Quick Answer

Use financial ratios for business health as a baseline, then run three operating metrics every month: True Effective Rate, Personal Runway, and Client Concentration Risk. Measure them with a consistent method so month-to-month comparisons stay reliable. Then act on the signal: keep high-quality clients, renegotiate work where hidden effort erodes returns, and reduce dependency when one client starts dominating revenue. The framework is practical because it ties each metric to a decision, not just a report.

Why Traditional Financial Ratios Fail the Business-of-One#

Before you build a better financial command center, separate what ratio analysis can do from what it cannot. Ratio analysis can extract useful insight from financial statements, and in some study contexts, financial ratios have distinguished failed and non-failed companies several years before failure. But the method has clear limits. If you ignore benchmark fit, historical inputs, or inflation effects, the conclusion can point you in the wrong direction.

| Ratio type | Best read as | Key caution |

|---|---|---|

| Activity | Useful when compared against the right industry benchmarks | Easy to misread if the benchmark group does not match the business model |

| Leverage | One view of financial structure | Misleading if treated as a full health verdict on its own |

| Profitability | A summary of reported performance | Does not explain performance completely, and historical inputs do not necessarily say much about future performance |

| Liquidity | A helpful check based on reported figures | Cross-period comparisons get weaker when inflation is not accounted for |

For a freelancer or consultant, the fit can be uneven. Ratio analysis is strongest when the benchmark group and business context are a close match. That does not make the ratios useless. It means you need to be careful about what question each one is actually answering before you use it as a decision tool.

Here is where the old toolkit tends to fall short.

- The Limits of 'Activity' Ratios: Activity-style metrics are most useful when you compare them against the right industry benchmarks. If the benchmark group does not match your business model, the ratio is easy to misread.

- The Limits of 'Leverage' Ratios: Leverage ratios can tell you something about financial structure, but they are only one part of the picture. Treating any single ratio as a full health verdict can lead to misleading conclusions.

- The Limits of 'Profitability' Ratios: Profitability ratios summarize reported performance. They do not explain it completely, and because the inputs are historical, they do not necessarily tell you much about future performance.

- The Limits of 'Liquidity' Ratios: Liquidity ratios also rely on reported figures. They can help, but cross-period comparisons get weaker when inflation is not accounted for.

The practical problem is not that these ratios are wrong. On their own, they can be too indirect for day-to-day operating decisions in some business-of-one contexts. If you want better control, pair them with measures that map more closely to how your business actually works.

Related: Is Labuan's Offshore Financial Center Right for Your Business-of-One?.

