Quick Answer

Yes - choose a pte tax election only when a side-by-side model stays positive after state credit treatment, compliance effort, and entity cash timing. Start with eligibility and filing mechanics, including the New York online election process and California’s original-or-superseding return requirement. Then test owner-by-owner outcomes, especially cross-state credit use and Section 199A effects, before treating IRS Notice 2020-75 deduction upside as real.

The PTE Tax Election: A CEO's Framework for Navigating the SALT Cap#

A pte tax election is worth making only when the net result stays positive after owner credits, compliance work, and cash timing. PTET is an entity-level state tax election for eligible pass-throughs. IRS Notice 2020-75 allows certain state and local income taxes paid by partnerships or S corporations to be deducted at the entity level. The practical test is straightforward: does that federal benefit still hold after state credit mechanics and execution risk are fully modeled?

| Rule | Amount | MFS |

|---|---|---|

| Schedule A limit | $40,000 | $20,000 |

| Reduced above MAGI | $500,000 | $250,000 |

| Not below | $10,000 | $5,000 |

That sounds simple, but sequence matters. You are not deciding whether PTET is available in the abstract. You are deciding whether this entity, with this owner mix, in this filing footprint, should commit to an election that can be operationally unforgiving. A model that ignores owner-specific credit use, timing of payments, or return mechanics can show a positive result on paper and still produce a worse real-world outcome.

If SALT limits are part of your fact pattern, run the test using current rules. The 2025 IRS Schedule A instructions show a $40,000 limit ($20,000 MFS), reduced above $500,000 MAGI ($250,000 MFS), but not below $10,000 ($5,000 MFS). Start with the net outcome, not election availability, and build the comparison in this order:

- Confirm the entity can elect.

- Confirm the election can be made correctly and on time.

- Map how owners actually receive and use the state-side credit.

- Measure the federal entity-level deduction.

- Layer in compliance work, cash timing, and any owner-level mismatches.

- Recheck whether the result is still positive after all of that.

A costly PTET mistake is usually not misunderstanding the headline concept. It is skipping one of those steps because the projected federal benefit looked attractive early in the process.

A practical way to keep the analysis disciplined is to use one elect-versus-non-elect model with the same assumptions on both sides. Keep profit, sourcing, and ownership percentages fixed. Then change only what the election changes: entity-level tax deduction, state credit flow, payment timing, and related return mechanics. If you let the assumptions drift between scenarios, the answer gets harder to trust.

For CEOs and finance leads, that matters because PTET is often treated as a tax-side technical issue when it is really a tax-and-operations decision. Someone has to own the election calendar, the estimated payment process, the proof of payment, the owner communication, and the return package. If no one owns those items, the benefit can erode fast.

Eligibility check#

Start by confirming that the entity can elect at all. Do not start by estimating savings.

| Step | Focus |

|---|---|

| Pull the prior-year federal return and the entity's relevant state returns | Filed returns |

| Confirm how the entity is classified on filed returns | Entity classification |

| Confirm whether the current-year state rules still support that type of entity | Current-year state rules |

| Verify how the election is made, and where proof of election will come from | Election method and proof |

| Verify when the election becomes irrevocable | Irrevocability |

| Verify what payments are required and when | Payment timing |

| Verify how each owner receives and uses the related credit | Owner credit path |

| Only then start modeling tax savings | Modeling order |

Confirm the entity classification on filed returns first. California defines a qualified PTE as an entity taxed as a partnership or S corporation, and New York limits PTET to eligible partnerships and New York S corporations. If the entity does not meet the state definition, stop there.

That first stop point matters because teams often waste time building savings estimates for entities that never had a clean path into the regime. Pull the filed federal return, pull the state returns that establish how the entity has been filing, and reconcile the classification before anyone starts forecasting tax impact. If the filed posture and the assumed posture are not the same, fix that mismatch before moving forward.

