Quick Answer

Start by treating a form d exempt offering as a verification exercise, not an approval signal. Pull the filing in EDGAR, compare it with the term sheet and subscription documents, and ask founders to back key claims with specific records. Focus on consistency in issuer details, exemption type, dates, valuation support, and use of proceeds. Then decide proceed, pause, or pass based on evidence quality, unresolved risks, and whether liquidity constraints fit your timeline.

What Does a Form D Filing Really Mean for You as an Investor?#

A Form D exempt offering tells you one important thing and not much more: the company says it is selling securities under an exemption. It does not mean the SEC approved the deal, reviewed the merits, or checked whether it is a good investment.

That distinction matters because "filed with the SEC" sounds more reassuring than it is. It does not mean screened or endorsed. SEC staff does not take action on Form D filings, so the filing tells you the issuer is claiming an exemption under Regulation D, not that the terms are fair, the valuation is sensible, or the business is sound.

What the filing does and does not tell you#

A Form D is still useful because it gives you a concrete starting point. You can see the issuer's identity, contact information, related persons, the exemption claimed, the amount being offered, the amount already sold, and the minimum investment amount. Those fields let you test whether the story in the pitch deck matches what the company told the SEC.

What you do not get is the disclosure package you would expect in a registered public offering. In a registered deal, the prospectus must describe the business, financial condition, results of operations, risk factors, and management, and it must include audited financial statements. In a private placement, you generally get fewer disclosure-based protections, so your diligence burden goes up, not down.

| Point of comparison | Form D filing | Registered public offering |

|---|---|---|

| Review level | Notice filing only; not SEC approval or merit review | Registration statement filed with the SEC |

| Disclosure depth | Limited notice information | Prospectus plus broader filed information |

| Investor protections | Fewer disclosure-based protections | More formal disclosure requirements |

| Liquidity expectations | Often limited; transfer and sale restrictions may apply | Not established by Form D; evaluate liquidity from offering terms and market realities |

| Your due diligence burden | High; you must verify facts and ask for supporting documents | Still important, but more information is publicly required |

Accredited-investor status is part of this picture, but do not confuse eligibility with safety. Under Rule 501(a), an investor qualifies as accredited only if they meet the applicable standards. That status does not reduce business risk, fraud risk, or liquidity risk. Early-stage investing is still high risk, and under Rule 506(c), all purchasers must be accredited and the issuer must verify that status.

Your first EDGAR check#

Before you read a deck twice or join a founder call, pull the filing from EDGAR. Form D filings are public there, including accession numbers. Check these items first:

| Check | What to verify | Follow-up |

|---|---|---|

| Issuer identity and contact details | Company name and legal address match the subscription documents, website, and email domain you received | If the names do not line up with the materials you were sent, that is a real red flag |

| Related persons | Founders, executives, directors, or promoters listed on the filing | If key people pitching you are missing, ask why |

| Exemption claimed | Confirm the offering type the company says it is relying on | Test whether the story in the pitch deck matches what the company told the SEC |

| Offering and sales amounts | Compare the total amount offered, amount sold, and minimum investment against the deck and term sheet | If the amount sold or minimum investment do not line up, that is a real red flag |

| Date of first sale | Form D is generally due within 15 days after the first sale | If the dates look off, ask for an explanation |

| Amendments | If the offering has continued for more than 12 months, or material facts changed, look for an amendment | Material errors should have been corrected promptly through an amended filing |

- Issuer identity and contact details: company name, legal address, and whether they match the subscription documents, website, and email domain you received.

- Related persons: founders, executives, directors, or promoters listed on the filing. If key people pitching you are missing, ask why.

- Exemption claimed: confirm the offering type the company says it is relying on.

- Offering and sales amounts: compare the total amount offered, amount sold, and minimum investment against the deck and term sheet.

- Date of first sale: Form D is generally due within 15 days after the first sale, meaning the date the first investor became irrevocably contractually committed. If the dates look off, ask for an explanation.

