client was handled differently from another.

Maintain the three recurring support files in the table above:

- Income support

- Expense support

- Quarterly position note

For income support, consistency matters more than complexity. Name files in a way that lets you retrieve them quickly. Tie the invoice to the contract or SOW and to the payment confirmation. If a payment arrives late, partial, or combined with another amount, note it immediately rather than assuming you will remember later. If you had to make a judgment call in a non-obvious case, attach the note to that invoice while the reasoning is still clear. A simple digital filing pattern like What Is a Digital Shoebox and How to Organize It for Tax Time can help keep this consistent.

For expense support, the business-purpose note is often what keeps a weak record from becoming unusable. A receipt alone may show that you spent money. It may not show why it belonged in the business file or how you handled a mixed-use item. Keep the note brief, but specific enough that you would still understand it months later. The goal is not to narrate every purchase. The goal is to avoid a pile of receipts with no decision trail.

The quarterly position note is the file that turns recordkeeping into management. It is where you stop asking, "Did I save the documents?" and start asking, "Is the business I am running still the business this structure was built for?" A quarterly note should reveal drift quickly. Maybe domestic and foreign revenue are no longer in the mix you expected. Maybe costs that used to be minor are no longer minor. Maybe subcontractor use has started to affect how simple your operating model really is. You do not need a long memo. You need an honest one.

There are several signals that your "light admin" has become too light:

- invoices are being issued before you are sure how they should be treated

- bank receipts cannot be matched cleanly to invoices

- client types have changed, but the invoice process has not

- expenses are saved without a business-purpose note

- recurring mismatches are being explained verbally rather than documented

- the same confusion shows up more than once and never gets escalated

When that starts happening, do not tell yourself the regime is simple enough that it will probably be fine. Tighten the file immediately. Often the fix is operational, not technical. Use one folder per client, one naming convention, one place for treatment notes, one monthly close checklist, and one person who owns the final review.

Monthly close is where this discipline becomes sustainable. Meanwhile, review invoices issued, payments received, and open mismatches in the same fixed order every month. Confirm that every invoice has a support trail. Confirm that every material expense has its receipt, payment proof, and business-purpose note. Update the turnover tracker and revenue split. Add any escalation points to the quarterly note instead of carrying them in your head.

In practice, this is where you start to see whether the simplified route still fits your current facts. That is why the final stage is not a tax-year scramble. It is a scheduled comparison.

Stage 3. Compare your path before the year forces it#

Re-run your structure choice quarterly so you can change lanes before deadlines compress your options. Use the table below as a working comparison, not a one-time exercise. Because Portugal-specific thresholds, rates, and route-specific obligations are not verified here, use the table as a planning prompt to check against current guidance or advisor input, not as a statement of settled rules.

| Criteria | Freelancer under simplified route | Freelancer under organized accounting | Company route |

|---|---|---|---|

| Admin load | Often feels lightest if records stay clean | May involve more formal bookkeeping | Usually adds separate company-level records |

| Cash-flow predictability | Depends on verified tax and VAT treatment | May improve when actual costs need closer tracking | Depends on verified owner-pay, tax, and distribution design |

| Audit and evidence exposure | Still needs proof even if admin feels light | May require heavier documentation and clearer profit tracking | Usually spans both company and owner records |

| Best fit | Often reviewed for stable service work and clean invoicing | Often compared when complexity or cost tracking rises | Often compared when liability, hiring, retained earnings, or more formal operating needs become live questions |

| Seek advisor input when | Turnover threshold to confirm with the tax authority, VAT unclear, or client mix is mixed | Costs rise, books drift, or a switch may be needed | Comparing owner-pay options, adding partners, or taking larger contracts |

The point of this comparison is not to create doubt every quarter. It is to stop drift from becoming the default. It is easy to stay on the same path because changing later feels inconvenient, not because the current path still fits. A short quarterly comparison gives you a cleaner basis for deciding whether the simplified route still matches your business as it is now, not as it was when you started.

Run the comparison against your actual operating pattern. Ask:

- Is invoicing still clean and repetitive, or am I making more case-by-case treatment calls?