After that, verify four mechanics before you model any benefit. These are not clerical details. They determine whether the modeled tax result is achievable in practice.

| Checkpoint | What to confirm now |

|---|---|

| Election method | New York: annual online election. California: election on a timely filed original or superseding return (not amended). |

| Irrevocability | New York: irrevocable after the due date of the first PTET estimated payment. California: irrevocable for that year once made. |

| Payment flow | California ties election-year mechanics to a payment due on or before June 15. |

| Owner credit path | How each owner receives and uses the state credit in that jurisdiction. |

Start with election method. The question is not just whether the state offers PTET. The question is whether your team knows exactly how the election is made for that state and year, and whether the return path you are planning actually supports it. California makes this concrete because the election must be on a timely filed original or superseding return, not an amended return. If your process assumes you can decide later and fix it on amendment, your process is already misaligned with the rule stated here.

Next, treat irrevocability as a management issue, not just a legal note. An irrevocable election changes the standard for internal sign-off. You should not treat it like a flexible year-end cleanup item. If the due date for the first estimated payment is the point after which the decision is locked, that date is your operational deadline, not the return filing date that may be getting more attention inside the company. The wrong internal calendar can send the election sideways.

Then move to payment flow. California's June 15 requirement is not just a payment step. It is part of whether the expected credit holds up. If that payment is late or short, you are not simply dealing with an administrative annoyance. You may be changing the economics of the election itself.

In California, underpayment tied to the June 15 requirement can reduce credit by 12.5% of the owner's pro rata share of the unpaid amount. For other states, keep the workpaper explicit when a rule has not been verified: mark the election window as unresolved and the threshold as unresolved until someone confirms the current-year rule.

Those unresolved items prevent silent assumptions from entering the model. If a team member cannot verify the current-year election window or threshold, the model should show that gap in plain language rather than burying it in a tax estimate that looks final. In practice, that means your workpaper should contain unresolved items as visible flags, not side comments.

Owner credit path is where many early-stage PTET models become too optimistic. Do not assume that because the entity pays tax, every owner will extract equal value from the related credit. Build an owner roster and review the mechanics owner by owner. At a minimum, your roster should answer these questions before you call the election beneficial:

- Which owners are residents in which states?

- Which owners are expected to receive the credit in the state where the election is being made?

- Is the anticipated benefit dependent on another state recognizing or absorbing that credit cleanly?

- Are any owners likely to be outliers even if the entity-level result looks positive?

This is also where you should pause if ownership changed during the year, if the state filing footprint changed, or if income sourcing is less stable than usual. PTET modeling is easiest when the facts are steady. It becomes less reliable when the filing profile is still moving.

For the eligibility phase, use this sequence:

- Pull the prior-year federal return and the entity's relevant state returns.

- Confirm how the entity is classified on filed returns.

- Confirm whether the current-year state rules still support that type of entity.

- Verify how the election is made, and where proof of election will come from.

- Verify when the election becomes irrevocable.

- Verify what payments are required and when.

- Verify how each owner receives and uses the related credit.

- Only then start modeling tax savings.

That sequence is conservative, but it saves time. The entities that move through PTET cleanly are usually not the ones with the smartest-looking high-level estimate. They are the ones that locked down the mechanics before anyone relied on the estimate. Once eligibility and mechanics are clear, the next question is whether the election is actually worth making in your fact pattern.

Elect, do-not-elect, or pause#

A quick screen can save you from a full model that was never likely to work.

| Path | Usually fits when | Verify before acting |

|---|---|---|

| Elect | You are SALT-constrained, the entity qualifies, and owner credit mechanics are usable | Current-year election steps, payment timing, owner credit treatment, entity cash capacity |

| Do not elect | You are not meaningfully constrained, the entity is ineligible, or state-side relief is weak | That non-election is truly cleaner and does not hide a state-credit issue |

| Pause and escalate | Multi-state filings, mixed owner residency, or meaningful QBI sensitivity | Owner-by-owner outcomes, resident-credit rules, current-year state guidance |

This screen is useful because it forces discipline before the model gets dressed up with optimistic assumptions. In practice, each path has a different burden of proof.

