Quick Answer

An HSA can be a strong tool for self-employed global professionals if eligibility is current and documented. It can function as a medical reserve, a separate buffer for care decisions while traveling or relocating, and a long-term tax-favored account for qualified medical expenses. Before contributing or reimbursing yourself, confirm HSA-qualified coverage, verify current IRS rules, and keep clear records.

The Strategic Guide to Health Savings Accounts and HSAs#

This guide treats an HSA, or health savings account, as a three-part asset with current IRS rules setting the edges. In practice, a health savings account can serve as your medical reserve, a cross-border buffer, and a long-term tax-favored account for future qualified medical expenses.

| Rule | Timing |

|---|---|

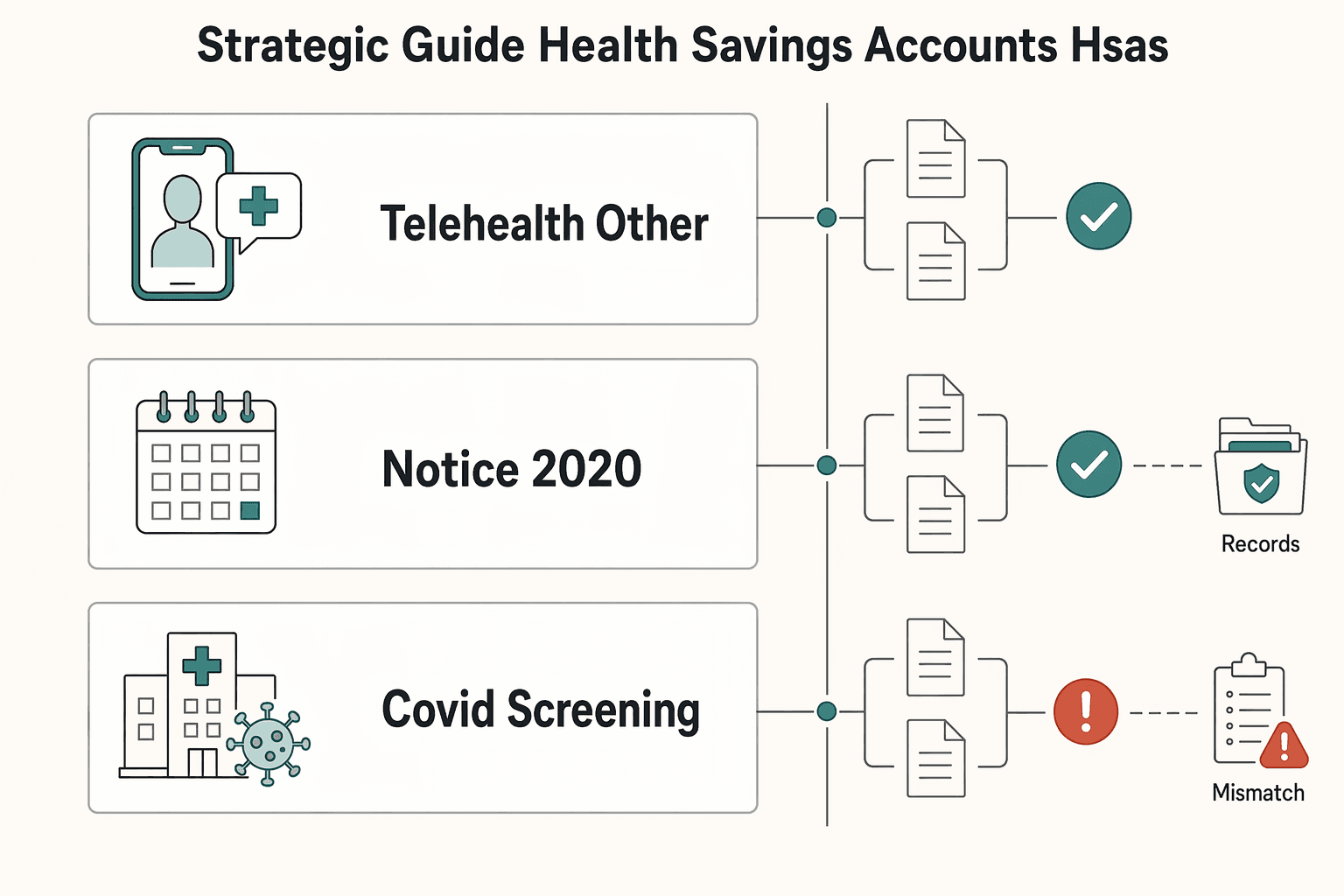

| Telehealth and other remote care | An HDHP could have a $0 deductible for plan years beginning after 2022 and before 2025 |

| Notice 2020-15 relief | Applies only to plan years ending on or before December 31, 2024 |

| COVID-19 screening/testing and preventive-care safe harbor treatment | Excluded effective July 24, 2023 |

- As a medical reserve, it keeps healthcare costs from hitting your main business cash flow or primary emergency fund.

- As a cross-border buffer, it gives you a separate lane for care decisions when you are traveling or relocating, while recognizing that not every expense will qualify.

- As a long-horizon account, it gives you the option to spend now or preserve funds for later healthcare needs when cash flow is stable.

That strategy works only if your eligibility is current and documented. Start with IRS Pub. 969, and use IRS.gov/Pub969 to confirm the latest updates.

Pub. 969 notes temporary rules, including that an eligible individual could remain contribution-eligible despite certain coverage outside the HDHP during the stated relief periods. It also notes that an HDHP could have a $0 deductible for telehealth and other remote care for plan years beginning after 2022 and before 2025. It states that Notice 2020-15 relief applies only to plan years ending on or before December 31, 2024, and that COVID-19 screening/testing was excluded from preventive-care safe harbor treatment effective July 24, 2023.

