Quick Answer

Yes. Choose it only if your Indonesia Second Home Visa plan is fully documented before filing: exact E33 terms, your work-activity boundary, and a tax model for the 183-day trigger. Treat the two 90-day clocks as non-negotiable: visa use after issue and commitment reporting after entry. If your file still has unresolved points on the US$130,000 bank route or US$1,000,000 property route, pause and verify with immigration and licensed advisers before transferring funds.

Beyond the Brochure: Is This a Smart Move or a Compliance Trap?#

Treat this as a go/no-go business decision, not a lifestyle pitch. There may be upside in a longer-stay base, but only if you verify the operating rules before you commit money, contracts, and relocation timing. Your risk check comes down to three definitions:

- Remote-work permission scope: what the official visa terms clearly allow, prohibit, or leave unstated about your actual work activity.

- Tax residency exposure: when your presence, income pattern, or business setup could trigger local filing or tax obligations.

- Proof-of-funds capital lock-in: whether funds must be placed to qualify, plus the verified terms for amount, location, hold period, release, and currency or repatriation risk.

If any one of these is unclear, you are not ready to apply. Use the table below to pressure-test the move before you spend anything.

| What you gain | What can go wrong | What to verify before applying |

|---|---|---|

| Potentially more stability than short, repeatedly renewed stays, if terms are confirmed | You assume your client work is permitted when the rule is unclear | Current official visa text and any explicit work limits |

| Better planning visibility once current rules are verified | You create filing or tax exposure you did not model | Current tax-residency trigger pending official and adviser verification; confirm filing scope with a qualified adviser |

| A route that may fit applicants comfortable with potential capital commitments | Your qualifying capital becomes hard to unwind on exit | Current threshold, placement, hold, release, and transfer terms pending official verification |

Use two early safeguards. First, verify rules against current official sources. Second, build a decision file before any transfer or booking: funds evidence, account records, contract structure, client geography, and your written risk assumptions. Phase 1 is where you decide fit, compare alternatives, and set hard stop/go criteria before you spend or relocate.

You might also find this useful: Tax Residency in Indonesia: A Guide for Bali's Digital Nomads.

Phase 1: Strategic Assessment - Is This Visa Right for Your Business-of-One?#

Use this as a go/no-go filter. If you cannot verify the core rules in current official sources, treat this route as not ready.

That caution matters because the evidence gap is real. Verify current visa-rule text directly with the Indonesian Directorate General of Immigration before inferring legal rights, tax outcomes, capital requirements, or residency progression from this section alone.

Define the four decision terms first#

- Tax residency exposure: risk that your presence, income pattern, business setup, or family footprint creates local filing or payment obligations.

Current Indonesian trigger: pending verification from official tax records and a qualified adviser before use.

- Remote-work permission scope: what is clearly allowed, prohibited, or unstated for your real work activities.

Official boundary for your activity mix: pending verification from current visa records and qualified immigration advice before use.

- Capital lock-in: funds or assets required to qualify, plus amount, placement, hold period, release, and transfer mechanics.

Current placement, hold, release, and transfer terms: pending official verification before use.

- Long-term residency pathway: what can renew, convert, or progress after the initial grant, and under what conditions.

Current pathway terms: pending official verification before use.

Decision table (fill only with verified current rules)#

| Option on your shortlist | Work permission clarity | Tax treatment model | Capital commitment type | Residency trajectory |

|---|---|---|---|---|

| Indonesia Second Home route | Work permission clarity pending official verification | Tax treatment model pending qualified tax verification | Capital commitment terms pending official verification | Residency trajectory pending official verification |

| Alternative long-stay visa (other jurisdiction) | Work permission clarity pending official verification | Tax treatment model pending qualified tax verification | Capital commitment terms pending official verification | Residency trajectory pending official verification |

| Remote-work-specific visa (elsewhere) | Work permission clarity pending official verification | Tax treatment model pending qualified tax verification | Capital commitment terms pending official verification | Residency trajectory pending official verification |

If you cannot complete every cell with a current source and date, pause before any transfer, lease, or booking. Close those gaps before you lock in a move.