If you are leaning elect, the standard is not "there appears to be a federal deduction." The standard is that the entity qualifies, the election can be made correctly, the payment flow is manageable, the owners can use the credits in the way the model assumes, and the entity has enough cash capacity to fund the tax when due. If one of those items is shaky, you do not yet have an elect case. You have a draft hypothesis.

If you are leaning do not elect, the risk is different. Teams sometimes default to non-election because it feels simpler, but simplicity is only a good answer if it does not leave meaningful value on the table. The non-election path still needs a comparison. Ask whether the decision is truly cleaner after taking SALT limits into account, or whether it is just more familiar. The right non-election decision should survive a side-by-side model, not just a preference for less filing complexity.

If you are in pause and escalate, take that label seriously. It does not mean the election is probably good and just needs a few details checked. It means the details are likely the decision. Multi-state filings, mixed owner residency, and material QBI sensitivity are exactly the kinds of facts that can turn a strong entity-level result into a mixed or negative owner-level result.

Model elect versus non-elect using the same profit assumptions and the same owner mix. If the benefit disappears after compliance cost, cash timing, or credit mismatch, skip it.

The "same assumptions" point is worth emphasizing because it is one of the easiest places to distort the analysis. Do not let the elect case use one profit estimate and the non-elect case use another. Do not use one ownership roster for one scenario and a cleaned-up roster for the other. Do not assume smoother payment execution in the elect case than your accounting process can realistically deliver. If the comparison is not symmetrical, the output is not a decision tool.

A practical way to frame the model is to ask four questions in order:

- What is the federal benefit from the entity-level deduction?

- What state-side credit or offset is expected for each owner?

- What is the cost of making and administering the election?

- What is the effect of timing, including when cash leaves the entity and when owners actually realize relief?

That last point matters more than many teams expect. Even when the annual tax answer is positive, the timing may still be uncomfortable. If the entity must make payments before owners see the practical benefit, the company needs to be comfortable funding that gap. If the company is already tight on cash, the tax result can be positive while the operational result still feels wrong. That is not a reason to ignore the election, but it is a reason to treat the liquidity effect as part of the decision rather than an afterthought.

You should also decide in advance how much owner variance you are willing to accept. Some groups only move forward if the election is broadly positive across owners. Others are willing to proceed if the entity-level and majority-owner result is clearly favorable and the outlier treatment is understood. The key is to make that standard explicit before the filing season gets compressed. If you wait until draft returns are in motion, the conversation becomes reactive.

A simple internal decision rule can help:

- Elect if the net benefit remains positive after credit usage, compliance effort, and timing are reflected, and there is no unverified step that could change the answer.

- Do not elect if the entity is ineligible, the owners cannot use the credits in the way the model requires, or the expected benefit is too thin once real execution costs are included.

- Pause if the answer depends on unresolved resident-credit treatment, unresolved current-year guidance, or a QBI result that has not actually been modeled.

That headline screen is useful, but most mistakes show up in the details that follow.

