Quick Answer

For most freelancers in Germany, the first step is to confirm whether you must pay into the state pension, since many are exempt but certain professions and KSK eligible creatives are not. Then the main decision is usually between a tax-deductible but rigid Rürup-Rente and a flexible global ETF portfolio, while the Riester-Rente is usually a secondary option for independent professionals.

The Global Professional's Playbook for German Pensions: A 3-Step Framework#

As a global professional, you've built a career on expertise and autonomy. You make calculated decisions and stay in control. Yet once you hit the German pension system, many freelancers and self-employed experts feel that control slipping away. It can quickly turn into a high-stakes compliance problem, bringing back the kind of bureaucracy you probably wanted to avoid in the first place.

The available information is often fragmented, written in dense legalese, and designed for a different era - or a different type of worker. You've likely run into a confusing mix of terms like gesetzliche Rentenversicherung, Riester-Rente, and Rürup-Rente, with very little practical guidance on what actually applies to your situation. This isn't just frustrating; it's a strategic risk. Making the wrong choice, or no choice at all, can have real financial consequences.

Think of this as your executive playbook. We'll replace uncertainty with a practical 3-step framework designed for a "Business-of-One" like yours, moving you from compliance anxiety to informed control. This framework will help you:

- Define your precise legal obligations, cutting through the noise to determine what you are truly required to do.

- Evaluate your options with the sharp eye of an investor, weighing the real-world trade-offs of various pension schemes.

- Integrate your German assets into a coherent global strategy that works for you, no matter where your career takes you next.

By the end of this guide, the German pension system should feel less like a black box and more like a system you can handle with confidence.

Step 1: Define Your Obligation (The Compliance Audit)#

Before you build a retirement strategy, get clear on your legal requirements. This part is non-negotiable. For any self-employed professional in Germany, the first question is: "What am I legally required to do?" Answer that first, and you remove a large share of the uncertainty before making any financial decisions.

| Group | GRV status |

|---|---|

| Most freelancers | Not automatically obligated to pay into the state pension (GRV) |

| Teachers, coaches, and educators | Likely required to contribute |

| Nurses, therapists, and caregivers | Likely required to contribute |

| Midwives | Likely required to contribute |

| Tradespeople (Handwerker) | Likely required to contribute |

| Artists and publicists (e.g., journalists, writers) | Likely required to contribute |

First, a quick map of the terrain. The German retirement system rests on three pillars:

- Pillar 1: State Pension (Gesetzliche Rentenversicherung - GRV): The mandatory, state-run pension insurance program. It operates on a pay-as-you-go system, where current workers' contributions fund current retirees' pensions.

- Pillar 2: Occupational Pensions (Betriebliche Altersversorgung - bAV): Employer-sponsored plans, generally not relevant to freelancers.

- Pillar 3: Private Pensions (Private Altersvorsorge): Individually funded retirement plans, including government-supported options like the Riester-Rente and Rürup-Rente, which we will evaluate in Step 2.

While most freelancers are not automatically obligated to pay into the state pension (GRV), critical exceptions exist. You are likely required to contribute if your work falls into specific categories, including:

- Teachers, coaches, and educators

- Nurses, therapists, and caregivers

- Midwives

- Tradespeople (Handwerker)

- Artists and publicists (e.g., journalists, writers)

If your profession is on this list, participation in the state pension is a legal duty, not a choice.

Demystifying the KSK (Künstlersozialkasse): The Critical Exception for Creatives#

For freelance artists, musicians, writers, and journalists, the Künstlersozialkasse (KSK) is the key exception. The KSK is not an insurance provider; it is a fund that effectively treats you like an employee for social security purposes. If you are accepted, you pay only half of your health and state pension insurance contributions, while the KSK covers the other half, funded by the government and a levy on companies that hire creative freelancers. Membership is mandatory for eligible creative professionals who earn above a minimum threshold.

Mitigating the "One-Client Trap" (Scheinselbstständigkeit)#

Another major compliance risk is being misclassified as a "false self-employed" person, or Scheinselbstständigkeit. This happens when you operate as a freelancer on paper, but your working relationship closely resembles that of an employee. If German authorities make that finding, you and your client can be forced to pay back-dated social security contributions for up to four years, plus penalties.

Key red flags that regulators look for include:

- Economic Dependence: You earn the vast majority (typically over 83%) of your income from a single client.

- Following Directives: You are obligated to follow your client's instructions on when, where, and how you work.

- Integration: You are integrated into the client's internal processes, using a company email and having a designated workspace.

- Lack of Entrepreneurial Risk: You do not have your own business branding, do not actively market your services, and bear little financial risk.

In practice, if you want to protect your autonomy and keep control of your business, structure your client engagements to avoid these indicators.