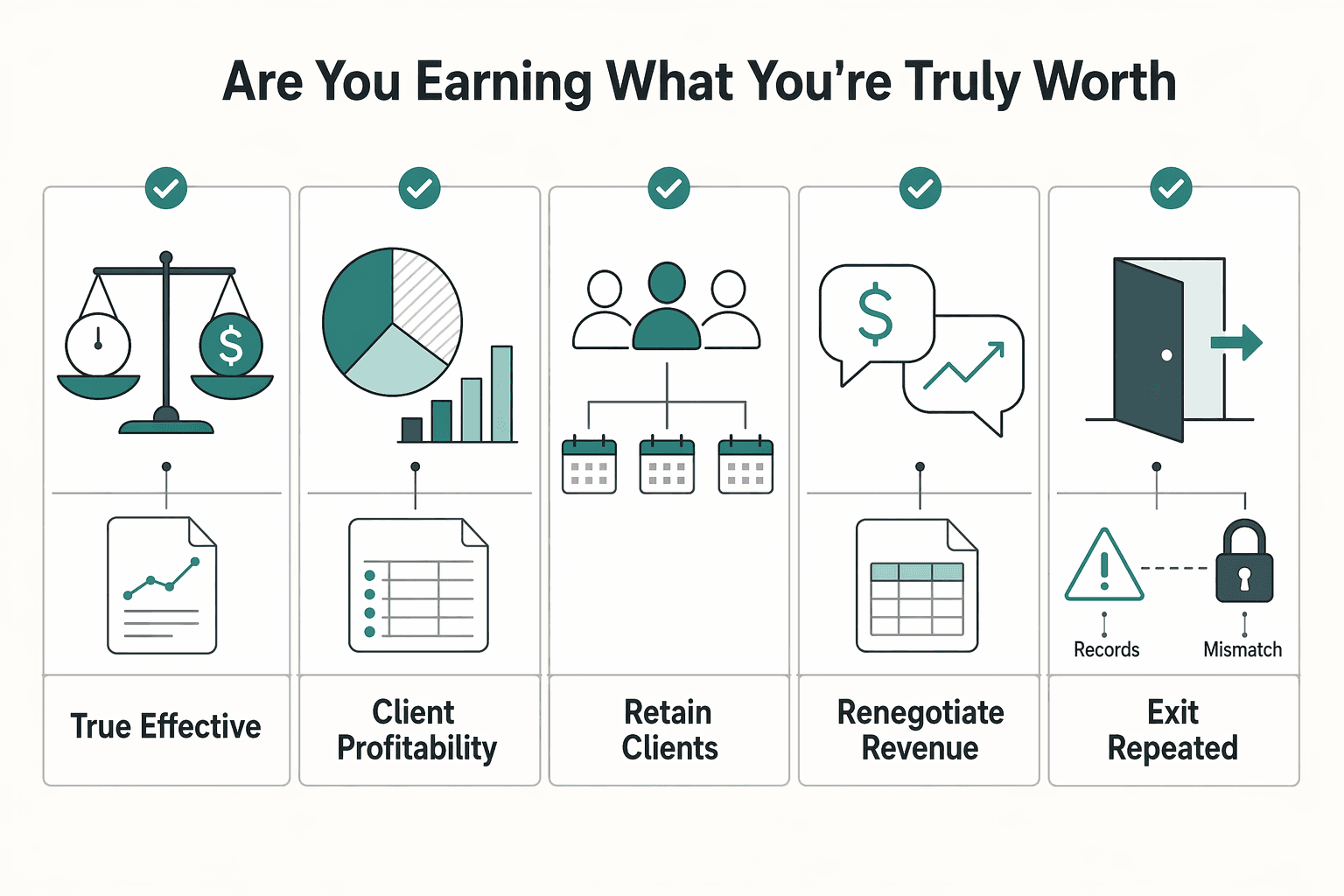

Pillar 1: Your Profit Engine: Are You Earning What You're Truly Worth?#

Once you move past generic ratio checks, start with what actually drives your business: whether your work is paying off after the hidden effort is counted. For a Business-of-One, True Effective Rate and Client Profitability Score usually tell you more than net margin alone and are often more useful than traditional ratios built for capital-intensive companies. Keep a separate eye on concentration risk too: relying on one income source for more than 50% of revenue can be precarious.

Use them this way:

- True Effective Rate: your real earning power after accounting for how your working time is actually consumed.

- Client Profitability Score: a client-level view of which engagements are truly worth keeping once hidden effort is included.

Consistency matters more than complexity. At minimum, include the work that usually gets missed: non-billable time tied to delivery, rework, and scope creep. Keep your method consistent across clients and periods so the comparison stays fair.

This is where many solo businesses lose the signal. Revenue looks healthy, but one client requires constant clarification, repeated revisions, or extra coordination that never appears on the invoice. Another client may pay a bit less on paper but runs cleanly, approves quickly, and creates almost no admin drag. If you do not capture that hidden effort, both clients can appear similar when they are not.

A practical template:

| Client | Revenue (period) | Hidden effort check (revisions/scope creep/non-billable) | Profit signal (TER/CPS) | Decision |

|---|---|---|---|---|

| Client A | Current period data | Low / medium / high | Improving / stable / declining | Retain |

| Client B | Current period data | Low / medium / high | Improving / stable / declining | Renegotiate |

| Client C | Current period data | Low / medium / high | Improving / stable / declining | Exit |

Treat the table as an operating routine, not a one-time audit:

- Retain clients with strong profit signals and manageable delivery friction.

- Renegotiate when revenue looks fine but hidden workload is eroding real profit.