- Amendments: if the offering has continued for more than 12 months, or material facts changed, look for an amendment.

The failure mode here is not just "no filing found." Sometimes the filing exists, but the names, amount sold, or minimum investment do not line up with the materials you were sent. That is a real red flag. So is a company brushing off material errors that should have been corrected promptly through an amended filing.

A clean filing is a useful checkpoint, not a finish line. It tells you where to focus next: the people involved, the legal exemption claimed, the fundraising timeline, and the numbers you now need the company to support with documents.

If you want a deeper dive, read Taxes in Germany for Freelancers and Expats.

The 'Exempt' Red Flag: Three Hidden Risks You Must Understand#

In a form d exempt offering, the key shift is practical: the issuer can rely on an exemption instead of full registration, so more verification work moves to you. Focus on three risks first: information asymmetry, limited regulatory review, and uncertain liquidity.

| Risk | What public-market investors usually get | What you may not get here | What you should verify next |

|---|---|---|---|

| Information asymmetry | More standardized public disclosure | Mainly the materials the issuer chooses to provide | How detailed the financial reporting is, what assumptions drive projections, and whether the deck, subscription documents, and Form D stay consistent |

| Limited regulatory review | A full registration pathway before sale | Exempt-offering pathway with fewer registration-layer checks | Which exemption is claimed, whether the sales approach matches it, and whether the deal facts match the filing |

| Illiquidity | A clearer resale path in active public markets | A predictable way to sell on your timeline | Transfer limits, any repurchase terms, and what realistic event could create liquidity |

Information asymmetry: Start by testing consistency, not storytelling. If numbers, assumptions, or offering terms shift across documents, treat that as a diligence issue you need resolved before moving forward.

Limited regulatory review: Match behavior to the exemption. If the issuer says Rule 506(b), broad public advertising should raise questions; if it says Rule 506(c), investor accreditation verification should be a visible part of the process.

Illiquidity: Assume exit is uncertain unless the documents clearly show otherwise. Confirm what rights you actually have and what concrete trigger, if any, could convert your position to cash.

Related: What are 'Blue Sky Laws' and How Do They Affect Startups Raising Capital?.

Your Due Diligence Playbook: How to Vet a Form D Offering Like a Pro#

Use a verification-first workflow: confirm the record, vet the people, test the documents, then pressure-test the terms.

| Area | What the issuer says | What you independently verify |

|---|---|---|

| EDGAR details | The offering is filed correctly under an exemption | The filing record is present, core issuer details match across materials, and key deal details are consistent |

| Management background | The team has the right track record | Public history is consistent with the bios and offering narrative, with no unresolved contradictions |

| PPM claims | The business case is strong and risks are manageable | Assumptions are explicit, risks are specific, conflicts are clearly disclosed, and terms are consistent across the deck, PPM, and subscription documents |

| Use-of-proceeds narrative | Capital will be used for growth | Spending use is concrete, ties to milestones, and does not conflict with the rest of the packet |

Step 1: Verify the filing record. Pull the filing record yourself and reconcile it against the full investor packet. If you rely on Federal Register material during legal verification, do not treat FederalRegister.gov XML as legally sufficient on its own; capture the linked official PDF on govinfo.gov. Also treat the SEC consolidated CFI page as a pointer, not a final authority, and click through to current CFI pages. Output: verified filing record plus a mismatch log.

Step 2: Diligence the people. Use the names in the filing as your anchor, then test whether public history supports the issuer's narrative. When titles, timelines, or claims conflict across sources, treat that as unresolved risk until clarified. Output: short management risk memo with open questions.

Step 3: Review the PPM as a consistency test. Focus on four checks: business-model assumptions, risk disclosure quality, conflict disclosures, and cross-document consistency (deck vs. PPM vs. subscription documents). Keep a separate note for publicity risk, since communications tied to an offering can be treated as an offer under securities-law framing, and exempt offerings still have restrictions. Output: document-consistency memo with ranked red flags.