Step 2: Evaluate Your Options (The Strategic ROI Analysis)#

Once your legal duties are clear, you can shift from compliance to strategy. As CEO of your "Business-of-One," the next question is where your retirement capital should go. For most high-earning professionals in Germany, this comes down to one central choice: do you channel your capital into a state-subsidized Rürup-Rente or a flexible, self-directed global ETF portfolio?

This isn't just a financial choice. It's a decision about control, flexibility, and your long-term plan. The core trade-off is immediate, significant tax relief versus long-term control.

The Rürup-Rente (or Basis-Rente) is a state-subsidized private pension plan designed for the self-employed. Its primary benefit is straightforward: your contributions are fully tax-deductible up to the annual maximum (€29,344 for singles in 2025). This immediately reduces your taxable income, providing substantial savings in your highest-earning years. But that tax advantage comes at the price of real inflexibility.

Here's a head-to-head comparison to frame your decision:

| Feature | Rürup-Rente (The "Golden Handcuffs") | Global ETF Portfolio (The "Freedom Asset") |

|---|---|---|

| Tax Efficiency | Immediate & High. 100% of contributions (up to the annual cap) are tax-deductible now. Payouts in retirement are then subject to income tax. | Long-term & Favorable. Contributions are from post-tax income. Growth is taxed only when you sell, often at a lower flat rate for capital gains. |

| Flexibility & Access | Extremely Rigid. Capital is locked until retirement (age 62+). You cannot take a lump-sum payment; funds must be converted into a lifelong monthly annuity. | Total Liquidity. You have 100% control to access your capital anytime, for any reason - a critical advantage for managing life's opportunities or crises. |

| Portability | Very Low. If you leave Germany, the contract is essentially frozen. You cannot add more funds, and accessing the annuity from abroad can create tax complications. | Globally Portable. Your brokerage account is location-independent. You can manage it from anywhere, completely delinked from your country of residence. |

| Fees & Performance | Often High & Opaque. As insurance products, they can carry heavy, hard-to-spot acquisition and management fees that erode long-term returns. | Ultra Low-Cost. Broad-market ETFs have minuscule expense ratios (often <0.25%), so more of your money stays invested. |

Dr. Chris Madu, an independent financial advisor for expats, captures this dilemma well: "Die Rürup-Rente ist steuerlich hochinteressant, aber für jeden, der plant, Deutschland irgendwann zu verlassen, ist sie eine absolute Katastrophe. Für global mobile Professionals ist das ein goldener Käfig."

His warning is simple: the tax benefits you gain today are paid for with the inflexibility you face tomorrow. If you might eventually leave Germany, that trade-off matters.

Why the Riester-Rente is a Strategic Distraction#

In your research, you will inevitably encounter the Riester-Rente. For most independent professionals, you can disregard it. The Riester plan is a state-subsidized vehicle designed primarily for employees contributing to the state system, low-income earners, and families. For a high-earning independent professional, its contribution limits are too low and its structure is misaligned with your financial goals, making it a distraction from the core decision.

