Quick Answer

Use a three-policy structure in Germany: Privathaftpflichtversicherung for private-life third-party claims, Berufshaftpflichtversicherung for losses tied to professional work, and Rechtsschutzversicherung to help fund disputes in insured legal areas. Confirm boundaries before purchase, since private cover excludes professional incidents and legal-expense cover is modular. Then verify wording for exclusions, territorial reach, and insured activities so each likely claim has a clear policy home.

If you live and work in Germany, the real risk is not just whether you have insurance. It is whether each policy matches the kind of claim that can hit you. A basic checklist does not help much when a private-life claim, a client loss, and a legal dispute each sit in a different place. Think of it as a three-layer defense. Each layer deals with a different problem and helps protect your assets, your work, and your ability to act when something goes wrong.

Layer 1: The Personal Shield (Privathaftpflichtversicherung)#

Start here. Privathaftpflichtversicherung is third-party private liability insurance for everyday private-life risks. It pays third-party claims if you are legally liable under statutory liability rules, up to your agreed sum insured (Deckungssumme). It can also help defend against unfounded claims. It does not cover intentional unlawful damage, motorist-caused accident liability, or business and professional incidents.

What it covers in practice#

Use it for incidents in your private sphere where you caused damage to someone else. Typical examples include accidentally damaging a neighbor's property or causing injury as a pedestrian or cyclist in private life.

A private claim can become expensive quickly, so without cover your own assets may be on the line.

Where the boundary sits#

Keep the boundary clear. This policy is for private life only. If the incident happened in client work or another professional activity, move it to Layer 2.

| Common incident | Covered by personal liability | Typical exclusion | Next policy to check |

|---|---|---|---|

| You crack a neighbor's window in a private situation | Usually yes, if you are legally liable | Intentional damage | None (core use case) |

| You injure someone while cycling privately | Often yes, subject to tariff terms and limits | Intentional unlawful act | None, unless another specific policy applies |

| You cause a car accident as the driver | No | Motor vehicle liability is separate | Motor vehicle liability |

| You damage rented rooms, fixed installations, or rented items | Often possible as Mietsachschaden, depending on tariff | Not all rented-property scenarios are covered the same way | Check personal liability wording |

| You lose a rental or building key that belongs to someone else | Sometimes, if key-loss cover is included and the key is third-party property | Own key or missing key-loss module | Check personal liability add-on |

| You lose a work office or access key | Depends on private versus professional use and own versus third-party key | Professional key risks may sit outside private cover | Professional liability or employer arrangements |

| A client claims your advice caused financial loss | No | Professional activity is outside private cover | Professional/business liability |

How to choose the right scope#

Price is a weak filter here. Start with who needs to be covered and which everyday gaps actually matter in your household.

| Factor | What to check | Article detail |

|---|---|---|

| Tariff structure | Who needs cover | single covers only you; family extends cover to additional people |

| Partner inclusion | Unmarried partner status | Check that an unmarried partner is explicitly named in the policy |

| Children | Inclusion rules | Often tied to the first uninterrupted education path |

| Sum insured | Reference points | 50 million euro total and at least 10 million euro per injured person are commonly cited reference points, not legal minimums |

| Price examples | Context only | 20 to 50 euro per year or under 5 euro per month are market signals, not guaranteed outcomes |

| Landlord proof | Contract requirement | Check what the contract actually requires before relying on assumptions |

Use that table as your shortlist, then verify the details in the actual wording before you buy.

Before you buy#

Before you buy, confirm the basics in the wording instead of assuming the tariff name tells you enough.

- Confirm the policy is explicitly for the private sphere.

- Check exclusions for self-employed or freelance activity.

- Verify whether Mietsachschaden and third-party key loss are included, and under what wording.

- Confirm your sum insured and per-person limits.

- Read territorial scope carefully, since worldwide cover duration depends on the tariff.

Once this layer is in place, keep private-life risk separate from client and project risk. If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

Layer 2: The Professional Shield (Berufshaftpflichtversicherung)#

Treat this as the work-risk layer. If a client says your service caused loss, start by checking Berufshaftpflichtversicherung before relying on private liability cover.

This policy covers self-employed professionals and companies against the financial consequences of professional mistakes. Typical triggers are losses tied to advice, delivery errors, or missed details. It also serves a defense function by handling justified claims and helping defend against unfounded ones.

Keep the policy boundary sharp#

Do not lump professional liability, operational business liability, and cyber into one bucket. They are often structured as separate components, and that is where gaps appear.

- Berufshaftpflicht focuses on service and professional liability.

- Betriebshaftpflichtversicherung focuses on liability arising from business operations.

- Cyber can be separate and may include both your own losses and third-party liability, depending on the wording.