The practical risk is building a 2026 plan around rules that applied to earlier plan years. Before you contribute, confirm HDHP status in your plan materials, keep the plan summary, and organize contribution records and medical receipts. If you are self-employed, review Can You Deduct Health Insurance Premiums as a Freelancer? as related planning context.

With that foundation in place, the rest of this guide follows the order that matters most: eligibility and setup first, practical use abroad second, and long-term strategy last.

Your Health Savings Account Guide to a Financial Fortress#

The strategic case is simple: an HSA is valuable because several rules can work together if you stay inside them. At its core, it is a savings account that lets you set aside money on a pre-tax basis for qualified medical expenses.

Master the Triple-Tax Advantage#

An HSA can offer a three-part tax advantage, with one important qualifier. The tax benefits depend on following the qualified-use rules.

| Tax Advantage Stage | How It Works for Your HSA | Key Boundary |

|---|---|---|

| 1. Contribution | You set aside money on a pre-tax basis. | You may contribute only if you have an HSA-eligible plan. |

| 2. Growth | The account may earn interest or other earnings that are not taxable. | Tax treatment still depends on following HSA rules. |

| 3. Withdrawal | You can use HSA funds at any time for qualified medical expenses. | HSA funds generally may not be used to pay premiums. |

Used correctly, that structure can lower your out-of-pocket healthcare costs and give you more control over when those costs hit.

Build a Medical Emergency Fund#

An HSA works best when you treat it as a separate medical reserve, not as a loose extension of your checking account. A traditional emergency fund still matters, but this gives you a dedicated pool for qualified medical expenses, which are often sudden and disruptive.

The practical move is to keep this reserve rule-based: use it for qualified expenses, and verify edge cases before you spend. Healthcare.gov points readers to IRS Publication 969 for HSA qualification details and Publication 502 for qualified medical expenses.

Unlock Long-Term Planning Potential#

The long-term planning potential is meaningful, but only if you respect the boundaries. Balances may earn non-taxable interest or other earnings, and qualified medical withdrawals remain available when you need them.