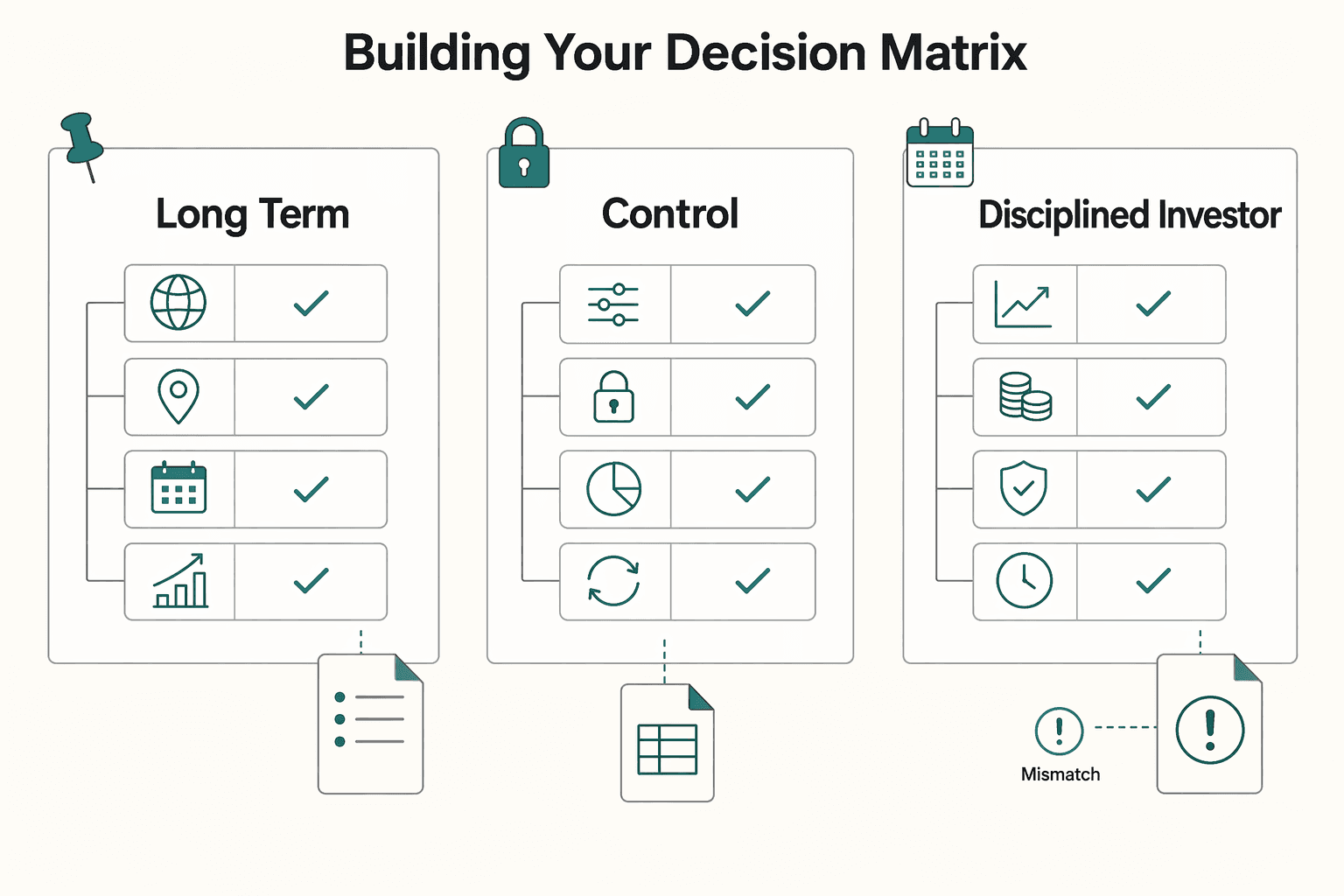

Building Your Decision Matrix#

To make a rational, data-driven decision, answer these questions honestly:

- What is my long-term commitment to Germany? If you are certain you will retire here, the tax benefits and guaranteed annuity of a Rürup plan may be more attractive. If you see yourself leaving in 5-10 years, its inflexibility becomes a significant liability.

- How much do I value liquidity and control? If access to your capital for major life events or other investment opportunities is a priority, a self-directed ETF portfolio is the clear winner.

- Am I a disciplined investor? Rürup plans are "set-it-and-forget-it" products. An ETF portfolio requires active management and discipline, but offers far greater potential for long-term growth with lower fees.

These questions force you to confront the reality of your global lifestyle and risk tolerance, so the path you choose supports your plans instead of boxing you in later.

Step 3: Integrate Your Portfolio (The Cross-Border Strategy)#

Your financial life does not exist in a German silo. As a global professional, the final step is to integrate your German assets into a coherent, resilient global retirement strategy. That means dealing with cross-border complexity early, so your German chapter enhances - rather than complicates - your long-term wealth plan. The pension decision also sits inside the wider tax picture, which is why A Deep Dive into Germany's Tax System for Freelancers is a useful companion when you model the rest of the plan.

The Exit Strategy: Can You Get Your Pension Contributions Back?#

This is a critical question for any globally mobile professional. The short answer is yes: under specific circumstances, you can claim a refund of your contributions to the German state pension plan (Deutsche Rentenversicherung or GRV).

| Rule | Requirement | Detail |

|---|---|---|

| 60-month limit | Less than 60 months of contributions | For citizens of many non-EU countries with social security agreements, like the USA, Canada, Australia, and India. |

| 24-month waiting period | At least 24 months since the last contribution | You must have left Germany and the EU before you can apply for a refund. |

| Citizenship and residency | Non-EU/EEA citizen residing outside the EU/EEA | This option is generally only available under these conditions. |

The rules are precise:

- The 60-Month Limit: For citizens of many non-EU countries with social security agreements (like the USA, Canada, Australia, and India), you are only eligible for a refund if you have contributed for less than 60 months (five years). Cross this threshold, and you are generally locked into the German system and will receive a German pension at retirement age, no matter how small.

- The 24-Month Waiting Period: You must have left Germany (and the EU), and a waiting period of at least 24 months must have passed since your last contribution before you can apply for a refund.

- Citizenship and Residency: This option is generally only available to citizens of non-EU/EEA countries who are residing outside of the EU/EEA.

If you may leave Germany, knowing these rules from the outset gives you much more control over your exit strategy as you approach the five-year mark.

Leveraging Totalization Agreements: Your Global Social Security Shield#

Many professionals, especially those from the United States, worry that contributions made in Germany will simply vanish if they move home. This is where Totalization Agreements become an important safeguard. The US-Germany Social Security Agreement, for example, is designed to prevent this exact scenario.