Profile-fit checklist (practical go/no-go)#

This route only makes sense if your day-to-day operating model still works after the move and after any commitments you verify.

- Client geography: Does your client mix and meeting cadence still work from your likely base?

- Business model: Have you mapped your actual monthly activities, including invoicing, delivery, contracting, and management, to verified permission language?

- Liquidity needs: Can you protect your operating buffer if qualifying capital is required?

- Family plans: Are family or dependent rules and timing verified early enough to avoid relocation delays?

- Timeline horizon: Does your stay horizon match verified renewal or progression rules, not assumptions?

Before committing funds, keep a one-page decision file: dated official pages, adviser notes, client-country mix, expected days on the ground, liquidity snapshot, and unverified assumptions.

Fit outcomes by archetype#

With the current evidence gap, archetype outcomes are unknown until you verify current official rules.

| Archetype | Outcome | Why |

|---|---|---|

| Any archetype | Unknown from current evidence | Confirm fit with the relevant immigration authority. |

Bottom line: your biggest risk in Phase 1 is not choosing between visas. It is committing before the rules are verified. Related: How to Write Compelling Case Studies for Your Portfolio.

Phase 2: The Compliance Gauntlet - De-Risking Your Finances and Remote Work#

Before you move money or travel, verify three items in writing: your proof-of-funds commitment, your exact work-activity permissions, and your tax-status trigger. In this phase, your job is to build an evidence file that matches your real operating model.

Verify the funds commitment before you transfer anything#

Your first control point is the commitment deadline and format. The cited Second Home eVisa FAQ says the commitment must be completed within 90 days after arrival. One listed route is a US$130,000 deposit in your name at a state-owned bank. The same page also lists a US$1,000,000 property route, while a 2022 immigration press release states a Rp2,000,000,000 proof-of-fund baseline. Reconcile any mismatch before sending funds.

| Item | Figure or timing | Source |

|---|---|---|

| Commitment completion | 90 days after arrival | Cited Second Home eVisa FAQ |

| Bank deposit route | US$130,000 deposit in your name at a state-owned bank | Cited Second Home eVisa FAQ |

| Property route | US$1,000,000 property route | Cited Second Home eVisa FAQ |

| Proof-of-fund baseline | Rp2,000,000,000 | 2022 immigration press release |

| Visa use window | 90 days from issue | Cited eVisa FAQ |

For planning, treat proof-of-funds lock-in as whatever may need to stay in place to support your status. The sources here support amounts and timing, but they do not confirm current withdrawal mechanics, minimum-balance handling, or downstream consequences if funds move.

Define your repatriation pathway as the documented process for moving funds out later. Confirm required documents, approval path, and operational steps in writing with the bank and immigration before transfer.

Also manage timing risk explicitly. The cited eVisa FAQ says the visa must be used within 90 days from issue, so you are managing two clocks: entry validity and post-arrival commitment completion.

Audit your work model against the local-employment boundary#

Do not assume one universal work rule applies across all Second Home-related permits. A dependent or family-related Second Home page states holders are "Prohibited from working in employment relationship." The cited Second Home eVisa FAQ uses different wording and says holders may "Work in Indonesia if eligible (meet the conditions of multiple residence permit activities)." Confirm the exact visa code and activity permissions on your own approval before you rely on either statement.

| Work factor | Question | Key distinction |

|---|---|---|

| Client location | Are clients and delivery fully outside Indonesia, or do you have Indonesian counterparties or local delivery? | Outside Indonesia vs Indonesian counterparties or local delivery |

| Invoicing flow | Which entity invoices, which account receives funds, and does any Indonesian entity pay you? | Invoicing entity, receiving account, and any Indonesian payer |

| Contract wording | Do contracts clearly state service scope, responsible entity, and where performance is treated as occurring? | Service scope, responsible entity, and where performance is treated as occurring |

| Decision authority | Are you doing preparatory support, or are you negotiating or signing contracts and directing core revenue activity from Indonesia? | Preparatory support vs negotiating, signing, and directing core revenue activity from Indonesia |

Use those four questions to audit your real work pattern, not just the label "remote work."