A wrong recommendation, accidental property damage during a visit, and a data incident can all fall into different components. If you do not map those risks explicitly, you can end up with overlap in one area and no cover in another.

Also avoid blanket assumptions about legal duty. Professional liability is mandatory for some regulated professions, not universally for all freelancers, and rules can vary by profession and sometimes by state. If you work in a regulated field, verify the exact statute, chamber rule, or licensing requirement that applies to you.

Match the claim to the right component#

| Work scenario | Primary risk type | Policy component to verify | Common exclusion to check |

|---|---|---|---|

| Your advice leads to a client's financial loss | Pure financial loss | Berufshaftpflicht or Vermögensschadenhaftpflicht wording for insured activities | Activity outside insured scope, intentional unlawful act |

| You damage client property during a visit | Property damage | Betriebshaftpflicht module or combined business liability wording | Missing operational module, activity outside insured scope |

| Your code, migration, or configuration error causes downtime or data issues | Financial loss plus data-related risk | Professional liability wording plus data/privacy and cyber components | No data/privacy wording, no cyber extension, own-loss not included |

| A claim is brought abroad for work you delivered cross-border | Foreign-territory liability | Territorial scope and foreign-claims wording in the relevant liability component | Territory limits or excluded jurisdictions |

| A subcontractor you hired causes loss in your project | Subcontracting risk | Subcontractor clause and treatment of your liability from subcontracting | Cover applies to your liability only, not the subcontractor's own personal liability |

Map the policy to your real services#

Job titles are too blunt for underwriting. Buy based on the services you actually deliver, then check whether the wording follows that service list.

| Service type | Main risk | What to verify |

|---|---|---|

| Advisory | Pure financial loss | Confirm consulting, recommendations, reviews, and training are explicitly insured if part of your paid work |

| Technical delivery | Data-transfer, data-protection or electronic-data risk | Verify wording for build, migrate, configure, maintain, or access systems, plus foreign-claim handling |

| Cross-border work | Foreign claims | Check territorial scope and how foreign claims are handled |

| Data handling | Privacy breaches, transmission errors, and cyber events | Verify where these sit across professional and cyber components |

If your paid work spans more than one of these categories, make sure the wording follows the full mix rather than just your headline job title.

Buy on wording, not brochure bullets#

Brochure summaries are not enough. Base your decision on the full contract set: policy terms, Versicherungsschein, and endorsements or addenda. That wording hierarchy tells you whether the contract actually fits your work.

A practical method is to map your current service list line by line to insured activities, then test a few realistic claim scenarios against the wording. Pay close attention to territorial scope, subcontractor treatment, and post-contract reporting rules, including whether a Nachmeldefrist is actually agreed.

Buyer checklist for contract fit#

Use this as a contract-fit check before you sign.

- Confirm insured activities match what you actually sell now.

- Check territorial scope for where you work, where clients are, and where claims could be brought.

- Verify subcontractor wording, including whether cover is only for your liability or also the subcontractor's own liability.

- Check post-termination reporting exposure, and whether a contractual Nachmeldefrist exists for qualifying reporting after contract end.

- Confirm the claims workflow: how to report, what records to keep, and how defense against unfounded claims is handled.

- If the issue shifts from liability to funding a dispute, move to Layer 3. Rechtsschutzversicherung can help with legal costs, but it does not cover every dispute.

Related: Can Digital Nomads Claim the Home Office Deduction?.

Layer 3: The Legal Shield (Rechtsschutzversicherung)#

Use this layer when a dispute starts and you need the means to pursue or defend your position. It helps fund legal action so you do not abandon a case simply because the costs are too high.

It can cover statutory lawyer fees, court costs, witness compensation, and expert fees. If you lose and must reimburse the other side, that can also be covered. Out-of-court legal fees and mediation are often included, but not uniformly, so confirm this in your contract terms.

Keep one boundary in mind. Coverage only applies in the legal areas you actually insured. Policies are modular and not standardized, so a private package alone may not cover disputes tied to your self-employed work. For business disputes, confirm business and professional scope linked to your commercial activity.

Timing is the other main filter. Disputes caused before policy start (Vorvertraglichkeit) are typically excluded. Waiting periods (Wartezeit) are common, often around three months. Some terms describe them as three to six months, depending on the policy. Some cases can be exempt from waiting periods, such as certain traffic-accident or crime-victim situations, so verify the exact wording.

| Dispute type | Module to include | When coverage typically starts | What to confirm before purchase |

|---|---|---|---|

| Client does not pay your invoice or disputes your fee | Beruf (business/professional legal protection) | Usually after waiting period (often ~3 months, sometimes 3 to 6 months) | Self-employed activity is explicitly covered; contract-dispute scope; pre-contract exclusions |

| Private contract conflict | Privat | Usually after waiting period | Which private legal areas are included; whether contract disputes are included |

| Rent or landlord/neighbor conflict | Miete & Immobilien | Usually after waiting period | Tenant scope, not only owner scope; property or address limits; territorial scope |

| Traffic-related dispute | Verkehr | Sometimes immediate in specific accident-victim cases, otherwise per policy waiting rules | Covered persons and mobility situations; vehicle scope; territorial scope |