That does not make every future use automatically tax-advantaged. If you expect to use HSA funds outside qualified medical spending, confirm the current IRS rules before you act.

Establish Clear Rules and Control#

For a business of one, consistency beats assumptions. The core checkpoints are straightforward: confirm you are on an HSA-eligible plan before contributing, keep withdrawals tied to qualified medical expenses, and check IRS guidance when a use case is unclear. That discipline is what turns the account into dependable financial infrastructure instead of a tax problem you discover later.

If you are also reviewing your cash reserves, see The Best High-Yield Savings Accounts for Freelancers.

The Acquisition Guide: Building Your Health Savings Account Foundation#

If you want this strategy to hold up, build your HSA in four passes: confirm eligibility, validate plan qualification, confirm contribution-rule checkpoints, and keep records that support future withdrawal checks.

| Pass | CRS checkpoint | Article action |

|---|---|---|

| 1 | Eligibility to Establish and Contribute to an HSA | Confirm you are eligible before you move money |

| 2 | HSA-Qualified High-Deductible Health Plans | Validate HSA-qualified status, minimum deductible, and out-of-pocket limit from formal documents |

| 3 | Contribution Limits | Verify the current-year cap before money goes in and repeat before each contribution cycle |

| 4 | Eligibility to Withdraw HSA Funds | Keep records that help validate eligibility when money went in and qualified use when money came out |

Use Congressional Research Service report R45277 (updated February 23, 2026) as a checkpoint map. Its structure tracks the decisions you need to make in order: Eligibility to Establish and Contribute to an HSA, HSA-Qualified High-Deductible Health Plans, Minimum Deductible, Disqualifying Coverage, Contribution Limits, and Eligibility to Withdraw HSA Funds.

Step 1 Verify eligibility before you open or fund anything#

Start with eligibility, not provider branding. Confirm your policy is an HSA-qualified high-deductible health plan and that you are eligible to establish and contribute before you move money.

Verify from formal plan documents and official guidance, not summary marketing copy. Confirm the current-year values for:

- Minimum deductible: [verify current amount]

- Maximum out-of-pocket limit: [verify current amount]

- Contribution cap: [verify current amount]

If a plan says "HSA-compatible" but you cannot match that to the underlying terms, pause and verify before contributing.

Also review disqualifying coverage before contributing. If you have other coverage, confirm it does not affect eligibility. If you are making insurance and tax decisions at the same time, use Gruv's guide on deducting health insurance premiums as a freelancer as related setup context.

Step 2 Validate plan qualification checkpoints in writing#

Treat plan qualification as its own checkpoint. Confirm your plan's HSA-qualified status, minimum deductible, and out-of-pocket limit from formal documents before contributing.

If any requirement is unclear or conflicting across documents, pause and resolve it before funding the account.

Step 3 Confirm contribution-rule checkpoints for the current year#

Use the Contribution Limits checkpoint directly: verify the current-year cap and your contribution plan before money goes in.

Repeat this check before each contribution cycle.

Step 4 Prepare for withdrawal-rule checkpoints from day one#

R45277 separates Contribution Limits from Eligibility to Withdraw HSA Funds. Keep records that help you validate both sides: eligibility when money went in, and qualified use when money came out.

- Store core records: enrollment confirmation, plan documents showing HSA-qualified status, contribution confirmations, statements, receipts, invoices, and proof of payment.

- Use one naming convention:

YYYY-MM-DD_provider_amount_currency_purpose.pdfis a practical pattern, not a legal requirement. - Keep a basic audit trail: a simple log can include service date, provider, amount, currency, reimbursement status, and reimbursement date when applicable.

For related planning context, see All-in-One ETF Portfolio: Pros, Cons, and Tax Checks for Global Professionals.