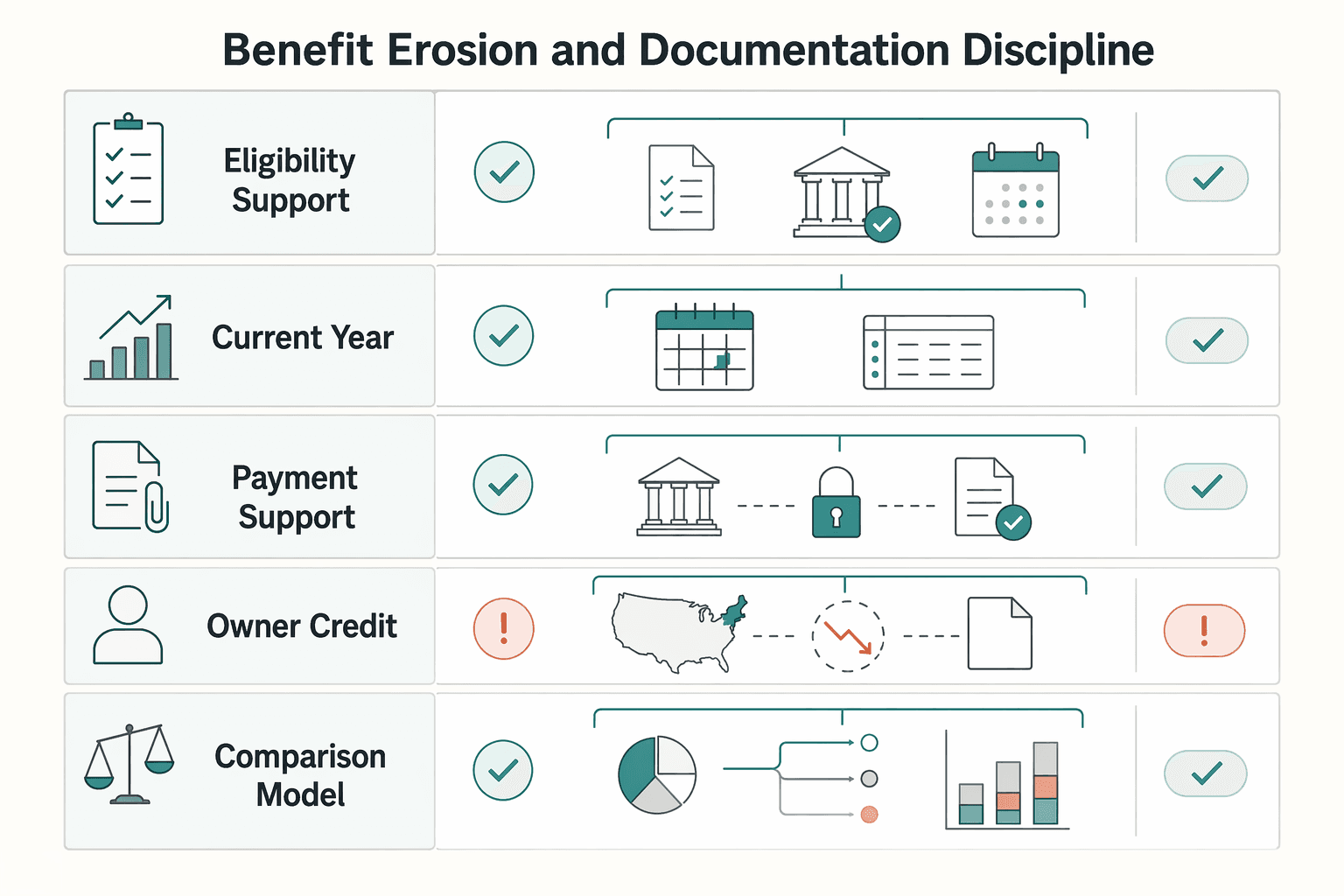

Benefit erosion and documentation discipline#

Resident-credit mismatch is a major failure point. New York resident credit for another jurisdiction's PTET requires a "substantially similar" tax, and New York's published list notes a legislative cutoff of December 15, 2023. If your result depends on that list, re-verify before filing.

| File section | What to keep |

|---|---|

| Eligibility support | Filed returns that confirm the entity classification and the filing posture you are relying on |

| Current-year mechanics | Screenshots, portal confirmations, draft return pages, or other proof that show how and when the election was made |

| Payment support | Bank records and payment confirmations |

| Owner credit support | Draft schedules or workpapers showing how each owner is expected to receive and use the state-side credit |

| Comparison model | The elect-versus-non-elect analysis with the assumptions clearly stated, including any unresolved items that were flagged for verification |

This is where the benefit often erodes. The entity may deduct the tax at the entity level for federal purposes, but if a resident-credit assumption fails for one or more owners, the total economic result can change fast. That is why owner-level verification is not a final cleanup step. It belongs in the core model.

