Quick Answer

Yes, media perils insurance is often necessary when you publish reported pieces, newsletters, sponsored posts, or client campaign content. Buy based on fit, not label: verify territory wording, confirm whether the form is claims-made or occurrence-based, and read exclusions for allegations like defamation or copyright infringement. Then line those terms up with your LLC contracts, and keep declarations, endorsements, and Certificate of Insurance records organized before you rely on the policy.

The Global Professional's Playbook for Media Perils Insurance#

If you publish or distribute information, your content is both your product and a source of risk. In plain terms, media perils insurance is specialized professional liability coverage for content-related claims. You may also see it called media liability insurance or E&O for media risks.

This guide is for independent professionals, including journalists, bloggers, and consultants, especially if you work across borders. It helps you decide whether to buy coverage, what to verify before you buy, and how to avoid a policy that does not match the way you actually work. Common allegations include defamation, including libel in written form and slander in spoken form, copyright infringement, and other IP disputes. If your business gathers and shares information, your exposure can look a lot like a publisher's.

The real question is not just whether you have insurance. It is whether the policy fits how you operate. Start with two checks:

- Territory wording: "Worldwide" language can still be narrowed by local regulations, licensing rules, or trade sanctions.

- Policy form: Media coverage can be claims-made or occurrence-based, and that changes whether coverage is tied mainly to when a claim is made or when an incident happened.

Here is the roadmap for the rest of the article:

- Phase 1 maps your real exposure. You finish with an inventory of what you publish, the likely allegations, and the clients or markets that raise risk.

- Phase 2 turns that map into protection choices. You finish with a practical boundary line for what contracts, business structure, and insurance each do, and where each one stops.

- Phase 3 gives you a buying standard. You finish with a checklist for wording, territory, policy form, and proof-of-insurance needs such as a Certificate of Insurance (COI), since clients may ask for one before work begins and some may decline to engage without it.

If you keep one rule in mind, let it be this: buy for your publishing reality, not the policy label. Related: A Guide to Media Liability Insurance for Content Creators.

Phase 1: Assess Your Unique "Media Threat Surface"#

Start here, not with policy forms. Document what you actually publish, deliver, or help distribute. If you cannot map assets, rights, and distribution, you cannot reliably match coverage to your real exposure.

Assess each deliverable that could be alleged to cause financial or reputational harm on its own. Focus first on high-value, client-facing work, especially anything tied to business decisions or public distribution.

Inventory the assets that create exposure#

Use four practical buckets so each risk attaches to a specific asset. Flag anything that guides a client decision, is public-facing, or is likely to be republished for closer review.

| Asset bucket | Examples | Trigger example |

|---|---|---|

| Published analysis | Whitepapers, audits, reports, or market analysis | A company alleges your analysis is false and damaging |

| Client campaign assets | Ad copy, landing pages, slogans, social posts, campaign concepts | An unlicensed image or a poorly researched slogan |

| Multimedia | Podcasts, videos, webinars, interviews, photo sets, clips | Third-party material may be unlicensed or disputed |

| Code and technical deliverables | Scripts, dashboards, datasets, prompts, embedded code, technical contributions | Work is alleged to be flawed or stolen, creating downstream consequences |

Use a short intake checklist#

Before publication or delivery, run a short intake check for each asset. You are trying to identify rights, distribution, and who might claim harm before the work goes live.

| Intake question | What to capture |

|---|---|

| What are you publishing or delivering? | Asset name, format, client, and date |

| Whose rights are involved? | Third-party text, images, code, data, logos, music, quotes, interview material, or personal information |

| Where will it be distributed? | Website, platform, client channels, markets, and expected resharing |

| Who could claim harm? | Companies, competitors, creators, platforms, interview subjects, data subjects, or clients |

For higher-stakes assets, consider keeping a clean record trail: draft, final, date, source list, approvals, and any history for client-supplied material.

