Quick Answer

Expand a SaaS business internationally in three stages: secure the operating basics, prove one market, then automate billing and compliance before scaling. That means separate business accounts, written signing authority, day-count tracking, contract and invoice controls, a one-market micro-launch based on reachable demand, and a billing setup with clear tax, reconciliation, and pricing-display rules.

Stage 1: The Bulletproof Foundation - Fortify Your Base Before You Expand#

Before you spend on localization or outreach, lock down four unglamorous basics: your entity setup, your day-count tracker, your contract language, and your invoice controls. The exact legal and tax treatment of these items is jurisdiction-specific, so verify the details before you rely on them.

Choose a structure you can keep separate#

Start with a structure you can operate cleanly, not the one someone told you is the standard answer. The right choice depends on where you live, where you bank, how you get paid, and who will sign for the business. This week, do four things:

- Open and use separate business accounts only.

- Put signing authority in writing so client agreements are signed in the business capacity.

- Set a bookkeeping cadence now, monthly at minimum, so invoices, reimbursements, and tax records are captured while they are still easy to verify.

- Define advisor escalation triggers: adding a new billing country, changing entity footprint, hiring locally, or signing a long exclusive deal.

A common operational failure mode is mixed funds, informal signatures, and books that only get cleaned up when a bank, tax office, or buyer starts asking questions.

Track residency by travel pattern, not by guesswork#

If you travel, use a forward-looking tracker instead of rough estimates. Start with three questions: Is your home-country tax residence clearly established or already fuzzy? Are you slow-traveling in one place or rotating across several? Are you relying on any relief tied to physical presence?

For each country you may touch, keep unresolved fields for the rules you still need to verify: current tax-residency threshold pending official verification, current stay or visa limit pending official verification, and current home-country relief test pending official verification.

The day count alone is not enough. Keep a proof file that is easy to reconcile: passport scans, entry and exit records, boarding passes, accommodation records, and a calendar that matches them.

Tighten contracts and invoicing before the first foreign sale#

Do not assume a single clause removes agency or permanent-establishment risk. The goal is to avoid language and billing habits that blur who you are, what authority you have, and why tax was handled the way it was.

If EU sales are in scope, keep these VAT anchors in one place:

| Item | Requirement | Note |

|---|---|---|

| EU-wide threshold | Check whether the threshold is relevant for your supplies | EUR 10 000 |

| OSS special scheme | Register in one Member State of identification and report all supplies covered by that scheme through OSS | You still file domestic VAT returns because OSS does not replace them |

| Union and non-Union OSS returns | File returns | Quarterly |

| Import scheme | File returns | Monthly |

| Cross-border SME scheme | Check eligibility early | Union turnover must not exceed EUR 100 000 |

| Cross-border SME scheme | Complete the process requirements | Prior notification is required; selected Member States may require an EX number before exemption starts; the process should not take longer than 35 working days unless anti-evasion checks delay it |

| VAT Cross-border Rulings (CBR) | Use for complex cross-border VAT treatment questions | Advance rulings |

Separately, review the contract basics before you use any template:

| Contract area to review | What to confirm before use |

|---|---|

| Role framing | Confirm language reflects independent contractor status where appropriate |

| Authority | Confirm who can negotiate/sign and whether either party can bind the other |

| Scope | Confirm deliverables, acceptance points, and change handling are explicit |

| Term | Confirm renewal and termination mechanics are clear |

| Exclusivity | Confirm scope and carve-outs are intentionally defined |

On invoicing, set the control list before volume arrives. Validate the customer tax ID in the relevant official source. Confirm invoice wording rules for the billing country, display currency and tax treatment consistently, and retain the documents that explain why tax was or was not charged. If reverse charge applies, verify the required wording from official guidance or an adviser before you use it.

If you sell into the EU, check early whether the EUR 10 000 EU-wide threshold is relevant for your supplies and whether an OSS special scheme would simplify reporting. If you opt in, you register in one Member State of identification and report all supplies covered by that scheme through OSS. You still file domestic VAT returns because OSS does not replace them.

