Quick Answer

Choose your domicile first and make every record support it. Start with one state path, then complete licensing and vehicle updates before changing banks and client paperwork. Keep proof items such as a South Dakota overnight receipt and residency affidavit when applicable, and file IRS Form 8822 so federal records match. Align contracts, invoices, and Form W-9 naming with the same legal identity, then run a three-layer internet plan for work delivery: primary, failover, and same-day fallback.

Your First Move Isn't Buying an RV - It's Establishing a Bulletproof Legal & Tax Foundation#

Before you compare rigs, choose your domicile and make it provable. This comes first because a cheap setup can get expensive fast when your license, vehicle records, banking profile, and client paperwork do not match.

Your goal is not to be "audit-proof." It is to show clear intent, consistent records, and one credible home-base story. If a state agency, bank, insurer, or payment platform asks questions, all of your records should point the same way.

Pick the state you can actually maintain#

If you're choosing among South Dakota, Texas, and Florida, pick the state you can set up cleanly and stay compliant with, not the one with the best marketing pitch.

| State | Setup friction | Ongoing compliance burden | Vehicle and business admin realities | Audit defensibility signals |

|---|---|---|---|---|

| South Dakota | Documented traveler path. Licensing can require proof of one in-state overnight stay within the last year. If you use mail forwarding, you must complete a residency affidavit. | Verify current renewal and registration requirements. | Verify current vehicle fees and entity filing requirements. | Strong when you keep the overnight receipt and affidavit. The affidavit includes perjury language with penalties of 2 years imprisonment and $4000 fine. |

| Texas | Higher licensing friction. You must present two printed residency documents, and one generally must show at least 30 days of Texas residence. | Since Jan. 1, 2025, most non-commercial vehicles no longer need a safety inspection before registration, but emissions testing still applies in emissions counties. Non-commercial vehicles also face a $7.50 inspection program replacement fee, with $16.75 for certain newly purchased unregistered vehicles covering two years. | Viable if you can reliably produce printed residency proof and confirm county emissions impact before committing. Verify current business filing requirements. | Stronger when residency documents, license, vehicle records, and client-facing address match exactly. |

| Florida | Moderate setup burden. Class E licensing requires two different Florida residential-address documents, and out-of-state addresses are not accepted for this credential. Filing a Declaration of Domicile supports intent. | Vehicles brought in with out-of-state registration are generally required to be registered within 10 days after residency, employment, or school triggers. | Setup is paperwork-sensitive. Confirm document acceptability before you travel for appointments. Verify current entity filing requirements and fees. | Stronger when Declaration of Domicile, license file, vehicle registration, and mailing history all point to Florida. |

South Dakota has a documented traveler path in its public requirements. If you choose Texas or Florida, do not assume mail forwarding alone will satisfy residency proof.