Define permanent establishment (PE/BUT) risk as the chance your activity creates a taxable business presence in Indonesia. DGT corporate-subject guidance includes examples such as a dependent agent and a service-duration trigger of more than 60 days in 12 months. Treaty rules may change PE tests. If your facts are mixed, do treaty analysis early rather than assuming a single domestic rule controls.

Decide your tax position before you land#

Model your tax status before arrival, not after. DGT states a foreign citizen is treated as a domestic tax subject when they stay more than 183 days within 12 months, and the days do not need to be consecutive.

Define tax residency status as the point where your filing position can change based on day count and facts. The same DGT article indicates that domestic taxpayer scope can include income from Indonesia or outside Indonesia, subject to its threshold condition.

Escalate before arrival if any of these apply: you may approach the 183-day line, you operate through a foreign company, you could have Indonesian-source income through PE/BUT, or you expect treaty relief. Treaty outcomes are fact-specific. The DGT withholding workflow references Certificate of Domicile documentation for non-resident treatment, and DGT also lists PER-23/PJ/2025 (09-12-2025) on domestic or foreign tax-subject determination.

| Risk area | Why it matters | What evidence to keep | Who to confirm with |

|---|---|---|---|

| Funds commitment | Missed timing or unclear commitment handling may create compliance risk | Dated eVisa FAQ PDF, visa issue date, entry record, bank letter, transfer receipt | Immigration and the specific state-owned bank |

| Repatriation pathway | Operational gaps can make future fund movement uncertain | Written bank process note, required-document checklist, approval-contact log | The same state-owned bank and immigration |

| Work permission scope | Captured Second Home pages show different work wording by permit context | Your visa approval details, activity mapping, written interpretation note | Immigration and licensed immigration counsel |

| PE/BUT exposure | Business activity facts can create Indonesian business tax exposure | Contracts, signing-authority map, client or entity map, work-location log, treaty memo | Indonesian tax counsel |

| Tax residency and treaty position | Crossing day-count or fact thresholds can change filing treatment | Travel-day tracker, income map, CoD file, adviser memo, current threshold verification note | Indonesian tax adviser and home-country adviser |

If you want a deeper dive, read The Global Digital Nomad Visa Index: 50+ Countries Compared. Before you commit capital, map your likely stay pattern and tax-residency exposure with the Tax Residency Tracker.

Phase 3: The Execution Playbook - Your Bulletproof Application & Arrival Plan#

Once your money, work, and tax position are set, this becomes an execution and control exercise. File the correct E33 path, verify fees in the live portal, and meet the 90-day post-entry commitment reporting deadline.

Build a submission-ready file before you touch the portal#

For E33 Visa Rumah Kedua, you upload electronic files, so prepare complete PDF or JPEG documents first and map each file to the portal field it supports. Use this submission readiness checklist before you upload anything.

| Item | Category | Detail |

|---|---|---|

| Passport | Required item | Current document validity rule pending official verification; a cited family FAQ shows at least 36 months, but do not assume that rule applies to every route. |

| Upload-ready files | Required item | PDF or JPEG format. |

| Bank statements | Required item | Three months of bank statements in your name showing at least USD $2000 living-funds proof. |

| Visa code and stay option | Required item | Keep your exact visa code and selected stay option, with a screenshot of the live portal page used. |

| Relationship documents | Dependency item | For dependents or family, translated into Indonesian unless already in English. |

| Sponsor documents | Dependency item | If you are asked for sponsor documents, pause and verify the visa path; the cited E33 page states this route does not require a sponsor. |

| Timing checks | Verification item | Validate visa use within 90 days from issue, and commitment compliance report within 90 days after entry. |

| Fee checks | Verification item | Validate fees in the live portal against your exact visa code or subcategory; official pages show Rp.13.000.000 on one page vs Rp12.000.000 / Rp18.500.000 on another. |

| Validity vs stay | Verification item | Confirm the case record distinguishes visa validity from period of stay, because immigration states they are different. |

Use the table above as your master checklist. If you are filing with family or a special route, add relationship documents and translation checks early. Before payment, confirm both 90-day clocks, the live fee tied to your exact visa code, and the distinction between visa validity and period of stay.