Union and non-Union OSS returns are quarterly, while the import scheme is monthly. If the cross-border SME scheme may fit, check eligibility early. Union turnover must not exceed EUR 100 000, a prior notification is required, selected Member States may require an EX number before exemption starts, and the process should not take longer than 35 working days unless anti-evasion checks delay it. For complex cross-border VAT treatment questions, VAT Cross-border Rulings (CBR) exist for advance rulings.

You might also find this useful: How to Choose Your First International Market for Expansion.

Stage 2: The Precision Offensive - Target and Win Your First International Market#

After Stage 1, pick one market, test it quickly, and earn the right to scale. The costly mistake is not moving slowly; it is over-localizing across multiple markets before you have proof that a specific segment will buy and activate.

Shortlist two or three markets and score each one against the same criteria. Treat this as one connected go-to-market system, not a set of isolated tactics. Define your ICP with firmographic, technographic, and behavioral criteria, because a country alone is not a segment.

Screen for demand you can reach#

Base the decision on reachable demand, not interesting demand. Before you commit budget, answer these four questions:

- Problem intensity: Are buyers already describing this problem in local search, communities, sales calls, or competitor reviews? Set a minimum evidence bar first, and keep the current benchmark pending source verification until the evidence is documented.

- Buyer readiness: Can this segment buy your product type without a long education cycle? Look for adjacent SaaS usage, implementation questions, and active vendor comparisons. If IT ownership is heavy, plan for organizational inertia and slower adoption.

- Channel accessibility: Can you reach this segment through channels you can actually run, such as paid search, LinkedIn, ABM, or network partnerships? If your only path is broad paid acquisition, treat it as high risk. With 2026 CAC pressure, loose awareness tests are usually the wrong first move.

- Compliance friction: What blocks first sale or first activation? List legal, privacy, contracting, tax, procurement, and security work, and keep setup-time and advisory-cost benchmarks pending source or adviser verification.

Keep an evidence file for each market: search screenshots, buyer interview notes, competitor pricing pages, channel-cost assumptions, and objection logs. If you cannot produce that file, you do not have a decision yet.

| Criteria | What to verify | Market A | Market B | Market C |

|---|---|---|---|---|

| Demand signal strength | Search intent, repeated buyer pain language, inbound or interview evidence | 1-5 | 1-5 | 1-5 |

| Competitive saturation | Number and sophistication of visible local alternatives | 1-5 | 1-5 | 1-5 |

| Localization effort | Product, copy, onboarding, and support changes required | 1-5 | 1-5 | 1-5 |

| Regulatory complexity | Compliance work required before first sale or first activation | 1-5 | 1-5 | 1-5 |

| Sales cycle fit | Match between segment buying motion and your current operating capacity | 1-5 | 1-5 | 1-5 |

Localize only what changes conversion#

Do not translate everything at once. Split localization into three layers and prioritize what affects conversion now.

| Layer | Includes | Priority |

|---|---|---|

| Product localization | UI text, onboarding prompts, billing emails, and help content tied to sign-up and first value | Localize activation blockers first |

| Go-to-market localization | Positioning, ads, landing pages, pricing context, and outreach | Use buyer language and pain points from that market, not home-market copy translated word-for-word |

| Trust assets | Site copy, proof points, onboarding clarity, and support expectations | Show relevant case studies and clear implementation steps; do not promise support or procurement depth you cannot sustain |

Run a micro-launch, then iterate by segment#

Use a narrow micro-launch before any broad rollout: local search intent plus targeted ads to one defined segment. Judge results at three funnel checkpoints, not clicks alone:

| Checkpoint | Measure | Target |

|---|---|---|

| Message resonance | CTR or reply rate | Current target threshold pending source verification |

| Qualified conversations | Qualified conversations | Current target threshold pending source verification |

| Activation intent | Demo follow-through, trial starts, or implementation questions | Current target threshold pending source verification |

Keep the experiment tight and change one variable at a time: audience, promise, proof, or landing page. If you use external support, avoid fee models tied only to ad spend; they can reward spend instead of outcomes while you are still learning.

Move to Stage 3 only when one market shows repeatable evidence, not a one-off spike: a named segment, a message that consistently lands, one or two channels producing qualified conversations, documented objections, and early activation intent that justifies scaling operations and compliance. For the next step, see How SaaS Teams Set Pricing and Packaging for International Markets.