- Are costs still limited, or are they starting to matter enough that structure choice affects how I think about them?

- Is client geography stable, or has it become mixed enough that VAT review needs more attention?

- Am I still running a solo service model, or are hiring, subcontractors, or retained earnings becoming real operating issues?

You do not need a theoretical answer. You need a decision memo you can act on. One page is enough. State the current route, the reasons it still fits, the reasons it may not, and what needs verification before you decide to stay or change.

This stage is also where you should separate comfort from fit. A route can feel familiar and still be a poor fit for the business you are now running. A more complex route is not automatically better just because revenue or workload has grown. What matters is whether the structure matches the facts. Look at how you earn, how you spend, how predictable cash flow feels, how much evidence burden you can actually support, and where uncertainty is building.

A helpful way to use the table is to compare only the criteria creating pressure. If admin load is still low and records are clean, the simplified route may continue to work well. If you are increasingly focused on actual costs, profit tracking, or formal bookkeeping, organized accounting may deserve closer review with an advisor. If liability, hiring, retained earnings, or more formal operating needs are becoming part of the business, the company route becomes a live comparison instead of a distant possibility.

The trigger to escalate is not only a hard threshold. It is also recurring ambiguity. If you find yourself asking the same unresolved questions each quarter, that is already a sign that the current setup may be under strain. If VAT treatment is repeatedly unclear, if client mix keeps shifting, or if cost structure and operations are changing faster than your files can keep up, advisor input becomes less optional and more preventive. For EU client checks, add a repeatable verification step using How to Verify a European VAT Number Using the VIES System.

Do not wait for year-end pressure to make this call for you. Book a pre-year-end review while there is still time to act. If your decision depends on assumptions or any unverified threshold, verify those assumptions first.

Frequently Asked Questions

Can I use last year's blog figures to plan 2026?

No. Treat last year's blog figures as stale until you confirm them through current Portuguese authority guidance or written advisor input. One unverified number can distort registration, VAT readiness, escalation timing, and structure decisions.

What records matter most if I want fewer surprises later?

Keep contracts, invoices, proof of payment, client location notes, and short memos for judgment calls. The best records let you rebuild the full story of a transaction without guessing. If you cannot explain why an invoice was treated a certain way, the file is too weak.

When should I talk to a qualified tax professional?

Talk to a qualified tax professional when VAT treatment is unclear, client geography changes, costs become material, or you are comparing freelancer and company routes. Also escalate if your setup relied on older unverified content or non-tax sources. Do it before the issue reaches live billing or stays unresolved through a quarter close.

What if the rule itself seems ambiguous?

If a rule seems ambiguous, do not improvise on a live invoice. Pause, document the fact pattern, and get a written answer you can keep in your compliance file. Record who the client is, where they are located, what is being billed, which date matters, and what treatment question is unclear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- europarl.europa.eu/RegData/etudes/STUD/2025/764371/ECTI_STU%282...trusted

- europarl.europa.eu/RegData/etudes/STUD/2025/764371/ECTI_STU(202...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- taxation-customs.ec.europa.eu/system/files/2024-01/guidelines-vat-committe...trusted

- atlanticcouncil.org/wp-content/uploads/2023/03/Fostering-a-Fourt...external

- feps-europe.eu/wp-content/uploads/2026/01/Yearbook_2026.pdfexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Portugal Digital Nomad Visa Decisions That Prevent D8 Delays

Start with verification, not paperwork. In this research set, some material is useful only as EU VAT context, not as D8 instruction, and mixing those categories is one of the fastest ways to build the wrong plan. We use the same separation rule in [Global Digital Nomad Visa Index](/blog/global-digital-nomad-visa-index) comparisons.

Portugal NHR Tax Regime Decisions for 2026 Freelancers

If you are planning around Portugal NHR in 2026, start by checking which legal path actually applies to you. Public pages still mix the legacy regime with newer labels, and that overlap is enough to push people into the wrong assumptions before they file a return, issue an invoice, or set pricing for the year.