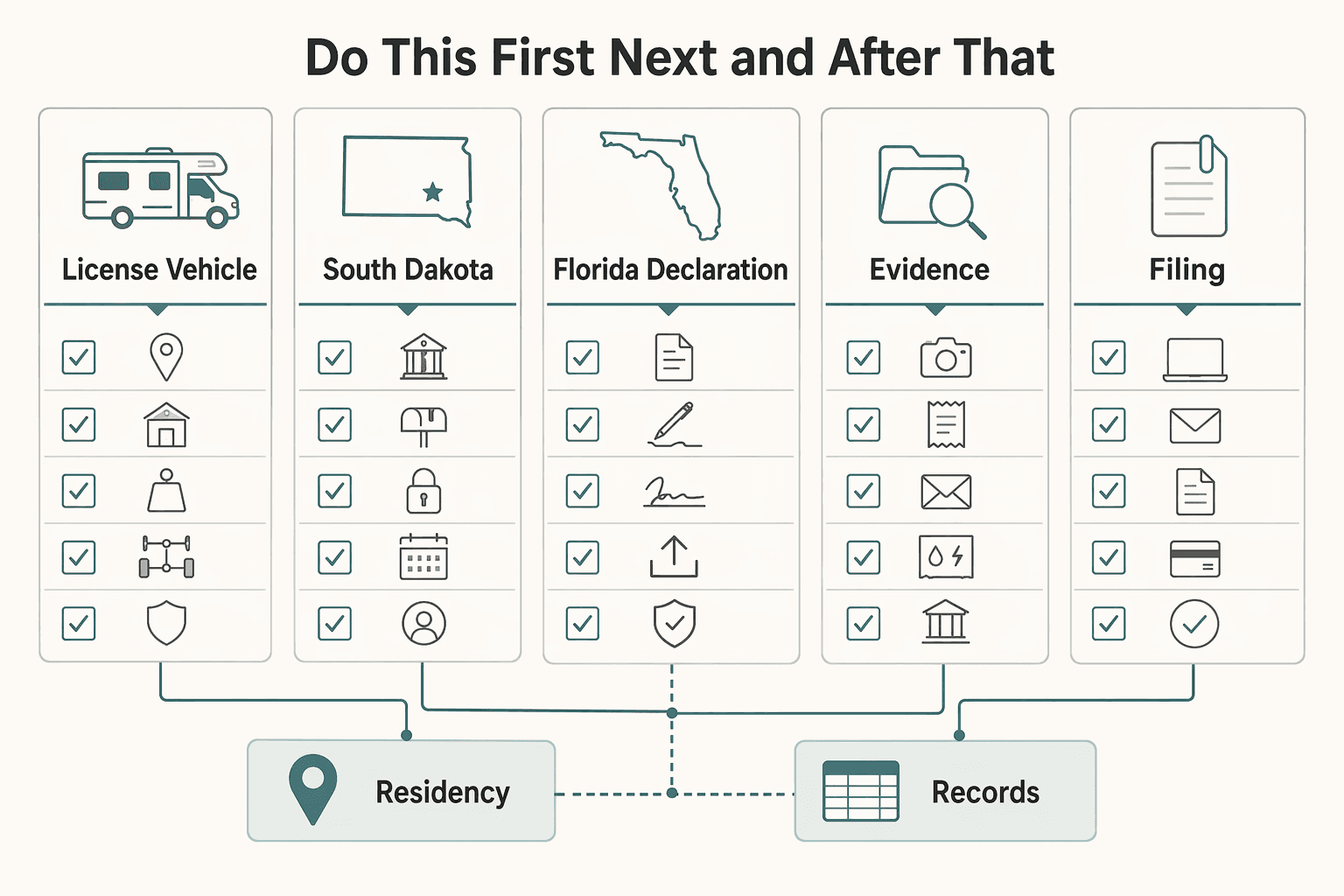

Do this first, next, and after that#

Once you choose a state, sequence matters. A clean setup is easier than fixing mismatched records later, especially if you update banks, insurers, and business records out of order.

| Step | Action | Detail |

|---|---|---|

| 1 | Choose one state | Verify current licensing and registration requirements directly before booking travel |

| 2 | Build the proof path | Use the proof path that state accepts |

| 3 | Complete identity and licensing steps | Then file supporting domicile paperwork where relevant |

| 4 | Register vehicles | Do it on that state's timeline |

| 5 | Update federal and financial records | Use the same address, including IRS Form 8822 |

| 6 | Align business records | Do this after personal records are consistent, using the same legal name and address |

Before each submission, check your legal name, address format, and unit details line by line. Small formatting mismatches can trigger manual review.

Keep an evidence file you can pull quickly if a bank, insurer, or state agency asks how the address was established:

- License and vehicle registration copies

- South Dakota overnight receipt and residency affidavit, if applicable

- Florida Declaration of Domicile, if applicable

- Texas printed residency documents used, if applicable

- IRS Form 8822 copy or filing confirmation

- Address-change confirmations from bank, insurer, and payment processor

Make your entity, contracts, and payouts say the same thing#

Your legal setup only helps if your business records tell the same story. If you operate as a sole proprietorship, there is no separate legal entity between you and the business. An LLC can improve separation of business liabilities from personal assets, but only if you keep real operational separation: separate bank accounts, separate cards, and no commingling of funds.

For a single-member LLC, default federal income-tax treatment is disregarded entity status. On Form W-9, the owner name goes on line 1 and the business or disregarded entity name goes on line 2. If your contracts, invoices, payout profiles, and W-9 naming do not line up, payment delays and review friction are more likely.

Set clear boundaries for payment disputes too. Card-paid transactions are generally reported on Form 1099-K by the payment settlement entity, not on Form 1099-NEC or 1099-MISC from the client. For billing errors on credit cards, Regulation Z uses a written-notice process with a 60-day notice window and a 30-day acknowledgment timeline. Resolution must happen within two complete billing cycles, no later than 90 days. If card disputes are common in your client mix, read this with Should Your Freelance Business Accept Credit Cards?.

Use one legal entity name, one tax-identity path, and one dedicated business banking setup from day one. That consistency makes the finance plan in the next section work for cashflow instead of against it.

Building Your Resilient Mobile Headquarters#

Your mobile HQ should fail gracefully, not suddenly. On a budget, that can mean giving every stop three layers: a primary link, a failover link, and a fallback you can use the same day if conditions change.