Screen your adviser before they handle a single upload#

Use any adviser as a processor of your evidence, not the owner of your compliance risk. Screen them on these points:

| Screening point | Ask this | Pass signal | Red flag |

|---|---|---|---|

| License status | Who is legally responsible for this filing, and what is their registration or authority? | Named accountable person with verifiable status | No accountable person, no verifiable status |

| Scope boundaries | What is included (E33 filing, family add-ons) and what is explicitly excluded (tax or work interpretation unless separately scoped)? | Written scope with exclusions | "We handle everything" with no written limits |

| Fee transparency | What are your service fees vs government charges for this exact visa code? | Itemized quote tied to visa code | Lump-sum pricing with no breakdown |

| Escalation process | If portal rules, fees, or commitment steps conflict, who escalates and within what response window? | Named escalation contact and documented process | "We'll deal with it later" |

| Communication cadence | How often will you send status updates, and will I get document copies or screenshots? | Agreed schedule with copies of filings and portal status | No schedule, no document trail |

Work through post-arrival milestones, not vague day ranges#

After approval, the main risk is execution drift. Use fixed milestones and keep proof as you go.

| Milestone | What to file/do | What proof to keep | Who confirms completion |

|---|---|---|---|

| Arrival setup | Enter before visa-use expiry; confirm what was issued at the checkpoint under your visa conditions | Visa grant, entry record, e-ITAS and Re-Entry Permit evidence (when issued for your visa conditions) | Immigration checkpoint records + your own document check |

| Identity/tax registration | If your stay may exceed 183 days in 12 months, assess domestic tax-subject exposure and NPWP registration needs (current 16-digit format) | NPWP registration proof, travel-day log, adviser notes | Indonesian tax adviser confirms your status position |

| Commitment compliance | Within 90 days after entry, report commitment fulfillment through an accepted route, including the US$130,000 state-bank deposit route or the US$1,000,000 qualifying property route | Bank letter, transfer receipt, property documents (if used), proof immigration accepted the report | Immigration confirmation of reported compliance |

Treat the commitment report as your non-negotiable deadline. Immigration has stated that failure to prove compliance after 90 days can lead to stay-permit or visa revocation and deportation. If any filing, fee, or reporting step stalls, escalate immediately through official immigration contact channels or the online complaint portal. The FAQ below covers the blockers you are most likely to hit and the fastest fixes.

We covered this in detail in A Guide to Indonesia's KITAP (Permanent Stay Permit).

Your Verdict: A Strategic Asset, Not Just a Visa#

Proceed only if your plan is validated against current official requirements, not assumptions. If your next step depends on old screenshots, informal advice, or unclear terms, pause before you file.

Keep the same sequence: Assess, De-Risk, Execute. The go/no-go test is whether your setup is documented, review-ready, and resilient if rules are checked line by line.