Map the risk to the record#

Once you know what the asset is, pair each risk with the records you would want if someone challenged it.

| Risk type | Possible claim scenario | Possible consequence (varies) | Records that may help review |

|---|---|---|---|

| Defamation | A company alleges your published analysis is false and damaging | Operational, financial, or reputational disruption while the claim is handled | Research notes, source materials, dated drafts, review and approval history |

| Copyright or trademark | A deliverable includes unlicensed or disputed protected material | Operational disruption while disputed material is reviewed or replaced | License/permission records, receipts, attribution notes, client-supplied asset trail, version history |

| Privacy | Potential privacy or data-handling issue (confirm scope with your insurer) | Unknown until validated | Source files, review notes, publication copies, and any documented permission or handling decisions |

| Plagiarism | Potential close-copying concern (confirm scope with your insurer) | Unknown until validated | Research log, outline history, draft iterations, internal development notes |

For privacy and plagiarism, do not fill gaps with assumptions. If the risk is unclear, flag it and document your reasoning.

Verify exposure before you shop#

Before you ask for quotes, write a working exposure note with placeholders you can verify later. Use this as a decision aid, not as a damages prediction.

Current exposure note (example placeholders to verify): largest contract value potentially affected, replacement cost of disputed assets, response/review effort, and revenue potentially at risk if an asset is pulled or delayed.

Phase 1 output: a documented risk map you can carry into Phase 2, including your asset inventory, intake answers, retained records, and working exposure note. If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

Phase 2: Architect Your Multi-Layered Legal Shield#

A workable setup is a stack: entity structure, contract controls, and media liability insurance. Each layer does a different job, and each has a predictable failure mode if you rely on it alone.

Start with the entity, but know its boundary#

Use your entity to separate personal exposure from business debts, but do not treat it as immunity. For an LLC, that separation is the core function: members are generally not personally liable for the entity's debts. Just as important, know where that protection stops. The business can still be sued, and business assets can still be at risk. Your own torts can also create personal liability.

Make it usable in practice by keeping records easy to produce: filed formation documents and signed agreements showing the entity, not you personally, is the contracting party.

Use contracts to allocate risk, not to pretend risk disappears#

A good contract lets you allocate responsibility clearly. It does not stop someone from filing a claim. Review five clause groups with counsel:

| Clause group | What it addresses |

|---|---|

| Indemnity | Who compensates whom for specified losses |

| Limitation of liability | Which damages are limited or excluded, within legal limits |

| IP ownership and use rights | What is owned, what is licensed, and what use is permitted |

| Dispute handling | Whether covered disputes go to arbitration or court |

| Governing law and forum selection | Which law applies and where disputes are decided |

Keep governing law and forum selection separate in your drafting. One chooses the law. The other chooses the place or court. For IP terms, be explicit. Copyright starts with the author, and transfers require signed writing. If clients supply assets, your contract should also state what rights they grant you to use those materials.

Insurance is the funding layer#

This is the layer that can fund a legal defense when the other layers cannot. Media liability policies typically cover defense for claims like libel, slander, and defamation. Many forms also address allegations such as copyright or trademark infringement, false light, invasion of privacy, and misappropriation of name or likeness.

Check the policy form before you focus on price. Some policies are claims-made-and-reported, and some are occurrence-based. Also verify whether defense costs reduce the limit. Some forms state they can reduce and even exhaust available limits.

| Layer | Primary purpose | Failure mode if used alone | Evidence to keep |

|---|---|---|---|

| Entity (LLC) | Separate personal exposure from entity debts and obligations | The company can still be sued and its assets exposed; your own torts may still create personal exposure | Filed formation records, executed contracts naming the entity |

| Contracts | Allocate risk, define scope, and set IP/dispute rules | Claims can still be filed; unsigned IP transfer language may fail to transfer ownership | Signed MSA/SOW, indemnity and limitation clauses, signed IP transfer/license language, dispute clause text |

| Insurance | Fund defense and potentially other covered loss payments for media-related claims | It does not prevent claims; policy terms can materially narrow practical protection | Full policy, declarations, endorsements, application, carrier notices, claim-report timeline, records for challenged work |

Leave this phase with a usable setup#

Before you move to policy selection, make sure this stack will hold up in a real claim:

- Confirm formation records are current and retrievable, and that client agreements are signed in the entity's name.