Step 4: Diligence terms before you underwrite upside. Confirm security type, preference waterfall position, dilution mechanics, transfer limits, and governance rights from controlling documents, not summaries. Insert verified legal/timing specifics only after counsel or primary-source confirmation: [filing timeline placeholder], [voting threshold placeholder], [transfer restriction placeholder], [preference term placeholder]. Output: decision checkpoint stating whether your rights, subordination risk, and liquidity constraints are clear.

Use this triage before founder Q&A:

- Pass: records and documents align, management checks are coherent, and buyer rights are clear.

- Pause: missing documents, unclear proceeds narrative, or unresolved inconsistencies.

- Fail: material conflicts between selling behavior and claimed exemption path, undisclosed conflicts, or controlling terms that contradict the pitch.

You might also find this useful: How to Price AI-Assisted Freelance Services.

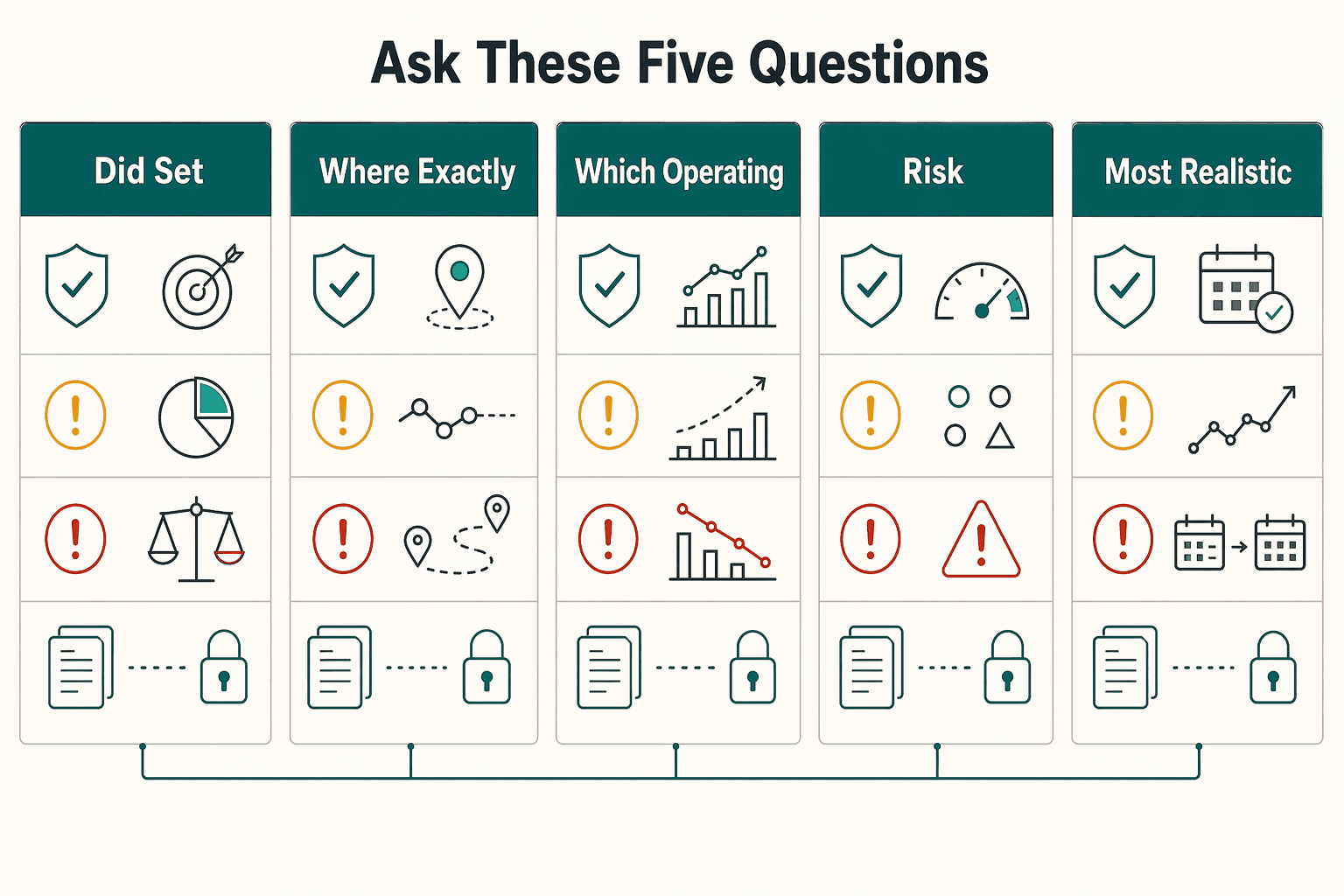

The Five Critical Questions to Ask the Founder Before You Invest#

After your document review, use the founder call to test whether each key claim is specific, consistent, and verifiable.

Use one claim-to-evidence check on every material answer#

Ask: "What document or data point should I review to confirm that?" If securities were issued in California, check state filing status directly: securities issued in California must be exempted or qualified. If the issuer says it relied on California Corporations Code section 25102(f), ask for the Limited Offering Exemption Notice (LOEN) and filing confirmation from the DFPI Self-Service FRANSES Portal. Also confirm they understand the LOEN fee is based on the total offering value, not just the California portion.

| California check | What to confirm | Follow-up |

|---|---|---|

| State filing status | Securities issued in California must be exempted or qualified | Check state filing status directly |

| Section 25102(f) reliance | If the issuer says it relied on California Corporations Code section 25102(f), ask for the Limited Offering Exemption Notice (LOEN) | Ask for filing confirmation from the DFPI Self-Service FRANSES Portal |

| LOEN fee basis | The LOEN fee is based on the total offering value, not just the California portion | Confirm they understand the fee basis |

Ask these five questions#

| Question | Claim-to-evidence | Red flag |

|---|---|---|