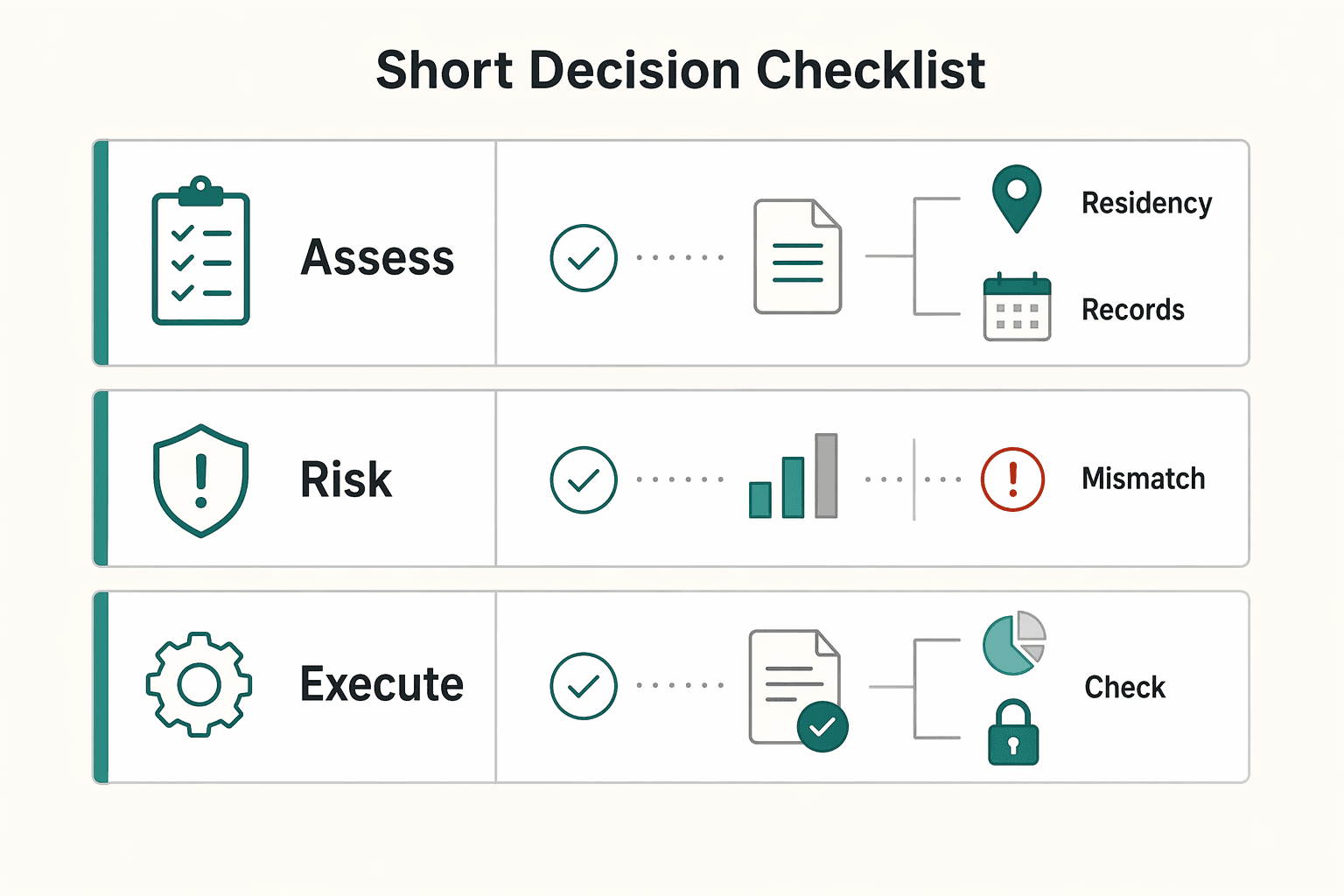

Short decision checklist#

- Assess

Pass if you have the live requirement text saved and mapped to your exact facts. Fail if your checklist comes from secondary summaries or unverified visa-code notes.

- De-Risk

Pass if qualified advisers have reviewed your tax exposure and your remote-work structure against the current terms you plan to use. Fail if either area is still based on "common practice" rather than documented review.

- Execute

Pass if your financial-commitment plan is operationally safe for your cash position and your document set is internally consistent: identity, ownership, source of funds, translations, and dates. Fail if you would need to improvise funding, patch mismatched records, or explain conflicts after submission.

A practical control point: keep a dated copy of the exact rules you relied on when preparing the file. Also watch for fraud or abuse risk in how third parties present the process.

Who this is for / not for#

| Better fit | Poor fit |

|---|---|

| You can document eligibility cleanly from current official requirements | You are relying on unofficial shortcuts or outdated guidance |

| Your tax and remote-work structure has already been professionally reviewed | Your tax or work position is still unresolved |

| If your route includes a financial commitment, it is planned without destabilizing your broader finances | Your plan depends on tight liquidity or post-filing adjustments |

Next step: verify the current official requirements, then finalize your document pack only against those confirmed live rules. For a step-by-step walkthrough, see A Guide to Getting a Golden Visa in Spain. If you are still choosing between Indonesia and other long-stay routes, compare your options with Gruv's Visa for Digital Nomads.

Frequently Asked Questions

Do you become an Indonesian tax resident just by getting this visa?