The Deployment Guide: Using Your Health Savings Account Abroad with Confidence#

Using an HSA abroad can become a documentation and decision-sequencing problem, not an automatic yes/no rule. Treat HSA tax qualification and insurance reimbursement as separate checks. A plan can deny a foreign claim for plan reasons without fully answering the HSA tax question.

Before you reimburse yourself, run a simple risk check:

- Does the expense type appear to align with current IRS qualified-expense guidance?

- Can you clearly prove you paid it?

- Does your file explain enough local context to make sense later?

If your travel is turning into longer stays or partial residency, Gruv's Canada digital nomad guide covers adjacent planning topics.

Separate tax qualification from insurance reimbursement#

This separation matters. Plan-specific reimbursement mechanics can affect whether your claim is paid, but those mechanics do not automatically settle HSA tax treatment.

Use official IRS guidance for the tax side, and keep source limits in mind. IRS Publication 4012-A (Rev. 2-2026) is a volunteer resource guide, not a definitive abroad reimbursement checklist.

Build the evidence pack before you reimburse#

If you expect to defend a reimbursement later, build the file while the visit is still fresh. The checklist below is practical recordkeeping guidance, not a definitive IRS abroad reimbursement checklist.

| Field | What to save | Execution note |

|---|---|---|

| Service date | Invoice or visit summary | Record the treatment date clearly |

| Provider name | Receipt, invoice, or clinic paperwork | Keep local spelling as shown |

| Service description | Itemized bill and short English note if needed | Clarify vague labels like "services" |

| Amount paid | Receipt plus payment proof | Match invoice to the payment record |

| Currency | Original invoice | Keep the original local-currency amount |

| Optional USD reference | Card statement or your own conversion note | Use one consistent method for your records |

| Local context note | Brief memo to file | Note country, provider type, and unusual context |

Store this in the record folder from the prior section, whether that is a single folder or a combined PDF, so the file still makes sense without follow-up.

Use a simple pay, capture, then reimburse path#

The safest path is usually the simplest one: pay, capture evidence immediately, then reimburse yourself only after the file is complete. In practice, that means using a payment method that works reliably where you are, saving the invoice and proof of payment on the spot, and adding a short context note when needed. If any core record is missing, pause reimbursement and fix the documentation while the visit is still recent.

You might also find this useful: A Guide to Superannuation for Australian Freelancers. For broader cross-border tax planning, FEIE Calculator can be a separate planning input.

The Advanced Guide: Turning a Health Savings Account into a Wealth Tool#

The move from spending tool to long-horizon asset is mostly about sequence: confirm eligibility first, optimize contributions second, invest third. If you skip that order, a common risk is avoidable contribution cleanup.

Start with eligibility, not enthusiasm#

For global professionals, FEIE planning is an early gate before you fund an HSA. FEIE and related housing benefits can change how much foreign-earned income remains exposed to U.S. tax, and that taxable-income picture should be clear before you contribute.

Use this decision framework to keep the order straight.

| If this sounds like your year | What to do now | Why it matters |

|---|---|---|

| You expect to exclude most or all foreign-earned income | Pause new contributions and verify taxable earned income with a qualified advisor | Helps reduce excess-contribution risk |

| Your day count is still moving because of travel | Wait until your 12-month window is clear, then decide | The physical presence test is based on exact day counting |

| You are also claiming a housing benefit | Have the housing amount figured first | That amount is figured first and can reduce FEIE room |

Keep the FEIE mechanics precise. Under the physical presence test, the IRS looks for 330 full days during any period of 12 consecutive months. A full day is 24 consecutive hours, midnight to midnight, the 330 days do not need to be consecutive, and missing the threshold means you do not meet that test.

A one-page memo in your records helps: your FEIE method, your 12-month window, whether housing benefits are included, and your advisor's conclusion on taxable earned income before contributions.