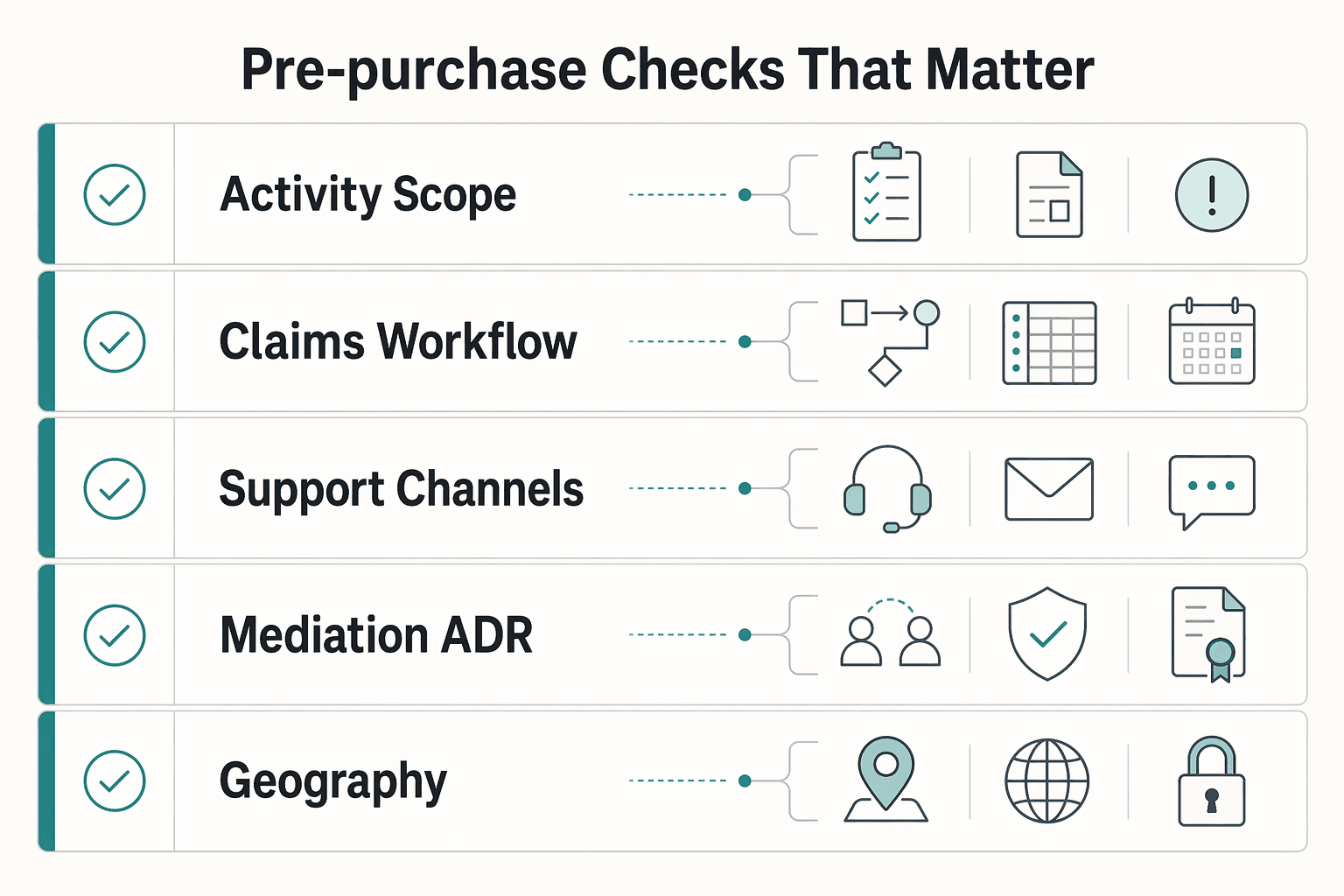

Pre-purchase checks that matter#

This cover only helps if the right module is in place before the dispute begins.

| Check | Confirm | Article note |

|---|---|---|

| Activity scope | Freelance or self-employed activity is covered, not just employee situations | The right module must be in place before the dispute begins |

| Claims workflow | Reporting step, approval step, and timing | Confirm timing and approval steps |

| Support channels | Hotline access or lawyer recommendations, and response times | Available support can include hotline access or lawyer recommendations |

| Mediation | Whether mediation is included and for which modules | Often included, but not uniformly |

| Geography | Where you live, work, travel, and face disputes | Confirm geographic applicability |

If any of those points are vague before purchase, clarify them before the dispute exists.