No. In Indonesia, tax residency is generally based on your facts, especially day count (more than 183 days in 12 months) and/or intent to reside, not the visa label alone. If you become a domestic tax subject, you may face worldwide income exposure. Foreign and Indonesian income can come into scope under current rules, including PTKP-related conditions, so confirm current thresholds before filing and do not assume treaty relief under a DTA/P3B without advice.

Can you work remotely for foreign clients on this route?

Only with caution. Current materials show different wording across Second Home-related contexts, including a prohibition on work in an employment relationship in one context and a conditional work allowance in another. Verify the exact visa index terms you are using before you act. If your setup could create a permanent establishment (BUT), meaning a taxable business presence in Indonesia, pause and get licensed immigration and tax advice first.

Do you need a sponsor for the current E33 filing path?

Not on the current E33 page. If you are asked for a sponsor, re-check that you are using the correct visa index and the current checklist. Keep screenshots of the live E33 requirements and your submission trail so your filed route is clear.

How should you think about the bank route versus the property route?

Choose the route that matches your evidence and liquidity plan, not the one that sounds more attractive. Current E33 materials show a commitment route for a US$130,000 state-owned bank deposit or a US$1,000,000 qualifying apartment or flat purchase commitment. | Route | Core eligibility evidence | Capital and liquidity tradeoff | Common documentation pitfall | |---|---|---|---| | State-owned bank route | Commitment to place at least US$130,000 in your own account at a state-owned bank | Lower stated threshold, but funds are still a formal commitment | Documents that do not match the current E33 commitment terms | | Property route | Commitment to buy a qualifying apartment or flat worth at least US$1,000,000 | Higher stated capital commitment | Property documents that do not align with the current E33 route terms |

Does the property option give you full freehold ownership?

No. Hak Pakai is a right to use or occupy, not the same as full freehold ownership (Hak Milik). Before you rely on property for visa compliance, confirm the exact title structure and legal documents.

Should you choose Indonesia or Thailand for a long stay?

Pick based on your profile and documents, not marketing language. Use this quick chooser first, then verify current criteria in the live program pages before filing. | Choose this | If this sounds like you | Why it may fit | |---|---|---| | Indonesia E33 | You can meet the capital-commitment route (US$130,000 bank or US$1,000,000 property) and want Indonesia as your base | The route is structured around commitment evidence in the current E33 requirements | | Thailand LTR | You fit one of the official four LTR visa types and prefer category-based qualification | Thailand publishes category tracks and a baseline 17 working day processing indication, with possible delays if more documents are requested | | Neither yet | Your work model, tax position, or documents are still unclear | You reduce rework and risk by clarifying legal and tax facts before applying |

Is the Indonesia Second Home Visa a direct path to citizenship?

No. It is a residency pathway, not a citizenship pathway. ITAP is permanent-stay status that can be requested by converting from ITAS, and immigration states ITAP is granted for 5 years in this context. Treat visa status, permanent stay, and citizenship as separate legal stages.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cdn.ca9.uscourts.gov/datastore/uploads/immigration/immig_west/B.%...trusted

- docs.un.org/en/A/65/761trusted

- documents1.worldbank.org/curated/en/631331483676357761/pdf/111628-WP-...trusted

- federalregister.gov/documents/2026/02/23/2026-03595/employment-a...trusted

- govinfo.gov/content/pkg/CHRG-115shrg24573/html/CHRG-115s...trusted

- scholarship.law.vanderbilt.edu/cgi/viewcontent.cgitrusted

- stateoig.gov/uploads/report/report_pdf_file/isp-i-11-24a_...trusted

- stateoig.gov/uploads/report/report_pdf_file/isp-i-05-29a_...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

How to Write Compelling Case Studies for Your Portfolio

Treat your case study as buyer decision evidence, not as a polished recap of work you enjoyed doing. To build trust, give the reader enough real context and proof to answer one question: should they trust your judgment on a project like theirs?

Indonesia Tax Residency for Bali Digital Nomads

Confusion starts when equally confident people give opposite answers and you still need one filing position you can defend. In Bali, the same fact pattern can sound low risk in one conversation and high risk in the next.