- Update your contract template with counsel so indemnity, limitation, IP, dispute handling, governing law, and forum terms are intentional.

- Assemble one complete insurance file, including the policy, declarations, endorsements, and application, plus records for work most likely to be challenged so coverage review matches real exposure.

You might also find this useful: A guide to 'named perils' vs. 'all-risk' insurance policies.

Phase 3: Deploying Your Global Shield: What to Demand in a Policy#

Buy the policy wording, not the product label. By this point, you should know what you publish, where it travels, and which claims are most plausible. The task now is to confirm the policy matches that reality by reading the policy text itself.

1) Verify policy fit from clause text, not summaries#

If your work reaches clients or audiences across borders, do not rely on summary language alone. Ask your broker or insurer to show you the exact policy language that addresses:

- Allegedly false and damaging analysis

- Accidental copyright or trademark allegations in client-facing materials

- Any material limits or conditions tied to those allegation types

If they cannot point you to clause text, treat protection as unverified. Use the same rule you use for legal obligations generally: check primary text, not summaries.

2) Confirm core mechanics before comparing price#

Do not infer how coverage works from labels alone. Confirm it from the full policy text and endorsements.

| Review point | What to verify in writing |

|---|---|

| Coverage labels and trigger language | Ask where the policy text defines when and how a claim can qualify |

| Scope for your risk map | Ask where the text addresses risks tied to high-value, client-facing work |

| Optional add-ons | Ask what is included by default vs optional, with clause references |

If answers are vague, treat that as a purchase risk and ask for written responses with clause references.

3) Set limits from downside, not habit#

Set limits against your risk map, not the cheapest quote. Use three inputs:

- Largest contract exposure

- How quickly legal defense costs would strain cash flow

- How much uncovered loss your business can absorb without stalling operations

For content businesses, include allegation risk from work like potentially damaging analysis and accidental copyright or trademark issues in client-facing materials.