A disciplined way to test resident-credit risk is to separate the analysis into two layers:

- Entity layer: Does the election produce the federal entity-level deduction you expect?

- Owner layer: Does each owner actually receive and use the related state relief in the way the entity-level story assumes?

If the entity layer is favorable but the owner layer is mixed, do not average the issue away. Document who is helped, who is neutral, and who is potentially worse off. That gives you a real management decision instead of a blended number that hides the tradeoff.

Owner-level variance is another leak. An entity-level benefit can look positive while specific owners lose value because residency, sourcing, and credit usage differ. Treat that as an escalation signal, not a rounding issue. If you want more context on state residency friction, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

In practice, owner variance usually shows up in one of three ways:

- An owner can receive a credit but cannot use it in the way the model assumed.

- An owner's resident state treatment does not line up cleanly with the source-state PTET result.

- The entity-level deduction is real, but the state-side relief does not land evenly across the owner group.

You do not need a long narrative to manage that risk, but you do need a clean owner-by-owner review. A short schedule listing owners, resident states, expected credit path, and open verification items is often enough to show whether the election is broadly workable or whether it needs escalation.

QBI can also change the answer. IRS guidance defines QBI as a net amount including deduction items, so PTET deductions can affect Section 199A inputs. Do not assume direction. Model it, then sanity-check with A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

The operational mistake here is treating QBI as either always helpful or always harmful in the PTET context. The right instruction is simpler: do not assume direction. Model it. Your elect-versus-non-elect comparison should not stop at the PTET deduction itself. It should also show whether the deduction changes the Section 199A picture enough to matter. If the election only works because someone ignored QBI movement, the model is incomplete.

A short sanity-check routine helps:

- Confirm the profit estimate being used for the PTET model.

- Confirm that the same estimate is feeding the QBI comparison.

- Confirm that deduction items are being treated consistently across elect and non-elect scenarios.

- Confirm that any meaningful QBI movement is being surfaced to the decision maker, not buried in supporting tabs.

Documentation discipline matters because PTET is easy to explain at a high level and easy to mishandle in execution. Before sign-off, keep one prep file with the core support in one place:

- Prior-year federal and entity returns

- Current-year profit estimate

- Owner roster with resident states

- State filing footprint by source income

- Election confirmations (portal or filing proof)

- Payment confirmations and bank support

- Draft owner credit support by state

- The exact return version used to elect, especially California original or superseding return timing

Treat that file as a decision file, not just a return assembly folder. The point is not only to support filing. It is to let someone reviewing the election see, in one place, how the decision was made and whether the execution matched the assumptions.

A useful way to organize the file is in the same order the risk appears:

- Eligibility support

Include filed returns that confirm the entity classification and the filing posture you are relying on.

- Current-year mechanics

Save screenshots, portal confirmations, draft return pages, or other proof that show how and when the election was made.

- Payment support

Keep bank records and payment confirmations together so there is no later question about whether the required payment was made on time and in the right amount.

- Owner credit support

Keep the draft schedules or workpapers showing how each owner is expected to receive and use the state-side credit.

- Comparison model

Preserve the elect-versus-non-elect analysis with the assumptions clearly stated, including any unresolved items that were flagged for verification.

That structure helps when the issue is not whether the election was filed, but whether the election that was filed still matches the assumptions under which it was approved.

Also, do not underestimate the value of preserving the exact version of the return used to make the election. The California point above is a good example. If the election must be on a timely filed original or superseding return and not an amended return, you want the file to show exactly what was filed and when. That is not over-documentation. It is the evidence that the election path matched the rule.

Use a short memo request to your CPA. Ask for confirmation of eligibility, election method, irrevocability point, payment deadlines, owner credit path, projected federal effect, QBI impact, and mismatch exposure by owner.

Keep that memo request short on purpose. Long, open-ended tax emails tend to get broad answers. A short checklist-style request is more likely to produce direct confirmation you can act on. If your CPA replies without addressing one of the listed points, treat that as an unresolved item, not as implicit approval.