Stage 3: The Resilient System - Automate Compliance and Scale Your Peace of Mind#

Once one market is working, your next risk is operational drift. Do not add countries on top of an ad hoc checkout, tax, and reporting setup. Build a billing system that keeps cross-border sales traceable, repeatable, and easy to reconcile.

Choose the billing owner first#

Decide who the merchant is before you scale anything else. In the Gruv model, a Merchant of Record (MoR) is described as handling global sales tax and VAT liability and acting as the reseller instead of a simple payment processor. Treat that as a starting assumption and verify the exact contract scope and jurisdictions.

| Area to verify | Merchant of Record | Payment processor |

|---|---|---|

| Tax and VAT liability | Often positioned as handling calculation, collection, and remittance for covered sales; verify contract scope and jurisdictions | Usually processes payment while tax setup and filings stay with you |

| Invoicing role | May issue the customer-facing invoice or receipt in a reseller flow; confirm branding, required fields, and B2B handling | Can collect payment, while invoicing often stays in your billing or finance process |

| Chargebacks and disputes | May provide dispute operations; confirm who carries economic impact and what evidence you must provide | Usually provides dispute tooling, while you often manage evidence and operational impact |

| Refunds | May execute refunds in its checkout flow; confirm approval rules, reporting, and customer communications | Can return funds, while policy decisions and accounting treatment usually stay with you |

| Compliance ownership | Can reduce cross-border compliance workload; verify exact ownership, exceptions, and exclusions | Core monitoring and exception handling generally remain with you |

If you choose an MoR, run onboarding as an operations project, not a procurement checkbox.

- Product fit: Confirm subscriptions, upgrades, downgrades, usage billing, coupons, annual deals, and any provider-specific requirements from platform records or contract terms; none should require manual workarounds.

- Supported geographies: Verify current markets, your next two target markets, supported payment methods, and buyer entity types.

- Tax handling scope: Get written confirmation of what the provider handles and what stays with you.

- Payout flow: Verify payout timing, currencies, fee deductions, and report clarity across gross, tax, fees, and net.

- Migration risk: Export customers, active subscriptions, invoices, refunds, and plan IDs before cutover so you can reverse or reconcile if needed.

- Reporting requirements: Confirm required accounting fields and whether exports map to your ledger structure.

Make pricing display match the real charge#

Your pricing rule should be explicit by buyer type and region, and it should be tested before broader rollout. The core control is simple: what you show should match the final charge pattern you intend.

| Buyer type and region | Price shown | Price charged | Control to verify |

|---|---|---|---|

| B2C, EU markets | Tax-inclusive display is commonly used; verify local rule before launch | Final charge should follow the displayed tax treatment | Screenshot and test pricing page, checkout tax line, invoice, and card charge |

| B2B, EU markets | Define whether you show net price or tax-inclusive price | Tax treatment should align with collected buyer tax details and checkout logic | Test with valid buyer tax info and confirm invoice output |

| B2C/B2B, non-EU markets | Set one clear display rule per market and buyer type | Final charge should match that local display rule | Run live checkout tests by market and archive evidence |

Do not rely on assumptions. Store test evidence by market so you can catch mismatches before paid traffic scales.