Optimize contributions only after the tax picture is real#

Once eligibility is confirmed, then optimize contributions. Current annual limit and catch-up amount pending official IRS, benefits, or qualified adviser verification.

| Check | What to do |

|---|---|

| Current-year limits for your coverage tier | Confirm the current IRS annual limit |

| Catch-up amount | Current catch-up amount pending official IRS, benefits, or qualified adviser verification |

| U.S.-taxable earned income | Confirm how much remains after FEIE and any housing benefit with your tax advisor |

| Year-to-date contributions | Check across all sources |

| Confirmation trail | Save it with your tax file |

If your income is uneven, later-year funding can be cleaner because travel days, FEIE planning, and housing calculations are more settled. Front-loading can create rework if taxable earned income ends up lower than expected.

Use this operating checklist to keep the contribution side clean:

- Confirm current-year contribution limits from a current IRS or custodian source.

- Confirm with your tax advisor how much earned income remains U.S.-taxable after FEIE and any housing benefit.

- Check year-to-date contributions across all sources.

- Save the confirmation trail with your tax file.

The IRS Interactive Tax Assistant is a useful screening tool for FEIE eligibility. Use it for initial checks, then rely on qualified tax advice when contribution decisions depend on taxable-income calculations.

Turn the account into an investing tool#

Once the contribution side is clean, the next decision is operational: invest promptly if your time horizon and cash reserves support it. Balances can remain in cash when provider defaults, minimums, or auto-invest settings are not configured.

Keep the process simple: contribute when eligible, invest promptly, and keep your contribution and tax records organized.

The tradeoff is straightforward. If preserving more assets in the account puts pressure on your emergency buffer, use a steadier approach you can actually sustain.

If you are also deciding how to handle medical premiums on your return, coordinate that with the same tax-planning choices driving HSA contributions. Can You Deduct Health Insurance Premiums as a Freelancer? is a useful companion for that planning.

This pairs well with our guide on Mega Backdoor Roth Conversions for Freelancers With Uneven Cashflow.

Frequently Asked Questions About HSAs and Health Savings Accounts#

After the strategy and setup work, most readers still have a few practical questions about an HSA. Keep these answers short, and treat any coverage or contribution change as a verify-first moment.

Can I use my HSA abroad for medical care?#

The FEIE materials used for this article do not answer that directly, so do not assume foreign care is automatically reimbursable. Before you act, confirm current HSA treatment with your custodian or tax advisor.

How does the Foreign Earned Income Exclusion affect HSA contributions?#

The provided excerpts confirm FEIE qualification checkpoints, but they do not by themselves resolve HSA contribution treatment. FEIE applies only if you are a qualifying individual with foreign earned income and file a U.S. return reporting that income. Under the physical presence test, the IRS looks for 330 full days in a 12-month period, and each full day is 24 consecutive hours from midnight to midnight. If your day count or filing position is still moving, finalize the FEIE calculation first, then confirm contribution treatment with your advisor. For broader compliance workflow context, see A Deep Dive into FinCEN's Beneficial Ownership Information (BOI) Reporting.

What if I qualify for FEIE for only part of the year?#

If FEIE qualification covers only part of the year, the IRS says the maximum exclusion must be adjusted by qualifying days. Income is generally treated as earned in the year you performed the work, so reconcile your work timeline and qualifying days before finalizing the exclusion.

How can a self-employed person open an HSA?#

The excerpts supporting this section do not establish HSA opening steps, so avoid shortcuts here. Confirm current setup requirements with your custodian or tax advisor before you apply. If you are also planning deductions, see Can You Deduct Health Insurance Premiums as a Freelancer?.

Is an HSA better than an FSA for a freelancer?#

The provided excerpts do not establish an HSA-versus-FSA comparison, so this section cannot make a verified "better" call. Use this quick verification checklist first, then read HSA vs FSA for Freelancers Who Need Long-Term Flexibility for a deeper side-by-side.

| Compare this | HSA | FSA |

|---|---|---|

| What this section covers | FEIE qualification checkpoints only | Confirm with the relevant authority |

| What to verify separately | Current HSA treatment with your custodian or tax advisor | Current FSA terms in your plan documents |

| Practical takeaway | Do not assume contribution treatment without verification | Do not assume claims or deadline rules without verification |

What happens if I lose HSA-qualifying coverage?#

The provided excerpts do not establish post-change HSA contribution treatment. If your coverage changes, confirm account and contribution handling with your custodian or tax advisor before taking action.