When a dispute has to be pursued, this layer gives you a practical way to act alongside the first two. For a step-by-step walkthrough, see Liability Insurance for Freelance IT Consultants: Do You Need It?.

Before you finalize legal-protection coverage, tighten your client terms so scope and payment disputes are clearer from day one with a freelance contract generator.

Conclusion: Build Your Fortress, Then Operate with Confidence#

Treat this as three separate policies for three separate risks. One policy does not automatically cover the others.

In Germany, Privathaftpflichtversicherung protects you as a private person against third-party claims from everyday life and helps defend against unfounded claims. It does not cover professional activity, intentional damage, or car accidents, which fall under motor vehicle liability. Use it when a private-life incident causes damage and your own assets would otherwise be exposed.

Berufshaftpflichtversicherung can cover liability risks from your professional activity, especially financial-loss claims tied to your work. It does not replace private liability or legal-expenses insurance. Turn to it when a professional error leads to a claim, and in some regulated professions proof of cover may be required.

Rechtsschutzversicherung helps pay legal-dispute costs, typically lawyer fees, court costs, and compensation for witnesses or experts. It does not cover every dispute, and waiting periods are common, often around three months. It matters when you need legal action or defense in an insured legal area. Coverage usually depends on the cause not arising before policy start or during the waiting period.

| Policy | Main purpose | Typical trigger | Primary gap if missing |

|---|---|---|---|

| Private liability | Covers private-life damage claims | You cause damage or injury in everyday private life | Personal assets remain exposed to claims |

| Professional liability | Covers work-related liability claims | A client alleges your professional activity caused financial loss | Business-related claims can hit you directly |

| Legal expenses | Helps fund legal disputes | You need legal action or defense in an insured legal area | Valid claims or defenses may be too costly to pursue |

Use three decision checks now: confirm whether your profession requires proof, assess your personal asset exposure, and assess how likely disputes are in your situation (for example, a difficult landlord context). Then follow this sequence:

- Review the policies you already hold.

- Mark gaps across private, professional, and legal-expenses cover.

- Verify scope language, exclusions, insured legal areas, and waiting periods.

- Recheck coverage every two to three years and after major life changes.

You might also find this useful: A Guide to Health Insurance for Freelancers in Germany.

Once your insurance layers are set, simplify the money side of your workflow with invoice links, payout visibility, and traceable records in Gruv's freelancer solution.

Frequently Asked Questions

What is the difference between private and professional liability insurance?

Privathaftpflichtversicherung covers damage you cause in everyday private life, while Berufshaftpflichtversicherung covers professional mistakes and negligence tied to your services. If you spill coffee on a friend's laptop, that is a private-liability situation. If a client claims your professional work caused harm, that belongs under professional liability, not private liability.

Is private liability insurance mandatory if you rent in Germany?

Private liability insurance is not generally required by law. If you are renting, check the exact lease wording before you sign rather than treating it as a universal legal rule.

How much coverage should you buy?

Buy based on your risk profile, not the cheapest tariff. Start with your household setup, asset exposure, and whether items like key loss, pet-related damage, or legal services are included by default or only as add-ons. One 2026 guide lists personal-liability sums insured from at least EUR 10 million up to EUR 50 million, but scope and exclusions matter as much as the headline limit.

Are your children covered under a family policy?

Sometimes, but you should verify this in the policy wording before relying on it. Confirm whether your partner, children, and other dependents are explicitly included, and under what conditions.

What happens if you do not have personal liability insurance?

If you cause damage that would otherwise be covered, you may have to pay for it yourself. Depending on the claim, that can still mean significant out-of-pocket costs.

What should you check before you buy?

Start with product fit: private-life incidents, professional services, and legal-expense cover are separate products. Then review exclusions, including intentional or criminal acts, motor-vehicle incidents, and optional areas like key loss or pet-related cover. Also confirm territorial scope and make sure any professional policy actually matches your freelance activity.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 7 external sources outside the trusted-domain allowlist.

- congress.gov/event/117th-congress/senate-event/LC74171/texttrusted

- allianz.de/recht-und-eigentum/privat-haftpflichtversich...external

- bafin.de/DE/Verbraucher/Versicherung/Produkte/Rechtss...external

- bafin.de/EN/Verbraucher/Versicherung/Produkte/Haftpfl...external

- buzer.de/11_VersVermV_Versicherungsvermittlungsverord...external

- dejure.org/gesetze/VVG/100.htmlexternal

- dejure.org/gesetze/VVG/103.htmlexternal

- feather-insurance.com/blog/liability-insurance-germany-guideexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.