A practical version of that request is to ask for answers that are clearly yes, no, or needs verification. That format makes it easier to spot where the model is solid and where it is still provisional. It also prevents a common communication problem: everyone believes the election was reviewed, but key mechanics were never actually confirmed.

Good PTET decisions often have two features in common:

- The modeled benefit was tested owner by owner, not just at the entity level.

- The execution file could prove the election, the payment, and the expected credit path without rebuilding the analysis from scratch.

That is the discipline that keeps the election from becoming a year-end surprise.

FAQ#

Who is usually eligible for a pte tax election?#

Eligibility is state-specific, but the baseline here is entities taxed as partnerships or S corporations where the state program is open and properly elected. In New York and California, the mechanics matter as much as the entity type. If the filing method, deadline, or return path is unresolved, treat eligibility as unconfirmed.

When should I usually skip the election?#

Skip it when the entity is ineligible, the federal SALT benefit is not meaningful in your scenario, or owner-level credits do not translate into clean relief. Also skip it when projected gains vanish after payment timing, compliance burden, or QBI movement are included. If one broken assumption would flip the result, the election is probably too fragile.

Why does multi-state activity make this harder?#

Because credits are jurisdiction-specific and may not map cleanly across resident and source states. New York's substantial-similarity requirement adds another gate for certain resident-credit outcomes. If your case depends on cross-state credit treatment, verify each step with current-year state guidance and review the path state by state and owner by owner.

When should I involve a pro?#

Involve a pro when the result depends on multi-state resident-credit treatment, mixed owner residency, material QBI movement, or election timing that is close to deadline. Ask for a decision-ready answer that confirms eligibility, election method, irrevocability, payment timing, owner credit treatment, QBI effect, and mismatch risk by owner. That gives you a clear basis to approve, reject, or pause the election.

Before you lock in a PTET decision, map your filing footprint and owner residency in one place with the Tax Residency Tracker.

If your elect-versus-non-elect model is still borderline after credit and cash-timing checks, use Contact to validate your next operational step before filing.

Frequently Asked Questions

Who is usually eligible for a pte tax election?

Eligibility is state-specific, but the baseline here is entities taxed as partnerships or S corporations where the state program is open and properly elected. In New York and California, the mechanics matter as much as the entity type. If the filing method, deadline, or return path is unresolved, treat eligibility as unconfirmed.

When should I usually skip the election?

Skip it when the entity is ineligible, the federal SALT benefit is not meaningful in your scenario, or owner-level credits do not translate into clean relief. Also skip it when projected gains vanish after payment timing, compliance burden, or QBI movement are included. If one broken assumption would flip the result, the election is probably too fragile.

Why does multi-state activity make this harder?

Because credits are jurisdiction-specific and may not map cleanly across resident and source states. New York's substantial-similarity requirement adds another gate for certain resident-credit outcomes. If your case depends on cross-state credit treatment, verify each step with current-year state guidance and review the path state by state and owner by owner.

When should I involve a pro?

Involve a pro when the result depends on multi-state resident-credit treatment, mixed owner residency, material QBI movement, or election timing that is close to deadline. Ask for a decision-ready answer that confirms eligibility, election method, irrevocability, payment timing, owner credit treatment, QBI effect, and mismatch risk by owner. That gives you a clear basis to approve, reject, or pause the election. Before you lock in a PTET decision, map your filing footprint and owner residency in one place with the Tax Residency Tracker. If your elect-versus-non-elect model is still borderline after credit and cash-timing checks, use Contact to validate your next operational step before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

A Guide to the Qualified Business Income (QBI) Deduction for Freelancers

**You can classify your Section 199A path in one focused session, then move with confidence instead of guessing.** Treat this as an operating manual for the QBI deduction if you freelance. Classify first, optimize second. That order matters even more when you work across borders, where documentation and residency rules can vary by jurisdiction.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.