- Exit when repeated renegotiation fails and the engagement keeps consuming disproportionate time and attention.

To make the routine useful, run it in the same sequence each period. Pull client revenue from the same report. Review your calendar, project tool, or time records for delivery work that was not billed directly. Note revision cycles, approval delays, and scope changes while they are still fresh. Then classify the profit signal before you decide what to do. The point is not to build a perfect model. It is to stop relying on memory after a frustrating week.

A common failure mode is letting one recent annoyance outweigh the actual pattern. Another is doing the opposite: tolerating months of low-quality work because the invoice amount looks reassuring. A repeatable review helps on both sides. You can separate a temporary issue from a persistent one and see whether the engagement is improving, stable, or declining in a way that matters operationally.

When you renegotiate, pair pricing or scope changes with operational fixes. For related operating playbooks, see Hiring Your First Subcontractor and The Best Bank Accounts for Freelancers in Germany.

It also helps to decide in advance what a renegotiation is meant to fix. Sometimes the issue is price. Sometimes it is revision limits, approval timing, or the way work gets handed off. If you know which part is causing the drag, the conversation gets more concrete and the result is easier to track next month. If nothing changes after that, the decision to exit becomes much clearer.

For a step-by-step walkthrough, see Business-of-One Financial Dashboard: Track Compliance, Profitability, and Growth.

Pillar 2: Your Resilience Shield: How Many Months of Freedom Do You Have?#

Profit tells you what the work earns. Resilience tells you how much room you have when timing goes wrong. The practical question is simple: how many months can you keep operating without lowering your standards if cash inflow slows? Track Personal Runway monthly so delayed payments, slower demand, or personal disruption do not force reactive decisions.

Calculate Personal Runway the fast way#

The material here does not verify a single official runway formula, fixed month benchmark, or universal cash-inclusion rule.

Use one documented internal method and keep it consistent every month.

Personal Runway = documented cash definition / documented monthly expense baseline

Use one statement date each month and the same inclusion rules every time. Record what you included, what you excluded, and why. Before you rely on the result, reconcile your cash total to balances on the chosen date.

That note matters more than it seems. If runway drops from one month to the next, you want to know whether the change came from real spending, delayed cash collection, a reserve transfer, or a classification mistake. A short note beside the number is usually enough. Without it, the trend gets noisy and harder to trust.

Build a reserve by use case, not by vague comfort#

A reserve works better when each layer has a job. Tie your cash buffers to specific failure modes so the plan turns into action when pressure shows up.

| Reserve layer | Decision use case | Example pressure it can cover | Where to keep it | Allocation range |

|---|---|---|---|---|

| Income-delay buffer | Keep operating when invoices land late | delayed client payments, paused projects, billing disputes | most accessible cash account | Current benchmark pending source verification |

| Demand-slowdown buffer | Protect pricing discipline when new work slows | weaker pipeline, seasonal dips, longer sales cycles | separate savings or cash reserve account | Current benchmark pending source verification |

| Personal-disruption buffer | Cover non-business shocks without draining operating cash | illness, family disruption, forced time off, urgent repairs | ring-fenced reserve separate from daily spend | Current benchmark pending source verification |

Do not treat the allocation ranges as usable until you verify a current, authoritative source. FederalRegister.gov explicitly says it is not the official legal edition, and the banking capital item in the provided excerpt is marked Proposed Rule, with a displayed comment period ending 06/18/2026. The provided CRS source also focuses on large-bank prudential regulation, not freelancer runway thresholds.

The value of the layered approach is that it tells you what to do when pressure appears. If a late-paying client hits the income-delay buffer, that does not automatically mean the business model is failing. It means cash timing needs attention. If the demand-slowdown buffer starts doing the work, that points more toward pipeline or sales-cycle pressure. If the personal-disruption buffer is being used, the response may have little to do with pricing at all. Separate buckets make the diagnosis faster.