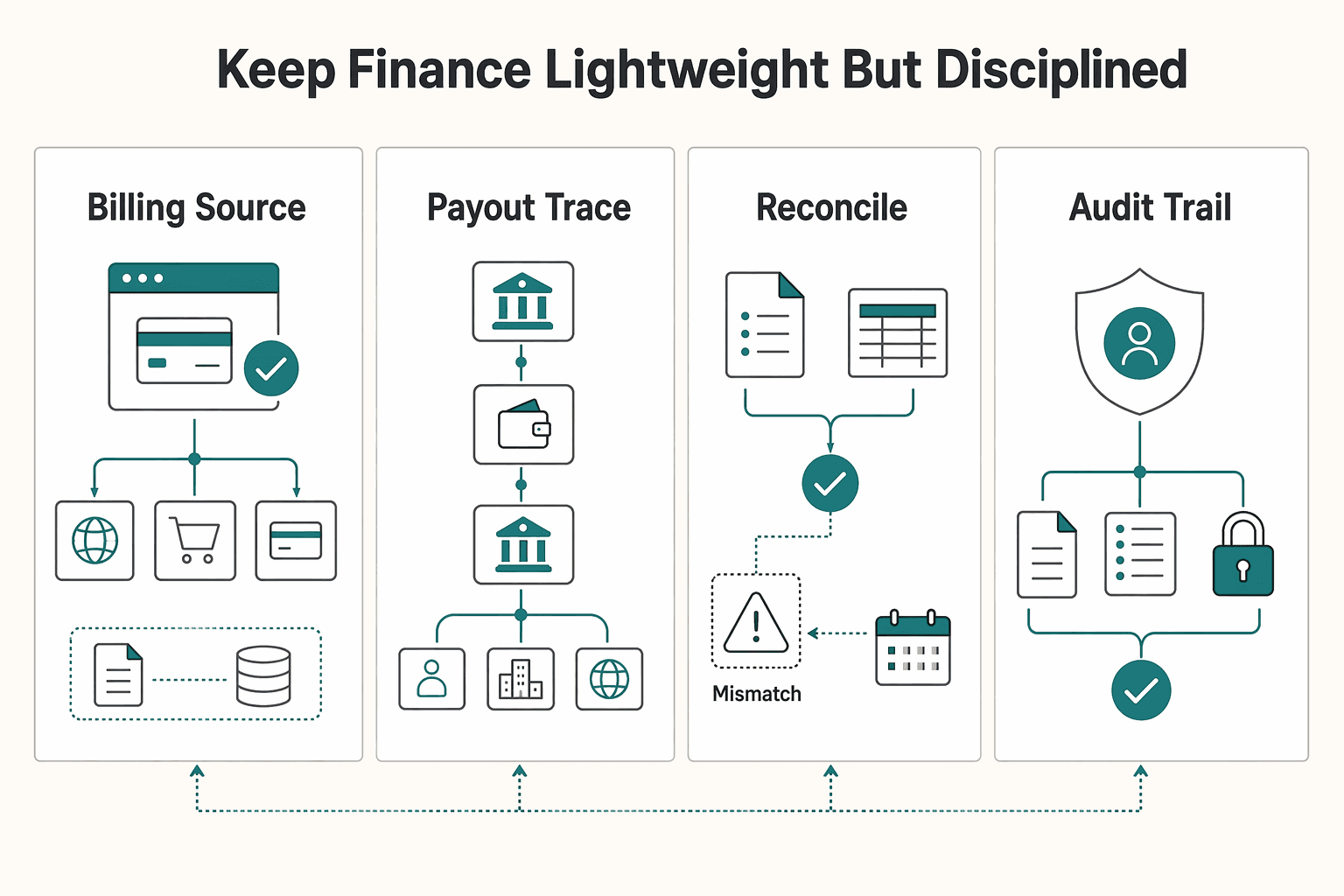

Keep finance lightweight but disciplined#

You can stay lean without losing control. Set a lightweight finance architecture with one billing source, clear ledger mapping, a defined reconciliation cadence, and one audit-trail owner.

| Minimum control | What "good enough" looks like | Likely failure mode if missing |

|---|---|---|

| Billing source | One source of final customer billing records | Duplicate subscriptions, missing invoices, revenue leakage |

| Ledger mapping | Gross sales, tax, fees, refunds, and chargebacks mapped consistently | Manual, error-prone reporting |

| Reconciliation cadence | Recurring review cadence based on transaction volume | Payout mismatches age out before you can trace them |

| Audit trail ownership | One owner for contracts, reports, invoice samples, payout statements, and exception logs | Missed deadlines and audit-time scramble |

If your pricing model evolves, use a modular orchestration layer that separates pricing logic from the payment gateway so you can change strategy without rewriting core systems. Keep API-first data flow between your CRM, ERP or accounting ledger, and payment layer so reconciliations do not depend on manual stitching.

You are ready to move from pilot to scale when test orders in each target region settle without manual fixes, your display rule matches final charges, reports reconcile on your cadence, and refunds/disputes follow a documented path. As volume rises, add continuous monitoring and automated evidence collection.