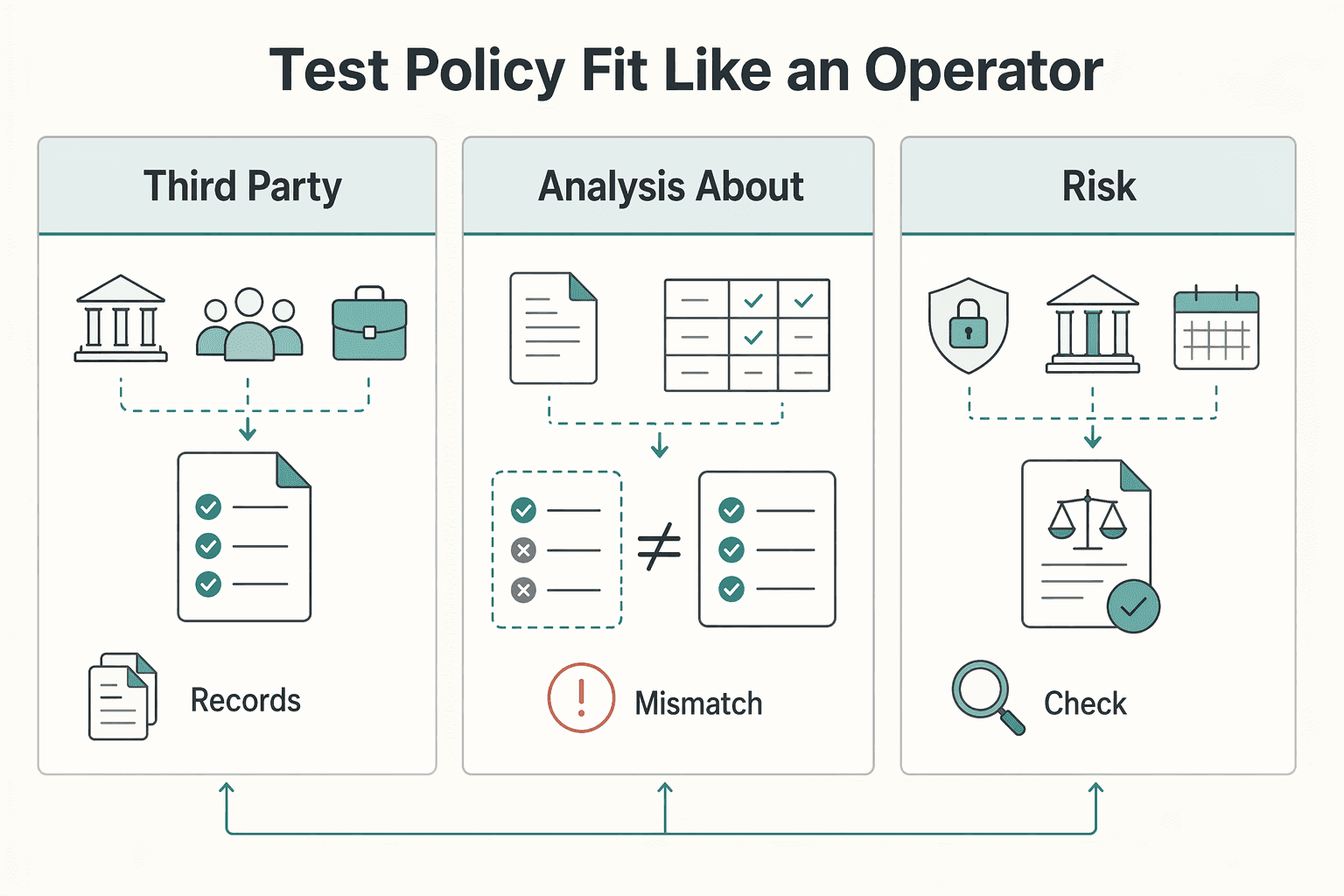

4) Test policy fit like an operator#

Policy wording varies, so review it by work pattern, then ask direct questions.

| Work pattern to test | Operational implication | What to ask your broker/insurer |

|---|---|---|

| Third-party assets in deliverables | Client-facing materials can trigger accidental IP allegations | "Show me where accidental copyright or trademark allegations are addressed." |

| Analysis about named people/companies | High-value commentary can attract allegedly false and damaging allegations | "Show me the clause text that addresses this allegation pattern." |

| Unknown-risk scenarios | Not every exposure is obvious up front | "Where does the policy text clarify what is in scope vs unverified?" |

If you operate in a regulated category, verify obligations against primary legal text. For example, the FTC Safeguards Rule applies to financial institutions under FTC jurisdiction.

Before you bind, complete this fit check:

- The full policy package and endorsements are on file.

- Answers on your highest-risk scenarios are tied to clause text.

- Your records for high-value client-facing work are organized and retrievable.

For a step-by-step walkthrough, see A Guide to Errors and Omissions (E&O) Insurance for Software Developers.

As you finalize your policy checklist, also map how claims-related records will be captured and retrieved in your payment operations. Review Gruv docs.

From Anxiety to Advantage: Your Bulletproof Business Awaits#

Your goal is not to eliminate risk. It is to keep operating when a complaint or dispute happens. The practical sequence from this guide is simple: assess your threat surface, align your legal layers, and deploy coverage with close attention to the wording that actually controls what is covered.

Start with your real output, not your job title. Inventory your actual deliverables, including reported pieces, newsletters, sponsored posts, podcasts, video clips, reposted material, and cross-border work. Then keep your LLC, contracts, and coverage aligned to that output so they do not drift apart.