Working on the road can be more challenging than working from home because the weak points are predictable: spotty coverage for calls, uneven work environments, and power limits. A resilient setup comes less from expensive gear and more from clear switching rules.

Use a stop-by-stop connectivity decision flow#

Every stop deserves a quick go/no-go check before you commit to meetings or delivery windows. That check tells you whether to stay put, switch links, or move the work session entirely.

Your primary link is the default for normal work. Keep using it only if it stays stable through real tasks like client tools, file delivery, and meeting prep.

Your failover link is the second path. Switch as soon as you see repeated drops, lag, or app instability instead of waiting for a full outage.

Your fallback location is for deadline work when both main links are not trustworthy. In practice, this is often a public location with internet. Libraries are often quieter than coffee shops for focused work, but they are usually not ideal for calls unless you can use a private room or step outside.

Use the pattern this way and switch early instead of hoping a weak connection will recover in time:

- Stay on primary when it passes a real workload test.

- Move to failover at the first warning signs.

- Use fallback for invoicing, file handoff, or time-sensitive client work when reliability drops.

| Connectivity pattern | Reliability risk | Setup complexity | Recurring cost pressure | Fit for client-facing work |

|---|---|---|---|---|

| Single-link setup | Higher risk when local signal is weak or congested | Low | Lower | Works for lighter async work; higher risk for important calls |

| Two-link setup | Lower single-point risk because you have a second path | Moderate | Moderate | Better when meetings and deliveries directly affect revenue |

| Mixed-path setup | Lower single-point risk, but still depends on local conditions and setup quality | Higher | Higher | Better fit when you regularly work from remote stops and need recovery options |

No stack is universally best. Choose based on how costly a dropped call or delayed delivery is for your work, and how often you actually work from weak-signal stops.

Size power around your workday, not around the brochure#

Power planning should start with your actual workload, then size solar, battery, and inverter as one chain. If you guess from marketing claims instead, weak points can show up fast on real workdays.

Build a device map for the work-critical gear you run every day, for example laptop, monitor, router, hotspot, lighting, and audio gear. For each item, track:

- Rated watts or charger output: verify from the device label or spec sheet

- Hours used per day: your current workday estimate

- Daily energy use (Wh): watts x hours

Add those values for a rough daily demand, then validate them after a few real workdays. Small always-on loads and charging losses can be easy to underestimate.

Then size the system as a chain so each part supports the others:

- Battery: enough usable energy for your daily demand plus margin for poor charging days.

- Solar: enough recharge potential for your typical travel and camping pattern.

- Inverter: enough capacity for what runs at the same time, not just one device in isolation.

Keep one worksheet and update it after your first week, and again after any stretch with limited charging conditions. That is often when the first estimate gets corrected.

Protect payments and client data with minimum remote-work controls#

Use a simple, repeatable baseline: keep devices updated, use encryption where available, require strong unique passwords, and enable multi-factor authentication on email, invoicing, banking, and payment accounts.

Use a VPN as part of your public-network policy, especially on fallback connections, but do not treat a VPN alone as complete protection.

Set one backup communication path before you need it. If your main connection fails, you should still be able to send a fast client update with a clear reconnect window.

Keep client continuity boring#

To clients, predictable execution often matters more than perfect conditions. Use this pre-call continuity checklist so you are not making last-minute decisions when signal or power starts slipping:

- Confirm time zone and include the zone name in scheduling messages.

- Test your planned connection and your backup path.

- Verify charge status for all work devices before the meeting window.

- Check audio environment and camera framing.

- If the signal is unstable, notify the client early and switch location before the call starts.

When a stop is shaky, switch first and explain briefly. What matters is that the meeting or handoff still happens, not that you stayed on the original plan.

For a step-by-step walkthrough, see Set Up a Home Video Studio on a Budget That Stays Reliable.

The Strategic Financial Plan: From Budgeting to Corporate Cash Flow Management#

Once your connectivity and power can survive a bad stop, cashflow becomes the next likely failure point. Treat the rig as an operating asset and your client payments as working capital, not as a travel allowance.

Model the rig as cashflow, not "monthly savings"#

A rent-versus-RV-payment comparison is too shallow to guide a real decision. Build a cashflow projection that separates fixed costs, variable costs, depreciation, and revenue risk so you can see the effect on both monthly liquidity and delivery stability.