| How did you set this valuation, and what has to be true for it to hold up? | Term sheet, cap table, prior financing docs, pricing support materials | Valuation story conflicts with ownership structure or deal terms |

| Where exactly will this round be spent, and what milestone does each major spend category fund? | Use-of-proceeds schedule, budget, hiring plan, debt obligations, PPM disclosures | Use-of-proceeds changes across call, deck, and signing documents |

| Which operating numbers do you track most closely, and what decisions changed because of them? | KPI reports, board updates, pipeline/cohort reports, financial package | Cited numbers do not appear in investor or management reporting |

| What are the biggest current risks, and what mitigation is already in motion? | Risk disclosures, legal/contract disclosures, concentration data, state notice records (including LOEN if relying on 25102(f) in California) | "No major risks," or compliance claims without records |

| What is the most realistic path to investor liquidity, and what must happen first? | Investor materials, capitalization documents, governing documents, transfer restrictions, subscription agreement | Liquidity framed as routine or near-certain regardless of restrictions |

- How did you set this valuation, and what has to be true for it to hold up?

Credible: clear method, core assumptions, and alignment with the rights investors are buying. Incomplete: broad market language without a bridge to business performance or dilution. Red flag: valuation story conflicts with ownership structure or deal terms. Claim-to-evidence: term sheet, cap table, prior financing docs, pricing support materials.

- Where exactly will this round be spent, and what milestone does each major spend category fund?

Credible: spend categories tied to sequence and milestones. Incomplete: "growth" language without a concrete allocation path. Red flag: use-of-proceeds changes across call, deck, and signing documents. Claim-to-evidence: use-of-proceeds schedule, budget, hiring plan, debt obligations, PPM disclosures.

- Which operating numbers do you track most closely, and what decisions changed because of them?

Credible: a small set of decision-driving metrics, recent trend, and action taken. Incomplete: metrics with no operational consequence. Red flag: cited numbers do not appear in investor or management reporting. Claim-to-evidence: KPI reports, board updates, pipeline/cohort reports, financial package.