That alignment matters because an LLC alone is not enough to protect company assets, and coverage can turn on precise policy language. If contracts include indemnity, usage-rights, or insurance terms, compare them against the declarations, full form, and endorsements. Full policy text may arrive late in the process, so ask for it early and review key triggers and exclusions before you rely on it.

When this setup stays current, you are generally better positioned to handle disputes and claims without unnecessary operational friction.

What you do next#

- Recheck your risk inventory when your deliverables, subject matter, channels, or client geography change.

- Review declarations, full policy form, and endorsements together, not just a summary.

- Compare contract obligations with actual coverage before signing.

- Keep policy documents, endorsements, certificates, signed contracts, permissions, corrections records, and publication approvals in one file.

- Get written clarification on unclear wording and store it with your policy records.

That is resilience in practice: steady review, aligned documents, and fewer surprises when pressure hits. For related reading, see A Guide to 'Reps and Warranties' Insurance in M&A.

If you want your operations backed by cleaner invoicing, payout tracking, and audit-ready records in one workflow, explore Gruv for freelancers.

Frequently Asked Questions

How is media liability insurance different from general liability?

They are not interchangeable. Media liability insurance, a specialized E&O form, is built for claims tied to what you publish or broadcast, including allegations like defamation, invasion of privacy, or copyright infringement. Before you buy, confirm your policy explicitly covers content-based third-party claims tied to your work. | Risk in your work | What policy is most likely relevant | Where gaps can remain | | --- | --- | --- | | Published content triggers a defamation allegation | Media liability / specialized E&O | Intentional false publication is typically excluded, and wording varies by policy | | Published content leads to a copyright claim | Media liability / specialized E&O | Coverage depends on policy wording and the specific facts | | Published content triggers a privacy complaint | Media liability / specialized E&O | Coverage depends on policy wording and the specific facts | | Non-content third-party liability issue | Policy response depends on coverage type and wording | Do not assume media liability responds |

If you already have an LLC, do you still need this coverage?

It may still be relevant if you publish work that can trigger content claims. Media liability insurance may fund defense costs and damages in a covered lawsuit, and some client contracts include liability-insurance clauses. Review contract terms and policy wording together before you sign.

Will it cover your international work?

The excerpts do not establish default international coverage. Treat this as policy-specific and verify the wording before relying on it for cross-border work.

Do you need to care whether the policy is claims-made?

The excerpts do not establish a single trigger type for all policies. Treat this as policy-specific and confirm the form and related terms in your own policy documents.

What kinds of journalist and blogger claims are most relevant?

Examples in the excerpts include defamation, invasion of privacy, and copyright infringement. Your risk can also depend on what you write about and how you write about it, so map your work to covered acts and exclusions in your policy wording.

What is commonly excluded?

Expect exclusions, not blanket protection. One common example is intentional acts, including knowingly publishing false information, as well as criminal acts. Read the exclusions section carefully against how you work.

What should you expect on cost?

Use an underwriting-input approach, not a fixed market number. Pricing can shift based on what you write about, how you write, and the insurer's view of the risk, and some applicants may be declined or quoted very high. Ask what factors drove your quote.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- app.leg.wa.gov/rcw/default.aspxtrusted

- cms.gov/files/document/medicare-drug-price-negotiati...trusted

- copyright.gov/help/faq/faq-definitions.htmltrusted

- copyright.gov/title17/92chap2.htmltrusted

- federalregister.gov/documents/2024/10/15/2024-22905/cybersecurit...trusted

- fema.gov/sites/default/files/documents/fema_pappg-v3....trusted

- ftc.gov/business-guidance/resources/ftc-safeguards-r...trusted

- hhs.gov/hipaa/for-professionals/special-topics/de-id...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Media Liability Insurance Decisions for Content Creators

If your income depends on publishing content, treat media risk as a current operating risk, not something to handle later when the business is bigger. **Media liability insurance** is a form of errors and omissions insurance focused on claims tied to content you create, publish, or distribute.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.