Its two primary functions are to:

- Prevent Double Taxation: The agreement determines whether you pay social security taxes to the US or German system, preventing the costly scenario where both countries demand contributions on the same income.

- Allow for Totalized Benefits: It allows the years you contribute in Germany to count toward your eligibility for US Social Security. If you don't have enough work credits under the U.S. system, the agreement can help you qualify for a partial benefit based on a combination of your U.S. and German credits. This ensures no contribution is ever truly "lost."

A Unified Framework: Integrating German Assets#

So, how does a rigid asset like a Rürup-Rente or your vested German state pension "talk" to your US-based SEP-IRA or UK SIPP? Not directly. You need to build a unified framework around them.

View your German assets through a global lens:

- Asset Allocation: Treat your German pension assets as the most conservative, illiquid portion of your global portfolio. If you have a Rürup-Rente, it's essentially a fixed-income annuity. Balance this by tilting your more liquid, self-directed portfolios more heavily toward global equities.

- Currency Risk: A pension denominated in Euros introduces currency risk if your long-term financial life will be centered on the US Dollar or British Pound. Account for this in your overall strategy, perhaps by holding other Euro-based assets or accepting it as a component of your diversification.

- Cross-Border Tax Treatment: Don't assume a tax-deductible contribution in Germany is automatically tax-free in your home country. While tax treaties prevent double taxation, the reporting can be complex. For instance, the IRS generally views German pensions as taxable ordinary income. Your German assets are not in a vacuum; they are part of a single financial picture that must be managed holistically.

Conclusion: You Are the CEO of Your Financial Future#

The real value of this framework is the shift in mindset it creates. You are no longer just reacting to opaque rules; you are directing your capital with a clearer view of the trade-offs. The anxiety of a compliance misstep or a wasted investment is replaced by something more useful: informed control.

First, you learned to Define your position by establishing your exact legal obligations. That reduces the risk of getting the basics wrong and gives you the clarity needed to think strategically about wealth creation, not just rule-following.

With that foundation in place, you can now Evaluate your options like a portfolio manager. The choice between a tax-advantaged Rürup-Rente and a flexible global ETF portfolio is no longer a mystery, but a business decision based on a clear matrix: immediate tax efficiency versus long-term liquidity; state-subsidized security versus global control.

Finally, and most critically, you learned to Integrate your German assets into your worldwide financial picture. Your financial life does not respect national borders, and neither should your strategy. Understanding pension refunds and Totalization Agreements turns your German contributions from a sunk cost into a portable component of a broader plan.

You now have the framework and the decision rules. The system may still be complex, but it is no longer undefined.

Frequently Asked Questions

Is the German state pension mandatory for freelancers?

Generally, no. Most freelancers are not automatically required to pay into the state pension. However, some professions such as teachers, coaches, midwives, tradespeople, artists, and publicists are likely required to contribute, and eligible creatives are typically brought into the system through the KSK.

Can I get my German pension contributions back if I leave Germany?

Yes, in some cases. A refund is generally available to citizens of non-EU/EEA countries who live outside the EU/EEA, contributed for less than 60 months, and have waited at least 24 months since their last contribution. If you cross the 60-month threshold, you are generally locked into the German system instead.

Is the Rürup-Rente a good investment for expats?

It can be, but mainly as a trade-off. Its main benefit is significant tax deductibility, but the money is locked until retirement and must be paid as a lifelong annuity. For globally mobile professionals who value liquidity and control, a global ETF portfolio may be more attractive.

How does the German pension system work for US citizens?

For US citizens, the key protection is the US-Germany Social Security Agreement. It helps prevent double taxation by determining whether you pay into the US or German system. It can also let German contribution years count toward eligibility for US Social Security benefits.

What is the KSK (*Künstlersozialkasse*) and do I have to join?

The KSK is the artists' social insurance fund, not an insurer itself. It treats eligible creative freelancers like employees for social security purposes and pays half of their health and state pension contributions. For eligible professions, membership is mandatory.

Can a self-employed person in Germany use the Riester-Rente?

Usually not directly. Riester is mainly designed for employees, but a self-employed person can qualify if their profession requires state pension contributions, such as through the KSK. A freelancer may also be indirectly eligible through a spouse with a Riester contract.

What are the maximum tax-deductible contributions for the Rürup-Rente?

For 2025, 100% of contributions are deductible up to €29,344 for an individual. For a married couple filing jointly, the maximum is €58,688. The article presents this as one of the Rürup plan's strongest advantages for peak earning years.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Germany Freelance Tax Decisions for Globally Mobile Consultants

Set your German tax position first, then register and file. If you are a globally mobile consultant, a lower-risk approach is a clear decision order, not a tax shortcut.