- What are the biggest current risks, and what mitigation is already in motion?

Credible: specific risks with concrete mitigation steps underway. Incomplete: generic risk language with no owner or execution detail. Red flag: "no major risks," or compliance claims without records. Claim-to-evidence: risk disclosures, legal/contract disclosures, concentration data, state notice records (including LOEN if relying on 25102(f) in California).

- What is the most realistic path to investor liquidity, and what must happen first?

Credible: plausible paths linked to business milestones and actual security terms. Incomplete: vision statements without the intermediate conditions. Red flag: liquidity framed as routine or near-certain regardless of restrictions. Claim-to-evidence: investor materials, capitalization documents, governing documents, transfer restrictions, subscription agreement.

Decision checkpoint#

- Proceed: answers are specific, document-backed, and consistent across filing and deal materials.

- Pause: key claims still need proof, especially on valuation support, use of proceeds, or California notice status.

- Pass: the narrative keeps shifting, evidence remains unavailable after follow-up, or explanations conflict with signing documents.

For a step-by-step walkthrough, see A guide to 'Form 8233' for foreign individuals receiving US scholarship or fellowship grants.

From Anxiety to Confidence#

Your confidence should come from evidence, not from how persuasive a pitch feels. When you evaluate a form d exempt offering, use the same workflow every time: verify the filing, pressure-test issuer disclosures, challenge key assumptions, and document your go/no-go rationale before you commit capital.

Start with accountability in the offering materials. In an SEC-filed offering statement, the issuer is identified as responsible for the securities information, while the platform states it did not verify adequacy, accuracy, or completeness. Treat that as a practical warning: availability is not the same as reliability. Then test the main failure points directly: valuation may be off, forward-looking statements may not play out, and the shares may be illiquid or restricted.

| Emotion-driven investing | Evidence-driven diligence | Likely outcome |

|---|---|---|

| You trust the story because the founder sounds credible | You match core claims to the filing and offering materials | Fewer surprises about who is accountable for what |

| You anchor on projected growth | You treat projections as uncertain and ask what must go right | Clearer view of execution risk |

| You focus on getting into the deal | You confirm whether you can tolerate a 5-7 year hold and restricted stock | Fewer liquidity regrets |

| You decide in the meeting | You record open risks and wait for documented answers | Cleaner proceed, pause, or pass decision |

Use this decision rule:

- Proceed when the filing is verifiable, disclosure accountability is clear, and your biggest risks are answered with documents.

- Pause when key facts are incomplete, valuation logic is thin, or the case depends mostly on forecasts.

- Pass when accountability stays unclear, answers remain vague, or liquidity risk does not fit your timeline.

Run the checklist, log unresolved risks, and only move forward once open questions are resolved.

We covered this in detail in A Guide to Form 1099-K for Freelancers Using Payment Apps.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dfpi.ca.gov/rules-enforcement/laws-and-regulations/law-a...trusted

- ecfr.gov/current/title-17/chapter-II/part-230/subject...trusted

- federalregister.gov/documents/2026/02/25/2026-03705/self-regulat...trusted

- federalregister.gov/documents/2020/03/31/2020-04799/facilitating...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- irs.gov/pub/irs-drop/td-9889.pdftrusted

- sec.gov/about/divisions-offices/division-corporation...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

How Blue Sky Laws Affect Startups Raising Capital

If you are raising money, state securities law matters from the start. For most startups, **the [blue sky laws](https://www.investor.gov/introduction-investing/investing-basics/glossary/blue-sky-laws) that matter are the state securities rules that sit alongside federal securities law**. Even if your round fits a federal exemption, states may still require notice filings, fees, and compliance with anti-fraud rules as money comes in.

How to Price AI-Assisted Freelance Services

Protect cashflow first, then optimize upside. Late-payment risk rises when scope is unclear, approval ownership is loose, and payment terms are left until late in the process.