Use this template with verified numbers from your own contracts, statements, and revenue history. The point is to compare your real cash movement, not a generic RV budget:

| Cost view | Stationary setup | Mobile setup | What to verify |

|---|---|---|---|

| Fixed costs | Rent, office, storage, insurance, or other fixed monthly costs | Loan or cash allocation, RV insurance, storage, software, or other fixed mobile costs | Signed lease, policy docs, loan statement |

| Variable costs | Utilities, commute, parking, or other variable costs | Fuel, campground fees, maintenance, connectivity, power, or other variable mobile costs | 3-month average, not one favorable month |

| Depreciation | Current furniture or equipment resale exposure, if relevant | Current RV depreciation estimate pending market verification | Do not assume a universal RV depreciation rate |

| Revenue risk | Current setup risk level pending your downtime review | Mobile setup risk level pending your downtime history | Missed days, rescheduled calls, weak-signal stops |

| Net monthly cashflow view | Income minus all monthly cash outflows | Income minus all monthly cash outflows | Review with reserve balances |

Keep tax tracking separate from cash budgeting. Starting Jan. 1, 2026, the IRS optional business standard mileage rate is 72.5 cents per mile for business use. It can support deductible vehicle operating costs, but it does not show what left your account this month.

Build reserves around downtime, not around optimism#

The practical reserve question is not whether something will go wrong, but how fast it will hit your cash. An emergency fund is cash for unplanned expenses, and experts often recommend 3 to 6 months of essential expenses. For mobile work, split that reserve into clear buckets:

| Bucket | Purpose | Examples |

|---|---|---|

| Maintenance reserve | Expected wear and planned service | Routine service, known upcoming repairs |

| Emergency liquidity | Operational shocks | Breakdowns, urgent lodging, replacement connectivity gear, medical travel |

| Discretionary spend | Nonessential travel and upgrades | Nicer campgrounds, upgrades, nonessential gear, extra travel days |

Use one hard trigger rule. If you tap emergency liquidity, or if available cash drops below one month of essential business and living spend, pause discretionary spend and nonessential travel until reserves recover.

Protect incoming cash before it becomes a collections problem#

Late payment is not just an annoyance on the road. It is an operations problem, because delays can land at the same time as fuel, site, and repair bills. Customer payments are the primary cash source for small businesses, and Federal Reserve research reports roughly four of every five firms face payment-related challenges.

Set terms to reduce exposure early, before a client delay turns into a cash squeeze:

- Use deposit or milestone billing for multi-week work or reserved travel windows.

- If a client requires full payment only at final delivery, reduce scope, shorten delivery windows, or decline the work.

- Keep a payment-method mix: account for card-fee drag, around 2 to 3%, and possible settlement or fund-availability delays from third parties.

- For larger invoices, compare ACH or bank transfer versus card convenience using your own timing and fee data. See Should Your Freelance Business Accept Credit Cards?.

- Keep a dispute or chargeback buffer so one contested payment does not force late bills elsewhere.

Use a written late-payment process so you are not improvising under pressure: due-date reminder, second notice after your stated grace period, work pause, final demand. For each invoice, keep a dispute file with signed scope, dated invoice, proof of delivery, approval email, and message history.

Review your own card statements quickly, too. If you need to send a billing-error notice, Regulation Z requires creditor receipt within 60 days. Acknowledgment is generally required within 30 days unless resolved sooner.

Check coverage gaps before they become cash gaps#

Insurance is only useful here if you can tie each policy to a cashflow risk. Keep your coverage stack, but test each policy against a real loss scenario:

| Coverage | Grounded detail | Business risk | What to verify |

|---|---|---|---|

| Full-time RV coverage | Typically relevant if you live in the RV more than six months a year; optional protections can include liability, medical payments, and loss assessment | Residence-related losses that spill into operating cash | Current coverage benchmark pending provider verification. |

| Health plan | Usable out-of-area access | One medical event forcing large out-of-network costs or travel disruption | Current coverage benchmark pending provider verification. |

| Business liability or professional liability coverage | If your work creates client-claim exposure | Negligence, service disputes, or damage claims your RV policy may not cover | Current coverage benchmark pending provider verification. |

Practical test: pull each declaration page and ask, "What exact cash loss hits you if this happens next week?" If you cannot answer that clearly, treat it as an open gap.

Related: How to Create a Business Budget for Your Freelance Business.

Before you lock your payment stack, run your real client mix through a payment fee comparison tool. Your RV budget should reflect net cash, not headline rates.

Conclusion: You Are Now the CEO of a Resilient Mobile Enterprise#

The budget-friendly version of full-time RV life works best when you run it like a business, not a series of guesses. Keep three disciplines active at the same time: a documented planning checklist, reliable connectivity backups, and cashflow discipline for uneven income and surprise costs.