Turn runway into payment-protection decisions#

Runway can trigger policy, not just reflection. The excerpts here do not validate one required freelancer policy, so treat the following as optional controls to test against your own data:

- renegotiate terms on new work toward earlier payment, partial upfront billing, or milestone billing

- shorten invoice cadence on ongoing work, for example by milestone or more frequent billing cycles

- apply a reserve policy that moves a fixed share of each payment into buffer before increasing owner draws

- delay new fixed-cost commitments until the buffer is rebuilt

Model cost volatility before you add delivery obligations. If subcontractor use is part of your plan, evaluate the cash impact first, then commit. Hiring Your First Subcontractor: Legal and Financial Steps is useful here.

Account structure can affect control too. Keeping reserves separate from your day-to-day spending accounts can make runway easier to verify and harder to erode. If you are revisiting setup, see The Best Bank Accounts for Freelancers in Germany.

Use a simple rule: when runway falls, tighten terms and discretionary spend. When runway rises, keep the reserve discipline anyway.

That last part is what prevents false confidence. A strong month can hide timing luck, one large payment, or a temporary workload spike. If you loosen standards every time cash improves, you lose the stabilizing effect that runway is supposed to create. The better use of a higher runway number is calmer decision-making, not faster spending.

If you want a deeper dive, read How to Get a Certificate of Residence (Form 6166) from the IRS.

Pillar 3: Your Risk Radar: Is Your Biggest Client Also Your Biggest Threat?#

A strong client can become a weak point if too much of your revenue depends on that one relationship. At its core, client concentration risk is a single exposure that can produce losses large enough to threaten operations. Track it as a standing warning light, not a one-time check.

Score it consistently or the number will lie#

Use a consistent internal method to track how dependent you are on your largest client.

The discipline matters more than any single snapshot. Keep your approach consistent over time, document your assumptions, and avoid changing your method only after you see the result.

A practical checkpoint is to review largest-client dependency from the same internal data source on a regular cadence and flag material shifts early. Most concentration blind spots come from inconsistent measurement.

It also helps to read the score alongside broader risk context. Concentration risk should be managed alongside credit, interest-rate, and liquidity risk, and downside can accelerate when a negative event hits. The score is a warning light, not the full diagnosis.

| Risk level | Concentration band | What to do |

|---|---|---|

| Lower exposure | Threshold pending advisor or business-record verification | Keep monitoring and avoid assigning new capacity to one client by default. |

| Moderate exposure | Threshold pending advisor or business-record verification | Start diversification before pricing power and negotiating room narrow. |

The score is only part of the risk picture. Too much reliance on a single client, product, or service increases downside exposure, and poor concentration-risk management has been linked to severe outcomes, including losses and failures. Operational setup matters too. If your payout flow depends on one provider, outages or security issues can amplify client risk, which is why cash-control structure matters. See The Best Bank Accounts for Freelancers in Germany.

Use a repeatable control loop: identify, measure, monitor, and control. Quantify your exposure, set concentration limits based on that analysis, review pipeline concentration on a fixed cadence, and track de-risking milestones, for example adding a second anchor client or narrowing oversized scopes. If you need added delivery capacity while diversifying, see Hiring Your First Subcontractor: Legal and Financial Steps.

In practice, de-risking usually works best when you split the response into two tracks. First, protect the current relationship by tightening scope, billing, and communication so the large client does not become even more volatile. Second, build alternatives on a separate cadence so diversification does not depend on a crisis month. If you wait until the client pauses work, you are already negotiating from a weaker position.

We covered this in detail in Choosing Functional Currency for Your Business.

If your concentration risk is above your comfort limit, use this to run a quick repricing scenario before accepting new scope: Freelance Rate Calculator.

You Are the CEO: Take Command of Your Financial Future#

This framework does more than tidy up a spreadsheet. It changes how you run the business. Traditional ratios can create noise when they are built for a model you do not actually operate. Building your own command center around Profit, Resilience, and Risk gives you a clearer basis for decisions.

This is not just semantics. It is a shift in posture. The freelancer reacts. The CEO directs.

- A freelancer worries about a slow month. The CEO uses Personal Runway to decide whether that downtime should go to new skills or business development.

- A freelancer takes on a demanding, low-margin client out of fear. The CEO checks expected profitability first and can decline work that does not support the business.