If growth still depends on side spreadsheets and memory, pause expansion until operations catch up.

If you want a deeper dive, read What is a Data Processing Agreement (DPA) and When Do You Need One?.

Conclusion: Trade Anxiety for Autonomy#

The goal here is not speed for its own sake. It is fewer compliance surprises, cleaner operations, and better decisions because you moved in the right order.

Start with the foundation. Your next action is practical: open a day-tracking spreadsheet for every country you enter and build a forward-looking travel model before you book more trips. If your plan gets close to the 183-day rule or the 90/180-day rule, or your contracts do not clearly state independent-contractor status, pause and verify the jurisdiction-specific rules before you sell more aggressively. That helps you reduce residency red lines and PE risk before late-stage remediation gets expensive.

Then validate the market, not your hopes. Pick one target market, check local search intent, and run small micro-ad tests before you commit to broader localization or in-country spend. If the proof is weak, do not explain it away. Set your traction benchmark from the saved source data, keep the test data, and make the next decision from evidence rather than enthusiasm.

Scale operations only after reporting is reliable. Cross-border growth increases audit risk, and thresholds can be crossed without a clear internal signal. If you notice compliance issues late, remediation usually gets more expensive. Before you add countries, verify that your billing and tax setup gives you timely visibility, and avoid piling on disconnected tools that can make finance and compliance harder to reconcile. Use this quick readiness check before expanding further:

- Legal structure clarity: day tracking in place, travel model updated, contract language reviewed, jurisdiction thresholds documented from official or adviser records

- Market proof quality: localized demand research saved, micro-ad results documented, one market chosen for the next test

- Compliance reliability: billing and tax reporting reviewed, tax obligations visible early, exceptions handled in a repeatable way

If an edge case still feels fuzzy, go back to the FAQ. If the decision turns on a specific country, contract, or filing obligation, get advisor review before you scale it.

For a step-by-step walkthrough, see How to Build a 'Glocal' Marketing Strategy for Your SaaS Product.

Frequently Asked Questions

Is a Merchant of Record just another payment processor?

Not necessarily. A Merchant of Record can be a different operating model, not just a different checkout button. Compare contract scope, reporting, and exception handling, and ask for sample invoices, payout reports, refund exports, and clear ownership answers before you cut over. If the contract language is vague, get legal or tax review before you cut over.

How do I reduce Permanent Establishment risk as a consultant or founder?

Use a market-by-market approach because legal and tax thresholds are jurisdiction dependent. Research each target market, review the local regulatory environment, document your operating model and contract terms, and get jurisdiction-specific legal and tax advice. If the position in a country is unclear, state that uncertainty explicitly and verify it before launch.

What is the difference between internationalization and localization in SaaS?

Internationalization prepares a SaaS product for global launch beyond a single-language setup. Localization is the market-specific adaptation you do after that. A practical sequence is to internationalize first, then localize for each target market.

How should I handle pricing display in Europe?

Do not use one Europe-wide assumption. Verify pricing display market by market because countries can differ materially in regulation, language, and culture. Check local display rules, checkout tax calculation, refund treatment, tax ID collection, invoice fields, and when tax appears for the buyer type you serve.

Do I need a foreign bank account to sell in another country?

Not always. This article does not provide country-specific banking requirements, so treat banking as a market-entry and compliance decision that must be verified per country. Research the market, review the regulatory environment, and confirm requirements with local legal, tax, and banking advisors before launch.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- gruv.ai/blog/a-guide-to-international-expansion-for-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

SaaS Internationalization for Teams That Need Launch Control

**You do not get orderly global growth by translating strings faster. You get it by treating saas internationalization as an operating discipline with named owners, launch gates, and documented stop conditions.** This tends to become true once you move past 1-2 languages or start shipping weekly updates across multiple markets. At that point, localization behaves more like infrastructure: invisible when it works and expensive when you ignore it.

When Freelancers Need a Data Processing Agreement and What to Redline First

Start with one decision before kickoff: if you will touch client personal data on client instructions, settle the DPA before anyone gets live access.