What are the current annual contribution limits?#

Verify the current limits before scheduling year-end funding.

Conclusion: Put This Health Savings Account Guide to Work#

An HSA is not a shortcut, but this guide should leave you with a practical framework for using a health savings account when you want more control over healthcare costs and potential tax advantages.

It is more than a place to stash receipts. An HSA lets you set aside money on a pre-tax basis for qualified medical expenses, and you can use those funds at any time for those expenses. You can contribute only if you have an HSA-eligible plan, and using untaxed dollars for eligible costs may lower out-of-pocket healthcare spending. HSA funds generally may not be used to pay insurance premiums.

The next move is practical: use this guide to confirm that you have an HSA-eligible plan, choose a provider, and fund the health savings account once your eligibility is clear. That is how this account becomes part of your financial safety net instead of another loosely managed account.

If you want a deeper dive, read Canadian Robo-Advisors for Global Professionals: Compliance, FX, and Account Fit.

If you want to tighten the rest of your cross-border money workflow with clearer operations and records, review Gruv's practical toolkit: Explore Tools.

Frequently Asked Questions

Can I use my HSA abroad for medical care?

Do not assume foreign care is automatically reimbursable. The FEIE materials used for this article do not answer that directly, so confirm current HSA treatment with your custodian or tax advisor before acting.

How does the Foreign Earned Income Exclusion affect HSA contributions?

The excerpts confirm FEIE qualification checkpoints, but they do not by themselves resolve HSA contribution treatment. FEIE applies only if you are a qualifying individual with foreign earned income and file a U.S. return reporting that income. Under the physical presence test, the IRS looks for 330 full days in a 12-month period, and each full day is 24 consecutive hours from midnight to midnight. If your day count or filing position is still moving, finalize the FEIE calculation first, then confirm contribution treatment with your advisor.

What if I qualify for FEIE for only part of the year?

Your maximum exclusion must be adjusted by qualifying days. Income is generally treated as earned in the year you performed the work, so reconcile your work timeline and qualifying days before finalizing the exclusion.

How can a self-employed person open an HSA?

The excerpts supporting this section do not establish HSA opening steps, so avoid shortcuts. Confirm current setup requirements with your custodian or tax advisor before you apply.

Is an HSA better than an FSA for a freelancer?

The provided excerpts do not establish an HSA-versus-FSA comparison, so this article cannot make a verified better call. Verify current HSA treatment with your custodian or tax advisor and review current FSA terms in your plan documents before comparing them.

What happens if I lose HSA-qualifying coverage?

The provided excerpts do not establish post-change HSA contribution treatment. If your coverage changes, confirm account and contribution handling with your custodian or tax advisor before taking action.

What are the current annual contribution limits?

Verify the current limits before scheduling year-end funding.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- app.leg.wa.gov/wac/default.aspxtrusted

- congress.gov/crs-product/R45277trusted

- healthcare.gov/glossary/health-savings-account-hsatrusted

- ilsos.gov/content/dam/departments/index/register/volum...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- mtmary.edu/footer/documents/2025.2026-faculty-handbook.pdftrusted

- qhpcertification.cms.gov/s/PY21_QHPApplicationIssuerInstructions_v1.1...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.

Can You Deduct Health Insurance Premiums as a Freelancer?

Most guides on how to deduct health insurance premiums as a freelancer fixate on headline savings and skip the real risk controls. That creates filing mistakes, not because freelancers ignore the rules, but because they never run a clear yes or no gate before claiming the deduction.