- A freelancer becomes dependent on a single large contract. The CEO monitors Client Concentration Risk and executes a diversification plan over time.

These metrics are decision tools. When you review them consistently, not just when cash feels tight or at tax time, they help replace emotionally driven guesswork with clearer choices. They can also create a record of how you make decisions, which matters when you need to compare what you expected with what actually happened. Over time, that is what turns a rough financial habit into real operating discipline.

You are not just trading time for money. You are building an enterprise designed to serve your life. This command center gives you clearer visibility into which levers to pull, which risks to take, and which opportunities to pursue. You are in command.

Related: How to Set Financial Goals for Your Freelance Business.

When you are ready to turn this checklist into a repeatable get-paid workflow, review Gruv for Freelancers.

Frequently Asked Questions

Which financial ratios are most important for a consultant or freelancer?

Use ratios alongside regular financial statement analysis so you can still spot issues like changes in liabilities or slow receivables collection. Practical action: pull the numbers from the same reports each month and document exactly what you include so the trend stays comparable. If a metric changes sharply, do not just record it. Add one short note explaining why.

How do I calculate business health for a service-based business?

Do not force business health into a single score. A more reliable view comes from ongoing financial statement analysis across your core statements, including assets, liabilities, and owners’ equity. Practical action: review your core statements on a fixed monthly cadence and investigate any movement you cannot explain from real business activity. For a structured cadence, see How to Conduct a Yearly Financial Review for Your Freelance Business. A good review process should make surprises smaller over time, not just better documented after the fact.

What is a good net profit margin for a solopreneur?

A single margin benchmark is not enough on its own. Financial ratios are comparative measures, and benchmark quality depends on source quality, industry match, and recency. Some datasets are built from IRS SOI Tax Stats and US Census Bureau inputs, and yearly estimates can be revised. Practical action: before you use any benchmark for pricing or spending decisions, log the source, date, and industry match. If the benchmark does not resemble your business model, treat it as background, not a rule.

How do I measure my financial runway as a freelancer?

The provided guidance does not support a fixed runway target. Treat runway as part of your ongoing financial review and use the same inclusion rules each month so trend comparisons stay usable. Practical action: reconcile your cash figure to current statements and document exactly what is included before making larger commitments.

What is client concentration risk and why does it matter?

The provided guidance does not support a universal concentration cutoff. Treat concentration as a dependency indicator you define consistently and track on a fixed schedule so changes are comparable over time. Practical action: include it in the same ongoing management reporting rhythm you use for other financial ratios. If you are reducing dependency by expanding delivery capacity, see Hiring Your First Subcontractor: Legal and Financial Steps. A concentration number is more useful when reviewed as part of a broader set of financial checks.

How can I use these metrics to price my services better?

Use these metrics to make pricing decisions from comparable trends, not guesswork. Practical action: before changing prices, review recent ratio trends from the same reports and log the benchmark source, date, and industry match. That keeps pricing decisions tied to tracked financial signals rather than one-off assumptions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far-overhaul/far-part-deviation-guide/far-ov...trusted

- biotech.law.lsu.edu/blog/A-Citizens-Guide-to-the-Corps-of-Engine...trusted

- clame.nyu.edu/Download_PDFS/E1C3DB/316311/How%20To%20Expla...trusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- cms.gov/Regulations-and-Guidance/Guidance/Transmitta...trusted

- congress.gov/crs-product/R47876trusted

- dmhc.ca.gov/Portals/0/Docs/OFR/Claims%20TAG_Accessible%2...trusted

- fdic.gov/resources/supervision-and-examinations/exami...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Get a Certificate of Residence (Form 6166) from the IRS

Start with purpose, not paperwork. Before anyone opens Form 8802, get clear on why the foreign payer or tax authority wants a U.S. residency certificate. That answer drives almost everything that follows: whether you should file at all, how the request should be framed, what tax period matters, and how much lead time you really need. If the reason stays vague, the rest of the process gets expensive fast.

The Best Bank Accounts for Freelancers in Germany

Pick the account that protects cashflow and keeps records clean when client behavior gets messy, not the one with the nicest app.