That is the difference between reactive travel and risk-first operations. You verify key constraints before each move, track the costs that affect your plan, and avoid building workdays on assumptions like "the campground probably has WiFi."

| Area | Reactive budget RVing | Risk-first mobile enterprise |

|---|---|---|

| Decision quality | Picks stops mostly on price or convenience | Picks stops after checking coverage, fees, work fit, and backup options |

| Income stability | Treats late payments and uneven months as surprises | Plans around invoice timing, reserves, and payment terms |

| Disruption handling | Reacts when weather, repairs, or signal issues happen | Uses fallback connectivity, known site costs, and a cold-weather trigger |

Week to week, the routine is simple. Before each move, confirm connectivity, fees, and weather exposure for the next stop. For example, Black Diamond Mines Regional Preserve states that public WiFi is not available and tells visitors to enable the "No Data Coverage Areas" map layer before relying on service. The preserve lists a $5 per vehicle fee when the kiosk is attended, so costs still need to be confirmed in advance.

Keep your weather trigger practical, too. If forecasts are trending below 32°F (0°C) for more than 2-4 hours, review your cold-weather plan early instead of waiting for the first freeze. That timing comes from storage-focused guidance, so treat it as a prompt to plan early, not as a universal rule for every full-time setup.

For your next planning cycle, focus on a few checks you can repeat:

- Review your planning checklist for gaps or stale details.

- Pre-check upcoming work stops for coverage, backup options, and known fees.

- Update your cash calendar for invoices, reserves, and repair capacity.

- Tighten your rules with The Best Budgeting Methods for People with Irregular Income and your payment-method policy in Should Your Freelance Business Accept Credit Cards?.

If you want a deeper dive, read The Best RVs and Campervans for Digital Nomads.

If you want a steadier get-paid workflow while you travel, see how Gruv handles freelancer invoicing and payout operations with clear status visibility in Merchant of Record for freelancers.

Frequently Asked Questions

How should you handle domicile as a full-time RVer?

Treat domicile as a compliance decision and verify current state rules directly before making changes. Because full-time RV living means using your RV as your permanent home, plan carefully but avoid guessing on legal or tax details this section cannot validate. If a rule is unclear, verify it from official state records before using it in your plan.

What is the practical way to think about internet reliability?

Treat connectivity as an operations risk. This article does not establish specific speed, uptime, or equipment requirements, so verify options for each stop during your actual working hours and keep a backup path. Add a connection check to each stop in your mobile ops routine.

What hidden costs matter most in full-time rving on a budget?

The main risk is copying someone else's budget as if it were a rule. Major RV costs are flexible, and there is no single exact budget for everyone, so your first checkpoint should be tracking your current spending before turning it into road assumptions. Treat headline examples like "$1600/month" as anecdotes, not targets.

How should you choose a rig without overspending?

Choose based on your own operating needs and total budget fit, and verify condition and maintenance records before you commit. This article does not provide universal rig-selection rules.

Are RV memberships worth it?

Maybe, but only after you verify current pricing, cancellation terms, location coverage, and booking constraints. Read recommendations carefully because some RV content includes affiliate links. Add memberships to your budget only after confirming they fit your actual travel pattern.

How do you protect payments while working on the road?

Start with clear terms and complete records for each invoice, then confirm your provider's current fee, funding, and dispute requirements before you standardize the process. Provider-specific fees, funding windows, and dispute timelines must be verified from current processor records before use. Then align your invoice workflow with your financial plan and review Should Your Freelance Business Accept Credit Cards?.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/an-essential-guide-to-building-an-emergency-...trusted

- consumerfinance.gov/rules-policy/regulations/1026/13trusted

- dps.texas.gov/news/vehicle-safety-inspection-changes-take-...trusted

- dps.texas.gov/section/driver-license/texas-residency-requi...trusted

- ecfr.gov/current/title-12/chapter-X/part-1026/subpart...trusted

- flhsmv.gov/driver-licenses-id-cards/what-to-bring/u-s-c...trusted

- flhsmv.gov/motor-vehicles-tags-titles/license-plates-re...trusted

- govinfo.gov/content/pkg/CHRG-114hhrg25209/html/CHRG-114h...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

The Best RVs and Campervans for Digital Nomads

If you're searching for the **best rvs for digital nomads**, do not start with brand hype or dealer roundups. Start with your workday. The wrong layout will cost you every day, even if the rig looks great on the lot.

The Best Budgeting Methods for People with Irregular Income

Budgeting with irregular income works better when you separate "money arriving" from "money you're allowed to spend," then run the same transfer routine each cycle.